Global Aplastic Anemia Market

Market Size in USD Billion

USD

7.12 Billion

USD

10.51 Billion

2025

2033

USD

7.12 Billion

USD

10.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.12 Billion | |

| USD 10.51 Billion | |

| % | |

|

What is the Aplastic Anemia Market Size and Growth Rate?

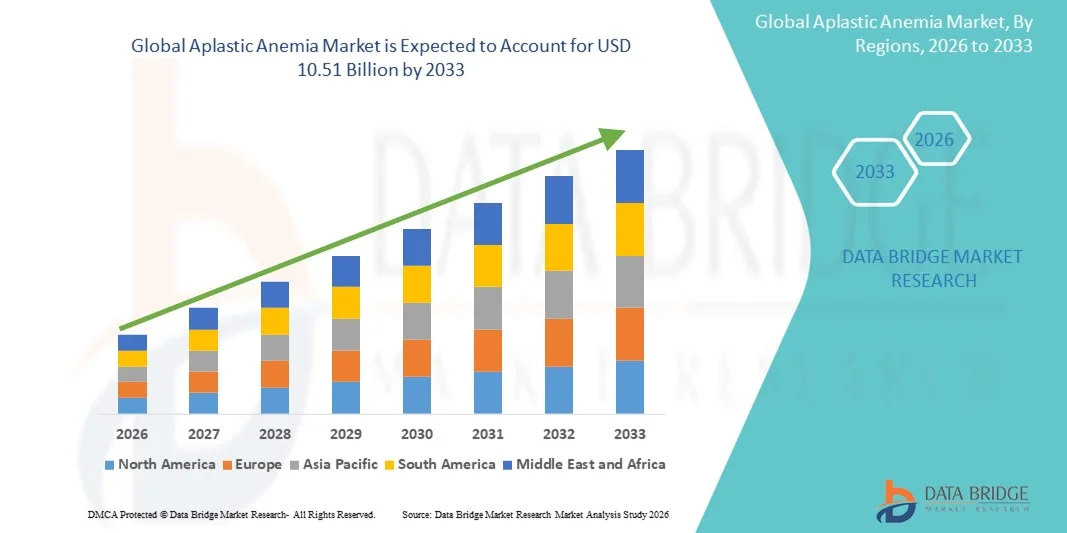

- As per Data Bridge Market Research Analysis the global aplastic anemia market size was valued at USD 7.12 billion in 2025 and is expected to reach USD 10.51 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by increasing awareness of rare blood disorders, advancements in treatment options, and the rising prevalence of aplastic anemia across both pediatric and adult populations

- Furthermore, the growing focus on early diagnosis, expansion of specialized hematology centers, and improved access to advanced therapies, including immunosuppressive treatments, stem cell transplantation, and novel drug candidates, are accelerating the uptake of Aplastic Anemia solutions, thereby significantly boosting the industry's growth

Market Size & Forecast

- Global Market Value (2025): USD 7.12 Billion

- Expected Market Value (2033): USD 10.51 Billion

- Forecast CAGR (2026–2033): 5.00%

Aplastic Anemia Market Analysis

- Aplastic Anemia, a rare but serious blood disorder, is increasingly gaining attention due to rising prevalence, advancements in treatment options, and the establishment of specialized hematology centers in both pediatric and adult populations

- The escalating demand for effective therapies is primarily fueled by growing awareness of the disorder, expansion of stem cell transplantation programs, immunosuppressive therapies, and improved access to advanced diagnostic and treatment facilities

- North America dominated the aplastic anemia market with the largest revenue share of 32.8% in 2025, characterized by well-established healthcare infrastructure, high healthcare spending, and the presence of leading biopharmaceutical companies. The U.S. is witnessing substantial growth in clinical adoption of immunosuppressive therapies, stem cell transplantation programs, and advanced diagnostic initiatives

- Asia-Pacific is expected to be the fastest-growing region in the aplastic anemia market during the forecast period, projected to expand at a CAGR of 15.7% from 2026 to 2033, driven by increasing healthcare modernization, rising awareness of rare blood disorders, expansion of specialized hematology centers, and improving access to advanced treatment options in countries such as Japan, China, and India

- Acquired Aplastic Anemia accounted for the largest market revenue share of 62.4% in 2025, attributed to its higher prevalence globally, enhanced treatment protocols, and increased awareness among healthcare providers

Report Scope and Aplastic Anemia Market Segmentation

|

Attributes |

Aplastic Anemia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Aplastic Anemia Market?

