Europe Parasitology Identification Market

Market Size in USD Billion

USD

1.02 Billion

USD

1.52 Billion

2025

2033

USD

1.02 Billion

USD

1.52 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.02 Billion | |

| USD 1.52 Billion | |

| % | |

|

What is the Europe Parasitology Identification Size and Growth Rate?

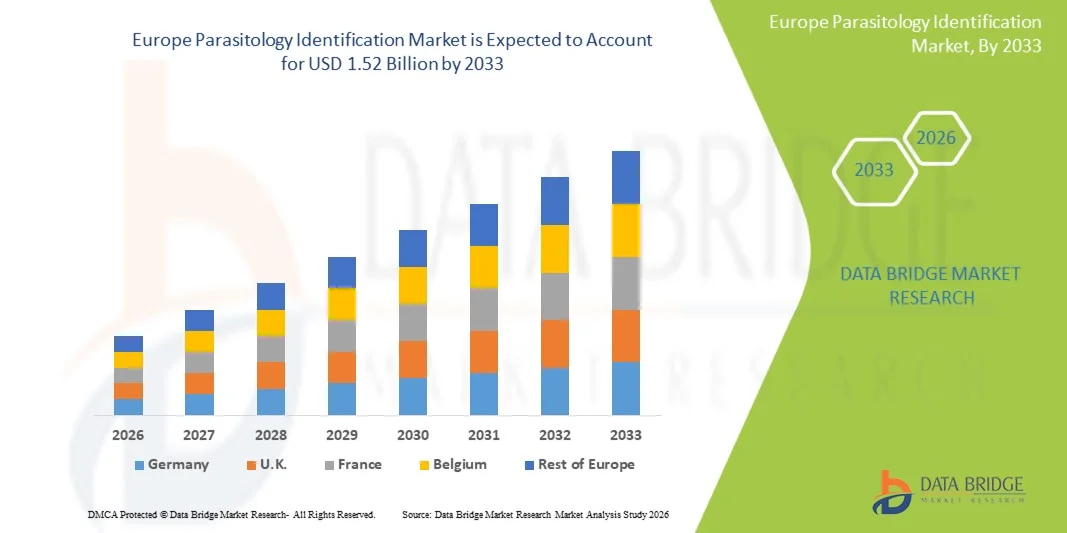

- As per Data Bridge Market Research Analysis the Europe parasitology identification market size was valued at USD 1.02 billion in 2025 and is expected to reach USD 1.52 billion by 2033, at a CAGR of 5.1% during the forecast period

- The market growth is largely fueled by the growing incidence and awareness of parasitic infections, increasing demand for accurate and rapid diagnostics across hospitals, diagnostic centres, and research labs, and rising adoption of advanced techniques such as molecular diagnostics, MALDI‑TOF MS, and rapid tests over classical methods

- Furthermore, rising government and public‑health initiatives in Europe focused on infectious disease surveillance, combined with enhanced healthcare infrastructure and investments in laboratory diagnostic capabilities, are driving the uptake of parasitology‑identification solutions, thereby establishing them as the modern standard for parasitic‑infection diagnosis

Market Size & Forecast

- Global Market Value (2025): USD 1.02 billion in 2025

- Expected Market Value (2033): USD 1.52 billion by 2033

- Forecast CAGR (2026–2033): 5.1%

Europe Parasitology Identification Market Analysis

- Parasitology identification solutions, offering diagnostic and detection capabilities for parasitic infections, are increasingly vital components of modern healthcare and research laboratories in both clinical and academic settings due to their enhanced accuracy, rapid results, and integration with laboratory information systems

- The escalating demand for parasitology identification solutions is primarily fueled by the growing incidence of parasitic infections, rising awareness of disease prevention, and a preference for advanced, rapid, and reliable diagnostic methods over traditional microscopy

- Germany dominated the Europe parasitology identification market with the largest revenue share of 32.4% in 2025, characterized by advanced healthcare infrastructure, strong government initiatives for infectious disease control, and a high adoption rate of molecular diagnostics and automated identification technologies, with hospitals and diagnostic laboratories experiencing substantial growth driven by innovations from leading diagnostic companies and research institutions

- Poland is expected to be the fastest growing country in the Europe parasitology identification market during the forecast period due to increasing healthcare investments, improving laboratory infrastructure, and rising public health awareness

- Consumables & Accessories segment dominated the Europe parasitology identification market with a market share of 46.7% in 2025, driven by their widespread use across diagnostic centers, hospitals, and research laboratories, and the rising demand for standardized, easy-to-use products for accurate parasitic detection and identification

Report Scope and Europe Parasitology Identification Market Segmentation

|

Attributes |

Europe Parasitology Identification Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

What is the Key Trend in the Europe Parasitology Identification?

