Global Automotive Linear Positions Sensors Market

Market Size in USD Billion

USD

29.60 Billion

USD

56.43 Billion

2025

2033

USD

29.60 Billion

USD

56.43 Billion

2025

2033

| 2026 - 2033 | |

| USD 29.60 Billion | |

| USD 56.43 Billion | |

| % | |

|

Automotive Linear Positions Sensors Market Overview

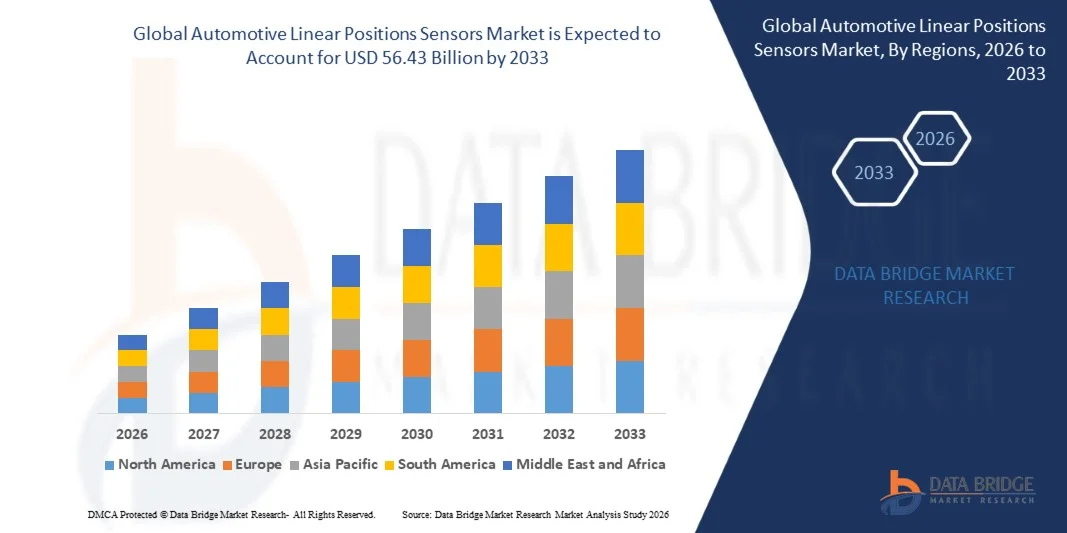

The Automotive Linear Positions Sensors Market was valued at USD 29.6 Billion in 2025 and is projected to reach USD 56.43 Billion by 2033, growing at a CAGR of 8.40% from 2026 to 2033. The market is experiencing consistent growth driven by rising integration of advanced sensing technologies in vehicles, increasing demand for electric and hybrid vehicles, and growing adoption of ADAS and drive-by-wire systems. Expanding use of linear position sensors in powertrain, chassis, steering, and safety systems is further supporting market growth across global automotive manufacturing hubs.

The increasing global shift toward vehicle electrification and stringent emission regulations is accelerating the adoption of high-precision, contactless sensing solutions in automotive systems. Automakers are increasingly replacing mechanical sensing components with electronic linear position sensors to improve efficiency, durability, and real-time control performance. Continuous advancements in sensor miniaturization, accuracy, and semiconductor integration are further enhancing their application across next-generation connected, autonomous, and electric vehicles.

Key Market Trends & Insights

- Asia-Pacific dominated the Automotive Linear Positions Sensors Market with the largest revenue share of 45% in 2025, supported by high automotive production volumes, rapid electrification, and strong integration of advanced sensing technologies in passenger and commercial vehicles

- The passenger vehicle segment led the market with a 72% share in 2025, driven by high production volumes and rapid adoption of advanced driver assistance systems

- North America is expected to be the fastest-growing region at a CAGR of 15.3% from 2026 to 2033, fueled by rapid adoption of electric vehicles, increasing integration of advanced automotive electronics, and strong demand for autonomous driving technologies

- Electric vehicle is the fastest-growing vehicle type, projected to register a CAGR of 16% from 2026 to 2033, supported by rapid global electrification and increasing deployment of advanced electronic control systems

