Europe Melanoma Cancer Diagnostics Market

Market Size in USD Billion

USD

1.55 Billion

USD

2.59 Billion

2024

2032

USD

1.55 Billion

USD

2.59 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.55 Billion | |

| USD 2.59 Billion | |

| % | |

|

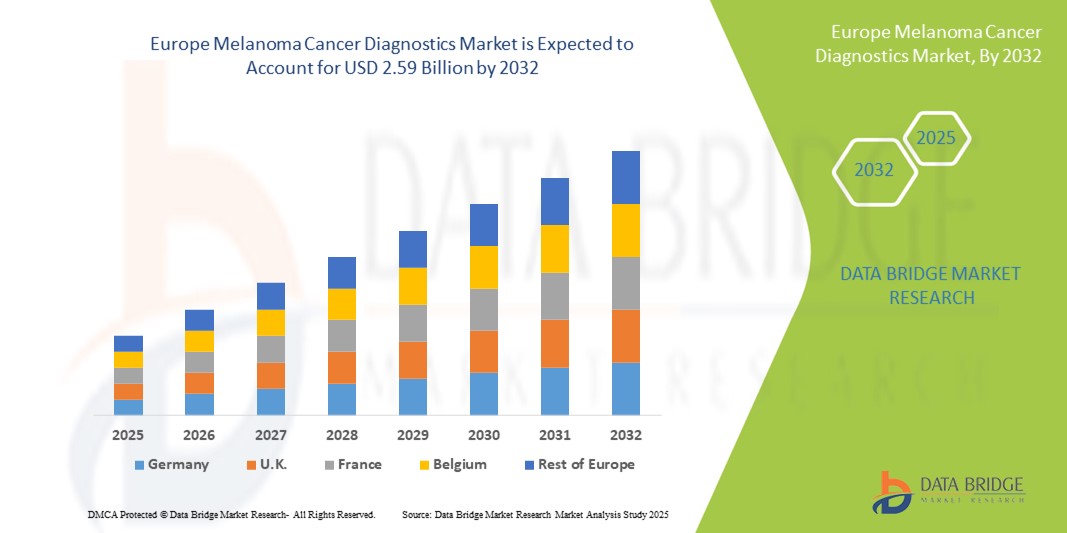

Europe Melanoma Cancer Diagnostics Market Size

- The Europe melanoma cancer diagnostics market size was valued at USD 1.55 billion in 2024 and is expected to reach USD 2.59 billion by 2032, at a CAGR of 6.6% during the forecast period

- The market growth is largely fueled by advancements in diagnostic technologies such as dermoscopy, molecular testing, and imaging techniques, along with increasing adoption of AI-assisted diagnostic tools for early detection, improving patient outcomes

- Furthermore, rising incidence of melanoma, growing public awareness about skin cancer, and supportive government initiatives for early screening and diagnostics are driving demand for effective melanoma diagnostic solutions, thereby significantly boosting the industry's growth

Europe Melanoma Cancer Diagnostics Market Analysis

- Melanoma cancer diagnostics, offering advanced tools and technologies for early detection and monitoring of skin cancer, are increasingly vital components of modern healthcare systems in both clinical and research settings due to their accuracy, efficiency, and integration with digital health platforms

- The escalating demand for melanoma diagnostics is primarily fueled by the rising incidence of melanoma in Europe, growing awareness among patients and healthcare providers, and a preference for early detection methods that improve survival rates

- Germany dominated the melanoma cancer diagnostics market with the largest revenue share of 32.5% in 2024, characterized by well-established healthcare infrastructure, government-supported screening programs, and high adoption of advanced diagnostic technologies

- Italy is expected to be the fastest growing country in the melanoma cancer diagnostics market during the forecast period, due to increasing healthcare investments, rising awareness campaigns, and expanding access to diagnostic service

- Biomarkers test segment dominated the melanoma cancer diagnostics market with a market share of 38.6% in 2024, driven by its high accuracy in detecting melanoma-specific genetic and protein markers, guiding personalized treatment, and supporting early diagnosis initiatives

Report Scope and Europe Melanoma Cancer Diagnostics Market Segmentation

|

Attributes |

Europe Melanoma Cancer Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Melanoma Cancer Diagnostics Market Trends

Advancements in AI-Assisted and Digital Diagnostics

- A significant and accelerating trend in the Europe melanoma cancer diagnostics market is the increasing integration of artificial intelligence (AI) and digital platforms with traditional diagnostic methods, enhancing accuracy and speed of melanoma detection

- For instance, the SkinVision AI platform analyzes skin lesions using smartphone images and provides risk assessment for melanoma, enabling early-stage detection outside clinical settings

