Global Animal Based Pet Food Ingredients Market

Market Size in USD Billion

USD

43.06 Billion

USD

72.34 Billion

2025

2033

USD

43.06 Billion

USD

72.34 Billion

2025

2033

| 2026 - 2033 | |

| USD 43.06 Billion | |

| USD 72.34 Billion | |

| % | |

|

Animal Based Pet Food Ingredients Market Overview

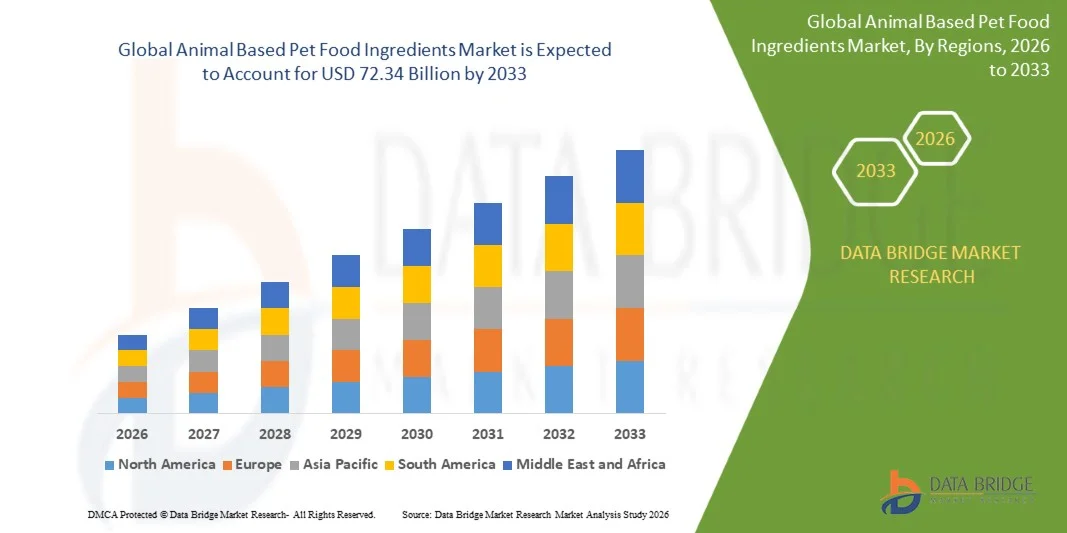

The Animal Based Pet Food Ingredients Market was valued at USD 43.06 billion in 2025 and is projected to reach USD 72.34 billion by 2033, growing at a CAGR of 6.70% from 2026 to 2033. The market is witnessing consistent and robust growth driven by rising global pet ownership rates, increasing humanization of pets, and growing consumer preference for high-protein and nutritionally superior pet food products formulated with premium animal-based ingredients. Growing awareness among pet owners regarding the health benefits of animal-derived proteins, fats, and essential nutrients for companion animals is significantly accelerating demand for quality animal based pet food ingredient solutions across dog, cat, fish, and other pet categories.

The rapid premiumization of the global pet food industry is compelling manufacturers to source high-quality animal-based ingredients including meat meals, rendered fats, hydrolyzed proteins, and specialty proteins derived from poultry, beef, pork, fish, and other animal sources. Increasing veterinary recommendations for protein-rich and grain-free diets for dogs and cats, combined with the rapid expansion of e-commerce pet food retail and specialty pet nutrition outlets, is further boosting adoption of diverse animal-based ingredient formulations. In addition, the growing demand for functional pet food products addressing specific health conditions such as digestive sensitivity, joint health, and immune support is driving innovation in hydrolyzed and blended protein ingredient development across the global pet food industry.

Key Market Trends & Insights

- North America dominated the animal based pet food ingredients market with the largest revenue share of approximately 38.4% in 2025, supported by high per-capita pet ownership rates, strong consumer willingness to spend on premium pet nutrition, and the presence of major pet food manufacturers actively sourcing high-quality animal-based ingredient solutions. Well-established pet food retail infrastructure and strong veterinary endorsement of protein-rich pet diets further consolidate regional market leadership.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 8.3% from 2026 to 2033. Growth is driven by rising pet adoption rates across China, Japan, South Korea, and India, increasing disposable incomes enabling premiumization of pet food spending, and expanding awareness of animal-based nutrition benefits for companion animal health and longevity.

