Global Blood Cancer Drug Market

Market Size in USD Billion

USD

5.30 Billion

USD

8.19 Billion

2024

2032

USD

5.30 Billion

USD

8.19 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.30 Billion | |

| USD 8.19 Billion | |

| % | |

|

Blood Cancer Drug Market Size

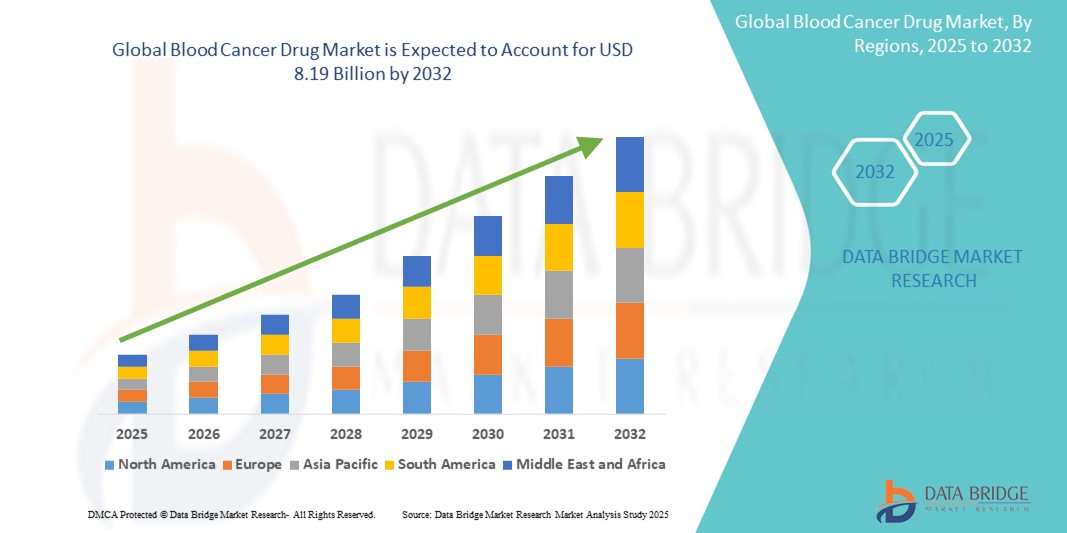

- The global blood cancer drug market size was valued at USD 5.30 billion in 2024 and is expected to reach USD 8.19 billion by 2032, at a CAGR of 5.60% during the forecast period

- The market growth for blood cancer drugs is largely fueled by the increasing global incidence and prevalence of various hematological malignancies, such as leukemia, lymphoma, and multiple myeloma. This rising disease burden, driven by factors such as an aging population and environmental influences, creates a continuous and growing demand for effective therapeutic interventions

- Furthermore, significant advancements in cancer research and development are introducing novel and more effective treatment options. This includes the development of targeted therapies, immunotherapies (such as CAR-T cell therapies and monoclonal antibodies), and personalized medicine approaches, which are transforming treatment outcomes and establishing these innovative drugs as the modern standard of care. These converging factors are accelerating the uptake of blood cancer drug solutions, thereby significantly boosting the industry's growth

Blood Cancer Drug Market Analysis

- The market growth for blood cancer drugs is largely fueled by the increasing global incidence and prevalence of various hematological malignancies, such as leukemia, lymphoma, and multiple myeloma. This rising disease burden, driven by factors such asan aging global population and improved diagnostic techniques, creates a continuous and growing demand for effective therapeutic interventions

- Furthermore, significant technological progress within oncology research and development is introducing novel and highly effective treatment modalities. These include the advent of targeted therapies, revolutionary immunotherapies (such as CAR-T cell therapies and bispecific antibodies), and personalized medicine approaches, which are fundamentally reshaping patient outcomes and establishing these innovative drugs as the modern standard of care. These converging factors are accelerating the uptake of blood cancer drug solutions, thereby significantly boosting the industry's growth

- North America dominates the blood cancer drug market with the largest revenue share of 39.1% in 2024. This leadership is characterized by a high prevalence of blood cancer diagnoses, robust healthcare expenditure, advanced research and development capabilities, strong presence of leading pharmaceutical and biotechnology companies, and favorable reimbursement policies for innovative therapies in countries

