Europe Surgical Visualization Products Market

Market Size in USD Billion

USD

1.00 Billion

USD

2.33 Billion

2024

2032

USD

1.00 Billion

USD

2.33 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.00 Billion | |

| USD 2.33 Billion | |

| % | |

|

Europe Surgical Visualization Products Market Size

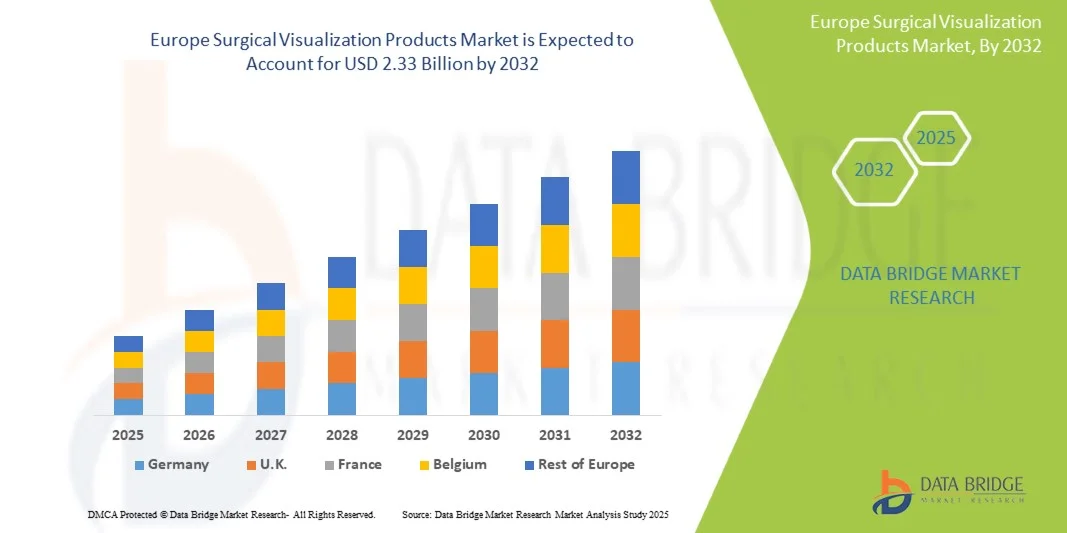

- The Europe surgical visualization products market size was valued at USD 1.00 billion in 2024 and is expected to reach USD 2.33 billion by 2032, at a CAGR of 11.1% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic diseases, an aging population, and continuous technological advancements in imaging systems, including high-definition and 3D visualization technologies, which are enhancing surgical precision and outcomes

- Furthermore, increasing investments by hospitals in state-of-the-art equipment and the growing demand for minimally invasive procedures are establishing surgical visualization products as essential tools in modern healthcare settings. These converging factors are accelerating the adoption of advanced surgical visualization solutions, thereby significantly boosting the industry's growth

Europe Surgical Visualization Products Market Analysis

- Surgical visualization products, including endoscopic cameras, imaging systems, and 3D visualization tools, are increasingly critical components of modern operating rooms in both hospitals and ambulatory surgical centers due to their ability to enhance precision, improve surgical outcomes, and support minimally invasive procedures

- The escalating demand for surgical visualization products is primarily fueled by the rising prevalence of chronic diseases, an aging population, and continuous technological advancements in imaging systems, including high-definition and 3D visualization technologies that improve surgical accuracy and efficiency

- Germany dominated the Europe surgical visualization products market with the largest revenue share of 28.5% in 2024, characterized by high healthcare expenditure, robust R&D activities, and the presence of key industry players, with hospitals and surgical centers experiencing substantial adoption of advanced visualization systems driven by innovations in imaging and integration with robotic-assisted surgeries

- Poland is expected to be the fastest-growing country in the Europe surgical visualization products market during the forecast period due to improving healthcare infrastructure, increasing surgical procedures, and rising investments in modern medical equipment

- Endoscopic camera segment dominated the Europe surgical visualization products market with a market share of 39.6% in 2024, driven by its central role in surgical visualization, compatibility with multiple procedures, and ease of integration into existing surgical setups

Report Scope and Europe Surgical Visualization Products Market Segmentation

|

Attributes |

Europe Surgical Visualization Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Surgical Visualization Products Market Trends

