Global Audiology Devices Market

Market Size in USD Billion

USD

15.67 Billion

USD

25.73 Billion

2025

2033

USD

15.67 Billion

USD

25.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 15.67 Billion | |

| USD 25.73 Billion | |

| % | |

|

Audiology Devices Market Overview

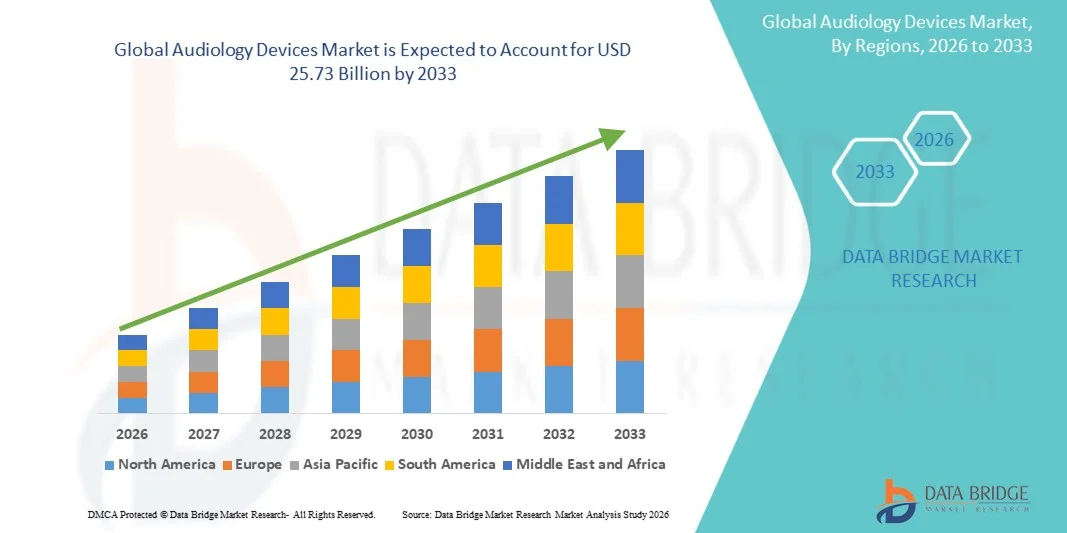

The Audiology Devices Market was valued at USD 15.67 billion in 2025 and is projected to reach USD 25.73 billion by 2033, growing at a CAGR of 6.40% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of hearing disorders, increasing geriatric population, and growing awareness regarding early diagnosis and treatment of hearing loss. Technological advancements in hearing aids, cochlear implants, and diagnostic audiology equipment are further accelerating market expansion across both developed and emerging economies.

The increasing incidence of age-related hearing impairment, noise-induced hearing loss, and congenital hearing disorders, combined with improving access to audiology care services, is encouraging hospitals, audiology clinics, and hearing care centers to adopt advanced audiology devices. Digital hearing aids, wireless connectivity features, AI-enabled sound processing, and minimally invasive cochlear implant technologies are replacing conventional hearing solutions in many markets, offering enhanced sound quality, personalized hearing experiences, and improved patient outcomes.

Key Market Trends & Insights

- North America dominated the Audiology Devices Market with the largest revenue share of 36.42% in 2025, supported by advanced healthcare infrastructure, high adoption of digital hearing technologies, and increasing government support for hearing care services.

- The Hearing Aids segment led the market with a 43.76% share in 2025, driven by the rising prevalence of age-related hearing loss and growing demand for technologically advanced hearing assistance devices.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.5% from 2026 to 2033, fueled by increasing awareness regarding hearing disorders, expanding healthcare access, and rising adoption of hearing care solutions across China, India, and Japan.

- The Digital technology segment is the fastest-growing technology category, projected to register a CAGR of 7.3%, reflecting growing preference for AI-enabled sound processing, wireless connectivity, and personalized hearing enhancement solutions.

- The BTE (Behind-the-Ear) Aids segment dominates the type category with a 39.84% revenue share in 2025, led by superior amplification capabilities, ease of handling, and suitability for a wide range of hearing impairments.

- Retail Sales account for 52.11% of the market, preferred due to strong presence of audiology clinics, hearing aid centers, and expanding consumer access to personalized hearing care products.

- The Hospitals segment is the fastest-growing end-user category, with a CAGR of 6.9%, driven by increasing patient volume for hearing diagnostics, cochlear implant procedures, and integrated audiology treatment services.

