Global Achondrogenesis Market

Market Size in USD Billion

USD

2.01 Billion

USD

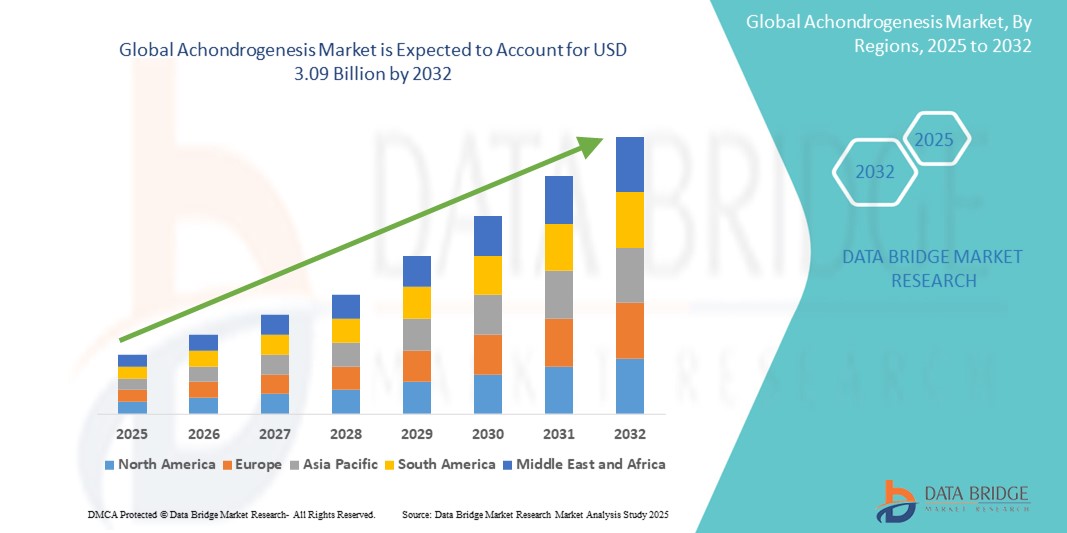

3.09 Billion

2024

2032

USD

2.01 Billion

USD

3.09 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.01 Billion | |

| USD 3.09 Billion | |

| % | |

|

Achondrogenesis Market Size

- The global achondrogenesis market size was valued at USD 2.01 billion in 2024 and is expected to reach USD 3.09 billion by 2032, at a CAGR of 5.50% during the forecast period

- The market growth is largely driven by increasing awareness and diagnosis of rare skeletal disorders, along with advancements in prenatal screening and genetic testing technologies enabling early detection of achondrogenesis

- Furthermore, growing investments in orphan drug development and supportive regulatory pathways are encouraging pharmaceutical innovations targeting rare conditions. These aligned efforts are enhancing treatment accessibility and research, thereby supporting the expansion of the achondrogenesis market globally

Achondrogenesis Market Analysis

- Achondrogenesis, a rare genetic disorder affecting skeletal development, is drawing growing attention in the medical and pharmaceutical sectors due to its severe impact on prenatal and neonatal health and the need for early and accurate diagnosis through advanced imaging and genetic screening techniques

- The demand for achondrogenesis-related diagnostics and supportive care is primarily driven by increased awareness of rare diseases, expanding availability of prenatal testing, and improved access to specialized medical facilities and genetic counseling services

- North America dominated the achondrogenesis market with the largest revenue share of 39.1% in 2024, supported by advanced healthcare infrastructure, higher prevalence of genetic testing, and proactive initiatives in rare disease research and funding, with the U.S. witnessing significant growth in early diagnosis and patient management through collaborations between research institutions and biotech firms

- Asia-Pacific is expected to be the fastest growing region in the achondrogenesis market during the forecast period due to rising healthcare investments, growing awareness of genetic disorders, and increasing access to prenatal care and diagnostics across emerging economies such as China and India

- Type II segment dominated the achondrogenesis market with a market share of 48.8% in 2024, driven by its relatively higher prevalence compared to Type IA and IB, along with improved clinical recognition and research focus on its genetic causes, particularly COL2A1 gene mutations

Report Scope and Achondrogenesis Market Segmentation

|

Attributes |

Achondrogenesis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Achondrogenesis Market Trends

“Advancements in Prenatal Genetic Screening and Diagnostic Technologies”