- The mid end segment dominated the vehicle type category with a 38% revenue share in 2025, led by high production volumes and widespread integration of sensor-based control systems in affordable passenger vehicles

- Powertrain accounted for 40% of the market in 2025, preferred by extensive use of linear position sensors in transmission control, throttle systems, and engine management units

- The vehicle body segment is the fastest-growing type category, with a CAGR of 15% from 2026 to 2033, driven by rising adoption of advanced comfort, safety, and automation features

Market Size & Forecast

- Global Market Value (2025): USD 29.6 Billion

- Expected Market Value (2033): USD 56.43 Billion

- Forecast CAGR (2026–2033): 8.40%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Automotive Linear Positions Sensors Market Segmentation

|

Attributes |

Automotive Linear Positions Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Analog Devices, Inc. (U.S.) · Bosch Sensortec GmbH (Germany) · BOURNS, INC. (U.S.) · Continental AG (Germany) · CTS Corporation (U.S.) · Gill Sensors & Controls (U.K.) · HELLA GmbH & Co. KGaA (Germany) · Infineon Technologies AG (Germany) · NXP Semiconductors (Netherlands) · Sensata Technologies (U.S.) · Stoneridge, Inc. (U.S.) · Penn Engineering (U.S.) · Illinois Tool Works Inc. (U.S.) · Stanley Black & Decker, Inc. (U.S.) · MW Industries, Inc. (U.S.) · DENSO CORPORATION (Japan) · Autoliv Inc. (Sweden) · Maxim Integrated (U.S.) · Hitachi Astemo Americas, Inc. (U.S.) · GMS Instruments BV (Netherlands) · Broadcom (U.S.) · Piher Sensors & Controls (Spain) · Elmos Semiconductor SE (Germany) |

|

Market Opportunities |

· Expansion in Electric Vehicle Powertrain Applications · Growth in Autonomous and Semi-Autonomous Vehicle Platforms · Increasing Adoption in Commercial Vehicle Fleet Electrification and Telematics Systems |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Linear Positions Sensors Market Trends

Trend: Rising Adoption of Contactless Linear Position Sensors in EV and ADAS Systems

Automotive manufacturers are increasingly shifting toward contactless linear position sensors to improve accuracy, durability, and performance in electric and autonomous vehicle platforms. These sensors are widely deployed in throttle control, braking systems, steering modules, and transmission units to support drive-by-wire and ADAS functionalities. Growing electrification of vehicles and replacement of mechanical potentiometers with Hall-effect and inductive sensing technologies are accelerating this trend.

Companies such as Infineon Technologies AG and NXP Semiconductors are actively advancing automotive-grade sensor ICs used in EV powertrains and safety-critical systems, strengthening adoption across global OEM platforms.

Automotive Linear Positions Sensors Market Dynamics

Key Market Driver: Growing Demand for EVs and Advanced Driver Assistance Technologies

The rapid expansion of electric vehicles and ADAS integration is significantly driving demand for high-precision linear position sensors across automotive systems. These sensors are essential for real-time monitoring and control in battery management systems, steering feedback, and automated braking functions. Increasing regulatory focus on vehicle safety and emissions reduction is further accelerating their deployment in next-generation vehicles.

Major automotive suppliers such as Bosch Sensortec GmbH and Continental AG are expanding sensor-based solutions for EV and ADAS platforms, enhancing vehicle intelligence and control accuracy.

Key Restraint/Challenge: High Cost and Integration Complexity in Legacy Vehicle Platforms

High development costs and complex integration into existing internal combustion engine architectures remain key challenges for market growth. Retrofitting linear position sensors into legacy mechanical systems requires redesign of control modules, wiring architecture, and electronic interfaces, increasing overall implementation costs. Compatibility issues between modern sensor technologies and older vehicle platforms further slow down large-scale adoption.

Automotive Tier-1 suppliers such as Sensata Technologies face continued challenges in balancing advanced sensor deployment with cost-sensitive mass-market vehicle production.

