Global Astrocytoma Market

Market Size in USD Billion

USD

1.16 Billion

USD

1.81 Billion

2024

2032

USD

1.16 Billion

USD

1.81 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.16 Billion | |

| USD 1.81 Billion | |

| % | |

|

Astrocytoma Market Size

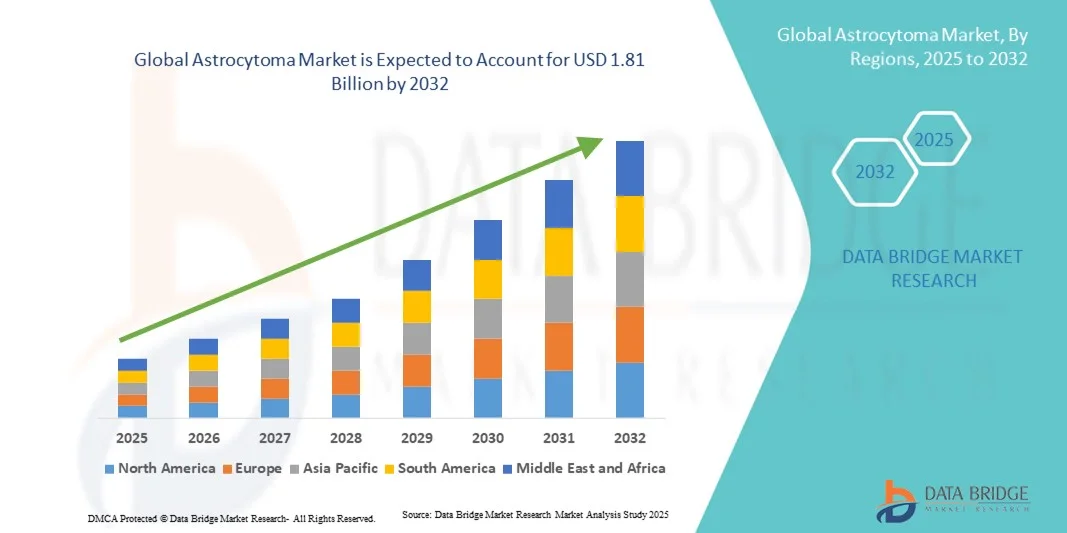

- The global astrocytoma market size was valued at USD 1.16 billion in 2024 and is expected to reach USD 1.81 billion by 2032, at a CAGR of 5.70% during the forecast period

- The market growth is primarily driven by the increasing prevalence of brain tumors, advancements in diagnostic techniques, and the development of novel therapeutic options

- In addition, the rising adoption of precision medicine, targeted therapies, and immunotherapies is contributing to the market's expansion, offering more effective treatment options for patients

Astrocytoma Market Analysis

- Astrocytoma, a type of brain tumor originating from astrocytes, represents a critical segment within neuro-oncology, with treatments including surgery, radiation, and chemotherapy, supported by ongoing research into targeted and precision therapies

- The escalating demand for effective astrocytoma management is primarily driven by the rising incidence of brain tumors, advancements in diagnostic imaging techniques, and growing adoption of innovative therapeutic approaches

- North America dominated the astrocytoma market with the largest revenue share of 39% in 2024, due to advanced healthcare infrastructure, high patient awareness, and a strong presence of key industry players involved in the development of novel therapies, clinical trials, and research initiatives

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, owing to increasing healthcare expenditure, improving access to diagnostic and treatment facilities, and rising awareness about early detection of brain tumors

- Glioblastomas dominated the astrocytoma market with a market share of 41.8% in 2024, driven by their higher prevalence, aggressive nature, and the critical need for multimodal treatment strategies involving surgery, radiation, and chemotherapy

Report Scope and Astrocytoma Market Segmentation

|

Attributes |

Astrocytoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Astrocytoma Market Trends

Advancements in AI-Driven Diagnostics and Treatment

- A significant and accelerating trend in the global astrocytoma market is the integration of artificial intelligence (AI) in diagnostic imaging and treatment planning. This fusion of technologies is significantly enhancing the accuracy and efficiency of clinical decision-making

- For instance, AI-driven tumor segmentation enhances radiotherapy precision by accurately identifying organs at risk, thereby reducing radiation exposure to healthy tissues

- AI integration in astrocytoma care enables features such as automated image analysis and personalized treatment recommendations. For instance, deep learning models have shown promising results in accurately identifying the presence and precise location of brain tumors in MRI images