- The Dry Pet Food form segment held the largest market revenue share of approximately 41.2% in 2025, driven by widespread consumer preference for convenient, shelf-stable dry pet food formulations incorporating meat meals, rendered proteins, and animal fat ingredients. High market penetration of dry kibble products in both dog and cat food categories globally supports dominant segment performance.

- The Treats and Snacks form segment is projected to register the fastest growth at a CAGR of around 8.6% from 2026 to 2033, driven by rising consumer spending on premium functional pet treats, growing humanization of pet feeding habits, and increasing demand for high-protein, single-ingredient animal-based treat products across dog and cat categories.

- The Meat and Meat Products ingredient segment held the largest market revenue share of approximately 58.3% in 2025, reflecting the foundational role of meat-derived proteins, meat meals, and meat by-products in commercial pet food formulations across all pet food forms and categories globally.

- The Fats ingredient segment is expected to grow steadily, driven by increasing use of animal-derived fats as a concentrated energy source, palatability enhancer, and carrier of fat-soluble vitamins in dry and wet pet food formulations across dog and cat product lines.

- The Dog pet segment accounted for the largest market share of approximately 46.7% in 2025 due to the massive global dog ownership base and high average spending on premium dog food products. Rising demand for breed-specific and life-stage-specific dog food formulations incorporating diverse animal-based proteins is further supporting dominant segment performance.

- The Cat pet segment is expected to grow at the fastest CAGR of around 7.4% from 2026 to 2033, supported by rapidly rising cat ownership rates globally, growing consumer preference for high-protein wet cat food formulations rich in animal-based ingredients, and increasing awareness of obligate carnivore nutritional requirements for feline health.

- The Poultry Protein type segment held the largest market revenue share of approximately 27.6% in 2025, driven by the widespread use of chicken and turkey meal, poultry fat, and poultry by-product meal as cost-effective, highly digestible, and palatable animal protein sources across all major commercial pet food categories globally.

- The Hydrolyzed Proteins type segment is projected to register the fastest growth at a CAGR of around 9.1% from 2026 to 2033, driven by rising prevalence of pet food allergies and sensitivities, increasing veterinary prescription of hydrolyzed protein-based elimination diets, and growing consumer awareness of the digestive health benefits of enzymatically processed animal proteins for companion animals.

Market Size & Forecast

- Global Market Value (2025): USD 43.06 Billion

- Expected Market Value (2033): USD 72.34 Billion

- Forecast CAGR (2026–2033): 6.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Animal Based Pet Food Ingredients Market Segmentation

|

Attributes |

Animal Based Pet Food Ingredients Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Darling Ingredients Inc. (U.S.) |

|

Market Opportunities |

• Growing Demand for Premium and Functional Animal-Based Pet Food Ingredients Supporting Product Innovation • Expansion of Hydrolyzed and Specialty Protein Ingredient Applications in Veterinary Diet and Sensitive Pet Food Formulations |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Animal Based Pet Food Ingredients Market Trends

Trend: Rising Pet Humanization and Growing Consumer Demand for Premium Animal-Based Nutrition

Increasing humanization of pets across developed and rapidly developing economies is fundamentally reshaping the global pet food industry, with pet owners increasingly seeking nutritionally superior food products formulated with high-quality animal-based ingredients that mirror the protein-rich diets they provide for themselves. This cultural shift is driving sustained demand for premium pet food formulations incorporating whole meats, fresh meat meals, specialty animal proteins, and high-quality rendered fats, compelling pet food manufacturers to source and develop more sophisticated animal-based ingredient portfolios.