Key Market Opportunity: Expansion in Electric Vehicle Powertrain Applications

The growing electrification of vehicle powertrains presents significant opportunities for linear position sensor integration in motor control, transmission systems, and regenerative braking mechanisms. EV architectures require precise motion sensing to optimize efficiency, torque control, and energy recovery performance. Increasing investments in EV platforms by global automakers are further expanding application scope across passenger and commercial vehicles.

Companies such as Infineon Technologies AG and NXP Semiconductors are actively developing advanced sensing solutions tailored for EV powertrain systems, supporting the transition toward fully electrified mobility ecosystems.

Automotive Linear Positions Sensors Market Scope

The automotive linear positions sensors market is segmented on the basis of vehicle type, type, end-user, and application.

- By Vehicle Type

On the basis of vehicle type, the global Automotive Linear Position Sensors market is segmented into high end, mid end, low end, and electric vehicles. The Mid End segment dominated the market with the largest share of 38% in 2025, driven by high production volumes and widespread integration of sensor-based control systems in affordable passenger vehicles. Rising demand for fuel efficiency and emission compliance has accelerated adoption of linear position sensors in this category. Automotive OEMs in emerging economies are increasingly equipping mid range vehicles with advanced sensing technologies. Strong balance between cost efficiency and performance further reinforces its dominant position. Continuous expansion of mass-market vehicle production supports sustained leadership.

The Electric Vehicles segment is projected to register the fastest growth at a CAGR of 16% from 2026 to 2033, driven by rapid global electrification and increasing deployment of advanced electronic control systems. Growing demand for precise position monitoring in battery management, braking systems, and regenerative control is boosting sensor integration. Rising investments by EV manufacturers in intelligent vehicle architecture are further accelerating adoption. Regulatory push toward zero emission mobility is expanding EV penetration across major markets. Continuous innovation in sensor miniaturization and accuracy enhances deployment across electric platforms.

- By Type

On the basis of type, the market is segmented into chassis, powertrain, and vehicle body. The Powertrain segment dominated the market with a share of 40% in 2025, supported by extensive use of linear position sensors in transmission control, throttle systems, and engine management units. Increasing demand for optimized fuel efficiency and enhanced drivetrain performance has strengthened sensor integration in powertrain systems. Established automotive manufacturing ecosystems further support large-scale deployment. High reliability requirements in engine and transmission applications reinforce its leading position. Continuous technological upgrades in propulsion systems sustain dominance.

The Vehicle Body segment is projected to register the fastest growth at a CAGR of 15% from 2026 to 2033, driven by rising adoption of advanced comfort, safety, and automation features. Increasing integration of sensors in seat adjustment, door systems, and HVAC controls is accelerating demand. Growing focus on intelligent cabin experience in both ICE and electric vehicles is further supporting expansion. OEM investments in smart vehicle interiors are enhancing deployment of position sensing technologies. Rising consumer preference for connected and automated vehicle features strengthens long-term growth.

- By End-user

On the basis of end-user, the market is segmented into passenger vehicles and commercial vehicles. The Passenger Vehicles segment dominated the market with the largest share of 72% in 2025, driven by high production volumes and rapid adoption of advanced driver assistance systems. Increasing consumer demand for safety, comfort, and automation has significantly boosted sensor integration in passenger cars. Strong presence of global OEMs focusing on technology-rich vehicles further supports growth. Expanding urban mobility and rising disposable incomes reinforce dominance. Continuous innovation in passenger vehicle electronics sustains market leadership.

The Commercial Vehicles segment is projected to register the fastest growth at a CAGR of 14% from 2026 to 2033, driven by rising demand for fleet automation and operational efficiency. Increasing adoption of sensors in heavy-duty trucks and logistics vehicles is improving performance monitoring and safety systems. Growth in e-commerce and freight transportation is further accelerating deployment. Fleet operators are increasingly investing in predictive maintenance and smart vehicle systems. Expanding regulatory focus on safety and emissions compliance supports long-term adoption.

- By Application

On the basis of application, the market is segmented into engine, power transmission, gear box, steering and pedals, and others. The Engine segment dominated the market with a share of 35% in 2025, driven by extensive use of linear position sensors for combustion control, valve positioning, and fuel injection systems. Rising demand for engine efficiency and emission reduction technologies has strengthened sensor deployment. Established integration in internal combustion engine architectures supports large-scale usage. Continuous optimization of engine performance systems reinforces its leading position. Strong OEM focus on precision engine control sustains dominance.

