Global Antithrombin Market

Market Size in USD Billion

USD

876.92 Billion

USD

1,256.64 Billion

2025

2033

USD

876.92 Billion

USD

1,256.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 876.92 Billion | |

| USD 1,256.64 Billion | |

| % | |

|

Antithrombin Market Size

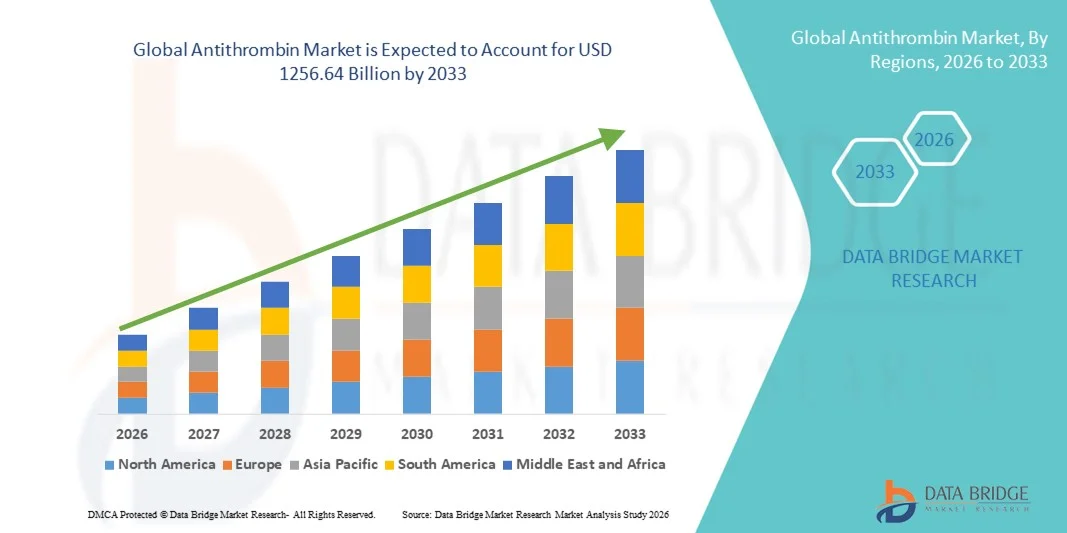

- The global antithrombin market size was valued at USD 876.92 billion in 2025 and is expected to reach USD 1256.64 billion by 2033, at a CAGR of 4.60% during the forecast period

- The market growth is largely fueled by the increasing prevalence of thrombotic disorders, rising awareness about anticoagulant therapies, and advancements in biopharmaceutical manufacturing, leading to greater adoption of antithrombin solutions in both clinical and hospital settings

- Furthermore, growing demand for safe and effective blood clot prevention therapies, coupled with increasing healthcare expenditure and expanding patient access to specialized treatments, is accelerating the uptake of Antithrombin solutions, thereby significantly boosting the industry's growth

Antithrombin Market Analysis

- Antithrombin, a vital protein in the human body, plays a crucial role in regulating blood coagulation and preventing excessive clot formation, making it essential in the treatment and management of thrombotic disorders in clinical and hospital settings

- The escalating demand for antithrombin solutions is primarily fueled by the rising prevalence of thrombotic disorders, increasing awareness about anticoagulant therapies, and growing adoption of advanced biologic and recombinant formulations in healthcare facilities

- North America dominated the antithrombin market with the largest revenue share of 41.8% in 2025, driven by advanced healthcare infrastructure, strong presence of key pharmaceutical companies, and extensive investment in anticoagulant therapy research, with the U.S. leading market expansion due to widespread adoption of innovative Antithrombin therapies

- Asia-Pacific is expected to be the fastest-growing region in the antithrombin market during the forecast period, registering a CAGR of 14.1%, fueled by increasing urbanization, rising healthcare spending, growing awareness of thrombotic disorders, and expanding access to advanced biologics and therapeutic solutions in countries like China, India, and Japan

