Europe Single Use Medical Devices Reprocessing Market

Market Size in USD Billion

USD

1.47 Billion

USD

4.75 Billion

2025

2033

USD

1.47 Billion

USD

4.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.47 Billion | |

| USD 4.75 Billion | |

| % | |

|

Europe Single Use Medical Devices Reprocessing Market Size

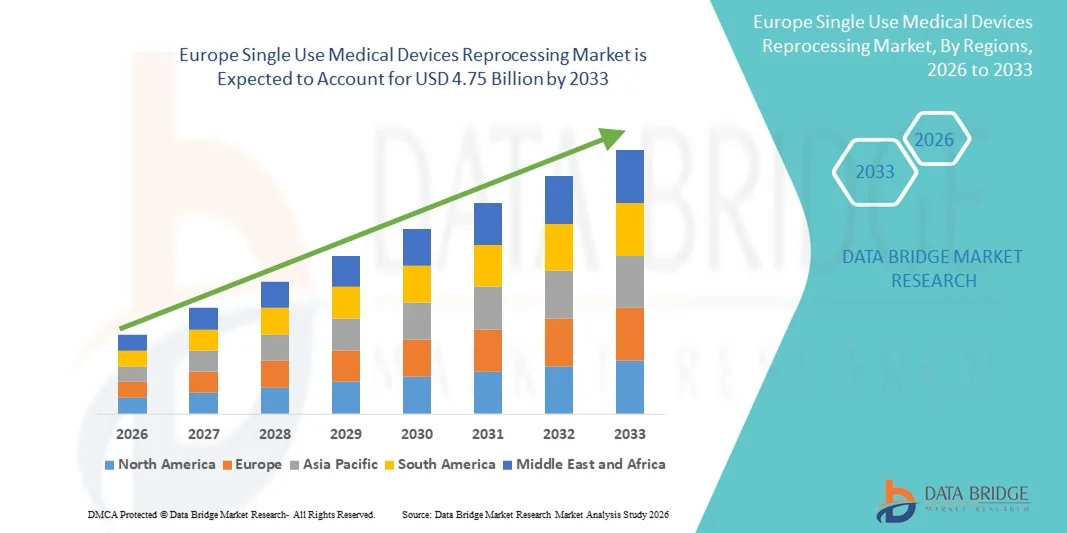

- The Europe single use medical devices reprocessing market size was valued at USD 1.47 billion in 2025 and is expected to reach USD 4.75 billion by 2033, at a CAGR of 15.8% during the forecast period

- The market growth is largely driven by increasing healthcare cost-containment pressures, sustainability initiatives, and rising adoption of regulated reprocessing practices across hospitals and healthcare facilities in Europe

- Furthermore, growing emphasis on environmental responsibility, reduced medical waste, and compliance with stringent regulatory frameworks is positioning reprocessed single-use medical devices as a safe, cost-effective, and sustainable alternative, thereby significantly boosting overall market growth

Europe Single Use Medical Devices Reprocessing Market Analysis

- Europe Single use medical devices reprocessing, involving the cleaning, sterilization, and functional testing of previously used disposable medical devices, is becoming an increasingly important practice across European healthcare systems as hospitals seek cost-efficient and environmentally sustainable solutions without compromising patient safety

- The rising demand for reprocessed single-use medical devices is primarily driven by mounting pressure to reduce healthcare expenditures, strict sustainability goals, and growing acceptance of validated reprocessing practices supported by regulatory oversight

- Germany dominated the Europe single use medical devices reprocessing market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, strong regulatory frameworks, and widespread adoption across hospitals where cost optimization and waste reduction initiatives are strongly emphasized

- Poland is expected to be the fastest growing country during the forecast period due to improving healthcare infrastructure, increasing hospital budgets, and growing awareness of the economic and environmental benefits of medical device reprocessing

- Class II devices segment dominated the market with a share of 57.2% in 2025, driven by their higher usage across complex surgical and diagnostic procedures, greater cost-saving potential through validated reprocessing, and stringent safety and performance requirements ensuring reliable outcomes

Report Scope and Europe Single Use Medical Devices Reprocessing Market Segmentation

|

Attributes |

Europe Single Use Medical Devices Reprocessing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Single Use Medical Devices Reprocessing Market Trends