“Advancements in 3D and AI-Assisted Visualization”

- A significant and accelerating trend in the Europe surgical visualization products market is the integration of 3D imaging and AI-assisted analytics into endoscopic and microscopic systems, significantly enhancing surgical precision and real-time decision-making

- For instance, the Olympus ORBEYE 3D Surgical Microscope provides surgeons with high-definition 3D visualization while integrating AI-based guidance tools to improve anatomical recognition and reduce intraoperative errors

- AI integration enables features such as real-time tissue differentiation, surgical workflow optimization, and predictive alerts for critical steps, enhancing overall procedural efficiency. For instance, Brainlab’s AI-assisted navigation systems offer real-time guidance for complex neurosurgical procedures, improving accuracy and reducing risks

- The seamless incorporation of these technologies into surgical workflows allows surgeons to access advanced imaging, preoperative planning data, and intraoperative guidance through a single interface, facilitating more efficient and precise operations

- This trend towards more intelligent and interconnected surgical visualization systems is reshaping expectations for operating room capabilities, with companies such as Karl Storz developing AI-enhanced endoscopic cameras capable of automated image optimization and procedural recommendations

- The demand for advanced 3D and AI-assisted visualization systems is growing rapidly across hospitals and specialized surgical centers, as healthcare providers increasingly prioritize precision, efficiency, and improved patient outcomes

Europe Surgical Visualization Products Market Dynamics

Driver

“Increasing Surgical Procedures and Technological Advancements”

- The rising number of minimally invasive and complex surgical procedures across Europe, coupled with continuous technological advancements in imaging systems, is a significant driver for the heightened demand for surgical visualization products

- For instance, in 2024, Stryker introduced an advanced 3D visualization system for orthopedic and spinal surgeries, offering improved depth perception and integration with robotic-assisted tools, boosting surgical precision and efficiency

- As hospitals and surgical centers aim to reduce complications and improve patient outcomes, advanced visualization systems provide high-definition imaging, real-time navigation, and enhanced ergonomic designs, offering a compelling upgrade over conventional surgical tools

- Furthermore, the adoption of digital ORs and interconnected surgical equipment is making advanced visualization products an essential component of modern surgical suites, enabling seamless coordination with other devices and robotic systems

- The efficiency, accuracy, and workflow optimization provided by these advanced systems, along with growing awareness among surgeons, are key factors propelling the adoption of surgical visualization products across hospitals and specialty centers in Europe

Restraint/Challenge

“High Costs and Regulatory Compliance Hurdles”

- The relatively high acquisition and maintenance costs of advanced surgical visualization systems pose a significant challenge to broader adoption, especially for smaller hospitals or budget-constrained healthcare providers

- For instance, premium systems from companies such as Leica Microsystems or Zeiss can cost several hundred thousand euros, limiting accessibility for smaller facilities despite their clinical benefits

- In addition, stringent regulatory requirements for medical devices in Europe, including CE marking and compliance with MDR guidelines, can slow product approvals and market entry, raising concerns among manufacturers

- While efforts are made to reduce costs and streamline approval processes, the combination of high investment and regulatory complexities can hinder market penetration, particularly in emerging European markets

- Overcoming these challenges through cost-effective solutions, leasing models, and robust compliance strategies is crucial for sustained adoption and growth of surgical visualization products across Europe

Europe Surgical Visualization Products Market Scope

The market is segmented on the basis of product type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the market is segmented into endoscopic cameras, accessories, light sources, display and monitors, video recorders & processors, camera heads, and video converters. The endoscopic camera segment dominated the market with the largest revenue share of 39.6% in 2024, driven by its essential role in minimally invasive surgeries and high compatibility with multiple surgical procedures. Hospitals and surgical centers prefer endoscopic cameras for their ability to deliver high-definition imaging, improve procedural accuracy, and integrate with 3D visualization and robotic-assisted systems. The demand is also bolstered by technological advancements such as AI-based image enhancement, auto-focus, and ergonomic designs that enhance surgeon comfort. In addition, the availability of modular systems and compatibility with various endoscopic accessories further increases adoption in diverse surgical applications.