- The Lyophilized segment dominated the largest market revenue share of 47.5% in 2025, owing to its superior stability, long shelf life, and suitability for storage and transportation in clinical settings

Report Scope and Antithrombin Market Segmentation

|

Attributes |

Antithrombin Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Antithrombin Market Trends

Enhanced Therapeutic Development and Clinical Adoption

- A significant trend in the global antithrombin market is the increasing focus on advanced therapeutic development and clinical application, driven by the growing prevalence of thrombotic disorders, hemophilia, and other coagulation-related conditions. This trend emphasizes innovations in recombinant technology, plasma-derived formulations, and novel delivery methods to enhance efficacy and patient outcomes.

- The market is witnessing rapid expansion in research and development activities aimed at producing next-generation antithrombin therapies, including improved bioavailability, extended half-life, and reduced immunogenicity. For instance, in March 2024, CSL Behring announced the launch of a recombinant antithrombin product in Europe, targeting high-risk surgical patients. Companies are increasingly collaborating with biotechnology firms, academic research institutions, and clinical laboratories to accelerate the development of highly effective and safer antithrombin products

- Enhanced patient-centric approaches are also shaping the market, with a focus on personalized medicine and tailored treatment regimens. Antithrombin therapies are being optimized to match specific patient profiles, improving therapeutic efficiency and reducing complications in critical care, surgical, and chronic treatment scenarios

- The demand for innovative antithrombin products is growing across both hospital and clinical settings, driven by the rising incidence of thrombotic and coagulation disorders, and the need for more reliable, consistent, and safe anticoagulant therapies. Emerging trends include the integration of real-world evidence, biomarker-driven approaches, and enhanced clinical trial designs to support regulatory approvals and broaden therapeutic indications

- Market expansion is supported by increasing investments in healthcare infrastructure, advanced diagnostic capabilities, and specialized treatment centers that facilitate the administration of antithrombin therapies. This is particularly evident in regions with high healthcare expenditure, growing awareness of coagulation disorders, and supportive government healthcare initiatives

- The adoption of novel delivery systems, such as subcutaneous formulations and long-acting recombinant variants, is enabling improved patient adherence, reduced hospitalization rates, and enhanced treatment convenience, further fueling market growth

Antithrombin Market Dynamics

Driver

Rising Prevalence of Thrombotic Disorders Driving Antithrombin Demand

- The primary driver of the antithrombin market is the rising prevalence of thrombotic disorders, hemophilia, and other coagulation-related diseases, which is creating a substantial demand for effective and targeted antithrombin therapies globally

- Increased awareness among healthcare professionals and patients regarding the importance of antithrombin in preventing complications, such as deep vein thrombosis, pulmonary embolism, and surgical bleeding, is driving the adoption of advanced antithrombin products

- For instance, the American Society of Hematology highlighted antithrombin replacement therapy in its 2024 clinical guidelines for high-risk patients

- Significant investment in research and development by pharmaceutical and biotechnology companies is enabling the launch of innovative antithrombin formulations and delivery platforms, catering to unmet medical needs and improving patient outcomes

- The expansion of specialized treatment centers, hospitals, and clinical laboratories, particularly in developed and emerging markets, is supporting the availability and accessibility of antithrombin therapies, facilitating broader adoption

- Ongoing clinical trials and regulatory approvals for next-generation antithrombin products are contributing to market growth by expanding therapeutic indications and improving treatment protocols for various coagulation disorders

- Strategic collaborations, partnerships, and mergers among key industry players are enhancing the development pipeline, strengthening distribution networks, and accelerating commercialization of innovative antithrombin therapies globally

Restraint/Challenge

Challenges and Barriers Limiting Antithrombin Market Growth

- The high cost of advanced antithrombin therapies can pose a barrier to adoption, particularly in price-sensitive and developing regions, limiting patient access to cutting-edge treatments

- Regulatory complexities and lengthy approval processes for new antithrombin formulations can delay market entry and affect timely availability to patients in need. For instance, the FDA’s extended review period for a recombinant antithrombin application in 2023 delayed commercialization in North America