- A significant and accelerating trend in the global achondrogenesis market is the rapid development and adoption of advanced prenatal diagnostic technologies, including next-generation sequencing (NGS), non-invasive prenatal testing (NIPT), and chromosomal microarray analysis. These innovations are enhancing the accuracy and timing of achondrogenesis diagnosis during early pregnancy stages

- For instance, companies such as Illumina and Natera are increasingly offering comprehensive genetic screening panels capable of detecting skeletal dysplasias such as achondrogenesis in utero, enabling earlier intervention and informed clinical decision-making

- Molecular diagnostics allow the identification of specific gene mutations such as COL2A1, aiding in precise differentiation between Type I and Type II achondrogenesis. These targeted tests not only facilitate early diagnosis but also support genetic counseling for affected families

- In addition, the integration of AI and machine learning into diagnostic platforms is enabling pattern recognition and predictive modeling for rare conditions, improving diagnostic workflows and outcome predictions. Research platforms are leveraging AI to analyze imaging and genetic data to support clinicians in diagnosing ultra-rare diseases such as achondrogenesis

- Hospitals and research centers are increasingly partnering with biotechnology firms to develop rare disease databases, further improving diagnostic accuracy and clinical understanding

- This trend toward early, precise, and tech-driven prenatal diagnostics is transforming the management of rare congenital disorders. As awareness grows and access to advanced diagnostic infrastructure improves, especially in developed regions, the demand for accurate screening tools is expected to drive innovation and growth in the achondrogenesis market

Achondrogenesis Market Dynamics

Driver

“Rising Focus on Rare Disease Research and Early Diagnosis Capabilities”

- The increasing global emphasis on rare disease awareness, funding, and research is a key driver propelling the achondrogenesis market. Government and non-profit organizations are supporting initiatives aimed at improving early diagnosis and access to care for individuals affected by rare skeletal disorders

- For instance, international alliances such as EURORDIS and the Rare Disease Clinical Research Network (RDCRN) are contributing to clinical trial networks and genetic research efforts that include conditions such as achondrogenesis

- Improved genetic counseling services and early diagnosis tools have led to greater identification of achondrogenesis cases during pregnancy, giving families critical time for decision-making and care planning

- Hospitals and specialized prenatal care centers are increasingly equipped with high-resolution ultrasound, molecular testing capabilities, and expert genetic consultation services—fostering early detection and multidisciplinary care approaches

- The rising number of academic collaborations and public-private partnerships is expected to further expand research and commercial investment in therapies and diagnostics, significantly boosting market opportunities for companies focusing on skeletal dysplasias

Restraint/Challenge

“Lack of Curative Treatment and Limited Awareness in Developing Regions”

- The absence of curative treatment options remains a significant challenge in the achondrogenesis market. Management is limited to supportive and palliative care, which can be emotionally and financially burdensome for families, particularly in low- and middle-income countries

- Due to the ultra-rare nature of the condition and the complexity of genetic diagnosis, there is limited awareness among healthcare providers in many developing regions, leading to underdiagnosis or misdiagnosis

- Furthermore, access to molecular genetic testing and prenatal diagnostic services is restricted in several parts of Asia, Africa, and Latin America, limiting early detection and counseling opportunities

- High costs associated with advanced genetic testing and lack of reimbursement policies in certain healthcare systems also act as barriers to wider market penetration

- Overcoming these challenges will require expanded global efforts in rare disease education, investments in healthcare infrastructure, and supportive policy frameworks that improve access to diagnostics and counseling services

- In addition, further research into therapeutic targets will be critical for the long-term evolution of the market

Achondrogenesis Market Scope

The market is segmented on the basis of type, diagnosis, treatment, end-users, and distribution channel

- By Type

On the basis of type, the achondrogenesis market is segmented into Type IA, Type IB, and Type II. The Type II segment dominated the market with the largest revenue share of 48.8% in 2024, primarily due to its comparatively higher occurrence and better clinical understanding. Type II is often linked to COL2A1 gene mutations, allowing for earlier and more accurate detection through molecular diagnostics. The segment benefits from a strong presence in genetic testing panels and a higher rate of confirmed diagnoses, contributing to its dominant share.

The Type IA segment is projected to witness the fastest growth rate from 2025 to 2032, supported by expanding research into rare skeletal disorders and increasing availability of advanced sequencing techniques. Enhanced awareness and growing interest in rare disease registries are also expected to drive deeper insights into less commonly diagnosed subtypes such as Type IA.