The accessories segment is anticipated to witness the fastest growth rate of 12% from 2025 to 2032, fueled by rising demand for complementary components such as insufflators, trocars, and instrument adapters that enhance the efficiency and versatility of surgical visualization systems. Accessories enable surgeons to customize their tools for specific procedures, improving operational flexibility and patient outcomes. Growth in this segment is supported by increasing numbers of specialty clinics and ambulatory surgical centers adopting minimally invasive techniques that require specialized accessories. Continuous innovation, lightweight materials, and ergonomic designs further drive the adoption of surgical accessories across Europe.

- By Application

On the basis of application, the market is segmented into arthroscopy, laparoscopy, ENT endoscopy, obstetrics/gynecology endoscopy, urology endoscopy, gastroscopy, and others. The arthroscopy segment dominated the market in 2024, driven by the high prevalence of orthopedic disorders, increased sports-related injuries, and rising adoption of minimally invasive joint procedures. Arthroscopic surgeries benefit from high-definition imaging and precision instruments, making visualization products essential for accurate diagnosis and treatment. Hospitals and specialty orthopedic centers prefer these systems for their reliability, enhanced visualization, and ability to reduce procedural complications. Advanced visualization tools allow surgeons to perform complex procedures with smaller incisions, leading to faster patient recovery. The integration of AI and 3D imaging further boosts the adoption of visualization products in arthroscopy.

The laparoscopy segment is expected to witness the fastest growth from 2025 to 2032, driven by the rising demand for minimally invasive abdominal surgeries in general surgery, bariatrics, and oncology. Laparoscopic procedures reduce hospital stays, postoperative pain, and recovery times, increasing patient preference and hospital adoption. The growing number of outpatient surgical centers and rising awareness of minimally invasive techniques contribute to this segment’s rapid growth. In addition, continuous technological improvements in laparoscopic cameras, light sources, and accessories further enhance procedural efficiency and outcomes.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, diagnostic imaging centers, ambulatory surgical centers, and others. The hospital segment dominated the market in 2024, holding the largest revenue share due to high procedure volumes, greater capital expenditure capacity, and preference for advanced surgical technologies. Hospitals invest heavily in high-quality visualization systems to improve surgical precision, patient safety, and overall clinical outcomes. Integration with robotic-assisted surgeries, AI analytics, and 3D visualization systems further reinforces hospital dominance. Hospitals also benefit from comprehensive service and maintenance agreements offered by manufacturers, ensuring reliable performance of visualization products.

The ambulatory surgical centers segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing shift of minimally invasive procedures from inpatient to outpatient settings. Cost efficiency, faster patient throughput, and rising patient demand for outpatient surgeries support the adoption of surgical visualization systems in these centers. Growth is further fueled by advancements in portable and compact visualization equipment suitable for smaller facilities. Rising investments in specialized clinics offering day surgeries and minimally invasive procedures contribute to rapid segment expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment dominated the market in 2024, accounting for the largest revenue share due to strong manufacturer-hospital relationships, bulk procurement, and direct after-sales service support. Hospitals prefer direct tender channels to ensure authenticity, timely delivery, and access to full-service support and training. Manufacturers also benefit from predictable demand, long-term contracts, and better margin control through direct tender arrangements.

The third-party distributors segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing number of specialty clinics, ambulatory surgical centers, and smaller hospitals relying on distributor networks for access to advanced surgical visualization products. Third-party distributors provide flexibility, localized support, and faster product availability across multiple European regions. Growing partnerships between distributors and emerging manufacturers offering cost-effective solutions further contribute to this segment’s rapid growth.

Europe Surgical Visualization Products Market Regional Analysis

- Germany dominated the Europe surgical visualization products market with the largest revenue share of 28.5% in 2024, characterized by high healthcare expenditure, robust R&D activities, and the presence of key industry players, with hospitals and surgical centers experiencing substantial adoption of advanced visualization systems driven by innovations in imaging and integration with robotic-assisted surgeries

- Hospitals and surgical centers in the country highly value advanced visualization systems for their ability to improve surgical precision, support minimally invasive procedures, and enhance patient outcomes through high-definition imaging and 3D visualization

- This widespread adoption is further supported by well-established healthcare infrastructure, skilled surgical professionals, and increasing investments in digital and robotic-assisted operating rooms, establishing surgical visualization products as essential tools across hospitals and specialty clinics in Germany