- The seamless integration of AI tools with existing medical imaging platforms facilitates centralized control over various aspects of the diagnostic and treatment process. For instance, through a single interface, clinicians can access and analyze imaging data, leading to a unified and automated workflow

- This trend towards more intelligent, intuitive, and interconnected diagnostic systems is fundamentally reshaping clinical expectations for brain tumor care. Consequently, companies are developing AI-enabled solutions to enhance diagnostic accuracy and treatment outcomes

- The demand for AI-driven diagnostics and treatment planning is growing rapidly across both academic and clinical settings, as healthcare providers increasingly prioritize precision and efficiency in patient care

Astrocytoma Market Dynamics

Driver

Increasing Incidence and Advancements in Medical Research

- The rising prevalence of high-grade astrocytomas, coupled with advancements in medical research, is a significant driver for the heightened demand for innovative treatment options

- For instance, the increasing incidence rates of anaplastic astrocytoma have spurred considerable investment in oncology research, leading to the development of advanced therapies

- As clinicians and researchers become more aware of potential treatment gaps and seek enhanced therapeutic strategies, novel therapies offer advanced features such as targeted action and improved efficacy, providing a compelling upgrade over traditional treatments

- Furthermore, the growing popularity of personalized medicine and the desire for tailored treatment plans are making innovative therapies an integral component of these systems, offering seamless integration with other medical devices and platforms

- The convenience of targeted therapies, remote monitoring for patients, and the ability to manage treatment plans through digital platforms are key factors propelling the adoption of advanced therapies in both clinical and research settings

- The trend towards personalized medicine and the increasing availability of patient-specific treatment options further contribute to market growth

Restraint/Challenge

High Treatment Costs and Limited Accessibility

- Concerns surrounding the high costs of advanced treatments, including novel therapies, pose a significant challenge to broader market penetration. As these treatments often require specialized administration and monitoring, they are susceptible to affordability issues, raising anxieties among potential patients about the accessibility of care

- For instance, the high cost of drugs, particularly immunotherapies, restricts patient access, especially in developing regions or for budget-conscious patients

- Addressing these affordability concerns through government subsidies, insurance coverage, and cost-effective treatment options is crucial for building patient trust and ensuring equitable access to care

- While prices are gradually decreasing, the perceived premium for advanced treatments can still hinder widespread adoption, especially for those who do not see an immediate need for the advanced features offered

- Overcoming these challenges through enhanced affordability measures, patient education on treatment benefits, and the development of more accessible treatment options will be vital for sustained market growth

Astrocytoma Market Scope

The market is segmented on the basis of type, treatment, application, end user, and distribution channel.

- By Type

On the basis of type, the global astrocytoma market is segmented into anaplastic astrocytomas, glioblastomas, diffuse astrocytomas, pineal astrocytic tumors, brain stem gliomas, pilocytic astrocytomas, and subependymal giant cell astrocytomas. The glioblastomas segment dominated the market with the largest market revenue share of 41.8% in 2024, driven by its high malignancy, aggressive progression, and high recurrence rates. Hospitals and research centers prioritize glioblastoma treatment due to the complexity and critical nature of these tumors. The market also sees strong demand due to extensive clinical research and investment in targeted therapies and immunotherapies. Furthermore, the rising incidence of glioblastomas globally and their challenging prognosis continue to drive market growth in this segment.

The anaplastic astrocytomas segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing R&D activities and advancements in molecular diagnostics. For instance, new classification methods are improving early detection and enabling personalized treatment strategies. Investment in healthcare infrastructure and awareness campaigns is enhancing treatment accessibility and patient outcomes. In addition, the growing prevalence of lifestyle-related health issues and stress is contributing to higher incidence rates. The combination of advanced research, technological developments, and rising patient awareness is driving rapid growth in the anaplastic astrocytoma segment.

- By Treatment

On the basis of treatment, the global astrocytoma market is segmented into surgery, radiation, and chemotherapy. The surgery segment dominated the market in 2024 due to its role as the first-line treatment for most astrocytomas. Complete surgical resection improves survival rates, particularly for lower-grade tumors. Technological advancements in neurosurgical tools and intraoperative imaging enhance precision and safety. Surgery is often complemented with radiation and chemotherapy to address residual tumor cells. The increasing demand for skilled neurosurgeons and advanced surgical infrastructure continues to support growth in this segment.

The chemotherapy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the development of new drugs and combination therapies. For instance, temozolomide-based treatments are increasingly applied in conjunction with surgery and radiation for high-grade tumors. Ongoing clinical trials are testing targeted and immunotherapy approaches alongside chemotherapy. Advances in drug delivery systems improve brain penetration, while personalized medicine is enabling patient-specific treatment regimens. These factors collectively contribute to the rapid expansion of the chemotherapy segment.

