Europe Sternal Closure Systems Market

Market Size in USD Million

USD

936.22 Million

USD

1,620.66 Million

2025

2033

USD

936.22 Million

USD

1,620.66 Million

2025

2033

| 2026 - 2033 | |

| USD 936.22 Million | |

| USD 1,620.66 Million | |

| % | |

|

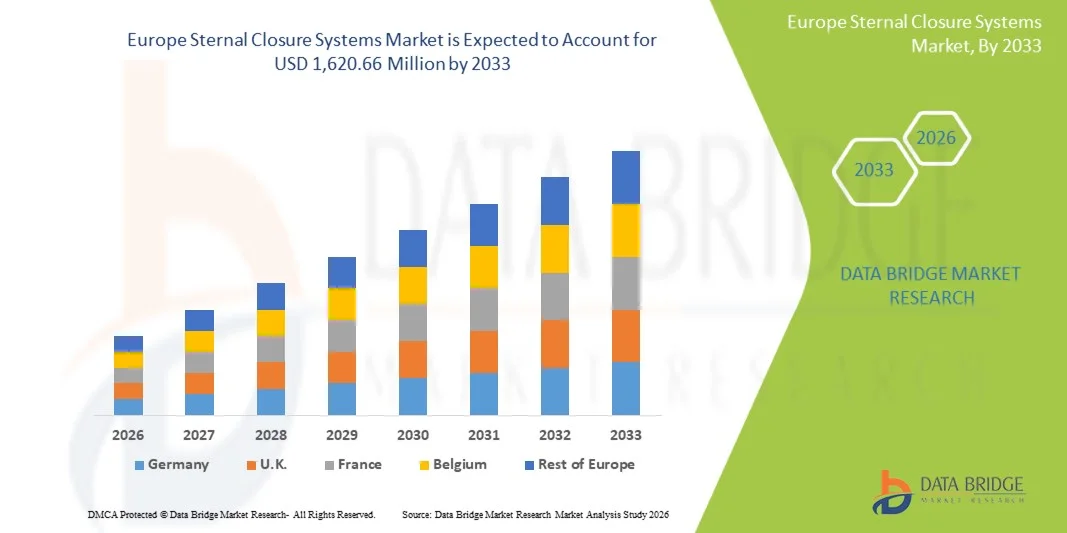

Europe Sternal Closure Systems Market Size

- The Europe sternal closure systems market size was valued at USD 936.22 million in 2025 and is expected to reach USD 1,620.66 million by 2033, at a CAGR of 7.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cardiothoracic surgeries, ongoing technological advancements in closure devices and favorable regulatory environments across European healthcare systems that support adoption of innovative surgical solutions

- Furthermore, rising demand for reliable and effective sternal closure solutions driven by the aging population, greater awareness of postoperative outcomes, and expanding procedural volumes in key European markets such as Germany, France, and the UK is encouraging broader adoption. These converging factors are accelerating the uptake of advanced sternal closure systems, thereby significantly boosting the industry’s growth

Europe Sternal Closure Systems Market Analysis

- Sternal closure systems, including closure devices and bone cement, are increasingly vital components in cardiothoracic surgeries, providing effective stabilization of the sternum post-operation, reducing complications, and supporting faster patient recovery in both hospitals and specialized cardiac centers

- The escalating demand for sternal closure systems is primarily fueled by the rising number of median sternotomy procedures, growing prevalence of cardiovascular diseases in Europe, and technological advancements in fixation techniques that enhance surgical outcomes and reduce postoperative complications

- Germany dominated the Europe sternal closure systems market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, high volumes of cardiac surgeries, and a strong presence of key medical device manufacturers adopting innovative wiring fixation and plate-screw systems

- Poland is expected to be the fastest growing country in the Europe sternal closure systems market during the forecast period due to expanding access to advanced cardiac surgical care, increasing healthcare investments, and rising adoption of modern fixation materials such as titanium and PEEK that offer superior strength and lower infection risks