Emerging Treatment Innovations and Personalized Approaches

- A significant and accelerating trend in the global Aplastic Anemia (AA) market is the rising focus on targeted therapies and personalized treatment strategies that are tailored to patient-specific disease severity, age, and comorbidities

- Advances in understanding the molecular and immunological mechanisms underlying AA are enabling clinicians to adopt individualized treatment protocols, optimizing therapeutic outcomes and minimizing adverse effects

- For instance, in June 2024, a study published in Blood Advances highlighted the efficacy of newly optimized immunosuppressive therapy combinations in improving remission rates and reducing relapse, underscoring the potential of precision medicine approaches in AA management

- The development of novel agents, such as thrombopoietin receptor agonists and selective immunomodulators, is enhancing treatment flexibility, allowing clinicians to combine therapies for better response rates

- Biopharmaceutical companies are increasingly investing in research and development to produce therapies with improved safety profiles, convenient dosing schedules, and broader indications, responding to both patient and physician demand for more effective and manageable treatments

- Gene therapy approaches are also gaining momentum as potential curative interventions, particularly in hereditary forms of AA, reflecting a broader shift towards regenerative and targeted treatment modalities

- Personalized treatment strategies are further supported by predictive biomarkers and diagnostic innovations that help stratify patients according to expected therapy response and risk profiles

- Combination regimens that integrate immunotherapy with supportive care measures, including transfusions and growth factors, are demonstrating improved overall survival and quality of life in clinical studies

- Patient-centered care models are increasingly being adopted, focusing on individualized monitoring, outpatient management, and real-time assessment of therapy effectiveness, thereby reducing hospitalizations

- The trend toward precision medicine and targeted interventions is driving collaborations between academic institutions, clinical research networks, and pharmaceutical companies to accelerate therapy development and approval

- Regulatory agencies are also supporting faster clinical trial pathways and conditional approvals for therapies addressing rare and severe cases of AA, further facilitating market expansion

- This ongoing emphasis on innovation, personalization, and therapeutic optimization is shaping the AA market landscape, creating opportunities for new entrants and advanced treatment solutions

Aplastic Anemia Market Dynamics

Driver

Rising Prevalence and Increasing Awareness Among Healthcare Providers

- The growing incidence of aplastic anemia globally, driven by factors such as autoimmune triggers, viral infections, and drug-induced etiologies, is significantly boosting demand for effective treatment options

- Increased awareness among hematologists, immunologists, and general practitioners regarding early diagnosis and intervention is enhancing patient outcomes and driving therapy adoption

- For instance, in March 2023, global health organizations initiated awareness campaigns highlighting early recognition of AA symptoms, leading to timely treatment initiation and better prognoses

- Improvements in diagnostic techniques, including advanced bone marrow analysis and molecular profiling, are enabling faster and more accurate detection of AA cases

- Rising patient advocacy and support networks are also educating patients and caregivers about available treatment modalities, increasing therapy uptake

- The availability of multiple therapeutic options, including immunosuppressive therapy, hematopoietic stem cell transplantation, and emerging drugs, provides clinicians with flexible and tailored treatment approaches

- Investments in healthcare infrastructure and specialized hematology centers in emerging economies are facilitating access to advanced AA care

- Ongoing clinical trials and expanded indications for existing therapies are encouraging healthcare providers to consider more aggressive and personalized treatment regimens

- The increasing focus on improving quality of life for AA patients, along with longer-term survival prospects, is motivating earlier and more proactive intervention strategies

- Healthcare reimbursement policies and insurance coverage expansions in several regions are making advanced therapies more accessible, contributing to market growth

- Educational initiatives targeting both providers and patients are enhancing treatment compliance and adherence to prescribed protocols

