Global Automotive Gears Market

Market Size in USD Billion

USD

45.67 Billion

USD

75.24 Billion

2024

2032

USD

45.67 Billion

USD

75.24 Billion

2024

2032

| 2025 - 2032 | |

| USD 45.67 Billion | |

| USD 75.24 Billion | |

| % | |

|

Automotive Gears Market Size

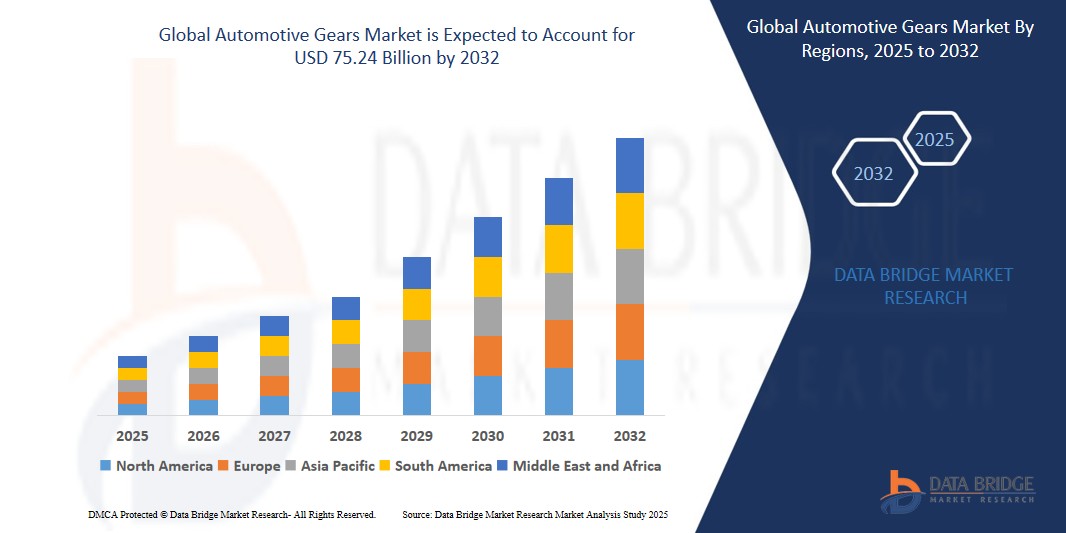

- The Global Automotive Gears Market size was valued at USD 45.67 billion in 2024 and is expected to reach USD 75.24 billion by 2032, at a CAGR of 6.44% during the forecast period

- The market growth is significantly influenced by the shift toward electric and hybrid vehicles (EVs/HEVs). As global regulatory bodies enforce stricter emission norms and consumers seek eco-friendly alternatives, automakers are increasingly adopting electric drivetrains. This transition necessitates the use of specialized gear configurations such as planetary and helical gears, which are tailored to meet the unique torque and speed requirements of EVs. Consequently, the growing penetration of EVs is opening new avenues for innovation and growth in the automotive gears market.

- Additionally, rising consumer expectations for smooth driving experiences and advanced transmission systems is propelling demand. Modern consumers increasingly value enhanced vehicle performance, quieter operation, and reduced mechanical losses. This trend has led to the rising adoption of automatic and dual-clutch transmissions (DCTs), which rely heavily on precise and high-quality gear systems. These evolving preferences are shaping the future of gear design and production, encouraging manufacturers to invest in advanced materials, manufacturing techniques, and precision engineering.

Automotive Gears Market Analysis

- Automotive gears are essential mechanical components used in vehicle transmissions and drivetrains, enabling efficient power transfer and improved vehicle performance. Their demand is rising due to increased vehicle production and advancements in transmission technologies.

- The market growth is driven by the shift towards electric and hybrid vehicles, which require specialized lightweight and high-strength gears for enhanced efficiency and durability.

- Growing adoption of automatic and dual-clutch transmissions, coupled with stricter fuel efficiency and emission standards, further boosts the need for advanced automotive gears.

- Manufacturers are focusing on innovative materials and design improvements to meet performance, noise reduction, and sustainability goals in modern vehicles.

