Europe Ophthalmic Surgical Instruments Market

Market Size in USD Billion

USD

3.45 Billion

USD

5.14 Billion

2024

2032

USD

3.45 Billion

USD

5.14 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.45 Billion | |

| USD 5.14 Billion | |

| % | |

|

Europe Ophthalmic Surgical Instruments Market Size

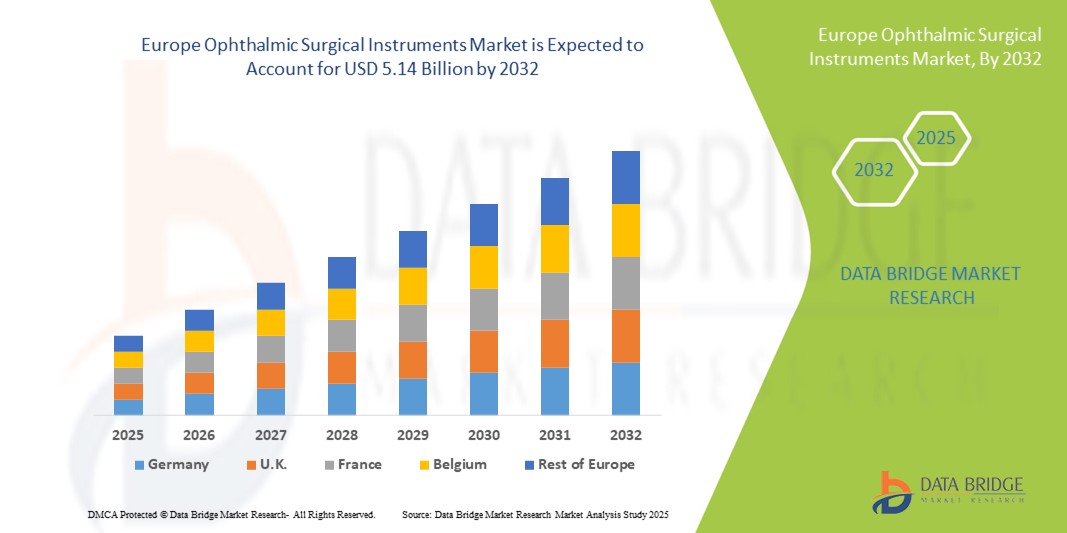

- The Europe ophthalmic surgical instruments market size was valued at USD 3.45 billion in 2024 and is expected to reach USD 5.14 billion by 2032, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the rising adoption of advanced ophthalmic procedures and the increasing prevalence of eye disorders, including cataracts, glaucoma, and retinal diseases, which are driving demand for precision surgical instruments

- Furthermore, advancements in minimally invasive surgical techniques, laser-assisted surgeries, and micro-incision procedures are boosting the adoption of innovative ophthalmic surgical instruments

Europe Ophthalmic Surgical Instruments Market Analysis

- Ophthalmic surgical instruments, used in precision eye surgeries such as cataract, glaucoma, and retinal procedures, are increasingly essential in modern healthcare settings due to their ability to improve surgical outcomes and patient recovery times

- The escalating demand for ophthalmic surgical instruments is primarily fueled by the rising prevalence of eye disorders, aging populations, and increasing adoption of minimally invasive and technologically advanced surgical procedures across hospitals and specialized eye care centers

- Germany dominated the Europe ophthalmic surgical instruments market with the largest revenue share of 38.5% in 2024, driven by its advanced healthcare infrastructure, high adoption of precision ophthalmic instruments, and strong presence of specialized eye care centers. The country’s focus on cataract, glaucoma, and retinal surgeries, along with collaborations with key medical device companies, reinforces its leadership position in the market

- France is expected to be the fastest growing country in the Europe ophthalmic surgical instruments market during the forecast period, registering the highest CAGR of 9.2% due to increasing investments in ophthalmology clinics, modernization of surgical facilities, and adoption of minimally invasive procedures. Rising awareness about eye care and government support for advanced surgical equipment further fuels market growth

- The Cataract segment dominated the Europe ophthalmic surgical instruments market with the largest revenue share of 36.9% in 2024, driven by the high prevalence of age-related cataracts and routine adoption of cataract surgery as a standard ophthalmic procedure