- The Digital segment dominated the market with a share of 81.23% in 2025 due to widespread adoption of advanced sound processing technologies, AI-enabled hearing enhancement systems, and wireless connectivity features

Market Size & Forecast

- Global Market Value (2025): USD 15.67 Billion

- Expected Market Value (2033): USD 25.73 Billion

- Forecast CAGR (2026–2033): 6.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Audiology Devices Market Segmentation

|

Attributes |

Audiology Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Sonova Holding AG (Switzerland) |

|

Market Opportunities |

· Increasing adoption of AI-enabled and wireless hearing aids presents significant growth opportunities · Expanding healthcare infrastructure and rising awareness regarding early hearing loss diagnosis · The growing geriatric population worldwide and increasing prevalence of noise-induced hearing disorders |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Audiology Devices Market Trends

Trend: Rising Adoption of AI-Enabled and Smart Hearing Technologies

Hearing care providers and audiology device manufacturers are increasingly adopting AI-powered and digitally connected audiology devices to improve patient outcomes and personalize hearing experiences. Modern hearing aids now integrate Bluetooth connectivity, machine learning algorithms, tinnitus masking, and real-time environmental sound optimization to enhance speech clarity in noisy environments. The growing popularity of rechargeable hearing aids and smartphone-controlled devices is further transforming patient convenience and long-term usability.

For instance, in January 2025, Sonova Holding AG expanded its AI-enabled hearing aid portfolio featuring adaptive sound processing and remote audiology support capabilities. Similarly, hearing care centers are increasingly utilizing cloud-connected audiology platforms for remote fitting and tele-audiology consultations, particularly across North America and Europe where digital healthcare adoption continues to rise.

Audiology Devices Market Dynamics

Key Market Driver: Increasing Prevalence of Hearing Loss and Aging Population

The growing global burden of hearing impairment is a major factor driving demand for audiology devices. Rising exposure to occupational noise, increasing use of personal audio devices, and age-related hearing deterioration are significantly expanding the patient population requiring hearing assistance and diagnostic services. According to the World Health Organization (WHO), over 1.5 billion people globally live with some degree of hearing loss, while nearly 430 million people require rehabilitation services for disabling hearing impairment.

Healthcare providers, hospitals, and hearing clinics are increasingly investing in advanced audiometers, cochlear implants, and digital hearing aids to support early diagnosis and long-term hearing rehabilitation. In addition, government-led hearing screening initiatives and reimbursement support in countries such as the United States, Germany, and Japan are accelerating adoption of advanced audiology technologies.

Key Restraint/Challenge: High Cost of Advanced Hearing Devices and Limited Accessibility

A significant challenge in the Audiology Devices Market is the high cost associated with technologically advanced hearing aids and cochlear implant procedures. Premium digital hearing aids integrated with AI-based sound optimization, wireless streaming, and rechargeable batteries often remain unaffordable for patients in low- and middle-income regions. In addition to device costs, expenses related to fitting, calibration, maintenance, and follow-up audiology services increase the overall treatment burden.

For example, cochlear implantation procedures can cost tens of thousands of dollars in developed markets, limiting accessibility for uninsured populations. Furthermore, inadequate availability of trained audiologists and hearing care infrastructure in rural regions across Asia-Pacific, Africa, and Latin America continues to restrict early diagnosis and treatment adoption.

Key Market Opportunity: Expansion of Tele-Audiology and Remote Hearing Care Services

The rapid expansion of telehealth infrastructure is creating strong growth opportunities for tele-audiology and remotely programmable hearing devices. Cloud-based hearing assessment platforms and smartphone-enabled hearing aids are enabling audiologists to provide remote consultations, device tuning, and hearing rehabilitation services without requiring frequent in-person visits.

The increasing penetration of internet-connected healthcare solutions across emerging economies is further supporting adoption of remote hearing care models. In 2024, GN Store Nord A/S and WS Audiology expanded digital hearing ecosystems integrating app-based hearing assessments and remote fine-tuning features to improve patient accessibility and long-term engagement. The growing demand for home-based healthcare solutions among elderly populations is expected to further accelerate the adoption of tele-audiology platforms globally.

Audiology Devices Market Scope

The Audiology Devices market is segmented on the basis of product, type, technology, sales channel, disease type, and end-user.

- By Product

On the basis of product, the Audiology Devices Market is segmented into bone anchored aids for hearing, cochlear implants, hearing aids, diagnostic devices, tympanometers, audiometers, and otoscopes. The Hearing Aids segment dominated the market with a share of 43.76% in 2025 due to the rising prevalence of age-related and noise-induced hearing loss, increasing awareness regarding hearing rehabilitation, and growing adoption of technologically advanced digital hearing solutions. High demand for wireless, rechargeable, and AI-enabled hearing aids with Bluetooth connectivity and personalized sound optimization is accelerating adoption among elderly and adult populations globally. In addition, increasing reimbursement support, expansion of audiology clinics, and strong product availability through retail hearing care networks are reinforcing segment growth. Continuous innovation by leading manufacturers in miniaturized and discreet hearing aid designs is further improving patient comfort and acceptance, strengthening the dominance of this segment across developed and emerging healthcare markets.