“Advancements in Molecular and Rapid Diagnostic Techniques”

- A significant and accelerating trend in the Europe parasitology identification market is the growing adoption of advanced molecular diagnostics, MALDI‑TOF MS, and rapid diagnostic tests (RDTs), which are enhancing accuracy, reducing turnaround times, and enabling high-throughput testing in clinical and research laboratories

- For instance, the BD MAX™ System integrates molecular techniques for automated parasite detection, allowing laboratories to quickly identify multiple parasitic pathogens from a single sample, improving workflow efficiency and diagnostic precision

- Molecular and RDT integration enables features such as multiplex pathogen detection, automated reporting, and early-stage infection identification. For instance, some Bio-Rad kits allow simultaneous detection of protozoan and helminth infections, enabling faster treatment decisions and reducing diagnostic errors

- The seamless integration of these diagnostic techniques with laboratory information systems facilitates centralized management of patient samples and test results. Through a single platform, laboratories can handle sample tracking, testing, and reporting efficiently, ensuring timely and accurate results

- This trend towards more automated, rapid, and high-accuracy identification methods is reshaping user expectations for parasitology diagnostics. Consequently, companies such as CerTest Biotec are developing multiplex and AI-assisted RDTs to improve diagnostic reliability and speed across hospitals and diagnostic centers

- The demand for rapid, accurate, and high-throughput parasitology identification solutions is growing rapidly across both public health and private healthcare sectors, as laboratories prioritize speed, precision, and workflow efficiency

Europe Parasitology Identification Market Dynamics

Driver

“Increasing Incidence of Parasitic Infections and Rising Laboratory Testing Demand”

- The rising prevalence of parasitic infections across Europe, coupled with growing awareness of early diagnosis and disease prevention, is a significant driver for the heightened demand for parasitology identification solutions

- For instance, in March 2025, BioMérieux announced the expansion of its molecular parasite detection portfolio, aiming to enhance laboratory capabilities in hospitals and diagnostic centers for faster and more reliable identification

- As healthcare facilities become more focused on early detection and outbreak prevention, parasitology identification solutions offer advanced features such as multiplex pathogen detection, automated reporting, and high sensitivity, providing a compelling upgrade over traditional microscopy

- Furthermore, the increasing investments in laboratory infrastructure and the growing adoption of modern diagnostic technologies are making parasitology identification systems an integral component of clinical diagnostics, research labs, and public health monitoring

- The convenience of standardized consumables, automated sample processing, and integrated reporting systems are key factors propelling adoption in both hospitals and diagnostic centers. The trend towards rapid testing and high-throughput laboratory workflows further contributes to market growth

Restraint/Challenge

“High Cost of Advanced Diagnostics and Regulatory Compliance Hurdles”

- Concerns surrounding the high cost of advanced molecular and automated parasitology identification systems pose a significant challenge to broader market adoption, particularly in smaller clinics and budget-constrained laboratories

- For instance, some laboratories have been hesitant to adopt MALDI‑TOF MS or multiplex RDTs due to the initial capital investment and ongoing consumable costs, limiting uptake in certain regions

- Addressing these cost concerns through affordable product lines, leasing models, and government funding initiatives is crucial for expanding market reach. In addition, regulatory compliance and validation requirements for diagnostic devices add complexity and can delay product launches in certain European countries

- While prices are gradually decreasing and rapid diagnostic options are becoming more cost-effective, the perceived premium for high-throughput, automated systems can still hinder widespread adoption in smaller labs and emerging markets

- Overcoming these challenges through cost optimization, regulatory guidance, and education on the benefits of advanced parasitology diagnostics will be vital for sustained market growth

Europe Parasitology Identification Market Scope

The market is segmented on the basis of products, methods, pathogen type, sample, stool concentration and sample preparation, and end user.