- By Diagnosis

On the basis of diagnosis, the achondrogenesis market is segmented into physical examination, molecular genetic testing, and biochemical testing. The molecular genetic testing segment held the largest market share of 45.7% in 2024, due to its critical role in confirming achondrogenesis by detecting specific genetic mutations. The increased use of next-generation sequencing and non-invasive prenatal testing (NIPT) has boosted the segment’s growth.

Biochemical testing is anticipated to grow at the fastest pace over the forecast period from 2025 to 2032, driven by improvements in metabolic screening techniques and the development of combined diagnostic approaches that support early detection in high-risk pregnancies.

- By Treatment

On the basis of treatment, the market is segmented into supportive therapy and palliative care. Supportive therapy dominated the segment with a market share of 59.4% in 2024, as it forms the core of current clinical management strategies, focusing on respiratory support, feeding assistance, and comfort care.

Palliative care is expected to see rising growth during forecast period from 2025 to 2032, due to the severity and incurable nature of the disease. Advancements in neonatal care and pain management are contributing to broader integration of specialized palliative services in hospital and home settings

- By End Users

On the basis of end-users, the achondrogenesis market is segmented into clinics, hospitals, diagnostic centers, research and academic institutions, and others. The hospital segment accounted for the largest share of 41.6% in 2024, driven by the presence of multidisciplinary teams, advanced diagnostic infrastructure, and the availability of genetic counseling. Hospitals also facilitate comprehensive prenatal and neonatal care, positioning them as the primary site for diagnosis and management.

The research and academic institutions segment is expected to grow rapidly during forecast period, due to increased investment in rare disease research and growing collaborations between academia and biotech firms focused on understanding and treating skeletal dysplasias

- By Distribution Channel

On the basis of distribution channel, the achondrogenesis market is segmented into direct tenders, hospital pharmacy, retail pharmacy, online pharmacy, and others. Hospital pharmacy led the market with the highest share of 38.9% in 2024, supported by centralized access to diagnostic kits, medications, and supportive care devices within hospital environments.

The online pharmacy segment is projected to witness the fastest CAGR from 2025 to 2032, driven by the expanding availability of specialized care products, greater convenience, and improved distribution logistics, especially in remote or underserved regions.

Achondrogenesis Market Regional Analysis

- North America dominated the achondrogenesis market with the largest revenue share of 39.1% in 2024, supported by advanced healthcare infrastructure, higher prevalence of genetic testing, and proactive initiatives in rare disease research and funding, with the U.S. witnessing significant growth in early diagnosis and patient management through collaborations between research institutions and biotech firms

- Consumers and healthcare providers in the region place high importance on prenatal care, early detection of congenital disorders, and availability of specialized medical expertise for rare genetic conditions such as achondrogenesis

- This high adoption is further supported by government initiatives, well-established reimbursement systems, and collaborations between hospitals, research institutions, and biotech firms, positioning North America as a leader in both clinical management and diagnostic advancement for rare skeletal disorders

U.S. Achondrogenesis Market Insight

The U.S. achondrogenesis market captured the largest revenue share of 79.2% in 2024 within North America, driven by advanced genetic testing infrastructure, early prenatal screening capabilities, and significant investment in rare disease research. The country’s strong network of specialized hospitals and academic institutions supports early diagnosis and multidisciplinary care for skeletal disorders. In addition, ongoing collaborations between biotechnology firms and federal research initiatives, such as those under the NIH Rare Diseases Clinical Research Network, are further propelling market development.

Europe Achondrogenesis Market Insight

The Europe achondrogenesis market is projected to expand at a steady CAGR throughout the forecast period, supported by national rare disease plans, universal healthcare systems, and increased access to prenatal diagnostic technologies. High public awareness and government funding for rare conditions contribute to a proactive approach in identifying and managing achondrogenesis. The region is also experiencing growth in collaborative research initiatives and biobanks, fostering the development of more accurate and accessible diagnostic pathways for congenital skeletal disorders.

U.K. Achondrogenesis Market Insight

The U.K. achondrogenesis market is anticipated to grow at a notable CAGR during the forecast period, driven by the country's National Genomic Healthcare Strategy and robust integration of genetic medicine into public health services. Rising awareness of rare skeletal disorders and increased access to early screening through the NHS are enhancing diagnosis rates. In addition, partnerships between universities and biotech companies are contributing to the development of more effective prenatal testing tools and data-driven research on ultra-rare conditions such as achondrogenesis.