In the dog food category, the transition from generic cereal-based formulations to meat-first, high-protein recipes is well advanced across North American and European markets, with leading retailers reporting strong consumer preference for dog food products listing named meat proteins such as chicken, beef, salmon, or lamb as primary ingredients. For instance, major pet food brands including Blue Buffalo, Hill’s Science Diet, and Royal Canin have significantly expanded their animal-based protein ingredient sourcing programs to meet growing consumer demand for authentic and traceable meat-derived ingredient solutions. Similarly, the rapid expansion of raw and freeze-dried pet food segments is creating new high-value application opportunities for premium animal-based ingredient suppliers.

The growing emphasis on functional nutrition in pet food is also accelerating innovation in specialized animal-based ingredient applications, including hydrolyzed proteins for hypoallergenic diets, organ meats and glandular ingredients for nutrient density, and marine-derived ingredients rich in omega-3 fatty acids for cognitive and joint health support. Industry data from 2024 indicates that premium and super-premium pet food segments, which heavily rely on quality animal-based ingredients, are growing at nearly twice the rate of the overall pet food market, underscoring the strong commercial opportunity for ingredient suppliers capable of meeting evolving nutritional and quality standards.

Animal Based Pet Food Ingredients Market Dynamics

Key Market Driver: Rising Global Pet Ownership and Premiumization of Pet Food Spending

The sustained global increase in pet ownership, particularly among millennials and Gen Z consumers who exhibit strong humanization tendencies toward companion animals, is creating a growing and increasingly sophisticated consumer base for premium pet food products incorporating high-quality animal-based ingredients. Rising disposable incomes in both developed and emerging markets are enabling pet owners to allocate greater spending toward nutritionally superior pet food formulations, directly driving ingredient quality upgrades across the pet food manufacturing value chain.

Commercial pet food manufacturers across North America, Europe, and Asia-Pacific are responding to premiumization trends by reformulating core product lines with named meat proteins, fresh or frozen meat inclusions, and specialty animal-derived ingredients that command consumer trust and premiums at retail. For instance, the U.S. pet food market has experienced consistent annual growth in the premium and super-premium segment over the past decade, with animal protein content and ingredient quality ranking among the top purchasing decision factors for dog and cat food buyers. The expanding availability of premium pet food products through e-commerce channels is further democratizing access to high-quality animal-based pet food formulations across diverse geographic markets.

Market data from 2024 indicates that the global pet food market exceeded USD 130 billion in total retail value, with animal-based ingredients representing the single largest cost component in premium pet food formulations. The accelerating transition from economy-tier to premium pet food categories across key Asian markets including China, Japan, and South Korea is expected to generate substantial incremental demand for quality animal-based ingredients through 2033, presenting significant growth opportunities for established and emerging ingredient suppliers serving the global pet food industry.

Key Restraint/Challenge: Raw Material Price Volatility and Supply Chain Traceability Requirements

The animal based pet food ingredients market faces significant challenges related to raw material price volatility driven by fluctuating livestock production costs, feed grain prices, and rendering capacity constraints across major meat-producing regions. Price volatility in key animal-based ingredient categories including poultry meal, beef meal, fish meal, and animal fats can significantly impact pet food manufacturing margins and complicate long-term ingredient procurement planning for both large and mid-tier pet food brands.

In addition, growing consumer and regulatory demand for ingredient transparency, supply chain traceability, and ethical sourcing documentation is increasing operational complexity and compliance costs for animal-based ingredient suppliers. Retailers and pet food brands are increasingly requiring detailed provenance data, third-party quality certifications, and documented welfare standards for animal-based ingredient suppliers, creating barriers for smaller players and requiring significant investment in supply chain management systems and audit infrastructure.

Industry assessments indicate that sourcing disruptions and price increases in key animal-based ingredient categories can result in meaningful pet food product reformulations, potential quality compromises, or consumer price increases that negatively impact purchase frequency, particularly in value and mid-tier pet food market segments that exhibit higher price sensitivity compared to premium product categories.

Key Market Opportunity: Expanding Applications for Hydrolyzed and Specialty Proteins in Veterinary and Functional Pet Diets

The growing global prevalence of pet food allergies, sensitivities, and diet-related health conditions is creating significant commercial opportunities for animal-based ingredient suppliers specializing in hydrolyzed protein production, novel protein sourcing, and specialty ingredient development. Veterinary prescription of hydrolyzed protein elimination diets for dogs and cats with confirmed food allergies is increasing substantially, driving premium pricing and strong loyalty in veterinary channel sales for hydrolyzed animal protein ingredient suppliers.