- Overall, the combined effect of rising prevalence, clinical awareness, and healthcare infrastructure development is a key driver propelling the growth of the Aplastic Anemia market

Restraint/Challenge

High Treatment Costs and Limited Access to Advanced Therapies

- One of the significant challenges in the AA market is the high cost of advanced therapies, including hematopoietic stem cell transplantation, immunosuppressive agents, and emerging targeted drugs, which can limit patient access, particularly in low- and middle-income countries

- Limited availability of specialized treatment centers capable of delivering complex interventions is another barrier, often requiring patients to travel long distances for care

- For instance, in 2022, reports highlighted that access to stem cell transplantation remained constrained in many regions due to infrastructure, donor availability, and cost considerations

- Adverse effects associated with intensive therapies, including immunosuppressive toxicity and graft-versus-host disease, necessitate careful monitoring and can deter both patients and clinicians from aggressive treatment approaches

- Regulatory delays in certain countries for the approval of novel therapies further restrict patient access to the latest treatment innovations

- Insurance coverage limitations for high-cost therapies can also hinder adoption, particularly for oral immunomodulators and gene therapies, which are not universally reimbursed

- The complexity of long-term follow-up and monitoring for therapy-related complications increases the burden on healthcare systems and patients alike

- Shortages of key therapeutic agents, as observed during supply chain disruptions in 2021–2023, have also impacted treatment continuity for patients requiring long-term therapy

- Addressing these challenges requires collaborative efforts between governments, healthcare providers, and pharmaceutical companies to improve access, affordability, and distribution of AA treatments

- Enhanced patient support programs, expanded insurance coverage, and policy interventions are essential to overcome these barriers and ensure equitable treatment availability

- Inadequate awareness in certain regions about advanced AA therapies further limits uptake, highlighting the need for global educational initiatives

- Without strategic interventions to improve accessibility and affordability, the high cost and complexity of treatment could restrain broader market growth, despite rising clinical demand

Aplastic Anemia Market Scope

The market is segmented on the basis of treatment type, disease type, mode of administration, distribution channel, and end-user.

- By Treatment Type

On the basis of treatment type, the Aplastic Anemia market is segmented into Bone Marrow Transfusion/Stem Cell Therapy, Blood Transfusion, and Drug Therapy. The Bone Marrow Transfusion/Stem Cell Therapy segment dominated the largest market revenue share of 48.6% in 2025, driven by its curative potential in severe cases, advanced donor matching techniques, and improved post-transplant patient care. Hospitals and specialty clinics are the primary settings, given the requirement for intensive monitoring, supportive care, and specialized expertise. Its dominance is reinforced by rising survival rates, reduced complication risks, increasing physician awareness, and growing patient advocacy programs. Adoption is further supported by international guidelines recommending stem cell therapy as first-line treatment for eligible patients, ensuring its leading market position.

The Drug Therapy segment is expected to witness the fastest CAGR of 11.8% from 2026 to 2033, fueled by the development of novel immunosuppressive drugs, thrombopoietin receptor agonists, and targeted therapies. The ability to manage patients in outpatient settings, combined with growing availability of oral formulations, simplified regimens, and improved side-effect profiles, is driving rapid adoption. Increasing R&D investments, expansion of specialty clinics, and rising patient preference for non-invasive treatments are also significant factors contributing to its robust growth trajectory.

- By Disease Type

On the basis of disease type, the market is segmented into Acquired Aplastic Anemia and Inherited Bone Marrow Failure Syndromes (Inherited Aplastic Anemia). Acquired Aplastic Anemia accounted for the largest market revenue share of 62.4% in 2025, attributed to its higher prevalence globally, enhanced treatment protocols, and increased awareness among healthcare providers. Early diagnosis, widespread availability of treatment centers, and government programs supporting rare disease care further reinforce its leading market position. Patient education initiatives and early intervention strategies have improved prognosis and treatment adherence, sustaining market dominance.

Inherited Bone Marrow Failure Syndromes are expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by advancements in genetic testing, early intervention strategies, and specialized therapies targeting congenital forms of the disease. Rising awareness of hereditary conditions, improved access to pediatric and adult treatment centers, and expansion of rare disease networks are contributing to faster adoption. Enhanced diagnostic capabilities, coupled with personalized therapy approaches, are further accelerating market growth in this segment.