- Asia-Pacific is expected to be the fastest-growing region in the blood cancer drug market during the forecast period, with an estimated CAGR of 9.8% from 2025 to 2032. This rapid growth is largely due to increasing healthcare investments, rising awareness of cancer, a growing burden of non-communicable diseases, improving access to advanced medical treatments, and a vast patient population in emerging economies across the region

- Medication segment dominates the blood cancer drug market with a market share of 50.3% in 2024, driven by its widespread use as a primary treatment and continuous development of novel drug formulations

Report Scope and Blood Cancer Drug Market Segmentation

|

Attributes |

Blood Cancer Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Blood Cancer Drug Market Trends

“Continuous Advancement in Targeted Therapies and Immunotherapies”

- A significant and accelerating trend in the global blood cancer drug market is the continuous advancement in targeted therapies and immunotherapies, which are fundamentally reshaping treatment outcomes. This includes the increasing adoption of highly specific drugs that block cancer-promoting pathways and revolutionary cell-based therapies such asCAR-T, offering patients more precise and effective treatment options with potentially fewer systemic side effects compared to traditional chemotherapy

- For instance, CAR-T cell therapies have become a game-changer for certain types of leukemia and lymphoma, demonstrating remarkable efficacy in patients who have failed other treatments. Similarly, the development and expanded use of monoclonal antibodies such asthose targeting CD38 in multiple myeloma continue to provide substantial benefits, often as part of new combination regimens

- Innovation in the blood cancer drug market also enables features such as more personalized treatment approaches based on the genetic and molecular makeup of a patient's tumor. This allows for tailoring therapies to individual patient profiles, leading to higher treatment success rates. For instance, the understanding of specific mutations, such asBCR-ABL in Chronic Myeloid Leukemia (CML) or BTK in certain B-cell cancers, has led to the development of highly effective inhibitors that precisely target these drivers

- The seamless integration of advanced diagnostic tools, such as liquid biopsies and measurable residual disease (MRD) testing, with therapeutic strategies facilitates real-time monitoring of disease status and treatment effectiveness. This creates a unified approach to cancer management, allowing for earlier detection of relapse or resistance and more timely adjustment of treatment plans

- This trend towards more intelligent, intuitive, and interconnected therapeutic strategies is fundamentally reshaping user expectations for cancer treatment. Consequently, pharmaceutical and biotechnology companies are continually investing in research and development to bring forth next-generation therapies, including novel targets, combination regimens, and advanced drug delivery systems, aiming for improved efficacy and patient quality of life

- The demand for blood cancer drugs that offer enhanced personalization, superior efficacy, and reduced toxicity is growing rapidly across healthcare sectors, as clinicians increasingly prioritize precision medicine and comprehensive patient care

Blood Cancer Drug Market Dynamics

Driver

“Rising Incidence of Hematologic Malignancies and Advancements in Targeted Therapies”

- The increasing global burden of blood cancers—including leukemia, lymphoma, and multiple myeloma—is a key driver accelerating the demand for innovative treatment options within the blood cancer drug market

- For instance, in January 2024, AbbVie Inc. and Genmab A/S announced positive Phase 3 results for their bispecific antibody epcoritamab (Epkinly) in treating diffuse large B-cell lymphoma (DLBCL), highlighting the significant potential of targeted immunotherapies in improving survival outcomes. Such clinical milestones underscore the ongoing innovation within the blood cancer drug landscape

- Continuous advancements in personalized medicine, including the development of CAR T-cell therapies, monoclonal antibodies, and small-molecule inhibitors, are expanding treatment options, enabling higher efficacy with fewer side effects compared to traditional chemotherapy

- In addition, increased healthcare spending, improved diagnostics, and awareness campaigns by organizations such as the Leukemia & Lymphoma Society (LLS) are encouraging early diagnosis and treatment uptake, further driving market growth

- The surge in FDA and EMA approvals for novel agents and combination regimens, along with expanded indications for existing therapies, is boosting the availability of effective solutions across all stages of disease progression

Restraint/Challenge

“High Treatment Costs and Access Barriers in Low-Income Regions”

- Despite promising advancements, the high cost of novel therapies remains a critical challenge in the blood cancer drug market. Treatments such as CAR T-cell therapies (such as Kymriah, Yescarta) can exceed USD 400,000 per patient, limiting accessibility in resource-constrained settings