The expanding market for functional and condition-specific pet food formulations addressing joint health, digestive wellness, weight management, and immune support is creating new application opportunities for specialized animal-based ingredients including collagen hydrolysates, chondroitin from marine and bovine sources, omega-3-rich fish oils, and targeted organ meat ingredients. In 2025, several leading pet food brands introduced new veterinary diet product lines featuring novel hydrolyzed protein sources such as hydrolyzed duck, hydrolyzed salmon, and hydrolyzed egg, supported by clinical evidence of improved tolerance in sensitized companion animals. Industry projections indicate that the veterinary diet and functional pet food segment could account for over 20% of total pet food market value by 2030, representing a high-margin growth frontier for specialized animal-based ingredient developers and suppliers.

Animal Based Pet Food Ingredients Market Scope

The Animal Based Pet Food Ingredients Market is segmented on the basis of form, ingredient, pet, and type.

• By Form

On the basis of form, the animal based pet food ingredients market is segmented into Dry Pet Food, Wet Pet Food, Veterinary Diets, Treats and Snacks, and Other Products. The Dry Pet Food segment held the largest market revenue share of approximately 41.2% in 2025, driven by widespread consumer preference for convenient, shelf-stable dry pet food formulations incorporating meat meals, rendered proteins, and animal fat ingredients. High market penetration of dry kibble products in both dog and cat food categories globally, combined with cost-effectiveness and ease of storage, supports dominant segment performance across retail and e-commerce distribution channels.

The Treats and Snacks segment is projected to register the fastest growth at a CAGR of around 8.6% from 2026 to 2033, driven by rising consumer spending on premium functional pet treats, growing humanization of pet feeding habits, increasing demand for high-protein, single-ingredient animal-based treat products, and expanding availability of innovative meat-based treat formats including jerky strips, freeze-dried meat bites, and dental chews across dog and cat categories.

• By Ingredient

On the basis of ingredient, the market is segmented into Meat and Meat Products, Fats, and Additives. The Meat and Meat Products segment held the largest market revenue share of approximately 58.3% in 2025, reflecting the foundational role of meat-derived proteins, meat meals, and meat by-products as the primary protein and amino acid sources in commercial pet food formulations across all pet food forms and categories. Growing consumer preference for meat-first pet food recipes and increasing inclusion of fresh and frozen meat ingredients in premium formulations further reinforce dominant segment positioning.

The Fats segment is expected to witness steady and sustained growth through 2033, driven by increasing use of animal-derived fats including poultry fat, beef tallow, and fish oil as concentrated energy sources, palatability enhancers, and carriers of fat-soluble vitamins in dry and wet pet food formulations. The growing recognition of specific animal fats’ functional benefits, including omega-3 fatty acids from fish oil for coat health and cognitive function support, is also driving formulation innovation and ingredient premiumization within this segment.

• By Pet

On the basis of pet, the market is segmented into Dog, Cat, Fish, and Others. The Dog segment accounted for the largest market share of approximately 46.7% in 2025 due to the massive global dog ownership base and high average consumer spending on premium dog food products. Rising demand for breed-specific, life-stage-specific, and health-condition-specific dog food formulations incorporating diverse and high-quality animal-based proteins is further driving dominant segment performance across multiple form and type categories.

The Cat segment is expected to grow at the fastest CAGR of around 7.4% from 2026 to 2033, supported by rapidly rising cat ownership rates globally, growing consumer preference for high-protein wet cat food formulations rich in animal-based ingredients, and increasing awareness of obligate carnivore nutritional requirements. The strong alignment between feline biological protein requirements and animal-based ingredient profiles positions the cat segment as a structurally high-growth application area for premium ingredient suppliers.