Report Scope and Ophthalmic Surgical Instruments Market Segmentation

|

Attributes |

Ophthalmic Surgical Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Ophthalmic Surgical Instruments Market Trends

Enhanced Precision and Technological Advancements

- A significant and accelerating trend in the Europe ophthalmic surgical instruments market is the growing adoption of advanced surgical instruments that enhance precision, reduce procedure times, and improve patient outcomes. These instruments are increasingly being integrated with high-resolution imaging systems, minimally invasive tools, and robotic-assisted platforms to support complex eye surgeries

- For instance, modern phacoemulsification handpieces, micro-incision instruments, and femtosecond laser-assisted tools are becoming standard in leading ophthalmic centers, allowing surgeons to perform delicate procedures with greater accuracy and safety

- Advancements in instrument ergonomics and material technology, such as lightweight alloys and corrosion-resistant coatings, are improving surgeon comfort and extending the lifespan of critical tools, contributing to better procedural efficiency

- The integration of imaging and navigation-assisted systems alongside surgical instruments facilitates precise planning, intraoperative guidance, and real-time assessment of surgical outcomes, ensuring higher success rates and fewer complications

- This trend towards more technologically sophisticated and precise surgical instruments is fundamentally reshaping ophthalmic care delivery in Europe, driving hospitals and eye care centers to invest in cutting-edge devices to meet patient expectations

- Consequently, manufacturers such as Alcon, Bausch + Lomb, and Carl Zeiss are focusing on launching innovative instruments that provide enhanced precision, reliability, and safety in ophthalmic surgeries

- The demand for advanced ophthalmic surgical instruments is growing rapidly across both public and private healthcare sectors, as healthcare providers increasingly prioritize improved surgical outcomes, efficiency, and patient satisfaction

Europe Ophthalmic Surgical Instruments Market Dynamics

Driver

Growing Need Due to Rising Prevalence of Ocular Disorders and Advanced Surgical Techniques

- The increasing prevalence of eye disorders, such as cataracts, glaucoma, diabetic retinopathy, and refractive errors, is a key driver for the rising demand for ophthalmic surgical instruments across hospitals, specialty clinics, and ambulatory surgical centers

- For instance, in April 2024, leading companies introduced advanced micro-incision cataract surgery tools and laser-assisted instruments, aiming to enhance surgical precision and reduce patient recovery times. Such technological advancements are expected to drive significant growth in the ophthalmic surgical instruments market during the forecast period

- Surgeons and healthcare providers are increasingly prioritizing instruments that improve surgical outcomes, reduce intraoperative complications, and ensure patient safety, boosting adoption across developed and emerging markets

- The growing emphasis on minimally invasive procedures and the integration of imaging systems, robotic-assisted tools, and high-precision devices are enabling more efficient, accurate, and safer surgeries, further propelling market expansion

- In addition, rising patient awareness about eye health and increasing access to ophthalmic care in emerging economies are contributing to a higher uptake of advanced surgical instruments

- The demand for versatile instruments capable of performing multiple procedures, such as vitreoretinal and glaucoma surgeries, is also encouraging manufacturers to innovate and expand their product portfolios

Restraint/Challenge

High Costs of Advanced Instruments and Need for Skilled Personnel

- The relatively high cost of technologically advanced ophthalmic surgical instruments remains a significant barrier to broader adoption, particularly among smaller clinics, outpatient centers, and healthcare facilities in developing regions. Premium instruments with laser-assisted features, robotic assistance, and high-precision optics often come with a substantial price tag, which can limit procurement and expansion

- In addition to cost concerns, these instruments require trained and experienced surgeons to operate effectively. The complexity of multi-functional devices means that improper handling or lack of expertise can lead to surgical errors, longer operative times, and potential complications, thereby constraining market growth

- Healthcare centers must often invest in specialized training programs and workshops to ensure that surgeons and staff are proficient in the use of these advanced instruments, further adding to operational expenditures

- The ongoing need for skilled personnel also creates a dependency on experienced professionals, which can slow the adoption rate in regions facing a shortage of trained ophthalmic surgeons