- For instance, in 2023, reports from several global health organizations emphasized disparities in access to cutting-edge treatments between high-income and low-income countries, with affordability and lack of infrastructure posing significant barriers to equitable care

- Reimbursement complexities and limited insurance coverage for expensive therapies in many regions contribute to delayed treatment or under-treatment, especially among economically disadvantaged populations

- In addition, logistical hurdles associated with advanced therapies, such as the need for specialized manufacturing, cold chain requirements, and transplant center accreditation, further restrict widespread adoption

- Overcoming these challenges will require policy-level interventions to subsidize costs, expanded global partnerships for clinical trials, and innovative pricing models such as outcome-based reimbursement and tiered pricing

Blood Cancer Drug Market Scope

The market is segmented on the basis of type, treatment, diagnosis, dosage form, end-user, and distribution channel.

• By Type

On the basis of type, the blood cancer drug market is segmented into leukaemia, lymphoma, and myeloma. The leukaemia segment held the largest market revenue share of 47.6% in 2024, driven by its high global prevalence and the availability of multiple approved therapies. The market also sees strong demand for leukaemia drugs due to ongoing advancements in targeted treatment options and increasing diagnosis rates across major regions.

The lymphoma segment is anticipated to witness the fastest growth rate of 19.8% from 2025 to 2032, fueled by increasing awareness, favorable reimbursement policies, and growing clinical research activity supporting next-generation therapeutics.

• By Treatment

On the basis of treatment, the blood cancer drug market is segmented into medication, radiation therapy, stem cell transplant, and others. The medication segment held the largest market revenue share of 50.3% in 2024, driven by its broad applicability across blood cancer types and widespread use in both hospital and home settings. The stem cell transplant segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing adoption of personalized therapy and rising success rates in relapse prevention and long-term remission.

• By Diagnosis

On the basis of diagnosis, the blood cancer drug market is segmented into blood tests, bone marrow biopsy, urine tests, and imaging tests. The blood tests segment held the largest market revenue share in 2024, driven by their importance in early-stage detection, disease monitoring, and therapy optimization.

The bone marrow biopsy segment is expected to witness the fastest CAGR from 2025 to 2032, favored for its diagnostic accuracy, especially in cases requiring cellular and molecular-level assessment to guide treatment strategy.

• By Dosage Form

On the basis of dosage form, the blood cancer drug market is segmented into capsule, tablets, injections, and others. The injections segment held the largest market revenue share in 2024, driven by their established role in chemotherapy and biologic drug administration, which require intravenous delivery in clinical settings.

The tablets segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the development of oral targeted therapies and patient preference for self-administered treatment options that enhance compliance and convenience.

• By End-User

On the basis of end-user, the blood cancer drug market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment accounted for the largest market revenue share in 2024, driven by advanced treatment infrastructure, availability of multidisciplinary care, and access to specialized oncology staff.

The homecare segment is expected to witness the fastest CAGR from 2025 to 2032, driven by rising preference for home-based care, expanding use of oral therapies, and cost-effectiveness in long-term treatment management.

• By Distribution Channel

On the basis of distribution channel, the blood cancer drug market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment held the largest market revenue share in 2024, driven by their integration into inpatient care workflows and management of high-value oncology drugs.

The online pharmacy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing digital health trends, convenience of doorstep delivery, and increasing patient engagement with e-health platforms.

Blood Cancer Drug Market Regional Analysis

- North America dominates the blood cancer drug market with the largest revenue share of 39.1% in 2024, driven by a well-established healthcare infrastructure, high prevalence of hematologic malignancies, and robust investment in oncology research and development

- Patients in the region benefit from early diagnosis, access to advanced therapeutics, and supportive reimbursement frameworks that encourage treatment adherence and the use of innovative therapies

- This strong market position is further supported by the presence of leading pharmaceutical companies, ongoing clinical trials, and growing adoption of personalized medicine, establishing North America as a key hub for blood cancer drug innovation and consumption

U.S. Blood Cancer Drug Market Insight

The U.S. blood cancer drug market captured the largest revenue share of 82% in 2024 within North America, fueled by high incidence rates of leukemia and lymphoma and a well-established healthcare infrastructure. The strong presence of biopharmaceutical companies and accelerated FDA approvals for novel therapies further propel the Blood Cancer Drug industry. Moreover, increasing investment in cancer research, along with the growing implementation of precision medicine and immunotherapy, is significantly contributing to the market’s expansion.