The Steering and Pedals segment is projected to register the fastest growth at a CAGR of 15% from 2026 to 2033, driven by increasing adoption of advanced driver assistance systems and electronic control units. Growing shift toward drive-by-wire technologies is significantly boosting sensor usage in steering and pedal mechanisms. Rising demand for autonomous and semi-autonomous vehicles further accelerates integration. OEM investments in vehicle safety and control precision are enhancing deployment. Continuous advancements in electronic steering systems support long-term expansion.

Automotive Linear Positions Sensors Market Regional Analysis

Asia-Pacific dominated the automotive linear positions sensors market and accounted for the largest revenue share of 45% in 2025, supported by high automotive production volumes, rapid electrification, and strong integration of advanced sensing technologies in passenger and commercial vehicles. The region benefits from a well-established automotive manufacturing base, cost-efficient electronics production, and increasing deployment of electric vehicles across major economies. Rising demand for fuel-efficient powertrains, expanding vehicle safety regulations, and growing adoption of ADAS technologies are accelerating market expansion. Strong presence of OEMs and component suppliers further reinforces regional leadership in sensor integration across multiple vehicle systems.

China Automotive Linear Position Sensors Market Insight

China held the largest share in the Asia-Pacific market in 2025, driven by its dominant position in global automotive manufacturing and rapid EV adoption. The country has a strong electronics and semiconductor ecosystem that supports large-scale production of linear position sensors for powertrain, chassis, and body applications. Increasing penetration of intelligent vehicles, coupled with strong government support for new energy vehicles, is further strengthening demand. Expanding exports of automotive components and continuous investments in smart mobility infrastructure are reinforcing China’s leadership in the regional market.

India Automotive Linear Position Sensors Market Insight

India is projected to register the fastest growth in the Asia-Pacific region, driven by rising vehicle production, increasing adoption of safety systems, and expanding electrification initiatives. Growing demand for passenger vehicles and commercial fleets is accelerating integration of sensor-based control systems in engines, steering, and transmission units. Expanding automotive manufacturing under localization programs is further supporting component demand. Increasing focus on affordable electric mobility and connected vehicle technologies is enhancing long-term market growth across the country.

Europe Automotive Linear Position Sensors Market Insight

The Europe Automotive Linear Position Sensors market is witnessing steady growth, supported by stringent emission regulations, strong adoption of EVs, and advanced automotive engineering capabilities. Increasing demand for high-precision sensing systems in powertrain optimization, safety applications, and autonomous driving technologies is driving market expansion. The region benefits from strong R&D investments and established automotive OEM networks. Rising focus on sustainable mobility and vehicle efficiency is further strengthening adoption of linear position sensors across multiple vehicle platforms.

Germany Automotive Linear Position Sensors Market Insight

Germany accounted for the largest share in the Europe market in 2025, driven by its strong automotive manufacturing base and leadership in premium vehicle production. High integration of advanced electronic control systems in engines, transmissions, and vehicle safety applications is boosting demand for linear position sensors. The country’s focus on automotive innovation, particularly in EV and hybrid technologies, is further supporting market expansion. Strong presence of global OEMs and Tier-1 suppliers reinforces Germany’s dominance in precision sensing technologies.

U.K. Automotive Linear Position Sensors Market Insight

The U.K. market is supported by increasing adoption of electric vehicles, rising demand for advanced driver assistance systems, and growing focus on vehicle safety technologies. Expanding automotive R&D activities and increasing integration of smart sensing systems in vehicle interiors and control units are driving market growth. Strong emphasis on reducing emissions and improving vehicle efficiency is further accelerating sensor deployment. In addition, growing investments in connected and autonomous vehicle development are supporting long-term expansion of the market.