- Plate-screw systems segment dominated the Europe sternal closure systems market with a market share of 45.9% in 2025, driven by their proven efficacy in providing rigid sternal stabilization and growing adoption across median sternotomy procedures in major European healthcare facilities

Report Scope and Europe Sternal Closure Systems Market Segmentation

|

Attributes |

Europe Sternal Closure Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Sternal Closure Systems Market Trends

“Advancements in Rigid Fixation and Minimally Invasive Techniques”

- A significant and accelerating trend in the Europe sternal closure systems market is the increasing adoption of rigid plate-screw fixation and minimally invasive sternal stabilization techniques, which enhance postoperative outcomes and reduce complications

- For instance, modern plate-screw systems allow surgeons to perform median sternotomies with better sternal alignment and stability, reducing recovery time and lowering the risk of infection

- Technological innovations such as bioresorbable plates and patient-specific fixation solutions are enabling more precise procedures and improved patient comfort, transforming standard sternal closure practices

- These advanced systems also integrate with surgical navigation tools and preoperative imaging, allowing for more accurate placement and reducing intraoperative errors in complex cardiothoracic surgeries

- This trend toward more effective, precise, and minimally invasive closure solutions is reshaping surgical standards, prompting manufacturers to develop innovative fixation systems with enhanced ergonomics and patient-specific designs

- The demand for advanced fixation technologies is growing across European hospitals and cardiac centers, as surgeons increasingly prioritize safety, reproducibility, and faster postoperative recovery in sternal closure procedures

- The increasing availability of advanced materials such as titanium and PEEK is also driving adoption, enabling lighter, stronger, and more biocompatible sternal closure solutions that improve patient outcomes

Europe Sternal Closure Systems Market Dynamics

Driver

“Rising Cardiac Surgeries and Need for Reliable Postoperative Stabilization”

- The increasing number of open-heart surgeries and cardiothoracic procedures in Europe is a significant driver for the growing demand for sternal closure systems

- For instance, hospitals in Germany and France are adopting advanced wiring and plate-screw systems to manage the rising procedural volumes and ensure optimal sternal healing

- Surgeons and healthcare providers seek reliable fixation methods to reduce postoperative complications such as sternal dehiscence and mediastinitis, driving system adoption

- Furthermore, technological advancements in fixation materials such as titanium and PEEK improve patient safety and long-term outcomes, supporting higher demand for premium sternal closure solutions

- The convenience and efficacy of modern closure systems, combined with increasing awareness among clinicians about postoperative benefits, are propelling adoption across both established and emerging European markets

- For instance, the rising geriatric population with higher cardiovascular risk is increasing the need for secure sternal stabilization in complex surgeries

- Expansion of healthcare infrastructure and investments in advanced cardiac surgical centers across countries such as Poland and Spain is also creating additional growth opportunities for closure systems

Restraint/Challenge

“High Cost and Regulatory Compliance Hurdles”

- The relatively high cost of advanced sternal closure systems compared to conventional wiring techniques poses a challenge to market penetration in budget-sensitive hospitals

- For instance, adoption of plate-screw systems and patient-specific fixation devices can be limited in smaller healthcare facilities due to budget constraints, slowing widespread implementation

- Regulatory approvals and compliance with European medical device standards can delay product launches and increase development costs, impacting market growth

- While technological innovations improve outcomes, the perception of high cost and procedural complexity can discourage some surgeons from adopting newer systems in routine procedures

- Overcoming these challenges through cost optimization, streamlined regulatory pathways, and increased clinical training will be essential to enable broader adoption and sustained market growth

- For instance, inconsistent reimbursement policies across European countries can hinder adoption of premium closure systems in some regions

- Limited awareness and training among surgeons on newer fixation techniques such as vacuum-assisted closure and interlocking systems can also slow adoption rates despite clinical benefits

Europe Sternal Closure Systems Market Scope

The market is segmented on the basis of product, procedure, fixation techniques, material, and end users.