The Cochlear Implants segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing incidence of severe to profound hearing loss, rising pediatric cochlear implantation procedures, and growing technological advancements in implantable hearing devices. Expanding government funding programs, improving surgical success rates, and growing awareness regarding early intervention for congenital hearing disorders are supporting rapid segment expansion. In addition, advancements in sound processing technology, wireless connectivity, and minimally invasive implant procedures are improving patient outcomes and encouraging wider adoption globally.

- By Type

On the basis of type, the Audiology Devices Market is segmented into RITE (Receiver-in-the-Ear) aids, ITE (In-the-Ear) aids, BTE (Behind-the-Ear) aids, and canal hearing aids. The BTE (Behind-the-Ear) Aids segment dominated the market with a share of 39.84% in 2025 due to its superior amplification capabilities, durability, and suitability for mild to profound hearing loss conditions. These devices are widely adopted among geriatric populations because of ease of handling, long battery life, and compatibility with advanced digital sound processing technologies. Increasing integration of wireless streaming, noise reduction systems, rechargeable batteries, and smartphone connectivity is further supporting segment growth. In addition, strong recommendations by audiologists and hospitals for BTE devices in severe hearing impairment cases continue to reinforce the leading position of this segment in the global market.

The RITE (Receiver-in-the-Ear) Aids segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by growing consumer preference for lightweight, cosmetically appealing, and high-performance hearing devices. These aids offer improved sound clarity, enhanced speech recognition, and better comfort compared to traditional hearing aid models. Increasing adoption among younger adults and technologically aware users, combined with rising availability of rechargeable and AI-enabled RITE devices, is accelerating market expansion globally.

- By Technology

On the basis of technology, the Audiology Devices Market is segmented into digital and analogue. The Digital segment dominated the market with a share of 81.23% in 2025 due to widespread adoption of advanced sound processing technologies, AI-enabled hearing enhancement systems, and wireless connectivity features. Digital audiology devices offer superior sound quality, adaptive noise cancellation, feedback suppression, and personalized hearing experiences compared to analogue devices, making them highly preferred among patients and hearing care professionals. In addition, rising integration with smartphone applications, cloud-based remote fitting platforms, and tele-audiology services is further accelerating adoption of digital hearing technologies globally.

The Digital segment is also expected to witness the fastest CAGR of 7.3% from 2026 to 2033, driven by continuous technological innovation in hearing healthcare devices and growing demand for smart, connected hearing solutions. Increasing investment in AI-based sound optimization, rechargeable battery technologies, and remote audiology platforms is supporting long-term market expansion. Furthermore, rising awareness regarding early hearing diagnosis and increasing consumer willingness to adopt premium hearing devices are contributing significantly to segment growth.

- By Sales Channel

On the basis of sales channel, the Audiology Devices Market is segmented into retail sales, government purchases, and e-commerce. The Retail Sales segment dominated the market with a share of 52.11% in 2025 due to the strong presence of audiology clinics, hearing aid dispensing centers, and specialty hearing care retailers worldwide. Patients prefer retail-based purchasing channels because they provide personalized hearing assessments, device fitting services, and post-purchase audiology support. In addition, partnerships between hearing aid manufacturers and retail audiology chains are improving accessibility to technologically advanced hearing devices. Increasing consumer awareness regarding hearing healthcare and expanding private hearing care infrastructure are further reinforcing the leading position of this segment globally.

The E-Commerce segment is expected to witness the fastest CAGR of 7.5% from 2026 to 2033, driven by increasing digitalization of healthcare purchasing channels and rising consumer preference for convenient online product access. Online platforms are enabling direct-to-consumer sales of hearing aids and audiology accessories with competitive pricing, virtual consultations, and home delivery services. Growing penetration of tele-audiology services and smartphone-enabled hearing assessment tools is further accelerating adoption of e-commerce channels in developed and emerging markets.

- By Disease Type

On the basis of disease type, the Audiology Devices Market is segmented into otosclerosis, Meniere’s disease, acoustic tumors, otitis media, and others. The Otitis Media segment dominated the market with a share of 34.42% in 2025 due to the high global prevalence of middle ear infections among pediatric and adult populations. Rising incidence of chronic ear infections, increasing ENT consultations, and growing adoption of diagnostic audiology equipment such as otoscopes and tympanometers are supporting strong segment growth. In addition, increasing awareness regarding early diagnosis and treatment of hearing-related complications caused by recurrent ear infections is reinforcing demand for advanced audiology devices globally.