- Moreover, maintenance, calibration, and servicing of sophisticated instruments are critical for ensuring reliability and patient safety, requiring additional infrastructure and recurring costs for healthcare providers

- While innovative instruments offer improved surgical outcomes, their high initial investment and the operational challenges associated with skilled usage can impede rapid market penetration

- Addressing these challenges through cost-optimized instrument designs, scalable training solutions, and service-support programs will be crucial for enhancing adoption rates

- Manufacturers focusing on developing user-friendly, durable, and multi-functional instruments that balance performance with affordability are likely to mitigate these restraints, ensuring steady growth in the ophthalmic surgical instruments market

Europe Ophthalmic Surgical Instruments Market Scope

The market is segmented on the basis of product, application, and end user.

- By Product

On the basis of product, the Europe ophthalmic surgical instruments market is segmented into cataract surgery devices, refractive surgery devices, glaucoma surgery devices, vitreoretinal surgery devices, ophthalmic microscopes, and ophthalmic surgical accessories. The cataract surgery devices segment dominated with the largest market revenue share of 38.5% in 2024, driven by the high prevalence of cataract cases across Europe and the widespread adoption of phacoemulsification and micro-incision techniques. Technological advancements, such as femtosecond laser-assisted cataract surgery and premium intraocular lenses, are further boosting demand. Leading hospitals and eye care centers are investing in these devices to ensure improved surgical outcomes, faster recovery times, and patient satisfaction. The availability of cost-effective, high-precision instruments also contributes to market dominance.

The vitreoretinal surgery devices segment is expected to witness the fastest CAGR of 10.8% from 2025 to 2032, propelled by the increasing incidence of retinal disorders and diabetic retinopathy in Europe. Advanced microsurgical tools, minimally invasive vitrectomy systems, and integrated imaging platforms are driving adoption. The growing geriatric population, coupled with higher demand for improved visual outcomes, supports rapid growth. Surgeons are increasingly preferring innovative vitreoretinal instruments for complex procedures, and collaborations between device manufacturers and hospitals are accelerating penetration in the market.

- By Application

On the basis of application, the Europe ophthalmic surgical instruments market is segmented into cataract, refractive, glaucoma, vitreoretinal, diabetic retinopathy, and others. The cataract segment dominated with the largest revenue share of 36.9% in 2024, driven by the high prevalence of age-related cataracts and routine adoption of cataract surgery as a standard ophthalmic procedure. Adoption is further supported by ongoing technological improvements in surgical techniques, including small-incision and laser-assisted procedures. Increasing awareness among patients regarding vision restoration and the growing number of ophthalmic surgical centers across Europe strengthen the market leadership of this segment.

The vitreoretinal application segment is expected to witness the fastest CAGR of 11.2% from 2025 to 2032, fueled by rising prevalence of retinal diseases such as macular degeneration, diabetic retinopathy, and retinal detachment. Surgeons are increasingly relying on advanced vitreoretinal surgical devices and imaging-assisted tools to achieve better precision and reduce complications. Expanding healthcare infrastructure, investment in specialized eye hospitals, and increased adoption of minimally invasive surgery techniques are driving market growth. Additionally, growing patient awareness and demand for improved vision care are further supporting the adoption of these specialized instruments.

- By End User

On the basis of end user, the Europe ophthalmic surgical instruments market is segmented into hospitals, specialty clinics, ambulatory surgery centers, and others. The hospitals segment dominated with the largest revenue share of 52.7% in 2024, owing to the availability of well-equipped ophthalmic surgical departments, higher budgets, and the ability to adopt advanced instruments across multiple specialties. Both public and private hospitals lead the deployment of high-precision ophthalmic devices, supported by trained ophthalmologists and access to cutting-edge surgical technologies. Hospitals also benefit from bulk procurement and long-term maintenance agreements with manufacturers, reinforcing their market dominance.

The specialty clinics segment is expected to witness the fastest CAGR of 10.5% from 2025 to 2032, driven by the growing number of eye care centers focused exclusively on ophthalmic procedures, increasing patient preference for outpatient surgeries, and adoption of minimally invasive techniques. Clinics are investing in high-end cataract, refractive, and vitreoretinal devices to enhance surgical outcomes and attract patients seeking specialized eye care. The expansion of private ophthalmic networks and increasing awareness of vision correction procedures contribute to rapid growth in this segment.