- AI-assisted diagnostics can identify subtle patterns in dermoscopy images and predict disease progression, while digital health platforms allow clinicians to track patient data over time. Furthermore, AI integration supports decision-making for targeted therapies and personalized treatment plans

- The seamless integration of AI and digital diagnostic tools with electronic medical records enables centralized patient management, facilitating better follow-up, data sharing, and research applications across hospitals and clinics

- This trend toward more intelligent, accurate, and connected diagnostic systems is reshaping expectations for melanoma detection and monitoring. Consequently, companies such as FotoFinder are developing AI-powered platforms to assist dermatologists in early melanoma identification

- The demand for AI-enabled and digitally integrated melanoma diagnostics is growing rapidly across both clinical and research sectors, as healthcare providers increasingly prioritize early detection and precision medicine

Europe Melanoma Cancer Diagnostics Market Dynamics

Driver

Increasing Melanoma Incidence and Awareness

- The rising incidence of melanoma across Europe, coupled with growing public and clinician awareness about early detection, is a significant driver for heightened demand for advanced diagnostics

- For instance, Germany’s national screening programs promote routine skin checks and AI-assisted dermoscopy, increasing patient uptake of diagnostic tests

- As the prevalence of melanoma cases grows, healthcare providers seek accurate tools such as biomarker testing and molecular diagnostics to support early diagnosis and treatment decisions

- In addition, the popularity of preventive health initiatives and skin cancer awareness campaigns is making melanoma diagnostics an integral component of national healthcare strategies

- Preventive health check-ups are preventive actions performed for the initial detection of melanoma cancer disease. Also, a rising preference for preventive health check-ups provides a safeguard against such asly exposure to any disease in the future

- Awareness to promote screening is the most important component of melanoma cancer prevention. The check-up is comprised of the identification of cancer and examinations of risk factors to limit loss at an early stage

- The convenience of rapid, non-invasive tests, digital reporting, and personalized risk assessments are key factors propelling adoption across hospitals, clinics, and dermatology centers

Restraint/Challenge

High Costs and Regulatory Hurdles

- The high costs associated with advanced melanoma diagnostics, including AI-powered platforms and biomarker tests, pose a significant challenge to broader market penetration

- For instance, some AI-based dermoscopy solutions require expensive devices and subscriptions, limiting adoption in smaller clinics or budget-sensitive regions

- Addressing regulatory compliance, validation requirements, and obtaining approvals across multiple European countries is crucial for market expansion. Furthermore, complex reimbursement policies can restrict accessibility for certain patient groups

- While prices are gradually decreasing and portable AI tools are emerging, the premium cost of high-precision diagnostics can hinder adoption, particularly among private practices and emerging markets

- The regulatory requirement for approvals of marketing or CE certification and application of laws and regulations could lead to making major changes in business or paying penalties, including the potential loss of business licenses. The resources and costs required to comply with these laws, rules, and regulations are quite high. Different manufacturing challenges for lipid nanoparticle production

- Overcoming these challenges through cost-effective solutions, streamlined regulatory approvals, and insurance coverage improvements will be vital for sustained market growth

Europe Melanoma Cancer Diagnostics Market Scope

The market is segmented on the basis of product type, test type, end user, and distribution channel.

- By Product Type

On the basis of product type, the Europe melanoma cancer diagnostics market is segmented into instruments, consumables and accessories, and others. The instruments segment dominated the market with the largest revenue share of 41.5% in 2024, driven by the high adoption of advanced diagnostic devices such as dermatoscopes, automated biopsy systems, and imaging platforms. Hospitals and diagnostic centers prioritize instruments for their accuracy, reliability, and integration with AI-assisted platforms, enabling efficient workflows and early detection. The segment benefits from continuous technological innovations, including portable and AI-enabled devices that facilitate precise melanoma diagnosis. Instruments also have strong demand due to their critical role in both clinical and research applications, supporting biomarker analysis and imaging-based diagnostics. In addition, the ability to standardize and validate results across different healthcare facilities further strengthens the market position of instruments in Europe.

The consumables and accessories segment is anticipated to witness the fastest growth rate of 10.8% CAGR from 2025 to 2032, fueled by the increasing use of biopsy kits, reagents, staining agents, and sample collection tools. Consumables are essential for routine diagnostic procedures and are frequently replenished, creating recurring revenue opportunities. The growth is further supported by rising melanoma incidence, adoption of molecular testing, and expansion of diagnostic laboratories that require continuous supply of consumables. Accessibility, cost-effectiveness, and compatibility with advanced instruments also drive adoption across hospitals and independent diagnostic centers.