- North America dominates the Automotive Gears Market with the largest revenue share of 32.51% in 2024, driven by a growing demand for home automation and security, as well as increased awareness of smart home technology.

- Asia-Pacific Automotive Gears Market is poised to grow at the fastest CAGR of 24% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India.

- The metallic segment dominated the largest market revenue share in 2024, driven by its high strength, durability, and wide usage in critical vehicle functions. Within this, steel gears are widely preferred due to their superior load-bearing capacity and cost-efficiency in mass production.

Report Scope and Automotive Gears Market Segmentation

|

Attributes |

Automotive Gears Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Gears Market Trends

“Rising Demand for Automotive Gears Due to Increasing Global Vehicle Production and Electrification”

- The sustained growth in global automobile production, especially in emerging economies like India, China, and Mexico, is significantly driving the demand for automotive gears. These components are essential for power transmission and performance optimization across both conventional and electric drivetrains.

- For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), global car production increased by 5% in 2023, with Asia-Pacific contributing the highest volume. This rise in vehicle output has a direct correlation with the demand for high-performance gear systems in the industry.

- The surge in electric vehicle (EV) adoption further amplifies this trend. EVs require precision-engineered gears for smooth power delivery, reduced noise, and increased torque handling. Manufacturers are therefore investing in custom gear solutions designed for electric drivetrains.

- A notable example includes ZF Friedrichshafen AG’s introduction of new e-drive gearboxes in 2024, specifically engineered for battery electric vehicles, supporting the industry's transition toward sustainable mobility.

Automotive Gears Market Dynamics

Driver

“Growing Emphasis on Lightweight Materials and Advanced Gear Design”

- With tightening fuel efficiency regulations and emission norms, automakers are prioritizing lightweight design strategies. This has created a strong push toward the use of lightweight materials such as aluminum alloys, composites, and high-strength plastics in gear production.

- Advanced gear design, including helical and herringbone configurations, is gaining popularity for their ability to reduce noise, improve durability, and handle higher loads efficiently.

- For instance, DuPont has collaborated with global OEMs to supply engineering thermoplastics used in high-performance plastic gears that offer reduced weight and enhanced thermal resistance, particularly suitable for compact hybrid systems.

- These innovations not only enhance vehicle performance but also meet regulatory requirements, making lightweight and advanced gears a critical growth factor for the automotive sector.

Restraint/Challenge

“Fluctuating Raw Material Prices and Supply Chain Volatility”

- One of the primary restraints facing the automotive gears market is the volatility in raw material prices, particularly for steel, aluminum, and rare earth composites. Since gear manufacturing is heavily reliant on these materials, fluctuations can significantly impact production costs and profit margins.

- The industry also continues to face disruptions in global supply chains due to geopolitical tensions, logistics backlogs, and trade restrictions. These factors have led to increased lead times and erratic component availability.

- For instance, during the 2023 Russia-Ukraine conflict, several European automotive suppliers experienced steel shortages and elevated costs, which directly affected gear manufacturing operations.

- Small and mid-sized manufacturers, lacking robust procurement networks, are especially vulnerable to such volatility, which challenges their ability to meet OEM timelines and maintain competitive pricing.

Automotive Gears Market Scope

The market is segmented on the basis of material type, application, product type, and vehicle type.

- By Material Type

On the basis of material type, the Automotive Gears Market is segmented into metallic and non-metallic. The metallic segment dominated the largest market revenue share in 2024, driven by its high strength, durability, and wide usage in critical vehicle functions. Within this, steel gears are widely preferred due to their superior load-bearing capacity and cost-efficiency in mass production. Other subtypes such as aluminium, brass, cast iron, carbon steel, and magnetic alloys contribute to specific use cases across different automotive systems.

The non-metallic segment, including composites and plastics, is expected to witness the fastest growth during the forecast period. This is driven by the growing demand for lightweight materials that enhance fuel efficiency and reduce emissions, particularly in electric and hybrid vehicles..

- By Application

On the basis of application, the market is segmented into transmission system, differential system, steering system, and others. The transmission system segment held the largest revenue share in 2024, owing to the essential role gears play in managing torque and speed within both manual and automatic transmissions. The increasing global production of passenger and commercial vehicles continues to support this segment’s dominance.