- By Application

On the basis of application, the astrocytoma market is segmented into pre-registration phase and clinical trial phase. The clinical trial phase dominated the market, as it is critical for developing new treatment protocols and therapies. For instance, ongoing trials explore innovative drug combinations, surgical techniques, and radiation methods. Clinical trials provide patients with access to cutting-edge therapies and contribute to scientific progress. Regulatory oversight ensures patient safety and therapy efficacy. Positive trial outcomes lead to approvals of novel treatments, reinforcing the segment’s dominance.

The pre-registration phase is anticipated to witness the fastest growth from 2025 to 2032, driven by accelerated development of new therapies and molecular diagnostic tools. For instance, collaborations between pharmaceutical companies, research institutions, and healthcare providers are expediting regulatory submissions. Increased investment in early-stage research is expanding the treatment pipeline. Streamlined regulatory pathways facilitate faster approvals for promising therapies. These factors collectively boost the growth of the pre-registration phase segment in the astrocytoma market.

- By End User

On the basis of end user, the astrocytoma market is segmented into hospitals, specialty clinics, and research centers. The hospitals segment dominated the market due to the comprehensive care they provide, including surgery, radiation, and chemotherapy. Hospitals have advanced medical technologies and multidisciplinary teams specializing in neuro-oncology. They play a crucial role in clinical trials and patient support, including rehabilitation and psychological care. The growing incidence of astrocytomas further reinforces hospitals’ central role in patient management and treatment.

The research centers segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing focus on innovative therapies and clinical trials. For instance, research centers are expanding personalized medicine initiatives and molecular profiling studies. Collaboration with hospitals, academic institutions, and pharmaceutical companies drives translational research. Research centers also contribute to professional training, biomarker discovery, and early detection strategies. Growing investment in cancer research accelerates the segment’s expansion in the global market.

- By Distribution Channel

On the basis of distribution channel, the astrocytoma market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market due to its role in dispensing specialized medications and managing chemotherapy and supportive drugs. Hospital pharmacies ensure patient safety, manage logistics, and collaborate with oncologists to optimize pharmacotherapy. Integration with electronic health records further enhances efficiency and accuracy, reinforcing their market dominance.

The online pharmacy segment is anticipated to witness the fastest growth from 2025 to 2032, driven by increasing demand for convenient access to medications. For instance, home delivery services and telemedicine support make it easier for patients to receive prescribed therapies. Online platforms offer broad access to specialized treatments, improving treatment adherence. Regulatory oversight ensures safety and compliance. The convenience and accessibility provided by online pharmacies are driving rapid adoption globally.

Astrocytoma Market Regional Analysis

- North America dominated the astrocytoma market with the largest revenue share of 39% in 2024, due to advanced healthcare infrastructure, high patient awareness, and a strong presence of key industry players involved in the development of novel therapies, clinical trials, and research initiatives

- Patients and healthcare providers in the region highly value access to advanced treatment options, clinical trials, and multidisciplinary care teams for managing complex astrocytomas such as glioblastomas and anaplastic astrocytomas

- This widespread adoption is further supported by significant government and private investment in cancer research, cutting-edge medical technologies, and the availability of specialized hospitals and research centers, establishing North America as a leading market for astrocytoma treatment

U.S. Astrocytoma Market Insight

The U.S. astrocytoma market captured the largest revenue share of 82% in North America in 2024, fueled by advanced healthcare infrastructure and a high concentration of research institutions focused on neuro-oncology. Patients increasingly prioritize access to innovative treatments such as targeted therapy, immunotherapy, and personalized chemotherapy regimens. The growing prevalence of glioblastomas and anaplastic astrocytomas, combined with robust clinical trial activities, further propels market growth. Moreover, the integration of molecular diagnostics and advanced imaging techniques in treatment protocols is significantly contributing to the market's expansion.

Europe Astrocytoma Market Insight

The Europe astrocytoma market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations, rising awareness of early diagnosis, and increasing access to advanced therapies. The region’s focus on multidisciplinary treatment approaches, including surgery, radiation, and chemotherapy, supports adoption. European countries are witnessing growth across both hospitals and specialty clinics, with astrocytoma treatments being incorporated into national cancer care programs. Improved patient education and government support for neuro-oncology research are further accelerating market growth.