- By Test Type

On the basis of test type, the melanoma cancer diagnostics market is segmented into biomarker tests, imaging tests, biopsy, fluorescent in situ hybridization (FISH) tests, comparative genomic hybridization (CGH) tests, immunohistochemical (IHC) tests, and others. The biomarker tests segment dominated the market with a share of 38.6% in 2024, driven by its high specificity in detecting melanoma-related genetic and protein markers. Biomarker tests facilitate early diagnosis, guide personalized treatment decisions, and are increasingly integrated into clinical workflows for patient stratification. Their adoption is bolstered by rising awareness among healthcare providers, advancements in molecular diagnostics, and growing research initiatives targeting melanoma. Biomarker tests are preferred for their minimally invasive nature, rapid results, and ability to monitor disease progression over time.

The imaging tests segment is expected to witness the fastest growth during 2025–2032, driven by AI-assisted dermoscopy, high-resolution imaging, and non-invasive technologies. Imaging tests are increasingly used in dermatology clinics for routine screening and follow-up, improving accuracy and patient convenience. Technological improvements in imaging devices, coupled with software that enhances lesion analysis, are contributing to rapid adoption. The segment benefits from the integration of imaging platforms with digital records, teledermatology, and remote consultation capabilities, expanding access across Europe.

- By End User

On the basis of end user, the melanoma cancer diagnostics market is segmented into hospitals, associated labs, independent diagnostic laboratories, diagnostic imaging centers, cancer research institutes, and others. The hospitals segment dominated with the largest market share of 45.2% in 2024, due to well-established infrastructure, availability of specialized dermatology departments, and high patient inflow. Hospitals prefer comprehensive diagnostic setups that combine instruments, biomarker tests, and imaging platforms for efficient melanoma detection. The segment benefits from government-supported screening programs and insurance reimbursements that facilitate adoption of advanced diagnostics. Hospitals also invest in AI-assisted platforms to improve early detection and patient outcomes, making them key drivers of market revenue.

The independent diagnostic laboratories segment is expected to witness the fastest growth rate of 11.4% CAGR from 2025 to 2032, fueled by increasing outsourcing of diagnostic services, expansion of private laboratories, and demand for rapid, specialized testing. These labs focus on molecular and biomarker-based diagnostics and cater to patients seeking timely, high-accuracy results outside hospital settings. Partnerships with hospitals and telemedicine services further enhance their market potential.

- By Distribution Channel

On the basis of distribution channel, the melanoma cancer diagnostics market is segmented into direct tender and retail sales. The direct tender segment dominated the market with the largest share of 62% in 2024, driven by bulk procurement by hospitals, cancer institutes, and government programs. Direct tender agreements ensure long-term supply, competitive pricing, and access to technical support from manufacturers, making it the preferred channel for large healthcare facilities. The segment benefits from strategic partnerships between diagnostic companies and healthcare providers, facilitating adoption of advanced instruments and test kits.

The retail sales segment is expected to witness the fastest growth rate of 12.1% CAGR from 2025 to 2032, fueled by increasing availability of diagnostic kits, AI-assisted mobile applications, and consumables for clinics and smaller diagnostic centers. Retail channels enhance accessibility, particularly for independent labs and emerging healthcare providers, supporting broader adoption of melanoma diagnostics across Europe. Growing awareness and adoption of home-based or point-of-care testing contribute to segment expansion. Overall, retail distribution is broadening access and accelerating the adoption of melanoma diagnostics across Europe.

Europe Melanoma Cancer Diagnostics Market Regional Analysis

- Germany dominated the melanoma cancer diagnostics market with the largest revenue share of 32.5% in 2024, characterized by well-established healthcare infrastructure, government-supported screening programs, and high adoption of advanced diagnostic technologies

- Patients and healthcare providers in Germany highly value early detection, precision diagnostics, and integration of AI-assisted platforms with clinical workflows, improving outcomes and treatment planning

- This widespread adoption is further supported by strong research initiatives, high healthcare expenditure, and growing public awareness about melanoma, establishing advanced diagnostic solutions as a preferred choice for hospitals, clinics, and cancer research institutes across the country

The Germany Melanoma Cancer Diagnostics Market Insight

The Germany melanoma cancer diagnostics market dominates the Europe market with the largest revenue share of 32.5% in 2024, fueled by its robust healthcare infrastructure, high public and private investment in cancer research, and widespread adoption of AI-assisted and biomarker-based testing solutions. Hospitals, cancer research centers, and diagnostic laboratories in Germany extensively utilize advanced imaging, molecular diagnostics, and minimally invasive biopsy techniques for accurate melanoma detection. The country’s emphasis on early detection, personalized treatment, and integration of digital health platforms strengthens its leading position. Germany’s focus on innovation and quality healthcare delivery continues to drive adoption across both urban and semi-urban regions.