The differential system segment is anticipated to grow steadily, supported by increased vehicle demand in off-road and utility applications. Meanwhile, the steering system and others (including timing gears and oil pump gears) are gaining traction due to the push toward advanced driver-assistance systems (ADAS) and electronic power steering (EPS).

- By Product Type

On the basis of product type, the market is segmented into intersecting shaft gears, skew shaft gears, planetary gears, non-metallic gears, parallel shaft gears, and others. The parallel shaft gears segment accounted for the largest revenue share in 2024 due to the widespread use of spur gear, rack and pinion gear, helical gear, and herringbone gear in various powertrain and drivetrain applications.

The intersecting shaft gear segment, comprising straight bevel gear and spiral bevel gear, and the skew shaft gear segment (including hypoid gear and worm gear) are vital in applications requiring angled torque transmission.

The planetary gears segment is projected to witness the fastest growth, particularly in electric vehicles (EVs) and hybrid powertrains due to their compact size and high torque capacity..

- By Vehicle Type

On the basis of vehicle type, the Automotive Gears Market is segmented into passenger cars and commercial vehicles. The passenger cars segment held the largest share in 2024, driven by the global expansion of urban mobility, increasing disposable incomes, and rising preference for automatic transmissions.

The commercial vehicles segment, including light commercial vehicles (LCVs) and heavy commercial vehicles (HCVs), is expected to grow at a notable CAGR, supported by infrastructure development, e-commerce logistics growth, and the electrification of fleet operations in major economies.

Automotive Gears Market Regional Analysis

- North America dominates the Automotive Gears Market with the largest revenue share of 32.51% in 2024, driven by a growing demand for home automation and security, as well as increased awareness of smart home technology.

- Consumers in the region highly value the convenience, advanced security features, and seamless integration offered by Automotive Gears with other smart devices such as thermostats and lighting systems.

- This widespread adoption is further supported by high disposable incomes, a technologically inclined population, and the growing preference for remote monitoring and control, establishing Automotive Gears as a favored solution for both residential and commercial properties.

U.S. Automotive Gears Market Insight

The U.S. Automotive Gears Market captured the largest revenue share of 73.55% in 2024 within North America, fueled by the swift uptake of connected devices and the expanding trend of home automation. Consumers are increasingly prioritizing the enhancement of home security through intelligent, keyless entry systems. The growing preference for DIY smart home setups, combined with robust demand for voice-controlled systems and mobile application integration, further propels the Automotive Gears industry. Moreover, the increasing integration of smart home technologies, such as Alexa, Google Assistant, and Apple HomeKit, is significantly contributing to the market's expansion.

Asia-Pacific Automotive Gears Market Insight

Asia-Pacific Automotive Gears Market is poised to grow at the fastest CAGR of 24% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards smart homes, supported by government initiatives promoting digitalization, is driving the adoption of Automotive Gears. Furthermore, as APAC emerges as a manufacturing hub for Automotive Gears components and systems, the affordability and accessibility of Automotive Gears are expanding to a wider consumer base.

China Automotive Gears Market Insight

The China Automotive Gears Market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and high rates of technological adoption. China stands as one of the largest markets for smart home devices, and Automotive Gears are becoming increasingly popular in residential, commercial, and rental properties. The push towards smart cities and the availability of affordable Automotive Gears options, alongside strong domestic manufacturers, are key factors propelling the market in China.

Japan Automotive Gears Market Insight

The Japan Automotive Gears Market is gaining momentum due to the country’s high-tech culture, rapid urbanization, and demand for convenience. The Japanese market places a significant emphasis on security, and the adoption of Automotive Gears is driven by the increasing number of smart homes and connected buildings. The integration of Automotive Gears with other IoT devices, such as home security cameras and lighting systems, is fueling growth. Moreover, Japan's aging population is likely to spur demand for easier-to-use, secure access solutions in both residential and commercial sectors.