- By Mode of Administration

On the basis of mode of administration, the market is segmented into Injectable, Oral, and Others. Injectable administration dominated the largest market revenue share of 70.2% in 2025, due to precise dosing requirements, rapid therapeutic effects, and hospital-based monitoring, especially for biologics, immunosuppressive agents, and advanced cell therapies. Hospitals and specialty clinics remain the main administration points for injectable therapies, as they ensure safety, efficacy, and adherence to clinical protocols. Its dominance is reinforced by patient monitoring programs, post-administration support, and established treatment guidelines that favor parenteral therapy for severe or refractory cases.

Oral administration is expected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by patient preference for home-based therapy, development of oral immunomodulators, simplified dosing schedules, and improved bioavailability. Convenience, reduced hospitalization needs, better adherence, and supportive telemedicine initiatives are key factors boosting the growth of oral formulations. Expansion of outpatient care models and increased availability of oral therapeutics for chronic management also contribute significantly to the rapid adoption of this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. Hospital Pharmacies accounted for the largest market revenue share of 57.3% in 2025, as they provide integrated care, safe administration of complex therapies, and continuous monitoring for patients with severe Aplastic Anemia. Hospitals facilitate specialized interventions such as stem cell transplantation and complex immunosuppressive regimens, ensuring safety and compliance with clinical standards. This segment is further strengthened by established hospital networks, insurance coverage, and collaborative care models that integrate diagnostics, treatment, and follow-up services.

Online Pharmacies are expected to witness the fastest CAGR of 13.2% from 2026 to 2033, driven by increasing adoption of e-commerce platforms, telemedicine-facilitated prescriptions, and patient preference for home delivery of medications. Enhanced convenience, improved access to therapies in remote regions, competitive pricing, and the growing digital healthcare infrastructure are key growth enablers. Expansion of online pharmacy services for chronic disease management and home-based care further accelerates adoption of this distribution channel globally.

- By End User

On the basis of end-user, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. Hospitals dominated the largest market revenue share of 54.6% in 2025, due to their capability to manage complex and severe AA cases, provide multi-disciplinary care, and integrate diagnostic and therapeutic services. Hospitals remain the primary point of care for both acute and chronic patient populations, offering specialized interventions, supportive therapies, and long-term monitoring. Their dominance is reinforced by the availability of hematology experts, access to advanced treatments, and established patient management protocols.

Homecare is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, driven by the availability of oral therapies, simplified parenteral regimens suitable for home administration, and patient preference for outpatient management. This segment benefits from patient-centric care models, telehealth support, reduced hospitalization costs, and improved treatment adherence. Growing awareness of home-based disease management, coupled with advancements in self-administration techniques, supports the rapid growth of the homecare end-user segment globally.

Aplastic Anemia Market Regional Analysis

- North America dominated the aplastic anemia market with the largest revenue share of 32.8% in 2025, characterized by well-established healthcare infrastructure, high healthcare spending, and the presence of leading biopharmaceutical companies

- The region benefits from advanced clinical programs, widespread access to immunosuppressive therapies, stem cell transplantation, and enhanced diagnostic initiatives

- High patient awareness, established treatment protocols, and government support for rare disease management are further contributing to market growth

U.S. Aplastic Anemia Market Insight

The U.S. aplastic anemia market captured the largest revenue share of 78% in 2025 within North America, fueled by the rapid adoption of immunosuppressive therapy regimens, expanded stem cell transplantation programs, and improved diagnostic capabilities. Increasing patient access to specialized hematology centers, combined with ongoing research and clinical trials for novel therapies, is driving market expansion. Additionally, collaborations between hospitals, research institutions, and biopharmaceutical companies are enhancing treatment availability and patient outcomes, significantly contributing to the growth of the U.S. market.

