Global Angiotensin Converting Enzyme Ace Inhibitors Market

Market Size in USD Billion

USD

3.80 Billion

USD

5.57 Billion

2024

2032

USD

3.80 Billion

USD

5.57 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.80 Billion | |

| USD 5.57 Billion | |

| % | |

|

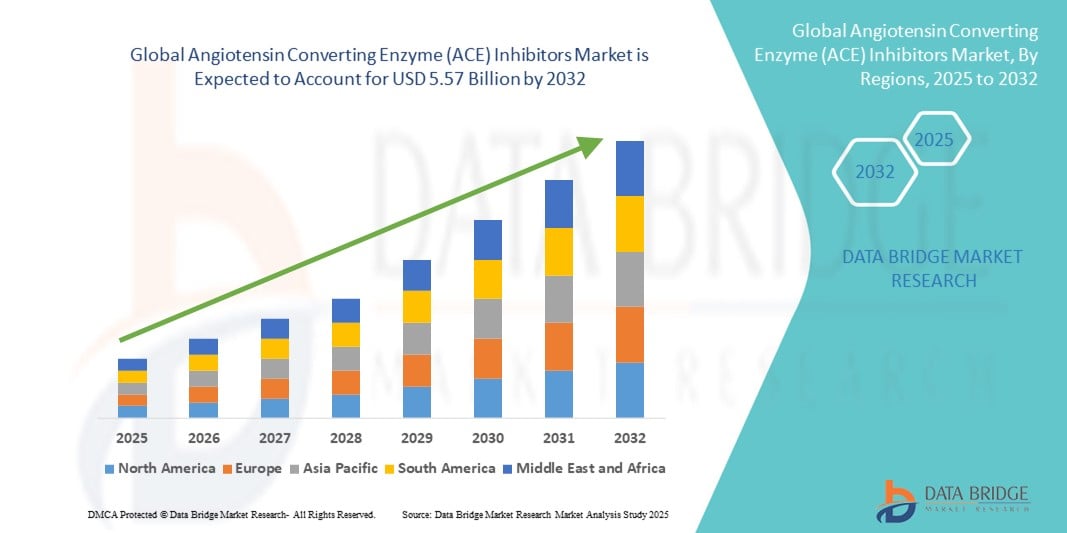

Angiotensin Converting Enzyme (ACE) Inhibitors Market Size

- The global Angiotensin Converting Enzyme (ACE) inhibitors market size was valued at USD 3.80 billion in 2024 and is expected to reach USD 5.57 billion by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is primarily driven by the increasing prevalence of cardiovascular diseases, hypertension, and diabetes worldwide, coupled with rising awareness about early diagnosis and management of these conditions

- Moreover, the continuous development of novel ACE inhibitors with improved efficacy, reduced side effects, and better patient compliance is enhancing treatment adoption across hospitals, clinics, and homecare settings. These factors are collectively driving the expansion of the ACE inhibitors market, positioning it as a key segment in the cardiovascular therapeutics landscape

Angiotensin Converting Enzyme (ACE) Inhibitors Market Analysis

- ACE inhibitors, a class of medications that relax blood vessels and reduce blood pressure, are increasingly essential in the management of hypertension, heart failure, and chronic kidney disease, offering improved patient outcomes and reduced cardiovascular risks in both outpatient and hospital settings

- The growing demand for ACE inhibitors is primarily driven by the rising prevalence of cardiovascular diseases, increasing awareness about hypertension management, and the expanding geriatric population with comorbidities that require long-term therapy

- North America dominated the Angiotensin Converting Enzyme (ACE) inhibitors market with the largest revenue share of 39.5% in 2024, characterized by high healthcare spending, well-established cardiovascular treatment protocols, and strong presence of key pharmaceutical players, with the U.S. experiencing significant adoption of combination therapies and novel ACE inhibitor formulations to enhance patient compliance and efficacy

- Asia-Pacific is expected to be the fastest growing region in the Angiotensin Converting Enzyme (ACE) inhibitors market during the forecast period due to increasing prevalence of cardiovascular disorders, improving healthcare infrastructure, and growing access to affordable generic medications

- Enalapril segment dominated the Angiotensin Converting Enzyme (ACE) inhibitors market with a market share of 33.2% in 2024, driven by its proven efficacy, favorable safety profile, and widespread physician preference for both monotherapy and combination therapy in hypertension and heart failure management