The Meniere’s Disease segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by rising prevalence of vestibular and balance disorders combined with growing diagnosis rates of inner ear diseases. Increasing use of audiometers and advanced hearing assessment technologies for evaluating hearing fluctuations and tinnitus symptoms is accelerating segment growth. Furthermore, growing investments in specialized ENT and audiology care services are supporting adoption of advanced diagnostic and rehabilitation solutions for Meniere’s disease management.

- By End-User

On the basis of end-user, the Audiology Devices Market is segmented into hospitals, ambulatory surgical centers (ASCs), and research institutes. The Hospitals segment dominated the market with a share of 48.37% in 2025 due to high patient inflow for hearing diagnostics, cochlear implant surgeries, and comprehensive audiology rehabilitation services. Hospitals are increasingly investing in advanced audiometers, cochlear implant systems, and digital hearing assessment platforms to improve diagnostic accuracy and treatment outcomes. In addition, availability of skilled ENT specialists, audiologists, and integrated hearing care infrastructure is supporting strong adoption of audiology devices across hospital settings globally. Increasing reimbursement support and growing government healthcare investments are further reinforcing the leadership of this segment in the market.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing preference for minimally invasive outpatient hearing procedures and cost-effective surgical care settings. ASCs provide shorter hospital stays, lower procedural costs, and faster recovery timelines for cochlear implantation and ENT-related procedures, making them increasingly attractive among patients and healthcare providers. In addition, expanding private healthcare infrastructure and rising demand for specialized outpatient hearing care services are accelerating segment growth globally.

Audiology Devices Market Regional Analysis

North America dominated the Audiology Devices market and accounted for the largest revenue share of 36.42% in 2025, supported by advanced healthcare infrastructure, strong adoption of digital hearing technologies, and increasing government support for hearing care services. The region also benefits from high awareness regarding early diagnosis of hearing disorders, favorable reimbursement policies, and the strong presence of leading hearing aid and cochlear implant manufacturers. Increasing prevalence of age-related hearing loss, growing demand for AI-enabled hearing aids, and rising adoption of tele-audiology platforms continue to strengthen North America’s leadership position in the global market.

U.S. Audiology Devices Market Insight

The U.S. Audiology Devices market is witnessing strong growth due to increasing prevalence of hearing impairment, rising geriatric population, and growing demand for technologically advanced hearing care solutions. The country’s advanced healthcare ecosystem, combined with strong adoption of digital hearing aids, cochlear implants, and wireless audiology devices, is driving market expansion across hospitals, audiology clinics, and ambulatory care settings. In addition, increasing availability of over-the-counter hearing aids, expanding tele-audiology services, and growing investments in AI-enabled hearing technologies are accelerating adoption across the country.

Europe Audiology Devices Market Insight

The Europe Audiology Devices market remains a major contributor to global revenue, driven by strong healthcare infrastructure, increasing awareness regarding hearing rehabilitation, and high adoption of advanced hearing technologies. The widespread use of digital hearing aids, cochlear implants, and diagnostic audiology equipment across hospitals and hearing care centers is supporting market growth throughout the region. In addition, favorable reimbursement frameworks, rising elderly population, and continuous technological innovation in hearing healthcare solutions are further strengthening the adoption of audiology devices across Europe.

U.K. Audiology Devices Market Insight

The U.K. Audiology Devices market is experiencing steady growth, supported by increasing prevalence of hearing disorders and rising investments in public hearing healthcare programs. Growing adoption of rechargeable hearing aids, wireless hearing devices, and remote hearing assessment technologies is contributing significantly to market expansion. Furthermore, rising awareness regarding early hearing loss detection and expanding access to ENT and audiology services are supporting increased demand for advanced audiology devices across the country.

Germany Audiology Devices Market Insight

The Germany Audiology Devices market is expanding steadily due to the country’s advanced medical technology sector, strong healthcare spending, and increasing adoption of next-generation hearing care solutions. Hospitals, ENT clinics, and audiology centers are increasingly utilizing AI-enabled hearing aids, cochlear implants, and digital diagnostic devices to improve patient outcomes and treatment efficiency. Continuous advancements in hearing technology, combined with strong government focus on preventive healthcare and hearing rehabilitation, are further driving market growth in Germany.