- By Products

On the basis of products, the Europe parasitology identification market is segmented into devices and consumables & accessories. The Consumables & Accessories segment dominated the market with the largest revenue share of 46.7% in 2025, driven by their widespread use across diagnostic centers, hospitals, and research laboratories. Consumables include reagents, slides, culture media, and sample preparation kits essential for standardized, accurate, and repeatable testing. They are preferred due to ease of use, affordability, and compatibility with multiple diagnostic methods. Laboratories adopt consumables to maintain workflow efficiency and ensure reliable results. Routine testing and high-throughput laboratory operations further strengthen the demand for consumables. The segment benefits from increasing awareness of parasitic infections and adoption of advanced diagnostic techniques.

The Devices segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing investments in laboratory infrastructure and adoption of automated and semi-automated diagnostic instruments. Devices such as centrifuges, analyzers, and MALDI‑TOF MS equipment offer higher accuracy, faster processing, and scalability in sample handling. Growing emphasis on automation and digital workflows is accelerating device adoption across Europe. Hospitals and research centers prefer devices for advanced diagnostics and multiplex testing. Rising R&D activities and public health initiatives are further boosting market growth for devices.

- By Methods

On the basis of methods, the market is segmented into fecal identification, morphological identification, molecular techniques, MALDI‑TOF MS, immunological techniques, rapid diagnostic tests (RDTs), and others. The Molecular Techniques segment dominated the market in 2025, owing to their high sensitivity, specificity, and ability to detect multiple pathogens from a single sample. Molecular methods, including PCR and multiplex assays, allow early-stage detection of protozoan and helminth infections, improving patient outcomes. Integration into clinical workflows ensures faster diagnosis and reduced reliance on manual microscopy. Hospitals and reference laboratories widely adopt molecular techniques due to reliability and standardized results. Molecular diagnostics are preferred for surveillance and outbreak management. Their adoption is reinforced by government programs and public health initiatives.

The Rapid Diagnostic Tests (RDTs) segment is expected to witness the fastest growth from 2026 to 2033, driven by the need for point-of-care testing and immediate results in both urban and remote healthcare settings. RDTs provide portability, simplicity, and rapid turnaround, enabling timely clinical decisions. Adoption is supported by increasing awareness of parasitic infections and public health initiatives. Diagnostic centers prefer RDTs for on-site testing and high-throughput screening. Technological improvements in RDT accuracy and sensitivity further support growth. RDTs also reduce dependency on complex laboratory infrastructure.

- By Pathogen Type

On the basis of pathogen type, the market is segmented into protozoan, helminths, and ectoparasites. The Protozoan segment dominated the market in 2025, driven by the high prevalence of protozoan infections such as giardiasis, amoebiasis, and malaria in certain European populations. Advanced identification methods, including molecular techniques and MALDI‑TOF MS, are primarily applied for protozoan detection. Routine surveillance programs and hospital testing contribute to sustained demand. Protozoan diagnostics are critical due to rapid disease progression and potential complications. Hospitals and research centers prefer protozoan testing for early intervention. Investments in public health programs and laboratory infrastructure strengthen this segment.

The Helminths segment is expected to witness the fastest growth from 2026 to 2033 due to rising awareness of soil-transmitted helminth infections and increased screening programs. Automated and molecular diagnostic methods enhance detection accuracy and efficiency. Adoption is increasing in hospitals, diagnostic centers, and public health laboratories. Helminth diagnostics are increasingly integrated into routine health checks. Rising government initiatives and funding programs are supporting segment growth. Technological advancements in sample preparation and analysis further boost market expansion.

- By Sample

On the basis of sample, the market is segmented into feces, blood, urine, serum & plasma, and others. The Feces segment dominated the market in 2025, driven by its central role in parasitic diagnostics, particularly for gastrointestinal parasites. Fecal samples are preferred due to ease of collection, high pathogen load, and compatibility with multiple identification methods. Routine testing, government screening programs, and hospital diagnostics contribute to sustained demand. Fecal diagnostics support high-throughput laboratory workflows. Laboratories favor fecal testing for standardized results and accuracy. Increasing adoption of molecular and RDT methods reinforces the segment’s dominance.