Report Scope and Angiotensin Converting Enzyme (ACE) Inhibitors Market Segmentation

|

Attributes |

Angiotensin Converting Enzyme (ACE) Inhibitors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Angiotensin Converting Enzyme (ACE) Inhibitors Market Trends

Personalized and Combination Therapy Adoption

- A significant trend in the global ACE inhibitors market is the increasing adoption of personalized treatment plans and combination therapies, tailored to patient-specific cardiovascular risk profiles, comorbidities, and genetic factors

- For instance, fixed-dose combinations of ACE inhibitors with diuretics or calcium channel blockers are being widely prescribed to improve blood pressure control and enhance patient adherence. Similarly, new formulations such as extended-release enalapril or lisinopril tablets offer more convenient dosing schedules for patients with chronic hypertension

- Integration with digital health tools, such as mobile apps and remote monitoring devices, allows healthcare providers to track patient response and adjust therapy in real-time, improving clinical outcomes. Some platforms provide alerts for missed doses and allow clinicians to monitor blood pressure trends remotely

- The growing emphasis on individualized therapy enables physicians to select ACE inhibitors based on efficacy, tolerability, and patient lifestyle factors, reducing adverse events and improving long-term cardiovascular management

- Pharmaceutical companies such as Novartis and Eli Lilly are focusing on developing combination therapies and digital adherence solutions, addressing both efficacy and convenience, which is shaping the future of ACE inhibitor therapy

- The demand for more effective, patient-centered treatment regimens is rising, driven by increased awareness of cardiovascular health, the prevalence of chronic diseases, and the need for optimized therapy adherence

Angiotensin Converting Enzyme (ACE) Inhibitors Market Dynamics

Driver

Rising Prevalence of Cardiovascular Diseases and Hypertension

- The increasing global incidence of hypertension, heart failure, and chronic kidney disease is a major driver for the ACE inhibitors market

- For instance, in March 2024, Pfizer launched an educational initiative promoting early detection and treatment of hypertension, encouraging the use of ACE inhibitors as first-line therapy. Such initiatives by key companies are expected to drive market adoption

- As awareness grows regarding the long-term risks of uncontrolled blood pressure, ACE inhibitors are increasingly prescribed to manage and prevent cardiovascular complications, boosting demand in both hospital and outpatient settings

- The aging population, rising obesity rates, and sedentary lifestyles further accelerate the need for effective blood pressure management, making ACE inhibitors a cornerstone in cardiovascular therapeutics

- Healthcare provider recommendations and guideline updates emphasizing ACE inhibitors for specific patient populations are also key factors propelling market growth

Restraint/Challenge

Adverse Effects and Regulatory Compliance Hurdles

- The safety concerns associated with ACE inhibitors, such as persistent cough, hyperkalemia, and rare angioedema, pose challenges to broader market adoption. Patients experiencing side effects may discontinue therapy, limiting market growth

- For instance, regulatory agencies in Europe and North America have issued warnings and dosage guidelines for high-risk patient groups, influencing prescribing practices and requiring careful monitoring

- Companies such as Merck and Takeda emphasize patient education, pharmacovigilance, and adherence monitoring to mitigate adverse effects and improve patient trust

- In addition, stringent regulatory approvals for new ACE inhibitor formulations, combination drugs, and generics can delay market entry and affect profitability

- Overcoming these challenges through safer formulations, patient education, post-marketing surveillance, and simplified dosing regimens is critical to sustaining growth and enhancing market acceptance

Angiotensin Converting Enzyme (ACE) Inhibitors Market Scope

The market is segmented on the basis of product type, drug, dosage form, application, and distribution channel.

- By Product Type

On the basis of product type, the Angiotensin Converting Enzyme (ACE) inhibitors market is segmented into dicarboxylate-containing agents, phosphonate-containing agents, and sulfhydryl-containing agents. The dicarboxylate-containing agents segment dominated the market with the largest revenue share of 46.3% in 2024, driven by their broad clinical efficacy, favorable safety profile, and widespread physician preference for treating hypertension and cardiovascular disorders. These agents are often prescribed due to proven long-term outcomes in reducing cardiovascular morbidity and mortality. In addition, their predictable pharmacokinetics, minimal drug-drug interactions, and cost-effectiveness make them a first-line choice in both developed and emerging markets. The strong clinical evidence supporting their use in chronic kidney disease and post-myocardial infarction patients further strengthens their market position. Furthermore, the availability of generic formulations enhances accessibility, fueling continued adoption globally.