- By Product

On the basis of product, the Europe sternal closure systems market is segmented into closure devices and bone cement. The closure devices segment dominated the market with the largest revenue share in 2025, driven by their extensive use in median sternotomy and complex cardiothoracic surgeries. Closure devices provide precise stabilization of the sternum, reducing the risk of postoperative complications such as sternal dehiscence and mediastinitis. Hospitals prefer closure devices for their versatility across different fixation techniques such as wiring and plate-screw systems. Technological advancements, including patient-specific designs and minimally invasive applications, further strengthen adoption. The segment also benefits from high procedural volumes in Germany, France, and the UK, making it the largest product category in Europe. Surgeons value closure devices for predictable outcomes and improved postoperative recovery.

The bone cement segment is expected to witness the fastest growth during the forecast period due to rising adoption in complex sternal reconstructions and revision surgeries. Bone cement enhances stability in fragile or osteoporotic sternums and is often used alongside wiring or interlocking systems. Innovations in biocompatible and radiopaque cements are supporting growth in hospitals and specialized surgical centers. Its compatibility with minimally invasive procedures increases its appeal. Rising awareness of improved patient outcomes and faster healing is fueling adoption. Surgeons are increasingly recommending bone cement in high-risk cases, contributing to the segment’s rapid growth.

- By Procedure

On the basis of procedure, the market is segmented into median sternotomy, hemisternotomy, and bilateral thoracosternotomy. The median sternotomy segment dominated the market in 2025 as it remains the most commonly performed cardiothoracic surgical approach, including CABG and valve replacement surgeries. Median sternotomy requires reliable sternal closure for optimal postoperative stability. Advanced closure devices and fixation techniques reduce complications and support faster patient recovery. Standardization of procedures across hospitals ensures consistent adoption of closure systems. Surgeons rely on this approach for both high-risk and routine cardiac patients. Its widespread use makes it the largest contributor to procedure-based market revenue.

The hemisternotomy segment is expected to witness the fastest growth from 2026 to 2033 due to rising preference for minimally invasive cardiac surgeries. Hemisternotomy offers smaller incisions, reduced surgical trauma, and quicker recovery. Specialized closure systems, including plate-screw and interlocking techniques, are ideal for this procedure. The segment is gaining traction in high-volume centers and emerging markets such as Poland. Growing clinician awareness and improved patient outcomes are driving adoption. Hemisternotomy adoption also aligns with trends toward patient-specific and ergonomically designed fixation solutions.

- By Fixation Techniques

On the basis of fixation techniques, the market is segmented into wiring fixation techniques, plate-screw systems, interlocking systems, cementing, and vacuum-assisted closure. The plate-screw systems segment dominated the market in 2025 with a market share of 45.9% due to superior rigidity, predictable outcomes, and reduced risk of sternal instability. Plate-screw systems are increasingly preferred in complex cardiac surgeries and high-risk patients. Advancements in surgical tools and compatibility with titanium and PEEK plates support adoption. Surgeons value these systems for consistent performance and reduced hospital stay durations. High procedural volumes in leading European hospitals reinforce market dominance. Plate-screw systems are also widely used in revisions and minimally invasive procedures.

The interlocking systems segment is expected to witness the fastest growth from 2026 to 2033, due to their versatility, ease of installation, and strong sternal stabilization with minimal tissue trauma. Interlocking systems are gaining adoption in revision surgeries and minimally invasive approaches. Emerging centers in Poland and Eastern Europe are key growth markets. These systems integrate well with modern closure devices and advanced fixation materials. Rising clinician awareness of improved patient outcomes is driving adoption. Interlocking systems are also increasingly favored for complex thoracosternotomy procedures, contributing to rapid growth.