The Blood segment is expected to witness the fastest growth from 2026 to 2033, fueled by molecular techniques and immunological assays for protozoan parasites such as Plasmodium species. Blood-based diagnostics provide rapid and reliable detection, especially in hospitals and research settings. Adoption is supported by increasing prevalence of blood-borne parasitic infections. Molecular integration enhances detection sensitivity and throughput. Blood samples are preferred for early-stage infection identification. Growth is further driven by hospital and diagnostic center investments in advanced equipment.

- By Stool Concentration and Sample Preparation

On the basis of stool concentration and sample preparation, the market is segmented into concentration technique and unconcentration technique. The Concentration Technique segment dominated the market in 2025 due to higher sensitivity in detecting low parasite loads in fecal samples. Techniques such as formalin-ethyl acetate concentration and flotation methods improve diagnostic accuracy and reproducibility. Concentration methods are widely adopted in hospitals and public health labs. They are critical for high-throughput routine testing and surveillance programs. Laboratory staff prefer concentration methods for reliable results. Ongoing technological improvements further strengthen dominance.

The Unconcentration Technique segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing use of automated sample preparation systems and the need for rapid diagnostic workflows. Unconcentrated methods simplify sample handling and reduce turnaround times. Adoption is rising in hospitals, diagnostic centers, and research labs. Automation and digital integration enhance workflow efficiency. Unconcentrated methods are preferred for large-scale screening and routine testing. Government and public health initiatives support segment growth.

- By End User

On the basis of end user, the market is segmented into diagnostic centers, hospitals, clinics, and others. The Hospitals segment dominated the market in 2025, driven by high patient inflow, requirement for rapid diagnosis, and adoption of advanced parasitology identification technologies. Hospitals use molecular techniques, MALDI‑TOF MS, and RDTs for outbreak management and routine diagnostics. Investments in laboratory infrastructure and patient safety drive adoption. Hospitals require high-throughput and standardized testing. Public health programs often prioritize hospital-based testing. Hospitals remain the primary revenue contributor in the market.

The Diagnostic Centers segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rise of specialized laboratories, government screening programs, and increased outsourcing from hospitals and clinics. Diagnostic centers offer cost-effective, rapid, and high-throughput testing solutions. Adoption is supported by rising awareness of parasitic infections and public health initiatives. Technological integration in diagnostic centers improves workflow efficiency. Increasing investments in equipment and infrastructure drive growth. Diagnostic centers are emerging as key players in the European market.

Europe Parasitology Identification Market Regional Analysis

- Germany dominated the Europe parasitology identification market with the largest revenue share of 32.4% in 2025, characterized by advanced healthcare infrastructure, strong government initiatives for infectious disease control, and a high adoption rate of molecular diagnostics and automated identification technologies, with hospitals and diagnostic laboratories experiencing substantial growth driven by innovations from leading diagnostic companies and research institutions

- Healthcare facilities and diagnostic laboratories in the country prioritize accuracy, rapid turnaround, and high-throughput testing, leading to widespread adoption of parasitology identification solutions across hospitals, research centers, and public health programs

- This dominance is further supported by substantial investments in laboratory infrastructure, skilled workforce, and government-backed infectious disease surveillance programs, establishing Germany as a leading hub for parasitology diagnostics in Europe

The U.K. Parasitology Identification Market Insight

The U.K. parasitology identification market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising incidence of parasitic infections and demand for rapid, accurate diagnostic solutions. Healthcare providers are increasingly adopting molecular assays, rapid diagnostic tests, and automated sample preparation for efficient parasite detection. Public health campaigns, infection control programs, and routine hospital screening initiatives are supporting market expansion. Laboratories are implementing high-throughput testing and workflow automation to meet growing diagnostic demands. The U.K.’s advanced healthcare infrastructure and focus on clinical accuracy continue to stimulate market growth. Government initiatives and private investments further reinforce the adoption of parasitology identification technologies.