Italy Melanoma Cancer Diagnostics Market Insight

The Italy melanoma cancer diagnostics market is expected to be the fastest growing country in the Europe market, with a projected high CAGR during the forecast period. Growth is driven by rising awareness campaigns, increasing investments in healthcare infrastructure, and expanding independent diagnostic laboratories. The adoption of AI-assisted platforms, biomarker testing, and teledermatology services is enhancing the accuracy and accessibility of melanoma diagnostics. Urbanization, preventive healthcare initiatives, and government-led early detection programs are further accelerating market expansion in Italy. Hospitals and specialized dermatology centers are increasingly adopting advanced diagnostic solutions to cater to a growing patient population and improve clinical outcomes.

U.K. Melanoma Cancer Diagnostics Market Insight

The U.K. melanoma cancer diagnostics market is expected to grow steadily due to increasing skin cancer awareness, preventive healthcare programs, and technological advancements in imaging and molecular diagnostics. Government initiatives, early detection campaigns, and high adoption of digital diagnostic tools in hospitals and clinics are driving demand. The integration of digital diagnostic tools and electronic medical records allows clinicians to efficiently track patient data, monitor lesion progression, and provide personalized treatment recommendations. In addition, government initiatives promoting early detection and research funding for melanoma cancer diagnostics are stimulating growth.

France Melanoma Cancer Diagnostics Market Insight

The France melanoma cancer diagnostics market is witnessing steady growth in market, supported by the expansion of dermatology clinics, adoption of non-invasive imaging techniques, and government-led skin screening programs. Hospitals and associated labs increasingly utilize biomarker tests and AI-assisted platforms to enhance early detection and patient management. Government-led skin screening programs and preventive healthcare policies are enhancing adoption rates across hospitals and associated laboratories. The growing demand for precision diagnostics and personalized therapy is encouraging healthcare providers to invest in advanced instruments and digital platforms.

Europe Melanoma Cancer Diagnostics Market Share

The Europe melanoma cancer diagnostics industry is primarily led by well-established companies, including:

- Sysmex Europe SE (Germany)

- BIOMÉRIEUX (France)

- Castle Biosciences, Inc. (U.S.)

- DermTech (U.S.)

- SYNLAB International (Germany)

- Biohit Oyj (Finland)

- Epigenomics AG (Germany)

- Damae Medical (France)

- SkylineDx (Netherlands)

- AMLo Biosciences Ltd (U.K.)

- Oxford Gene Technology IP Limited (U.K.)

- HYPHEN BioMed (France)

- Thermo Fisher Scientific Inc. (U.S.)

- Vermilion, Inc. (U.S.)

- Abbott (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- DiaSorin S.p.A. (Italy)

What are the Recent Developments in Europe Melanoma Cancer Diagnostics Market?

- In June 2025, hospitals in Málaga, Spain, collaborated with L'Oréal to develop an AI-driven study named 'SaVios' focused on early skin cancer detection. The project evaluates the effectiveness of the SkinVision mobile application, allowing users to scan skin lesions and receive automated risk assessments. The study aims to validate the app's utility in public health campaigns for melanoma prevention

- In May 2025, AI Medical Technology announced that its AI-powered melanoma diagnostic tool, Dermalyser, received CE Mark certification, enabling its commercial use across Europe. Dermalyser integrates with smartphones and dermatoscopes to provide risk scores for melanoma based on dermoscopic image analysis. In a Swedish clinical trial, Dermalyser demonstrated 95.2% sensitivity and 84.5% specificity, outperforming expert dermatologists and other AI tools.

- In January 2025, the European Association of Dermato-Oncology (EADO) released updated guidelines on melanoma diagnostics and treatment. These guidelines provide clinicians with evidence-based recommendations to enhance early detection, improve patient management, and standardize care across Europe. The updates reflect the latest clinical evidence and consensus from leading European experts

- In May 2024, an EU-funded initiative introduced a new skin cancer screening device designed for early detection of melanoma. This device aims to improve accessibility to screening, especially in underserved regions, and is part of broader efforts to enhance public health responses to skin cancer across Europe

- In May 2024, Bdetect, a medical equipment startup, launched a portable early detection device for skin cancer, developed with EU funding. The device uses different colored lights to determine whether a skin lesion is malignant or benign, simplifying skin cancer detection. This wireless, handheld device allows general practitioners to carry out quick routine screenings in their practices with the click of a button

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.