Europe Ophthalmic Surgical Instruments Market Regional Analysis

- The Europe ophthalmic surgical instruments market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing demand for advanced ophthalmic procedures and rising prevalence of eye disorders. The market is fueled by high adoption of precision instruments, including cataract surgery devices, refractive surgery devices, glaucoma surgery devices, vitreoretinal surgery devices, ophthalmic microscopes, and other surgical accessories. Key applications such as cataract, glaucoma, vitreoretinal, refractive, and diabetic retinopathy procedures are witnessing strong growth across hospitals, specialty clinics, and ambulatory surgery centers

- Continuous innovations, increasing outpatient surgeries, and rising focus on minimally invasive procedures are encouraging healthcare providers to upgrade their surgical instruments. Germany dominated the Europe market with the largest revenue share of 38.5% in 2024, driven by its advanced healthcare infrastructure, high adoption of precision ophthalmic instruments, and strong presence of specialized eye care centers

- The country’s focus on cataract, glaucoma, and retinal surgeries, along with collaborations with leading medical device companies, reinforces its leadership position

Germany Ophthalmic Surgical Instruments Market Insight

The Germany ophthalmic surgical instruments market is expected to expand at a considerable CAGR during the forecast period. The country’s advanced healthcare infrastructure, high adoption of precision ophthalmic instruments, and strong presence of specialized eye care centers underpin its market dominance. Germany is a leader in cataract, glaucoma, and retinal surgeries, with hospitals and specialty clinics actively integrating advanced surgical devices such as vitreoretinal and refractive surgery instruments. Collaborations with leading medical device companies, focus on minimally invasive procedures, and investments in surgical innovations further reinforce Germany’s position as the largest contributor to Europe’s ophthalmic surgical instruments market.

France Ophthalmic Surgical Instruments Market Insight

The France ophthalmic surgical instruments market is expected to be the fastest-growing country in Europe, registering the highest CAGR of 9.2% during the forecast period. Growth is fueled by increasing investments in ophthalmology clinics, modernization of surgical facilities, and rising adoption of minimally invasive procedures. Hospitals and specialty eye care centers are upgrading to advanced cataract, glaucoma, vitreoretinal, and refractive surgery devices to meet growing patient demand. Enhanced awareness about eye health, government initiatives supporting advanced surgical equipment, and increasing focus on improving procedural efficiency further accelerate market expansion, positioning France as a key growth hub in Europe.

Europe Ophthalmic Surgical Instruments Market Share

The ophthalmic surgical instruments industry is primarily led by well-established companies, including:

- Carl Zeiss AG (Germany)

- Alcon Inc. (U.S.)

- Ziemer Ophthalmic Systems AG (Switzerland)

- Johnson & Johnson and its affiliates (U.S.)

- Takagi Ophthalmic Instruments Europe Ltd. (U.K.)

- HOYA Corporation (Japan)

- Lumenis Be Ltd. (Israel)

- STAAR SURGICAL (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- TOPCON CORPORATION (Japan)

- NIDEK CO., LTD. (Japan)

- Bausch + Lomb (U.S.)

- A.R.C. Laser GmbH (Germany)

- Iridex Corporation (U.S.)

- SCHWIND eye-tech-solutions GmbH (Germany)

Latest Developments in Europe Ophthalmic Surgical Instruments Market

- In June 2022, Oertli Instrumente AG acquired Domedics AG, a Swiss company specializing in ophthalmic products and services. This acquisition aimed to strengthen Oertli's presence in the Swiss ophthalmology market and enhance its product offerings

- In March 2023, Oertli Instrumente AG launched an updated version of its OS 4 surgical platform, designed for glaucoma, vitreoretinal, and cataract (phaco) surgery. The updated platform featured enhanced functionalities to improve surgical outcomes

- In May 2025, EssilorLuxottica announced its agreement to acquire Optegra, a European ophthalmology platform operating in the UK, Czech Republic, Poland, Slovakia, and the Netherlands. The acquisition aimed to expand EssilorLuxottica's presence in the medical technology sector and integrate advanced diagnostics and surgical treatments with its core eyecare services

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.