Germany Parasitology Identification Market Insight

The Germany parasitology identification market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of parasitic diseases and growing demand for advanced diagnostic solutions. German hospitals and diagnostic centers are adopting molecular techniques, MALDI‑TOF MS, and immunological assays for rapid and precise parasite identification. Strong healthcare infrastructure and ongoing laboratory modernization promote adoption. Integration of diagnostics with laboratory information systems enhances workflow efficiency and reporting accuracy. Public health initiatives, disease monitoring programs, and research activities further drive market expansion. Laboratories prioritize accuracy, speed, and high-throughput capabilities to meet rising diagnostic demand.

France Parasitology Identification Market Insight

The France parasitology identification market is witnessing steady growth due to increasing demand for high-precision diagnostics and rising awareness of parasitic infections. Hospitals and diagnostic laboratories are adopting molecular techniques and rapid diagnostic tests for efficient detection and timely results. Government-led infection control programs and public health initiatives encourage widespread testing and surveillance. Laboratories focus on workflow automation and efficient sample preparation to meet increasing demand. The country’s emphasis on early detection and accurate diagnostics strengthens market adoption. Rising investments in laboratory infrastructure and development of skilled workforce support sustained growth.

Poland Parasitology Identification Market Insight

The Poland parasitology identification market is expected to grow at a fast pace during the forecast period, driven by increasing investments in diagnostic laboratories and rising adoption of molecular techniques. Private diagnostic providers, such as Diagnostyka, are expanding lab networks and offering specialized testing solutions, enabling broader access to parasitology diagnostics. Rising awareness of parasitic infections, especially in border and rural regions, is contributing to growing demand. Integration of automated sample preparation and high-throughput testing methods enhances diagnostic efficiency. Public health initiatives and screening programs are supporting adoption in hospitals and clinics. Overall, Poland’s strengthening diagnostic infrastructure and increasing emphasis on advanced testing position it as one of the fastest-growing markets in Europe.

Which are the Top Companies in Europe Parasitology Identification?

The Europe Parasitology Identification industry is primarily led by well-established companies, including:

- BIOMÉRIEUX (France)

- QIAGEN (Netherlands)

- Abbott (U.S.)

- Bruker Corporation (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- BD (U.S.)

- Bio Rad Laboratories, Inc. (U.S.)

- R Biopharm AG (Germany)

- ORGENTEC Diagnostika GmbH (Germany)

- altona Diagnostics GmbH (Germany)

- Meridian Bioscience, Inc. (U.S.)

- Luminex Corporation (U.S.)

- Tecan Trading AG (Switzerland)

- Trinity Biotech (Ireland)

- Serion GmbH (Germany)

- VWR International, LLC (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Coris BioConcept (Belgium)

- NovaTec Immundiagnostica GmbH (Germany)

- Quadratech Diagnostics (U.K.)

What are the Recent Developments in Europe Parasitology Identification Market?

- In October 2025, ARUP’s deep‑learning parasite detection system was reported to achieve 98.6% positive agreement with manual review, identifying 169 additional parasite organisms that had been missed by expert technologists highlighting the potential of AI-based diagnostics for intestinal parasites

- In July 2025, researchers at Karolinska Institutet (Sweden) and collaborators demonstrated that AI‑supported portable digital microscopy significantly improves detection of soil‑transmitted helminth (STH) infections in stool samples compared with traditional manual microscopy even for light‑intensity infections often missed by manual methods

- In March 2025, ARUP Laboratories announced the expansion of its AI‑augmented ova and parasite screening tool to include wet‑mount slides, becoming the first lab to apply AI across the entire ova‑and‑parasite testing workflow, improving sensitivity and reducing manual workload

- In January 2024, a report from European Food Safety Authority (EFSA) provided the 14th annual assessment on surveillance of E. multilocularis in wildlife across Europe part of ongoing efforts to monitor zoonotic parasitic threats in Europe, informing diagnostic, preventive, and public‑health strategies

- In September 2023, a new rapid molecular assay was reported that can simultaneously detect eight of the most common and clinically relevant gastrointestinal parasites enabling much faster diagnosis than traditional microscopy or culture-based methods.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.