North America Automotive Linear Position Sensors Market Insight

North America is projected to register the fastest growth at a CAGR of 15.3% from 2026 to 2033, driven by rapid adoption of electric vehicles, increasing integration of advanced automotive electronics, and strong demand for autonomous driving technologies. Rising focus on vehicle safety, performance optimization, and emissions reduction is accelerating deployment of linear position sensors across multiple applications. Expanding investments by automotive OEMs in smart mobility and software-defined vehicles is further supporting market growth. Strong technological advancements in sensor accuracy and durability reinforce regional expansion.

U.S. Automotive Linear Position Sensors Market Insight

The U.S. accounted for the largest share in the North America market in 2025, supported by strong automotive production, high EV penetration, and advanced technology adoption across vehicle systems. Increasing use of linear position sensors in powertrain control, steering systems, and braking applications is driving market growth. The country benefits from strong presence of leading automotive OEMs and technology providers focusing on autonomous and connected vehicle development. Rising consumer demand for safety, efficiency, and intelligent mobility solutions is further strengthening market expansion.

Automotive Linear Positions Sensors Market Share

The automotive linear positions sensors industry is primarily led by well-established companies, including:

- Analog Devices, Inc. (U.S.)

- Bosch Sensortec GmbH (Germany)

- BOURNS, INC. (U.S.)

- Continental AG (Germany)

- CTS Corporation (U.S.)

- Gill Sensors & Controls (U.K.)

- HELLA GmbH & Co. KGaA (Germany)

- Infineon Technologies AG (Germany)

- NXP Semiconductors (Netherlands)

- Sensata Technologies (U.S.)

- Stoneridge, Inc. (U.S.)

- Penn Engineering (U.S.)

- Illinois Tool Works Inc. (U.S.)

- Stanley Black & Decker, Inc. (U.S.)

- MW Industries, Inc. (U.S.)

- DENSO CORPORATION (Japan)

- Autoliv Inc. (Sweden)

- Maxim Integrated (U.S.)

- Hitachi Astemo Americas, Inc. (U.S.)

- GMS Instruments BV (Netherlands)

- Broadcom (U.S.)

- Piher Sensors & Controls (Spain)

- Elmos Semiconductor SE (Germany)

Latest Developments in Automotive Linear Positions Sensors Market

- In 2025, Allegro MicroSystems expanded its automotive-grade linear position sensing portfolio to enhance performance in EVs, ADAS, and powertrain systems. This development significantly improves sensing accuracy, thermal stability, and resistance to electromagnetic interference, making sensors more reliable in harsh automotive environments. The expansion strengthens adoption of contactless sensing in electric mobility platforms where durability and precision are critical. It also reinforces Allegro’s competitive positioning in high-growth EV and safety-critical applications

- In 2025, Continental AG enhanced integration of linear position sensors within chassis and powertrain systems, including braking, suspension, and transmission applications. This development improves real-time vehicle control, energy efficiency, and system-level safety performance. The impact supports the transition toward software-defined and electrified vehicle platforms with higher sensor dependency. It also strengthens Continental’s position in delivering integrated sensing ecosystems for advanced mobility solutions

- In 2025, Melexis introduced enhanced contactless linear position sensor ICs for automotive applications, focusing on pedal, steering, and transmission control systems. This advancement improves system longevity by reducing mechanical wear while increasing measurement precision in dynamic driving conditions. The impact is strong across EV platforms where high reliability and compact sensing solutions are required. It further accelerates the shift from traditional potentiometer-based systems to advanced semiconductor-based sensing architectures

- In 2024, TE Connectivity advanced its inductive and magnetic position sensor solutions for automotive systems, targeting braking, throttle, and chassis control applications. This development improves operational safety, robustness, and long-term stability in electrified and high-performance vehicles. It also supports OEM demand for rugged sensing systems capable of performing under extreme temperature and vibration conditions. The impact strengthens integration of precision sensing in next-generation vehicle control systems

- In 2024, Honeywell expanded deployment of its Hall-effect linear position sensing technologies across automotive throttle, transmission, and pedal systems. This advancement enhances accuracy and reduces mechanical degradation in high-duty-cycle automotive environments. The impact is particularly significant for hybrid and electric vehicles, where electronic control precision directly influences efficiency and safety. It reinforces Honeywell’s role in enabling durable, non-contact sensing solutions across evolving automotive architectures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.