Global Cancer Stem Cell Therapy Market

Market Size in USD Billion

USD

1.41 Billion

USD

2.94 Billion

2025

2033

USD

1.41 Billion

USD

2.94 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.41 Billion | |

| USD 2.94 Billion | |

| % | |

|

Cancer Stem Cell Therapy Market Size

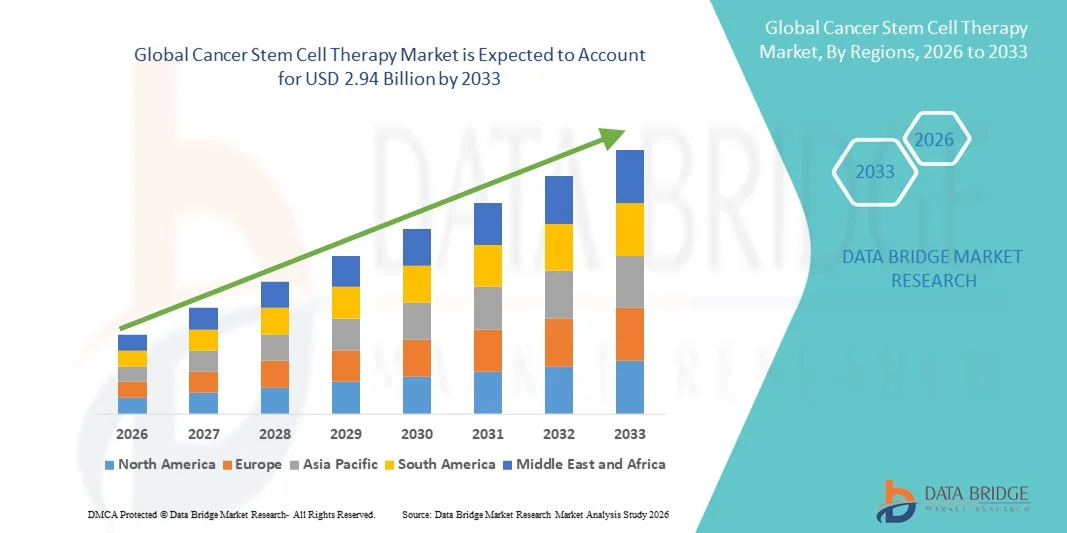

- The global cancer stem cell therapy market size was valued at USD 1.41 billion in 2025 and is expected to reach USD 2.94 billion by 2033, at a CAGR of 9.65% during the forecast period

- The market growth is primarily driven by the increasing prevalence of cancer worldwide, coupled with rising investment in advanced stem cell research and targeted therapeutic solutions. Growing awareness about personalized medicine and the potential of stem cell therapies in improving treatment outcomes is further propelling market adoption

- In addition, technological advancements in cell isolation, culture, and delivery techniques, along with supportive regulatory frameworks, are enhancing the development and commercialization of cancer stem cell therapies. These factors collectively are fostering significant growth in the global market

Cancer Stem Cell Therapy Market Analysis

- Cancer stem cell therapies, offering targeted treatment by eliminating tumor-initiating cells, are increasingly recognized as vital in modern oncology due to their potential to reduce recurrence, enhance treatment efficacy, and improve overall patient outcomes

- The rising demand for these therapies is primarily fueled by the growing prevalence of cancers globally, increased investment in stem cell research, and heightened focus on personalized medicine approaches

- North America dominated the cancer stem cell therapy market with the largest revenue share of 38.7% in 2025, driven by advanced healthcare infrastructure, significant R&D investment, early adoption of novel therapies, and the strong presence of key market players in the U.S., supported by favorable regulatory frameworks that accelerate clinical translation

- Asia-Pacific is expected to be the fastest growing region in the cancer stem cell therapy market during the forecast period due to increasing cancer incidence, expanding healthcare access, rising research initiatives, and growing collaborations between local and global biotech companies

- Stem cell-based cancer therapy segment dominated the market in 2025 with a market share of 40.2%, propelled by its proven efficacy in targeting resistant cancer cells and increasing clinical adoption across various cancer types