France Surgical Visualization Products Market Insight

The France surgical visualization products market is projected to expand at a substantial CAGR during the forecast period, driven by rising investments in healthcare infrastructure and the growing prevalence of chronic diseases requiring minimally invasive procedures. Hospitals and specialty clinics are increasingly adopting high-definition imaging systems and advanced endoscopic cameras. The French market is further supported by government initiatives promoting modern healthcare technologies and digital operating rooms. Both private and public hospitals are enhancing surgical capabilities through updated visualization equipment. Increasing awareness among surgeons regarding AI-assisted and 3D visualization tools boosts market adoption.

Spain Surgical Visualization Products Market Insight

The Spain surgical visualization products market is anticipated to expand at a considerable CAGR during the forecast period, fueled by increasing demand for minimally invasive procedures and modern surgical infrastructure. Hospitals and specialty clinics are adopting advanced visualization tools such as endoscopic cameras, 3D imaging systems, and AI-assisted processors to improve surgical precision. The country’s healthcare initiatives supporting technological modernization of hospitals further drive market growth. Rising patient awareness about faster recovery and reduced complications encourages the adoption of advanced visualization products. Integration with robotic-assisted surgeries and digital ORs adds further impetus to market expansion.

Poland Surgical Visualization Products Market Insight

The Poland surgical visualization products market is expected to be the fastest-growing in Europe during the forecast period, driven by improving healthcare infrastructure and increasing adoption of minimally invasive procedures. Hospitals and specialty clinics are rapidly upgrading to advanced endoscopic cameras, light sources, and video processors to enhance surgical outcomes. Government initiatives promoting digital operating rooms and investments in modern surgical technologies support market expansion. Rising awareness among surgeons and healthcare providers about AI-assisted and 3D visualization tools further fuels adoption. Both new installations and renovation projects in hospitals and ambulatory surgical centers contribute to the rapid growth of this market segment.

Europe Surgical Visualization Products Market Share

The Europe Surgical Visualization Products industry is primarily led by well-established companies, including:

- Olympus Corporation (Japan)

- Stryker (U.S.)

- FUJIFILM Holdings Corporation (Japan)

- Karl Storz GmbH & Co. KG (Germany)

- Medtronic (Ireland)

- Smith & Nephew (U.K.)

- CONMED Corporation (U.S.)

- Richard Wolf GmbH (Germany)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- GE HealthCare (U.S.)

- Ziehm Imaging GmbH (Germany)

- Shimadzu Corporation (Japan)

- Hologic Corporation (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Samsung Healthcare (South Korea)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Hypervision Surgical Ltd (U.K.)

- Alesi Surgical (U.K.)

- MITAKA EUROPE GMBH (Germany)

What are the Recent Developments in Europe Surgical Visualization Products Market?

- In October 2025, Olympus Corporation introduced the THUNDERBEAT II, a surgical energy device designed for hemostatic cutting and vessel sealing. This device integrates advanced energy technology to enhance surgical precision and efficiency in various procedures

- In October 2025, Stereotaxis announced the European launch of its Synchrony system, a next-generation platform designed to modernize interventional cath labs. The system integrates all lab visuals and controls into a single digital interface, offering enhanced workflow, clearer visualization, and improved connectivity through its companion cloud app, SynX

- In September 2025, ZEISS Medical Technology showcased new ophthalmic innovations and market milestones at the European Society of Cataract and Refractive Surgeons (ESCRS) 2025 conference in Copenhagen, Denmark. These innovations aim to expand ophthalmic care options and create industry-leading workflow solutions

- In July 2025, Zimmer Biomet announced its acquisition of Monogram Technologies for approximately USD 177 million to enhance its robotics portfolio, particularly in surgical robotics. Monogram specializes in semi- and fully autonomous surgical technologies, including a semi-autonomous knee replacement system approved by the FDA in March 2025

- In June 2025, UK-based medical robotics company CMR Surgical announced its intention to seek a sale valued at up to $4 billion as it prepares to enter the U.S. market. The company aims to expand its presence in the global surgical robotics field, with its main product, Versius, having been used in over 30,000 procedures across more than 30 countries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.