The sulfhydryl-containing agents segment is anticipated to witness the fastest growth rate of 18.5% from 2025 to 2032, fueled by their unique therapeutic advantages, including additional antioxidant and vascular protective properties. These agents are increasingly recognized for managing heart failure, renal complications, and patients at higher cardiovascular risk. Rising awareness among physicians regarding the clinical benefits of sulfhydryl-containing ACE inhibitors, particularly in reducing oxidative stress and endothelial dysfunction, is also driving adoption. Ongoing research and development efforts focusing on improving formulations, bioavailability, and patient tolerability are likely to further accelerate market growth.

- By Drug

On the basis of drug, the Angiotensin Converting Enzyme (ACE) inhibitors market is segmented into lisinopril, ramipril, enalapril, benazepril, fosinopril, captopril, moexipril, and others. The enalapril segment dominated the market with a revenue share of 33.2% in 2024, driven by its well-established efficacy, favorable dosing schedule, and strong physician and patient trust. Enalapril is widely used across hypertension, heart failure, and chronic kidney disease therapies. Its extensive clinical trials and real-world evidence supporting long-term cardiovascular benefits have positioned it as a preferred choice in both hospital and outpatient settings. The availability of multiple generic versions and fixed-dose combinations enhances patient adherence and affordability. Additionally, enalapril’s broad geographical presence and inclusion in clinical guidelines for multiple indications support its dominant market share.

The ramipril segment is expected to witness the fastest CAGR from 2025 to 2032, due to rising adoption in high-risk cardiovascular patients and increasing use in combination therapy formulations. Ramipril is often preferred in patients with diabetes, post-myocardial infarction, or chronic kidney disease for its proven renal and cardiovascular protective effects. Physician awareness of its long-term survival benefits and favorable safety profile is expanding its prescription base. The availability of ramipril in combination with diuretics or calcium channel blockers for simplified treatment regimens is also driving adoption.

- By Dosage Form

On the basis of dosage form, the Angiotensin Converting Enzyme (ACE) inhibitors market is segmented into oral tablets and oral solutions. Oral tablets dominated the market with a share of 87.1% in 2024, driven by patient preference for convenient administration, dose flexibility, and long shelf life. Tablets are particularly favored in outpatient care and retail pharmacy settings due to their ease of use, portability, and established prescription patterns. The wide availability of generic tablets ensures affordability, supporting consistent market demand. Physicians often prescribe tablets due to standardized dosing and proven clinical efficacy. The convenience and patient familiarity of tablets make them the primary choice for long-term therapy across various age groups.

Oral solutions are expected to witness the fastest growth from 2025 to 2032, supported by rising demand from pediatric and geriatric populations who require adjustable or easy-to-swallow formulations. Oral solutions allow precise dosing, particularly for patients with difficulty swallowing tablets, including children and elderly patients. Hospitals and long-term care facilities increasingly prefer oral solutions for flexible dosing management. The segment benefits from innovations in palatability, stability, and packaging, enhancing patient compliance. Additionally, increasing awareness about personalized medicine and patient-centric care supports the adoption of oral solution formulations.

- By Application

On the basis of application, the Angiotensin Converting Enzyme (ACE) inhibitors market is segmented into heart failure, hypertension, diabetes, heart attack, chronic kidney disease, and others. The hypertension segment dominated the market with a revenue share of 42.5% in 2024, driven by the high prevalence of hypertension globally and the critical role of ACE inhibitors as first-line therapy. Rising awareness of hypertension complications, increasing health check-ups, and improved diagnosis rates are further driving the segment. ACE inhibitors are preferred for their proven efficacy, renal protection, and tolerability in hypertensive patients. Their inclusion in treatment guidelines across multiple countries ensures consistent prescription trends.

The heart failure segment is projected to register the fastest growth rate during the forecast period, owing to increasing clinical adoption for reducing hospitalization rates and improving patient survival. ACE inhibitors are now recognized as essential in heart failure management due to their role in improving cardiac output and reducing ventricular remodeling. Rising prevalence of chronic cardiovascular diseases, particularly in aging populations, is boosting the segment. Moreover, combination therapies with beta-blockers and diuretics enhance therapeutic outcomes, driving physician preference.