- Safety concerns, potential adverse reactions, and immunogenicity risks associated with recombinant or plasma-derived antithrombin products may lead to cautious adoption by healthcare providers, impacting market growth

- Limited awareness and understanding of antithrombin therapy among patients in certain regions can restrict demand and hinder penetration, particularly in rural and underdeveloped areas

- Supply chain challenges, including dependency on plasma donations for plasma-derived antithrombin and maintaining quality standards during production, can affect consistent product availability and market expansion

- Addressing these challenges through cost optimization strategies, patient education initiatives, streamlined regulatory pathways, and enhanced production capabilities will be critical for sustaining long-term growth in the global Antithrombin market

Antithrombin Market Scope

The market is segmented on the basis of Technology Application, Source, and Dosage Form.

- By Technology Application

On the basis of technology application, the Antithrombin market is segmented into Therapeutics, Research, and Diagnostics. The Therapeutics segment dominated the largest market revenue share of 44.5% in 2025, driven by the growing prevalence of thrombotic disorders, increasing use of antithrombin in critical care, and the adoption of advanced treatment protocols in hospitals and specialty clinics. Hospitals and clinical centers prefer therapeutics due to its proven efficacy in preventing coagulation complications, while ongoing awareness campaigns by medical societies and health organizations further reinforce its adoption. In addition, insurance coverage and government reimbursement policies in developed regions contribute to the segment’s steady growth. The increasing number of surgeries, cardiovascular procedures, and high-risk patient populations further bolsters demand. Market leaders continue to expand production capacities and introduce improved formulations, enhancing patient outcomes and reliability. Continuous clinical studies highlighting benefits in personalized therapy also support the segment’s dominance. The integration of antithrombin therapeutics in standard treatment guidelines ensures sustained usage. Moreover, collaborations between hospitals and pharmaceutical manufacturers to ensure supply and training reinforce its leading position. Technological innovations in delivery methods and supportive care solutions enhance convenience for healthcare providers. Overall, the therapeutic application remains the cornerstone of antithrombin adoption worldwide, driving consistent market revenue.

The Research segment is expected to witness the fastest CAGR of 22.1% from 2026 to 2033, fueled by increased funding for coagulation and cardiovascular studies, expanding adoption in preclinical research, and rising collaboration between academic institutions and biotech companies. Research institutes are increasingly utilizing antithrombin in experimental protocols to explore novel therapies, biomarker identification, and molecular pathways. Growth is also supported by the integration of automated laboratory systems, high-throughput screening, and advanced analytical tools. Expanding biopharmaceutical R&D pipelines are incorporating antithrombin in translational research, especially in drug discovery and gene therapy studies. Governments and private funding agencies are emphasizing precision medicine research, accelerating demand. The emergence of recombinant antithrombin as a research tool further enhances accessibility and reduces dependence on plasma sources. In addition, the rise of contract research organizations (CROs) offering specialized antithrombin testing services contributes to segment expansion. Academic publications and conferences highlighting antithrombin research outcomes also boost adoption rates. The development of novel assay platforms for studying antithrombin mechanisms strengthens its research utility. Pharmaceutical companies increasingly invest in R&D collaborations with universities, creating a sustainable growth environment. Overall, research-focused applications are anticipated to record the highest growth momentum through the forecast period.