Asia-Pacific Audiology Devices Market Insight

The Asia-Pacific Audiology Devices market is expected to witness rapid growth at a CAGR of 7.5% from 2026 to 2033, driven by increasing awareness regarding hearing disorders, expanding healthcare access, and rising adoption of hearing care solutions across countries such as China, India, and Japan. Growing geriatric population, increasing prevalence of noise-induced hearing loss, and rising healthcare investments are supporting strong regional market expansion. In addition, improving availability of affordable hearing aids, increasing government-led hearing screening initiatives, and expanding audiology care infrastructure are accelerating adoption of audiology devices across emerging economies in the region.

Japan Audiology Devices Market Insight

The Japan Audiology Devices market is witnessing consistent growth due to rising demand for advanced hearing care technologies and increasing prevalence of age-related hearing impairment. Hospitals and hearing care providers are increasingly adopting digital hearing aids, cochlear implants, and AI-enabled diagnostic solutions to improve hearing rehabilitation outcomes. Moreover, growing healthcare digitization, rising adoption of tele-audiology services, and increasing focus on elderly healthcare management are further contributing to market growth in Japan.

China Audiology Devices Market Insight

The China Audiology Devices market is growing rapidly, driven by expanding healthcare infrastructure, increasing awareness regarding hearing healthcare, and rising adoption of technologically advanced hearing devices. Growing demand for affordable hearing aids, increasing government initiatives for hearing screening programs, and rising investments in ENT and audiology care services are significantly boosting market demand. In addition, rapid urbanization, increasing elderly population, and continuous advancements in wireless and AI-powered hearing technologies are positioning China as one of the fastest-growing markets for audiology devices globally.

Audiology Devices Market Share

The Audiology Devices industry is primarily led by well-established companies, including:

- Sonova Holding AG (Switzerland)

- Demant A/S (Denmark)

- WS Audiology (Singapore)

- GN Store Nord A/S (Denmark)

- Cochlear Limited (Australia)

- Starkey Laboratories, Inc. (U.S.)

- MED-EL Medical Electronics (Austria)

- Amplifon S.p.A. (Italy)

- Sivantos Pte. Ltd. (Singapore)

- Widex A/S (Denmark)

- RION Co., Ltd. (Japan)

- Natus Medical Incorporated (U.S.)

- William Demant Holding A/S (Denmark)

- Interacoustics A/S (Denmark)

- Oticon Medical (Sweden)

- Eargo, Inc. (U.S.)

- Benson Medical Instruments (U.S.)

- Maico Diagnostics GmbH (Germany)

- Auditdata A/S (Denmark)

- Inventis Srl (Italy)

- Microson S.A.U. (Spain)

- Horentek (Italy)

- Path Medical GmbH (Germany)

- Frye Electronics, Inc. (U.S.)

- Audina Hearing Instruments, Inc. (U.S.)

- Arphi Electronics Private Limited (India)

- Puretone Ltd. (United Kingdom)

- Auditech Hearing Services Pvt. Ltd. (India)

- Shenzhen Jinghao Medical Technology Co., Ltd. (China)

- Hearing Plus Pvt. Ltd. (India)

Latest Developments in Audiology Devices Market

- In August 2024, Sonova Holding AG announced the launch of the Phonak Audéo Sphere Infinio platform, recognized as the first hearing aid featuring real-time AI-powered sound processing technology. The device integrates DEEPSONIC AI chips to separate speech from background noise in real time, significantly improving speech clarity for users in noisy environments. This development highlights the growing integration of artificial intelligence into advanced hearing care solutions and strengthens Sonova’s competitive position in the Audiology Devices Market

- In March 2024, WS Audiology introduced the Rexton ReCharge hearing aid portfolio, offering affordable rechargeable hearing solutions designed to improve accessibility and convenience for hearing-impaired patients globally. The launch reflects the increasing industry focus on rechargeable and user-friendly hearing technologies aimed at expanding hearing aid adoption in both developed and emerging markets

- In February 2023, Cochlear Limited announced a strategic partnership with Amazon.com, Inc. to enable direct audio streaming support for cochlear implant users through compatible hearing devices. The collaboration was designed to improve entertainment accessibility and enhance wireless connectivity capabilities for individuals with hearing impairment, supporting the growing trend toward smart and connected audiology devices

- In October 2022, the U.S. FDA’s implementation of regulations permitting over-the-counter (OTC) hearing aid sales significantly transformed the global audiology devices landscape by expanding consumer access to hearing solutions without prescription requirements. The regulatory shift accelerated innovation in self-fitting, app-connected, and affordable hearing aid technologies, encouraging major manufacturers to strengthen their OTC hearing device portfolios

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.