Germany Achondrogenesis Market Insight

The Germany achondrogenesis market is expected to grow at a substantial CAGR over the forecast period, supported by its highly developed healthcare infrastructure and strong commitment to rare disease diagnostics. The country's emphasis on early-stage screening and personalized medicine, combined with a well-regulated reimbursement framework, is promoting adoption of advanced genetic testing. Moreover, research institutions and hospitals are actively participating in pan-European initiatives to enhance clinical understanding and treatment pathways for rare congenital disorders.

Asia-Pacific Achondrogenesis Market Insight

The Asia-Pacific achondrogenesis market is poised to grow at the fastest CAGR of 21.8% during the forecast period of 2025 to 2032, driven by growing investment in healthcare infrastructure, increasing birth rates, and a rise in prenatal care awareness across developing economies. Countries such as China, India, and Japan are adopting next-generation sequencing and expanding rare disease registries. Government initiatives promoting maternal and child health are further accelerating market demand, especially as prenatal diagnosis becomes more accessible to a broader population segment

Japan Achondrogenesis Market Insight

The Japan achondrogenesis market is gaining momentum due to the country’s advanced medical research environment and integration of precision medicine into clinical practice. Strong emphasis on prenatal health, combined with the widespread use of genetic counseling services, is driving early identification of rare skeletal conditions. In addition, Japan’s well-established public health insurance system supports access to diagnostics, making it a leading market for achondrogenesis-related testing and research in Asia.

India Achondrogenesis Market Insight

The India achondrogenesis market accounted for the largest revenue share in Asia Pacific in 2024, fueled by increasing availability of prenatal diagnostic services, rising public awareness of genetic conditions, and expanding private healthcare infrastructure. Rapid urbanization and government-led initiatives for maternal and child health, such as the National Health Mission, are supporting early intervention strategies. Furthermore, growing partnerships between domestic diagnostic firms and global biotech companies are enhancing access to affordable molecular testing, propelling market growth in the region.

Achondrogenesis Market Share

The achondrogenesis industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- F. Hoffmann La Roche Limited (Switzerland)

- Bio-Rad Laboratories, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Natera Inc. (U.S.)

- Cepheid (U.S.)

- ELITech Group (France)

- Autogenomics (U.S.)

- Sequenom (U.S.)

- GeneDx, Inc. (U.S.)

- 23andMe, Inc. (U.S.)

- Ambry Genetics (U.S.)

- Invitae Corporation (U.S.)

- Pathway Genomics (U.S.)

- Progenity, Inc. (U.S.)

- OmeCare (U.S.)

What are the Recent Developments in Global Achondrogenesis Market?

- In March 2024, Blueprint Genetics, a global leader in genetic diagnostics, expanded its rare disease testing portfolio to include enhanced panels for skeletal dysplasias such as achondrogenesis. This advancement aims to improve early detection and diagnostic accuracy through next-generation sequencing (NGS), enabling clinicians to identify gene mutations associated with Type I and Type II achondrogenesis. The update reflects the company's commitment to addressing diagnostic challenges in rare congenital disorders and supporting early intervention strategies

- In February 2024, Illumina, Inc., in collaboration with several European academic institutions, launched a multi-center research initiative focused on developing a more comprehensive genomic reference for skeletal dysplasias. The project aims to improve variant interpretation and clinical decision-making for ultra-rare disorders such as achondrogenesis, ultimately contributing to better patient outcomes through precise molecular diagnostics and genetic counseling

- In November 2023, PerkinElmer Genomics introduced an expanded whole-genome sequencing (WGS) service tailored for prenatal diagnosis, including conditions such as achondrogenesis. By offering faster turnaround times and deeper insights into rare genetic anomalies, the initiative addresses the need for comprehensive prenatal screening options in high-risk pregnancies and reinforces PerkinElmer’s role in advancing rare disease diagnostics

- In October 2023, Centogene N.V., a key player in rare disease diagnostics, partnered with healthcare providers across Asia-Pacific to increase access to genetic testing for underserved populations. The collaboration includes targeted outreach for skeletal dysplasia awareness and aims to improve early detection rates for conditions such as achondrogenesis through subsidized testing and physician training programs

- In August 2023, the National Organization for Rare Disorders (NORD) launched a new patient registry initiative specifically including skeletal dysplasias such as achondrogenesis. This registry is designed to collect clinical and genetic data from patients globally, fostering a better understanding of disease progression and supporting future research into therapeutic interventions. The move marks a significant step toward collaborative data-sharing in rare disease management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.