• By Type

On the basis of type, the market is segmented into Beef Proteins, Egg Proteins, Blended Proteins, Hydrolyzed Proteins, Pork Protein, Fish Protein, Poultry Protein, Ovine Proteins, Cervine Proteins, and Other Animal Proteins. The Poultry Protein segment held the largest market revenue share of approximately 27.6% in 2025, driven by the widespread use of chicken and turkey meal, poultry fat, and poultry by-product meal as cost-effective, highly digestible, and palatable animal protein sources across all major commercial pet food categories globally. Strong poultry supply chain infrastructure and broad consumer and pet acceptance of poultry-based ingredients reinforce segment leadership.

The Hydrolyzed Proteins segment is projected to register the fastest growth at a CAGR of around 9.1% from 2026 to 2033, driven by rising prevalence of pet food allergies and sensitivities, increasing veterinary prescription of hydrolyzed protein-based elimination diets, expanding consumer awareness of the digestive health benefits of enzymatically processed animal proteins, and growing investment by pet food manufacturers in hypoallergenic and limited-ingredient diet product development for sensitive companion animals.

Animal Based Pet Food Ingredients Market Regional Analysis

North America Animal Based Pet Food Ingredients Market Insight

North America dominated the animal based pet food ingredients market with the largest revenue share of 38.4% in 2025, supported by high per-capita pet ownership rates, strong consumer willingness to invest in premium pet nutrition, and the presence of a sophisticated pet food manufacturing ecosystem actively sourcing high-quality animal-based ingredient solutions. The region benefits from a well-established rendering and animal protein processing industry, robust veterinary nutrition infrastructure, and strong retail and e-commerce distribution channels for premium pet food products. Continuous product innovation by leading pet food brands and growing consumer awareness of ingredient quality and transparency further consolidate North America’s leadership position in the global market.

U.S. Animal Based Pet Food Ingredients Market Insight

The U.S. animal based pet food ingredients market captured the largest revenue share in North America in 2025, driven by the country’s position as the world’s largest pet food market and home to numerous leading pet food brands and specialty ingredient suppliers. Strong consumer demand for transparent, high-protein, and natural pet food formulations is driving significant investment in premium animal-based ingredient sourcing, including named meat proteins, fresh meat inclusions, and specialty animal-derived ingredients. The rapid growth of direct-to-consumer and subscription-based premium pet food brands is further accelerating demand for innovative and diverse animal-based ingredient solutions across dog and cat food categories.

Europe Animal Based Pet Food Ingredients Market Insight

The Europe animal based pet food ingredients market is expected to witness steady growth from 2026 to 2033, driven by high pet ownership rates in Western European markets, strong consumer preference for natural and sustainably sourced pet food ingredients, and stringent European Union regulations governing pet food ingredient quality and labeling transparency. Growing adoption of premium and functional pet food products incorporating certified animal-based ingredients, combined with increasing interest in novel protein sources such as insect protein and sustainable fish ingredients, is supporting market evolution across the region. Expansion of specialized veterinary diet distribution through veterinary clinics and online channels is also contributing to demand growth for high-quality animal-based ingredients.

U.K. Animal Based Pet Food Ingredients Market Insight

The U.K. animal based pet food ingredients market is expected to witness steady growth from 2026 to 2033, driven by high companion animal ownership rates, strong consumer interest in natural and grain-free pet food formulations, and increasing pet food premiumization trends across dog and cat food categories. The U.K.’s well-established pet specialty retail network and growing e-commerce pet food market are supporting broader consumer access to premium animal-based pet food products. Post-Brexit regulatory alignment is also influencing ingredient sourcing strategies for U.K. pet food manufacturers, creating opportunities for domestic and alternative international animal-based ingredient suppliers.

Germany Animal Based Pet Food Ingredients Market Insight

The Germany animal based pet food ingredients market is expected to witness strong growth from 2026 to 2033, supported by one of Europe’s largest pet populations, high consumer spending on premium pet nutrition, and strong regulatory and consumer emphasis on pet food ingredient quality, traceability, and ethical sourcing. German pet owners exhibit strong preference for natural, high-meat-content pet food formulations, driving sustained demand for quality animal-based proteins and fats. The country’s robust meat processing and rendering industry provides strong ingredient supply infrastructure supporting local and export-oriented pet food ingredient production.