Growing Focus on Sustainability and Cost Efficiency

- A significant and accelerating trend in the Europe single use medical devices reprocessing market is the increasing emphasis on environmentally sustainable practices combined with cost-saving initiatives, driving hospitals to adopt validated reprocessing protocols for disposable medical devices

- For instance, reprocessing of high-volume Class II devices such as cardiovascular catheters and electrophysiology tools allows healthcare facilities to significantly reduce medical waste while maintaining patient safety

- Advanced sterilization and functional testing technologies are being integrated into reprocessing workflows, enabling safe reuse of devices with consistent performance and reducing procurement costs for hospitals

- These practices not only contribute to operational efficiency but also support hospitals in meeting regulatory and environmental sustainability targets, including EU-wide waste reduction directives

- This trend is reshaping procurement strategies and hospital policies, with suppliers developing solutions that align with green healthcare initiatives and standardized safety protocols

- The demand for reprocessed single-use medical devices is expected to rise further across surgical and diagnostic applications, as hospitals increasingly seek to balance cost control with high-quality patient care

- For instance, hospitals are leveraging IoT-enabled monitoring systems to track device usage and lifecycle, ensuring optimized reprocessing schedules and operational efficiency

- Collaboration between medical device manufacturers and certified reprocessing service providers is increasing, enabling broader adoption of safe and validated reprocessed devices

Europe Single Use Medical Devices Reprocessing Market Dynamics

Driver

Increasing Pressure to Reduce Healthcare Costs and Medical Waste

- The growing financial burden on healthcare systems and the need to optimize operational budgets is a key driver for the adoption of reprocessed single-use medical devices in Europe

- For instance, hospitals in Germany and France are implementing validated reprocessing programs for Class II devices to lower procurement costs and reduce disposable medical device spending

- Reprocessed devices offer comparable safety and performance to new devices, allowing hospitals to maintain high-quality care while reducing unnecessary expenditure

- Furthermore, healthcare institutions are increasingly adopting circular economy practices to minimize medical waste, making reprocessing an essential component of sustainable healthcare operations

- The combination of cost reduction and environmental responsibility is compelling hospitals to invest in in-house and outsourced reprocessing solutions

- Validated reprocessing programs also support compliance with regulatory frameworks, ensuring hospitals meet stringent EU safety and quality standards while benefiting from cost savings

- For instance, growing partnerships between hospitals and certified reprocessors allow smaller healthcare facilities to access cost-effective reprocessing solutions without investing in complex equipment

- Increasing awareness campaigns and training programs for hospital staff on the benefits and safety of reprocessed devices are helping drive market adoption across Europe

Restraint/Challenge

Regulatory Compliance and Safety Concerns

- Challenges related to strict regulatory requirements and potential safety risks pose barriers to the widespread adoption of reprocessed single-use medical devices

- For instance, hospitals must adhere to European Medical Device Regulation (MDR) standards, which require rigorous validation, documentation, and traceability for reprocessed devices

- Concerns over device performance, cross-contamination, and infection control can make some healthcare providers hesitant to adopt reprocessed devices for critical procedures

- Ensuring consistent sterilization, functionality testing, and adherence to manufacturer guidelines is critical for maintaining clinical trust and patient safety

- The high initial investment for advanced reprocessing equipment or outsourcing partnerships can also be a financial hurdle for smaller hospitals or clinics

- Overcoming these challenges through standardized protocols, regulatory compliance, and hospital staff training is essential for driving sustained market growth and broader acceptance

- For instance, variations in national regulations across European countries create complexity for multi-country healthcare providers seeking uniform reprocessing practices

- Potential liability concerns and fear of legal repercussions in the event of device failure can limit adoption despite proven safety and performance of reprocessed devices

Europe Single Use Medical Devices Reprocessing Market Scope

The market is segmented on the basis of product type, price range, application, type, end user, and distribution channel.