- By Source

On the basis of source, the Antithrombin market is segmented into Human, Goat Milk, and Others. The Human-derived antithrombin segment held the largest market revenue share of 46.2% in 2025, primarily due to its well-established efficacy, regulatory approval, and wide clinical acceptance. Hospitals and specialty clinics prefer human-derived antithrombin for critical care settings, particularly for high-risk patients, surgical procedures, and thrombosis management. Strong clinical data supporting consistent activity and safety profile further enhances adoption. Pharmaceutical manufacturers continue to invest in plasma collection and purification technologies to maintain supply stability. Developed regions with established healthcare infrastructure exhibit higher usage due to reimbursement policies and trained personnel. Ongoing clinical trials and post-market studies contribute to trust in human-derived formulations. The segment benefits from high adoption in cardiovascular and liver-related therapies where plasma-derived antithrombin is standard. Continuous improvement in pathogen inactivation and safety measures further strengthens market leadership. Strategic partnerships between plasma suppliers and healthcare institutions ensure steady supply and accessibility. In addition, growing awareness campaigns regarding anticoagulation therapies and thrombotic disorder management support demand. The human-derived segment remains the backbone of antithrombin therapeutics globally.

The Goat Milk-derived segment is expected to witness the fastest CAGR of 21.8% from 2026 to 2033, driven by innovations in recombinant protein production, cost-effective scalability, and growing preference for sustainable alternatives. Academic and pharmaceutical research centers increasingly adopt goat milk-derived antithrombin for experimental studies and therapeutic trials. Its use is expanding in emerging markets due to lower production costs, ease of large-scale bioprocessing, and reduced reliance on human plasma. Regulatory approvals and clinical validation of goat milk-derived products further stimulate market growth. Biotech startups focusing on recombinant antithrombin production are enhancing global supply. The segment also benefits from rising awareness about ethical sourcing and animal-friendly production methods. Collaboration with contract manufacturing organizations (CMOs) accelerates distribution to research labs and hospitals. The increasing number of studies validating efficacy and bioequivalence to human-derived products reinforces adoption. Expansion of local production facilities in Asia-Pacific and Latin America supports regional market growth. Overall, goat milk-derived antithrombin is poised to register significant momentum throughout the forecast period.

- By Dosage Form

On the basis of dosage form, the Antithrombin market is segmented into Lyophilized and Liquid. The Lyophilized segment dominated the largest market revenue share of 47.5% in 2025, owing to its superior stability, long shelf life, and suitability for storage and transportation in clinical settings. Hospitals prefer lyophilized antithrombin for emergency readiness, patient-specific dosing, and flexibility in reconstitution. Strong adoption is driven by compatibility with standard dosing equipment and ease of handling in intensive care units. Regulatory approvals and quality certifications enhance confidence in the segment. Lyophilized formulations are widely used across cardiovascular, surgical, and critical care applications. Market leaders continue to introduce optimized lyophilized variants for improved solubility and reduced preparation time. Training programs for healthcare staff and awareness initiatives further reinforce usage. Growing demand from developed regions due to high patient volumes sustains revenue dominance. Strategic partnerships between manufacturers and distributors improve accessibility across hospitals and specialty clinics. Clinical studies highlighting efficacy and safety reinforce market preference. Overall, lyophilized antithrombin remains the preferred dosage form globally.

The Liquid dosage form segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, propelled by increasing demand for ready-to-use solutions in hospitals and clinics, reducing preparation time and minimizing dosing errors. Liquid formulations are gaining traction for point-of-care administration, improving workflow efficiency, and supporting rapid patient treatment. Pharmaceutical companies are introducing stable liquid antithrombin products suitable for refrigeration and easy handling. Growth is further accelerated by the adoption in emerging markets and hospital pharmacies that prioritize convenience and operational efficiency. Clinical validation of liquid forms ensures reliability, safety, and ease of use. Adoption is supported by technological advances in formulation, improved storage systems, and cold-chain logistics. Training and awareness initiatives help increase clinician confidence in liquid antithrombin. Overall, liquid dosage forms are anticipated to expand at the highest growth rate through the forecast period.