Europe Aplastic Anemia Market Insight

The Europe aplastic anemia market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing awareness of rare blood disorders, well-developed healthcare infrastructure, and government-led initiatives promoting early diagnosis. Rising investments in hematology research, growing patient support programs, and the availability of advanced treatment options such as bone marrow transplantation and immunotherapy are further boosting adoption across residential and hospital settings. Germany, France, and the U.K. are key contributors to regional market growth.

U.K. Aplastic Anemia Market Insight

The U.K. aplastic anemia market is anticipated to grow at a noteworthy CAGR during the forecast period, propelled by rising awareness about rare hematologic disorders and improved access to specialized treatment centers. Enhanced newborn and pediatric screening programs, along with the increasing adoption of immunosuppressive therapies, are supporting market growth. The U.K.’s robust healthcare system, coupled with the availability of advanced diagnostic facilities, is expected to continue stimulating market expansion.

Germany Aplastic Anemia Market Insight

The Germany aplastic anemia market is expected to expand at a considerable CAGR, driven by a strong healthcare infrastructure, high patient awareness, and increasing adoption of targeted therapies and transplantation programs. Government support for rare disease management, coupled with the emphasis on research and innovation in hematology, promotes the accessibility of advanced treatment options. The growing number of specialty clinics and outpatient care centers further contributes to the market's development.

Asia-Pacific Aplastic Anemia Market Insight

The Asia-Pacific aplastic anemia market is poised to grow at the fastest CAGR of 15.7% during the forecast period from 2026 to 2033, driven by increasing healthcare modernization, rising awareness of rare blood disorders, and expansion of specialized hematology and treatment centers. Countries such as Japan, China, and India are witnessing improved access to advanced therapies, enhanced diagnostic capabilities, and growing investments in healthcare infrastructure. Expanding patient awareness programs and government initiatives for rare disease management are further supporting market growth.

Japan Aplastic Anemia Market Insight

The Japan aplastic anemia market is gaining momentum due to a well-established healthcare system, increasing patient awareness, and advancements in stem cell transplantation and immunosuppressive therapies. The growing prevalence of rare blood disorders and the availability of specialized hematology centers enhance patient access to timely treatment. Increasing clinical trials and government support for rare diseases are further contributing to market expansion.

China Aplastic Anemia Market Insight

The China aplastic anemia market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, improved healthcare infrastructure, and increased access to specialized treatment centers. The rising awareness of rare blood disorders, expansion of immunosuppressive therapy programs, and the growing number of clinical trials for advanced therapies are key factors driving market growth. Government initiatives to support rare disease management and the development of hematology centers further strengthen market adoption.

Which are the Top Companies in Aplastic Anemia Market?

The Aplastic Anemia industry is primarily led by well-established companies, including:

• Roche (Switzerland)

• Fresenius Kabi (Germany)

• Novartis (Switzerland)

• Amgen (U.S.)

• Sobi (Sweden)

• BioMarin Pharmaceutical (U.S.)

• Sanofi (France)

• Takeda Pharmaceutical (Japan)

• Shire (Ireland)

• Bayer AG (Germany)

• AbbVie (U.S.)

• Catalent Pharma Solutions (U.S.)

• Sigma-Tau Pharmaceuticals (Italy)

• Viatris (U.S.)

• Lonza Group (Switzerland)

• Apellis Pharmaceuticals (U.S.)

• Grifols (Spain)

• CSL Behring (Australia)

Latest Developments in Global Aplastic Anemia Market

- In April 2025, Cellenkos announced that the FDA granted Orphan Drug Designation to its T‑regulatory cell therapy CK0801 for aplastic anemia. This designation aims to fast-track its development, and early clinical data showed promising safety and efficacy, with some patients achieving long-term transfusion independence

- In August 2025, the FDA accepted Ayrmid Ltd.’s priority review application for omidubicel, an allogeneic hematopoietic progenitor cell therapy derived from umbilical cord blood, for use in severe aplastic anemia. The review had a PDUFA target date of December 10, 2025

- In October 2025, Gamida Cell presented positive interim Phase data on omidubicel in patients with severe aplastic anemia at the AABB Annual Meeting. Results showed that 92.9% of patients achieved rapid neutrophil recovery (median 7 days), highlighting its potential as a powerful cell‑therapy solution

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.