- By Distribution Channel

On the basis of distribution channel, the Angiotensin Converting Enzyme (ACE) inhibitors market is segmented into retail pharmacy, hospital pharmacy, e-commerce websites, and online drug stores. Retail pharmacies held the largest market share of 45.6% in 2024, driven by widespread accessibility, trusted pharmacist guidance, and insurance coverage for prescription medications. Retail pharmacies remain the preferred channel for patients due to personal consultation, immediate availability, and familiarity. Pharmacies in urban and semi-urban regions ensure coverage for chronic care patients. Strategic collaborations between pharmaceutical companies and retail chains are also boosting product reach.

E-commerce websites are expected to witness the fastest growth from 2025 to 2032, fueled by the rising trend of online prescription fulfillment, convenience, and increasing adoption of digital health platforms. Online platforms offer home delivery, subscription services, and access to patient reviews, enhancing patient engagement. Growing smartphone penetration and secure payment options are further boosting online sales. E-commerce also provides reach to remote areas where retail pharmacies are limited.

Angiotensin Converting Enzyme (ACE) Inhibitors Market Regional Analysis

- North America dominated the Angiotensin Converting Enzyme (ACE) inhibitors market with the largest revenue share of 39.5% in 2024, characterized by high healthcare spending, well-established cardiovascular treatment protocols, and strong presence of key pharmaceutical players, with the U.S. experiencing significant adoption of combination therapies and novel ACE inhibitor formulations to enhance patient compliance and efficacy

- Patients and healthcare providers in the region prioritize clinically proven therapies, treatment adherence, and the availability of a wide range of ACE inhibitor formulations, which has bolstered market adoption

- This dominance is further supported by high healthcare expenditure, advanced diagnostic capabilities, strong presence of key pharmaceutical players, and government initiatives promoting early detection and management of cardiovascular disorders, establishing ACE inhibitors as a preferred choice for managing hypertension, heart failure, and chronic kidney disease

U.S. Angiotensin Converting Enzyme (ACE) Inhibitors Market Insight

The U.S. Angiotensin Converting Enzyme (ACE) inhibitors market captured the largest revenue share of 79% in 2024 within North America, fueled by the high prevalence of hypertension, heart failure, and chronic kidney disease. Patients and healthcare providers increasingly prioritize clinically proven therapies, adherence to treatment, and availability of a wide range of formulations. The growing adoption of combination therapies, alongside supportive government health initiatives and cardiovascular awareness programs, further propels market growth. In addition, advancements in digital health platforms for patient monitoring and prescription management are significantly contributing to the expansion of the U.S. ACE inhibitors market.

Europe ACE Inhibitors Market Insight

The Europe Angiotensin Converting Enzyme (ACE) inhibitors market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of cardiovascular disorders and increasing awareness about early detection and management. The increase in urbanization, coupled with the demand for effective chronic disease management, is fostering the adoption of ACE inhibitors. European patients and healthcare providers also value treatment efficacy, safety, and physician-preferred formulations. The region is witnessing significant growth across hospital and outpatient settings, with ACE inhibitors being widely prescribed for both new and ongoing therapy management.

U.K. ACE Inhibitors Market Insight

The U.K. Angiotensin Converting Enzyme (ACE) inhibitors market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing cases of hypertension, heart failure, and diabetic nephropathy. Moreover, growing awareness regarding the benefits of early intervention and guideline-recommended therapies is encouraging both healthcare providers and patients to prefer ACE inhibitors. The U.K.’s well-developed healthcare infrastructure, along with strong prescription coverage and e-pharmacy adoption, is expected to continue supporting market expansion.

Germany ACE Inhibitors Market Insight

The Germany Angiotensin Converting Enzyme (ACE) inhibitors market is expected to expand at a considerable CAGR during the forecast period, fueled by rising cardiovascular disease prevalence and strong emphasis on preventive healthcare. Germany’s advanced medical infrastructure, coupled with stringent regulatory standards and focus on patient safety, promotes the adoption of ACE inhibitors in hospital and outpatient settings. The integration of digital health records and telemedicine for therapy monitoring is also enhancing treatment adherence and supporting market growth.