- By Product Type

On the basis of product type, the market is segmented into Class I devices and Class II devices. The Class II devices segment dominated the market with the largest revenue share of 57.2% in 2025, driven by their extensive usage in complex surgical and diagnostic procedures. Hospitals prefer Class II devices for reprocessing due to their higher cost compared to Class I devices, offering significant cost-saving potential when reprocessed. In addition, Class II devices undergo rigorous functional and safety testing during reprocessing, ensuring reliability and compliance with European Medical Device Regulations. The demand for Class II devices is particularly strong in cardiology, orthopedics, and gastroenterology applications where procedural volumes are high. Class II devices also benefit from greater adoption by both in-house and outsourced reprocessing facilities due to standardized reprocessing protocols and validated sterilization methods. Manufacturers and reprocessing service providers are increasingly focusing on Class II devices to capitalize on the combination of cost efficiency, regulatory compliance, and safety assurances.

The Class I devices segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising adoption in smaller clinics and ambulatory surgical centers. Class I devices, being lower in cost and simpler in design, are more accessible for reprocessing in facilities with limited budgets and infrastructure. Their fast adoption is also supported by increased awareness of sustainable healthcare practices and environmental benefits. For instance, reprocessing high-volume Class I devices such as diagnostic catheters and minor surgical tools allows smaller hospitals to reduce procurement costs while contributing to waste reduction. The segment’s growth is further aided by government incentives and guidelines promoting safe reuse of Class I devices under validated procedures. In addition, the growing number of outpatient procedures and minor surgeries across Europe is creating a strong demand for Class I device reprocessing solutions.

- By Price Range

On the basis of price range, the market is segmented into high range and low/economy range. The high-range segment dominated the market in 2025, accounting for the largest revenue share, as hospitals and surgical centers prioritize high-value devices for reprocessing due to the substantial cost savings achievable on expensive Class II equipment. High-range devices such as cardiovascular catheters, endoscopes, and orthopedic implants benefit the most from validated reprocessing workflows, which ensure safety, functionality, and regulatory compliance. Reprocessing high-range devices also aligns with hospital sustainability initiatives, as reducing disposal of costly devices lowers environmental impact and operational expenditure. Hospitals with in-house or outsourced reprocessing units prefer high-range devices to maximize return on investment, while suppliers and service providers focus on offering comprehensive protocols and tracking systems for these devices. Advanced sterilization techniques and strict testing protocols further drive trust in reprocessed high-range devices, encouraging wider adoption.

The low/economy range segment is expected to witness the fastest growth from 2026 to 2033 due to the rising adoption of reprocessing in smaller healthcare facilities and emerging European countries. Low-range devices, such as basic surgical instruments and diagnostic tools, are increasingly being reprocessed to reduce cumulative costs and minimize waste. The segment’s growth is aided by the increasing number of outpatient procedures, small clinics, and ambulatory centers seeking cost-effective and environmentally friendly solutions. For instance, many clinics in Poland and Hungary are implementing validated low-range device reprocessing programs to optimize expenditures while adhering to safety standards. Growing awareness of environmental sustainability and government initiatives promoting reuse of disposable devices further propels the adoption of this segment.

- By Application

On the basis of application, the market is segmented into general surgery, anesthesia, arthroscopy and orthopedic surgery, cardiology, gastroenterology, urology, gynecology, and others. The cardiology segment dominated the market with the largest revenue share in 2025, driven by the high usage of expensive Class II devices such as electrophysiology catheters, stents, and balloon catheters. Hospitals prefer reprocessing cardiology devices to reduce operational costs while ensuring procedural safety and regulatory compliance. High procedural volumes in cardiology departments, coupled with stringent regulatory standards, make validated reprocessing a cost-effective and safe alternative. For instance, German and French hospitals have implemented cardiology device reprocessing programs to optimize expenditures and reduce medical waste. The segment also benefits from strong collaboration between device manufacturers and certified reprocessors.

The anesthesia segment is expected to witness the fastest growth from 2026 to 2033 due to the increasing number of surgical procedures and rising adoption of reprocessed anesthesia-related devices such as airway management tools and catheters. Smaller clinics and ambulatory surgical centers increasingly prefer reprocessed anesthesia devices to manage costs and enhance sustainability. For instance, hospitals in Poland and Italy are adopting anesthesia device reprocessing programs to reduce disposable usage and optimize supply chains. The growth of minimally invasive surgeries further contributes to demand in this segment. In addition, rising awareness of validated reprocessing protocols and environmental benefits is driving the adoption of anesthesia devices across European healthcare facilities.