- By Material

On the basis of material, the market is segmented into stainless steel, PEEK, titanium, and others. The stainless steel segment dominated the market in 2025 due to its long-standing clinical acceptance, cost-effectiveness, and mechanical durability in sternal closure procedures. Stainless steel wires and plates are widely used for both standard and complex surgeries. Hospitals prefer stainless steel for predictable outcomes and adherence to standard protocols. The material’s reliability and availability make it suitable for high procedural volumes. Compatibility with various fixation techniques reinforces its dominance. Its use in median sternotomy and bilateral thoracosternotomy ensures the largest market share.

The titanium segment is expected to witness the fastest growth from 2026 to 2033 because of superior biocompatibility, lightweight properties, and high strength-to-weight ratio. Titanium plates and screws reduce allergic reactions and integrate well with imaging techniques. They are preferred in premium cardiac centers for patient-specific applications. Increasing adoption in minimally invasive and revision procedures drives growth. Surgeons value titanium for improved patient outcomes and reduced complications. Its rising use in emerging European markets contributes to rapid expansion.

- By End Users

On the basis of end users, the market is segmented into hospitals and specialized surgical centers. The hospitals segment dominated the market in 2025 due to high procedural volumes of open-heart and cardiothoracic surgeries. Hospitals invest in advanced closure systems to reduce postoperative complications and ensure patient safety. Bulk procurement agreements and standardization of fixation techniques support adoption. Leading hospitals in Germany, France, and the UK are primary revenue contributors. Hospitals benefit from trained surgical teams and established protocols, reinforcing dominance. High procedural frequency ensures consistent demand for closure devices and fixation systems.

The specialized surgical centers segment is expected to witness the fastest growth from 2026 to 2033, due to their focus on complex and minimally invasive procedures. These centers adopt the latest technologies, including plate-screw and interlocking systems. Use of advanced materials such as titanium and PEEK is common in these facilities. Growth is driven by centers in Poland and Eastern Europe expanding cardiac surgical services. Focus on high-quality, patient-specific care increases adoption. Specialized centers often pioneer new techniques, further supporting market expansion.

Europe Sternal Closure Systems Market Regional Analysis

- Germany dominated the Europe sternal closure systems market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, high volumes of cardiac surgeries, and a strong presence of key medical device manufacturers adopting innovative wiring fixation and plate-screw systems

- Hospitals and surgical centers in the region highly value the reliability, precision, and reduced postoperative complications offered by advanced closure systems, including plate-screw and wiring fixation techniques, ensuring better patient outcomes

- This widespread adoption is further supported by the presence of key medical device manufacturers, well-trained surgical teams, and a focus on standardization of cardiac procedures, establishing sternal closure systems as a preferred solution in major German hospitals

The U.K. Sternal Closure Systems Market Insight

The U.K. sternal closure systems market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by increasing open-heart surgeries and cardiac procedures. Hospitals and specialized centers are adopting advanced closure devices to improve patient safety and reduce complications. Rising awareness among surgeons about rigid fixation techniques, such as plate-screw systems, is driving adoption. The country’s well-established healthcare infrastructure and focus on standardized surgical outcomes support growth. In addition, the integration of modern fixation materials such as titanium is gaining traction. Investments in minimally invasive cardiac procedures are further boosting market expansion in both public and private hospitals.

Germany Sternal Closure Systems Market Insight

The Germany sternal closure systems market is expected to expand at a considerable CAGR, driven by high procedural volumes in cardiothoracic surgery and advanced healthcare infrastructure. Hospitals prefer plate-screw and wiring fixation techniques for their proven reliability and patient safety outcomes. Germany’s focus on innovation, biocompatible materials, and minimally invasive surgical approaches encourages the adoption of modern closure systems. Surgeons are increasingly implementing patient-specific designs and advanced fixation methods to reduce postoperative complications. Strong presence of medical device manufacturers facilitates faster market uptake. In addition, Germany’s well-developed surgical training programs ensure consistent application of innovative sternal closure technologies across hospitals.