Asia-Pacific ACE Inhibitors Market Insight

The Asia-Pacific Angiotensin Converting Enzyme (ACE) inhibitors market is poised to grow at the fastest CAGR of 22% during the forecast period of 2025 to 2032, driven by increasing prevalence of hypertension and cardiovascular diseases, growing geriatric population, and improving healthcare infrastructure in countries such as China, India, and Japan. Government initiatives promoting chronic disease management, expanding health insurance coverage, and increasing affordability of generic ACE inhibitors are driving adoption. Furthermore, rising awareness of cardiovascular health and the growing number of hospital and outpatient facilities are expanding access to ACE inhibitor therapies across the region.

Japan ACE Inhibitors Market Insight

The Japan Angiotensin Converting Enzyme (ACE) inhibitors market is gaining momentum due to the country’s aging population, high incidence of cardiovascular disorders, and emphasis on preventive healthcare. The Japanese market values therapies with proven efficacy and favorable safety profiles, resulting in strong adoption of ACE inhibitors for hypertension, heart failure, and chronic kidney disease management. Integration of digital health monitoring systems and home healthcare solutions is also supporting adherence and patient outcomes, fueling market growth.

India ACE Inhibitors Market Insight

The India Angiotensin Converting Enzyme (ACE) inhibitors market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rising prevalence of hypertension, increasing cardiovascular disease awareness, and expanding healthcare infrastructure. India’s growing urban population, expanding middle class, and rising accessibility of generic ACE inhibitors are key factors propelling market growth. In addition, government health initiatives, increasing adoption of outpatient and telemedicine services, and availability of cost-effective treatment options are driving the widespread use of ACE inhibitors in both residential and commercial healthcare settings.

Angiotensin Converting Enzyme (ACE) Inhibitors Market Share

The Angiotensin Converting Enzyme (ACE) Inhibitors industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson and its affiliates (U.S.)

- Merck & Co., Inc. (U.S.)

- Sanofi (France)

- Bayer AG (Germany)

- AstraZeneca (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- GSK plc (U.K.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Bristol-Myers Squibb Company (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Daiichi Sankyo Company, Ltd. (Japan)

- UCB Pharma (Belgium)

- Endo International plc (Ireland)

- Sun Pharmaceutical Industries Ltd. (India)

- Cadila Pharmaceuticals (India)

- Lupin Pharmaceuticals, Inc. (India)

- Emcure Pharmaceuticals Limited (India)

What are the Recent Developments in Global Angiotensin Converting Enzyme (ACE) Inhibitors Market?

- In July 2025, the U.S. Food and Drug Administration (FDA) approved Vostally, an oral solution formulation of the ACE inhibitor ramipril. Developed by Rosemont Pharmaceuticals Inc., Vostally is indicated for the treatment of hypertension and for reducing the risk of cardiovascular events. This new formulation provides an alternative for patients who may have difficulty swallowing tablets, potentially improving adherence and making the drug more accessible to a wider range of individuals

- In April 2025, the FDA approved Vanrafia (atrasentan) to reduce proteinuria in adults with primary immunoglobulin A nephropathy (IgAN) at risk of rapid disease progression. While Vanrafia is not an ACE inhibitor, this approval is a significant development in the broader cardiorenal and kidney disease treatment landscape. It highlights the continued focus on developing novel therapies to manage conditions that are often treated with ACE inhibitors, and suggests a growing market for targeted therapies for specific patient populations

- In November 2021, In a major development concerning drug access and supply chain resilience, New Zealand's national drug procurement agency announced that as of May 2021, the ACE inhibitor cilazapril would no longer be funded for new patients. Existing patients were also being encouraged to switch to alternative ACE inhibitors, with the drug scheduled for complete delisting by the end of 2023

- In July 2021, A large observational study reported that Angiotensin Receptor Blockers (ARBs) are preferable to ACE inhibitors in treating hypertension due to a lower incidence of side effects such as cough and angioedema. This finding may influence prescribing practices and patient outcomes

- In May 2021, a report from the World Health Organization (WHO), which analyzed 11 observational studies, concluded that ACE inhibitors did not have detrimental effects in relation to COVID-19. This followed earlier concerns during the pandemic that these medications might increase susceptibility to the virus

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.