- By Type

On the basis of type, the market is segmented into in-house and outsource. The in-house segment dominated the market with the largest revenue share in 2025, as large hospitals and surgical centers prefer maintaining direct control over the reprocessing of high-value devices. In-house reprocessing allows hospitals to ensure strict adherence to sterilization protocols, regulatory compliance, and device tracking. For instance, German hospitals with in-house reprocessing units can monitor device lifecycle and quality checks, ensuring reliability and safety. The segment benefits from high procedural volumes in Europe, making it cost-effective to operate in-house units for Class II and high-range devices. Advanced sterilization and testing technologies are increasingly integrated into hospital workflows, further enhancing adoption.

The outsource segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising adoption of certified third-party reprocessing services in smaller hospitals, clinics, and ambulatory surgical centers. Outsourcing allows healthcare facilities to access validated reprocessing protocols without investing in expensive equipment or training. For instance, hospitals in Poland, Hungary, and other emerging European countries are increasingly relying on outsourced reprocessing providers to manage operational costs while ensuring safety. The growing network of certified reprocessors across Europe, coupled with regulatory support, is further driving the adoption of outsourced solutions.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by high procedural volumes, diverse surgical departments, and the frequent use of high-cost devices suitable for reprocessing. Hospitals prioritize both cost savings and regulatory compliance, making them the primary adopters of validated reprocessing solutions. For instance, hospitals in Germany and France leverage reprocessed Class II devices for cardiology and orthopedic surgeries to reduce expenditure and minimize waste. The segment also benefits from advanced in-house and outsourced reprocessing infrastructure, enabling high-volume operations.

Ambulatory surgical centers are expected to witness the fastest growth from 2026 to 2033 due to the rising number of outpatient procedures and smaller surgical interventions. These centers increasingly adopt validated reprocessed devices to reduce costs while maintaining patient safety. For instance, centers in Poland and Italy have implemented reprocessing programs for Class I and low-range devices to optimize operational efficiency. Government incentives promoting sustainable practices and environmental responsibility further encourage adoption. The segment’s growth is also supported by partnerships with certified reprocessing service providers, allowing smaller facilities to access cost-effective solutions.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into B2B and B2C. The B2B segment dominated the market with the largest revenue share in 2025, driven by bulk procurement and established contracts between hospitals, clinics, and certified reprocessing service providers. B2B channels allow healthcare facilities to access validated reprocessed devices, maintain quality standards, and optimize operational costs. For instance, German hospitals often procure reprocessed Class II devices via B2B agreements with certified service providers to ensure compliance and consistent device availability. The segment benefits from long-term contracts, high procedural volumes, and standardized supply chains.

The B2C segment is expected to witness the fastest growth from 2026 to 2033 due to the rising adoption of reprocessed devices in smaller clinics and outpatient facilities, which procure devices on a smaller scale to meet immediate operational needs. For instance, individual clinics in Eastern Europe are increasingly sourcing Class I and economy-range devices directly from certified reprocessors. The convenience, cost efficiency, and growing awareness of validated reprocessing protocols drive the adoption of B2C channels. In addition, digital platforms and online marketplaces for reprocessed devices are emerging, making B2C procurement more accessible.

Europe Single Use Medical Devices Reprocessing Market Regional Analysis

- Germany dominated the Europe single use medical devices reprocessing market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, strong regulatory frameworks, and widespread adoption across hospitals where cost optimization and waste reduction initiatives are strongly emphasized

- Hospitals in the region prioritize cost reduction and sustainability, leveraging reprocessed Class II and high-range devices to lower procurement expenses while maintaining patient safety and regulatory compliance

- This strong market presence is further supported by well-established regulatory frameworks, skilled healthcare personnel, and collaborations between hospitals and certified reprocessing service providers, making Germany a leader in Europe for medical device reprocessing

Germany Single Use Medical Devices Reprocessing Market Insight

The Germany single use medical devices reprocessing market captured the largest revenue share of 38.5% in 2025, driven by the country’s advanced healthcare infrastructure, high surgical volumes, and strong adoption of validated reprocessing protocols. Hospitals and surgical centers prioritize cost reduction and environmental sustainability, leveraging reprocessed Class II and high-range devices to optimize expenditure while ensuring regulatory compliance. Furthermore, collaborations between hospitals and certified reprocessing service providers enhance operational efficiency and safety. The emphasis on patient safety, combined with strict adherence to European Medical Device Regulations, further consolidates Germany’s leading position. Hospitals’ preference for in-house and outsourced reprocessing solutions, alongside growing awareness of sustainable healthcare practices, continues to propel market growth.