Asia-Pacific Animal Based Pet Food Ingredients Market Insight

The Asia-Pacific animal based pet food ingredients market is expected to witness the fastest growth rate from 2026 to 2033, recording a CAGR of approximately 8.3%, supported by rapidly rising pet ownership rates across China, Japan, South Korea, India, and Southeast Asian economies, increasing consumer disposable incomes enabling premium pet food adoption, and expanding awareness of animal-based nutrition benefits for companion animal health. The rapid development of organized pet specialty retail and online pet food commerce platforms is improving consumer access to premium pet food products and driving ingredient quality upgrades among regional pet food manufacturers.

Japan Animal Based Pet Food Ingredients Market Insight

The Japan animal based pet food ingredients market is expected to witness steady growth from 2026 to 2033, driven by a mature pet ownership culture with high per-capita spending on premium pet food products, strong consumer demand for natural and functionally differentiated pet food formulations, and well-developed pet specialty retail and veterinary channel distribution infrastructure. Japanese pet food consumers exhibit strong preference for high-quality, safe, and traceably sourced animal-based ingredients, driving premium ingredient adoption. The country’s sophisticated pet food manufacturing industry and culture of ingredient quality innovation support continued market development across premium and functional pet food categories.

China Animal Based Pet Food Ingredients Market Insight

The China animal based pet food ingredients market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly expanding urban pet ownership base, accelerating premiumization of pet food spending among middle-class consumers, and significant growth of domestic pet food manufacturing capacity. Rising consumer awareness of pet nutrition and ingredient quality is driving strong demand for premium animal-based pet food formulations incorporating identifiable meat proteins and specialty ingredients. Government support for pet industry development and the rapid growth of e-commerce pet food retail platforms are further accelerating market expansion, making China the most significant growth market for animal-based pet food ingredient suppliers in the Asia-Pacific region.

Animal Based Pet Food Ingredients Market Share

The Animal Based Pet Food Ingredients industry is primarily led by well-established companies, including:

- Darling Ingredients Inc. (U.S.)

- Tyson Foods, Inc. (U.S.)

- Cargill, Incorporated (U.S.)

- Archer-Daniels-Midland Company (U.S.)

- SARIA Group (Germany)

- DIANA Pet Food (France)

- Nestle Purina PetCare (U.S.)

- AFB International (U.S.)

- Sonac B.V. (Netherlands)

- Kemin Industries, Inc. (U.S.)

- Omega Protein Corporation (U.S.)

- International Flavors and Fragrances Inc. (U.S.)

- Hamlet Protein A/S (Denmark)

- Griffith Foods (U.S.)

- Boyer Valley Company (U.S.)

Latest Developments in Animal Based Pet Food Ingredients Market

- In February 2025, Darling Ingredients Inc. (U.S.) announced the expansion of its premium pet food ingredient production capacity, adding new rendering and processing lines dedicated to high-specification poultry meal and poultry fat production for the global pet food market. The expansion is designed to meet growing demand from premium pet food manufacturers for consistent, high-quality animal-based protein and fat ingredients with full traceability and quality certification documentation.

- In December 2024, Cargill, Incorporated (U.S.) launched a new line of hydrolyzed animal protein ingredients specifically formulated for veterinary diet and hypoallergenic pet food applications, expanding its portfolio of functional animal-based ingredient solutions for the premium pet food sector. The new hydrolyzed protein range offers improved digestibility, reduced allergenic potential, and enhanced palatability characteristics validated through companion animal feeding trials.

- In October 2024, DIANA Pet Food (France) introduced an expanded range of natural flavor and palatability-enhancing ingredients derived from premium animal-based raw materials, targeting premium and super-premium pet food manufacturers seeking to improve product acceptance and feeding motivation across dog and cat food categories. The new ingredient range incorporates proprietary enzymatic processing technologies to optimize palatability performance while meeting clean-label formulation requirements.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Animal Based Pet Food Ingredients Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Animal Based Pet Food Ingredients Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Animal Based Pet Food Ingredients Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.