Italy Sternal Closure Systems Market Insight

The Italy sternal closure systems market is anticipated to grow at a considerable CAGR during the forecast period, driven by rising volumes of open-heart surgeries and increasing adoption of advanced fixation techniques in hospitals and specialized surgical centers. Surgeons in Italy are increasingly using plate-screw and interlocking systems for improved sternal stabilization and reduced postoperative complications. The growing emphasis on minimally invasive cardiac procedures and patient-specific solutions supports market growth. Italian hospitals are investing in biocompatible materials such as titanium and PEEK to enhance patient safety and recovery outcomes. Expansion of cardiac care infrastructure, along with the presence of established medical device manufacturers, further accelerates adoption. Rising awareness among clinicians about innovative closure techniques is also driving the market forward.

Poland Sternal Closure Systems Market Insight

The Poland sternal closure systems market is expected to be the fastest growing in Europe during the forecast period, due to expanding access to advanced cardiac surgical care and rising healthcare investments. Hospitals and specialized surgical centers are increasingly adopting modern fixation systems, including plate-screw and interlocking techniques. Growth is fueled by rising cardiothoracic surgery volumes and the need for safer, faster-recovery procedures. Emerging facilities are focusing on biocompatible materials such as titanium and PEEK to improve patient outcomes. Increased awareness of postoperative benefits and adoption of minimally invasive procedures further accelerate growth. Expansion of specialized cardiac centers and training programs supports the rapid market uptake in Poland.

Europe Sternal Closure Systems Market Share

The Europe Sternal Closure Systems industry is primarily led by well-established companies, including:

- Zimmer Biomet. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- B. Braun SE (Germany)

- KLS Martin Group (Germany)

- Acumed LLC (U.S.)

- Kinamed Incorporated (U.S.)

- Stryker (U.S.)

- Teleflex Incorporated (U.S.)

- JEIL Medical Corporation (South Korea)

- Arthrex, Inc. (U.S.)

- A&E Medical Corporation (U.S.)

- Jace Medical, LLC (U.S.)

- Able Medical Devices (U.S.)

- Praesidia SRL (Italy)

- Dispomedica GmbH (Germany)

- Medicon eG (Germany)

- Orthofix Medical Inc. (U.S.)

- Abyrx, Inc. (U.S.)

- Idear SRL (Italy)

- Acute Innovations LLC (U.S.)

What are the Recent Developments in Europe Sternal Closure Systems Market?

- In March 2025, Arthrex published clinical study results demonstrating that its FiberTape® sternal closure system (a non‑metal suture alternative) showed superior outcomes versus traditional metal wires including lower sternal wound infection rates, reduced dehiscence, and shorter closure times in cardiac surgery patients

- In February 2025, Heart, Lung & Circulation published a peer‑reviewed study examining the effectiveness of various sternal closure devices post‑adult cardiac surgery. The research helps validate clinical practice and may influence the choice of devices used across European surgical institutions

- In August 2024, DePuy Synthes (part of Johnson & Johnson MedTech) announced the launch of the MatrixSTERNUM™ Fixation System, an advanced plate‑and‑screw solution designed to provide stronger locking strength and faster, low‑profile sternal fixation following open‑heart and chest surgeries

- In May 2024, researchers reported clinical use of a rigid fixation sternal closure system made from biocompatible carbon fiber a material innovation aimed at providing superior stability and reduced postoperative pain compared with conventional metal fixation methods. This series of cases represents the first documented worldwide clinical application of this carbon‑fiber system, indicating a shift toward exploring alternative high‑performance materials for sternum stabilization after open‑heart surgery

- In November 2021, NEOS Surgery showcased its new STERN Fix™ sternal fixation device at the annual European Association for Cardio‑Thoracic Surgery (EACTS) meeting in Barcelona. The product uses a carbon‑PEEK matrix instead of traditional stainless steel wires and is designed to reduce bone‑implant stress while improving handling and stability for open‑heart surgery sternotomy fixation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.