U.K. Astrocytoma Market Insight

The U.K. astrocytoma market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing patient awareness of brain tumors and the adoption of personalized treatment strategies. Rising concerns about high-grade astrocytomas, such as glioblastomas, are encouraging healthcare providers to implement advanced treatment protocols. The U.K.’s strong healthcare infrastructure, coupled with a robust clinical trial ecosystem and supportive e-health platforms, is expected to continue stimulating market growth.

Germany Astrocytoma Market Insight

The Germany astrocytoma market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of early detection, technological advancements in neuro-oncology, and access to state-of-the-art healthcare facilities. Germany’s emphasis on research, innovation, and patient-centric care promotes the adoption of advanced treatment options, including minimally invasive surgery, radiotherapy, and combination therapies. Integration of precision medicine approaches and multidisciplinary care teams is becoming increasingly prevalent, aligning with local healthcare standards and patient expectations.

Asia-Pacific Astrocytoma Market Insight

The Asia-Pacific astrocytoma market is poised to grow at the fastest CAGR of 23% during the forecast period of 2025 to 2032, driven by rising prevalence of brain tumors, increasing healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region’s growing inclination towards specialized cancer care, supported by government initiatives and healthcare modernization programs, is driving the adoption of astrocytoma treatments. Furthermore, expanding hospital infrastructure, the availability of advanced therapies, and rising patient awareness are enabling broader market penetration.

Japan Astrocytoma Market Insight

The Japan astrocytoma market is gaining momentum due to the country’s advanced medical infrastructure, high healthcare spending, and focus on innovative treatment solutions. Japanese healthcare providers emphasize precision medicine, early diagnosis, and integrated care for brain tumors. The increasing number of clinical trials, adoption of targeted therapies, and government support for cancer research are fueling growth. Moreover, Japan’s aging population is expected to increase demand for accessible, effective, and patient-friendly astrocytoma treatments in both hospital and specialty clinic settings.

India Astrocytoma Market Insight

The India astrocytoma market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, growing healthcare infrastructure, and increasing patient awareness. India is witnessing a rise in the prevalence of high-grade astrocytomas, leading to higher demand for advanced treatments such as surgery, chemotherapy, and radiation therapy. The push towards specialized cancer centers, government initiatives promoting affordable healthcare, and the availability of advanced diagnostic and treatment technologies are key factors propelling the market in India.

Astrocytoma Market Share

The Astrocytoma industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Genentech (U.S.)

- Novartis AG (Switzerland)

- Amgen Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- AstraZeneca (U.K.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Optune Gio® (U.S.)

- Novocure (U.S.)

- Cothera Bioscience (U.S.)

- Orbus Therapeutics (U.S.)

- Chimerix (U.S.)

- Candel Therapeutics (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

What are the Recent Developments in Global Astrocytoma Market?

- In August 2025, the U.S. Food and Drug Administration (FDA) approved Modeyso (dordaviprone), an oral medication developed by Jazz Pharmaceuticals, for the treatment of diffuse midline glioma (DMG), a rare and aggressive brain tumor primarily affecting children and young adults. This approval marks the first FDA-approved systemic therapy for DMG with a specific mutation, particularly for cases that have advanced despite prior treatments

- In July 2025, the FDA granted orphan drug designation to MB-101, an IL13Rα2-targeted CAR T-cell therapy, for the treatment of recurrent diffuse and anaplastic astrocytoma and glioblastoma. This designation facilitates the development and commercialization of MB-101, aiming to provide a novel therapeutic approach for these aggressive brain tumors

- In April 2025, researchers at Oregon State University achieved a significant breakthrough in nanoparticle-based drug delivery aimed at treating brain-related conditions. They developed dual peptide-functionalized polymeric nanocarriers to specifically deliver anti-inflammatory IRAK4 inhibitors to the hypothalamus in mice, significantly improving treatment outcomes for cancer cachexia

- In March 2025, Jazz Pharmaceuticals announced its acquisition of Chimerix for approximately USD 935 million. This acquisition provides Jazz with access to Chimerix’s lead drug candidate, dordaviprone, which is under FDA review for the treatment of H3 K27M-mutant diffuse glioma, a rare and aggressive brain tumor. The acquisition aims to expand Jazz's oncology portfolio and address high unmet needs in brain cancer treatment

- In August 2024, the U.S. Food and Drug Administration (FDA) approved vorasidenib (Voranigo) for the treatment of grade 2 astrocytomas and oligodendrogliomas harboring IDH1 or IDH2 mutations. This oral medication offers a new treatment option for patients who have undergone surgery and are not in need of immediate chemotherapy or radiotherapy. The approval marks a significant advancement in the management of low-grade gliomas

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.