Europe Blood Cancer Drug Market Insight

The Europe blood cancer drug market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by favorable regulatory frameworks and rising cancer awareness campaigns. Increasing access to early diagnostic tools, coupled with government funding for cancer research, is fostering the adoption of advanced blood cancer therapeutics. The region is witnessing significant growth across both public and private healthcare sectors, with targeted therapies being incorporated into standard treatment regimens.

U.K. Blood Cancer Drug Market Insight

The U.K. blood cancer drug market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the expanding NHS cancer care infrastructure and growing incidence of hematologic malignancies. In addition, a focus on value-based care and early adoption of novel biologics and CAR T-cell therapies are encouraging market expansion. The U.K.’s involvement in global oncology trials and its established pharmaceutical pipeline are expected to continue to stimulate market growth.

Germany Blood Cancer Drug Market Insight

The Germany blood cancer drug market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing demand for personalized medicine and strong support for oncology innovation. Germany’s advanced clinical research network, combined with its focus on early cancer detection, promotes the adoption of new blood cancer treatments. Integration of targeted therapies into treatment protocols is becoming increasingly prevalent, with strong healthcare reimbursement structures aligning with local patient and provider expectations.

Asia-Pacific Blood Cancer Drug Market Insight

The Asia-pacific blood cancer drug market is poised to grow at the fastest CAGR of 9.8% during the forecast period of 2025 to 2032, driven by rising cancer burden, growing healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region's increasing access to diagnostics and evolving treatment landscapes are driving demand for blood cancer drugs. Furthermore, as APAC becomes a strategic focus for clinical trials and biotech expansion, affordability and accessibility of novel therapies are reaching a wider patient base.

Japan Blood Cancer Drug Market Insight

The Japan blood cancer drug market is gaining momentum due to the country’s aging population, strong pharmaceutical innovation, and demand for precision oncology. The Japanese market places a significant emphasis on high-quality cancer care, and the adoption of advanced immunotherapies and molecular diagnostics is driving growth. Moreover, Japan's universal healthcare system and collaborative efforts in cancer R&D are likely to spur demand for next-generation therapies across both inpatient and outpatient settings.

China Blood Cancer Drug Market Insight

The China blood cancer drug market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country’s expanding healthcare reforms, rapid urbanization, and high cancer prevalence. China stands as one of the fastest-growing markets for oncology therapeutics, with blood cancer drugs gaining traction in both tier-1 hospitals and regional centers. The push towards precision medicine, along with growing participation in international clinical trials and strong domestic biotech innovation, are key factors propelling the market in China.

Blood Cancer Drug Market Share

The blood cancer drug industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Viatris Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Ireland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Lilly (U.S.)

- Merck & Co., Inc. (U.S.)

- AstraZeneca (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Amgen Inc. (U.S.)

- Biogen Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Samsung Bioepis (South Korea)

- Lupin Pharmaceuticals (India)

Latest Developments in Global Blood Cancer Drug Market

- In August 2023, The U.S. FDA granted accelerated approval to Pfizer's Elrexfio (elranatamab), a bispecific antibody targeting BCMA-expressing multiple myeloma cells. This provides a novel option for patients with relapsed or refractory multiple myeloma

- In April 2023, the FDA approved Omisirge (omidubicel-onlv), a cord blood-derived stem cell therapy, for use in adult and pediatric patients (12 years and older) with hematologic malignancies (blood cancers) who are planned for umbilical cord blood transplantation following myeloablative conditioning. This approval was specifically aimed at reducing the time to neutrophil recovery and the incidence of infection post-transplantation

- In March 2024, Breyanzi, a CAR-T cell therapy, received FDA approval for treating chronic lymphocytic leukemia (CLL) and small lymphocytic lymphoma (SLL), adding to its prior approvals for large B-cell lymphoma

- In March 2023, Pfizer announced its definitive merger agreement to acquire Seagen Inc., a global biotechnology company specializing in transformative cancer medicines, for approximately USD 43 billion in cash. The acquisition was successfully completed in December 2023 after receiving necessary regulatory approvals

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.