Europe Automotive Gears Market Insight

Europe Automotive Gears Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent security regulations and the escalating need for enhanced security in homes and offices. The increase in urbanization, coupled with the demand for connected devices, is fostering the adoption of Automotive Gears. European consumers are also drawn to the convenience and energy efficiency these devices offer. The region is experiencing significant growth across residential, commercial, and multi-family housing applications, with Automotive Gears being incorporated into both new constructions and renovation projects.

Germany Automotive Gears Market Insight

The Germany Automotive Gears Market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of digital security and the demand for technologically advanced, eco-conscious solutions. Germany’s well-developed infrastructure, combined with its emphasis on innovation and sustainability, promotes the adoption of Automotive Gears, particularly in residential and commercial buildings. The integration of Automotive Gears with home automation systems is also becoming increasingly prevalent, with a strong preference for secure, privacy-focused solutions aligning with local consumer expectations

U.K. Automotive Gears Market Insight

The U.K. Automotive Gears Market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating trend of home automation and a desire for heightened security and convenience. Additionally, concerns regarding burglary and safety are encouraging both homeowners and businesses to choose keyless entry solutions. The UK’s embrace of connected devices, alongside its robust e-commerce and retail infrastructure, is expected to continue to stimulate market growth.

Automotive Gears Market Share

The Automotive Gears industry is primarily led by well-established companies, including:

- GKN Automotive Limited(United Kingdom)

- Bharat Gears Ltd.(India)

- DuPont (United States)

- American Axle & Manufacturing, Inc.(United States)

- ZF Friedrichshafen AG(Germany)

- Robert Bosch GmbH(Germany)

- IMS Gear(Germany)

- UNIVANCE CORPORATION(Japan)

- SHOWA CORPORATION (Japan)

- AmTech International(United States)

- RSB Group(India)

- The Hi-Tech Gears Ltd.(India)

- Melrose Industries PLC (United Kingdom)

- GREAT TAIWAN GEAR LTD.(Taiwan)

- Franz Morat Holding GmbH & Co. KG(Germany)

- B & R Machine and Gear Corporation(United States)

- Dynamatic Technologies Limited (India)

- UAG LLP.(United States)

- Dana Limited(United States)

- Eaton(Ireland)

Latest Developments in Global Automotive Gears Market

- In April 2024, ZF Friedrichshafen AG, a global technology leader in driveline and chassis technology, unveiled a new line of next-generation e-drive gear systems optimized for electric vehicles. The launch took place at Auto China 2024 in Beijing and showcased ZF’s commitment to advancing EV mobility through high-efficiency gear technologies that reduce noise and improve torque delivery. This development underlines ZF’s strategic focus on electrification and its ongoing efforts to lead the evolution of automotive powertrains globally.

- In March 2024, GKN Automotive, a leading supplier of automotive driveline components, announced the expansion of its manufacturing facility in Pune, India, aimed at increasing production capacity for precision gears used in hybrid and electric vehicles. This investment aligns with the rising demand for EVs in Asia-Pacific and reflects the company’s strategy to support regional OEMs through localized, high-quality gear production tailored to emerging market requirements.

- In February 2024, American Axle & Manufacturing, Inc. (AAM) entered into a strategic partnership with BorgWarner Inc. to jointly develop modular gear assemblies for electric powertrains. This collaboration is set to accelerate the commercialization of lightweight, compact gear units designed to improve EV performance while reducing production complexity. The partnership signifies a broader industry move toward cooperative innovation in response to rapid electrification trends.

- In January 2024, Dana Incorporated launched a new thermal-resistant gear lubricant technology under its Spicer brand, designed specifically for high-torque electric vehicle gears. Introduced at CES 2024 in Las Vegas, the product enhances gear life, reduces friction, and supports efficient energy transfer in advanced EV systems. This innovation positions Dana as a key enabler of durable, sustainable mobility technologies.

- In December 2023, DuPont Mobility & Materials expanded its portfolio of polymer-based gear materials, introducing a new grade of high-performance thermoplastics for use in compact hybrid transmission systems. Developed in response to automakers’ increasing demand for lightweight, high-strength solutions, these materials are engineered to withstand high temperatures and torque loads while improving fuel efficiency and reducing emissions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.