France Single Use Medical Devices Reprocessing Market Insight

The France single use medical devices reprocessing market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by high procedural volumes, healthcare cost-containment initiatives, and increasing environmental awareness. Hospitals are increasingly adopting reprocessed devices in cardiology, gastroenterology, and orthopedic surgeries to reduce expenditure without compromising safety. In addition, government regulations and guidelines promoting safe reprocessing practices are encouraging wider adoption. France’s well-established healthcare system, coupled with investments in hospital infrastructure and digital tracking systems for devices, supports the market’s expansion across both public and private healthcare facilities.

U.K. Single Use Medical Devices Reprocessing Market Insight

The U.K. single use medical devices reprocessing market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising surgical volumes, healthcare cost pressures, and sustainability initiatives. Hospitals and surgical centers are adopting validated reprocessing programs for high-cost Class II and high-range devices to reduce operational expenditure and minimize medical waste. Awareness campaigns and training programs for clinical staff are promoting confidence in reprocessed devices. Furthermore, partnerships between hospitals and certified third-party reprocessors are expanding access to smaller healthcare facilities, supporting market growth. The emphasis on patient safety and compliance with European and national regulations continues to drive adoption.

Poland Single Use Medical Devices Reprocessing Market Insight

The Poland single use medical devices reprocessing market is poised to grow at the fastest CAGR during the forecast period, fueled by improving healthcare infrastructure, rising procedural volumes, and increasing awareness of cost-saving and environmentally sustainable practices. Smaller hospitals and ambulatory surgical centers are increasingly adopting reprocessed Class I and economy-range devices to manage operational costs effectively. Certified third-party reprocessors are expanding their networks in the country, making validated reprocessing accessible to emerging healthcare facilities. Government policies promoting safe device reuse and hospital adoption of circular economy practices are driving demand.

Europe Single Use Medical Devices Reprocessing Market Share

The Europe Single Use Medical Devices Reprocessing industry is primarily led by well-established companies, including:

- STERIS plc (Ireland)

- Stryker (U.S.)

- Medline Industries, Inc. (U.S.)

- Vanguard AG (Germany)

- Medtronic plc (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Centurion Medical Products Corporation (U.S.)

- Teleflex Incorporated (U.S.)

- Ascent Healthcare Solutions, Inc. (U.S.)

- ReNu Medical, Inc. (U.S.)

- SureTek Medical (U.S.)

- NEScientific, Inc. (U.S.)

- Innovative Health, Inc. (U.S.)

- Hygia Health Services, Inc. (U.S.)

- Soma Technology, Inc. (U.S.)

- MediPro Reprocessing (U.S.)

- RemedX (U.S.)

- Agiliti Health, Inc. (U.S.)

- Getinge AB (Sweden)

- Arjo (Sweden)

What are the Recent Developments in Europe Single Use Medical Devices Reprocessing Market?

- In November 2025, France launched a two‑year pilot project under Decree No. 2025‑895 to test the use of selected reprocessed single‑use medical devices, aiming to evaluate economic, environmental, and adoption impacts before wider implementation

- In February 2025, Denmark announced that it will allow the reprocessing of medical devices labelled as single‑use in hospitals beginning January 1, 2025, marking a major shift toward sustainable and cost‑effective healthcare by permitting reuse under regulated frameworks

- In December 2024, Health Care Without Harm Europe highlighted Denmark’s legislative change and broader EU interest in reprocessing single‑use medical devices as a vital step toward greener healthcare, emphasizing environmental benefits and reduced waste

- In April 2024, the European Commission’s DG SANTE published a comprehensive study and dashboard on the implementation of Article 17 of the EU Medical Device Regulation (MDR), providing data on how single‑use device reprocessing and reuse are being adopted across EU member states

- In May 2021, Article 17 of the EU Medical Device Regulation (MDR) came into force, establishing that entities reprocessing single‑use devices are considered manufacturers and setting unified European requirements while still allowing national opt‑in permissions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.