Antithrombin Market Regional Analysis

- North America dominated the antithrombin market with the largest revenue share of 41.8% in 2025

- Driven by advanced healthcare infrastructure, a strong presence of key pharmaceutical companies, and extensive investment in anticoagulant therapy research

- The market led market expansion due to widespread adoption of innovative antithrombin therapies, particularly in hospitals, specialty clinics, and research institutions. Increased focus on precision medicine, clinical trials, and improved treatment protocols further propelled the market growth in the region

U.S. Antithrombin Market Insight

The U.S. antithrombin market captured the largest revenue share within North America in 2025, fueled by a well-established healthcare and research ecosystem, robust pharmaceutical and biotechnology sectors, and rapid adoption of advanced antithrombin therapies. Strategic collaborations, growing clinical trial activities, and investments in next-generation anticoagulant solutions are driving market expansion. Additionally, government initiatives supporting awareness and treatment of thrombotic disorders are further enhancing adoption rates across hospitals and research centers.

Europe Antithrombin Market Insight

The Europe antithrombin market is projected to grow at a substantial CAGR throughout the forecast period, driven by increasing prevalence of thrombotic disorders, strong healthcare infrastructure, and high R&D investments by leading pharmaceutical players. Countries such as Germany, the U.K., and France are witnessing significant adoption due to well-established clinical research facilities and advanced hospital networks. Expansion of specialty treatment centers and regulatory approvals for novel therapies are also supporting market growth.

U.K. Antithrombin Market Insight

The U.K. antithrombin market is expected to register notable growth during the forecast period, fueled by increasing incidence of coagulation-related disorders and rising awareness among healthcare professionals. The country’s robust healthcare infrastructure, coupled with expanding clinical research and specialized anticoagulant therapy centers, is further enhancing accessibility and adoption of antithrombin therapies.

Germany Antithrombin Market Insight

The Germany antithrombin market is anticipated to expand at a considerable CAGR, driven by technological advancements in biologics manufacturing, strong hospital and research infrastructure, and heightened awareness of thrombotic disorders. The country’s emphasis on innovation and precision medicine promotes the adoption of next-generation antithrombin therapies, particularly in specialized clinics and academic research centers.

Asia-Pacific Antithrombin Market Insight

The Asia-Pacific antithrombin market is expected to grow at the fastest CAGR of 14.1% during the forecast period, driven by rising healthcare spending, increasing urbanization, growing awareness of thrombotic disorders, and expanding access to advanced biologics and therapeutic solutions. Countries such as China, India, and Japan are witnessing rapid adoption due to improving healthcare infrastructure, government initiatives promoting anticoagulant therapy, and the presence of emerging biotech firms introducing innovative antithrombin products.

Japan Antithrombin Market Insight

The Japan antithrombin market is gaining momentum owing to the country’s aging population, high prevalence of thrombotic disorders, and advanced healthcare infrastructure. Increasing adoption of recombinant and plasma-derived antithrombin therapies in hospitals and research institutions, combined with active clinical trial initiatives, is supporting market growth.

China Antithrombin Market Insight

The China antithrombin market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid expansion of healthcare and research infrastructure, increasing investments in anticoagulant therapy, and growing adoption of innovative antithrombin products across hospitals, diagnostic labs, and research facilities. Government initiatives supporting thrombotic disorder management and strong domestic pharmaceutical manufacturing capabilities are further propelling market growth.

Antithrombin Market Share

The Antithrombin industry is primarily led by well-established companies, including:

- CSL Behring (Australia)

- Grifols (Spain)

- Baxter International (U.S.)

- Octapharma (Switzerland)

- Sanquin (Netherlands)

- Kedrion Biopharma (Italy)

- Haematologic Technologies (U.S.)

- Bio Products Laboratory (U.K.)

- Talecris Biotherapeutics (U.S.)

- ADMA Biologics (U.S.)

Latest Developments in Global Antithrombin Market

- In March 2025, the U.S. Food & Drug Administration approved Qfitlia (fitusiran), the first antithrombin‑lowering therapy for routine prophylaxis in adult and pediatric patients (aged 12+) with hemophilia A or B, with or without inhibitors

- In October 2024, a comprehensive pipeline report highlighted that antithrombin III targeted therapeutics (including recombinant and novel formulations) were under active development, with multiple companies advancing Phase II/III studies for treatment of hereditary antithrombin deficiency and related thrombotic conditions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.