Report Scope and Cancer Stem Cell Therapy Market Segmentation

|

Attributes |

Cancer Stem Cell Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cancer Stem Cell Therapy Market Trends

Advancement in Personalized CSC Therapies

- A significant and accelerating trend in the global cancer stem cell therapy market is the increasing development of personalized therapies that target patient-specific cancer stem cell profiles, enhancing treatment efficacy and reducing recurrence

- For instance, BioRestor Therapeutics is developing customized CSC therapies for hematologic malignancies by analyzing individual tumor stem cell characteristics to tailor treatment regimens

- Advances in genomic profiling and biomarker identification allow therapies to be more precise, predicting patient response and minimizing off-target effects, thereby improving clinical outcomes

- The integration of high-throughput screening and molecular analysis tools facilitates rapid identification of effective therapeutic strategies, enabling clinicians to optimize patient-specific treatment plans

- This trend toward more personalized and targeted CSC therapies is reshaping oncology treatment paradigms, with companies such as Fate Therapeutics pioneering induced pluripotent stem cell (iPSC)-derived therapies tailored for specific cancer profiles

- The growing focus on precision medicine and targeted cancer eradication is driving rapid adoption of personalized CSC therapies in both research and clinical applications

- Advancements in AI-driven predictive models for CSC behavior are enabling researchers to design therapies that anticipate tumor evolution, improving long-term outcomes for patients

Cancer Stem Cell Therapy Market Dynamics

Driver

Increasing Cancer Prevalence and Investment in Stem Cell Research

- The rising global incidence of cancers, coupled with growing investments in stem cell research and development, is a significant driver of the cancer stem cell therapy market

- For instance, in March 2025, Celularity, Inc. announced a multi-million-dollar funding initiative to expand clinical trials of stem cell therapies targeting solid tumors, supporting market growth

- As cancer cases continue to rise, there is heightened demand for advanced therapies capable of addressing tumor recurrence and treatment resistance, positioning CSC therapies as a crucial solution

- Furthermore, supportive government and private sector funding for stem cell research accelerates development pipelines and clinical translation of novel therapies

- Technological advancements in CSC isolation, expansion, and targeted delivery are enhancing therapeutic outcomes, driving adoption across oncology centers globally

- The increasing awareness among oncologists and patients regarding the benefits of CSC-targeted therapies further propels market expansion in both developed and emerging regions

- For instance, collaboration agreements between biotech firms and academic hospitals are facilitating faster clinical translation of CSC innovations into real-world therapies

- The rising trend of integrating CSC therapies with conventional chemotherapy and immunotherapy regimens is expanding treatment applicability and improving patient survival rates

Restraint/Challenge

Regulatory Hurdles and High Treatment Costs

- Strict regulatory requirements and the high cost of CSC therapies pose significant challenges to widespread market adoption

- For instance, delays in FDA and EMA approvals for certain clinical trials have slowed the entry of innovative CSC therapies into mainstream oncology practice

- Stem cell therapies require complex manufacturing, stringent quality control, and compliance with advanced clinical guidelines, increasing development timelines and costs

- Furthermore, patient access is limited due to the premium pricing of therapies and lack of widespread insurance coverage, restricting adoption in price-sensitive markets

- While some companies, such as Orchard Therapeutics, are working to streamline production and reduce costs, affordability remains a key barrier to scaling these therapies globally

- Overcoming these challenges through regulatory harmonization, reimbursement strategies, and cost-optimization of production will be crucial for sustained market growth

- For instance, the need for standardized protocols and faster regulatory pathways is critical to enable broader access to CSC therapies across regions

- Complexities in long-term storage and transportation of stem cells, along with maintaining their viability, also limit market scalability in emerging markets

Cancer Stem Cell Therapy Market Scope

The market is segmented on the basis of type, cancer forms, and application.

- By Type

On the basis of type, the cancer stem cell therapy market is segmented into cell culturing, cell separation, cell analysis, molecular analysis, and others. The cell culturing segment dominated the market with the largest revenue share of 35.4% in 2025, driven by its crucial role in expanding and maintaining viable stem cells for therapeutic and research purposes. Cell culturing techniques enable scientists to produce sufficient quantities of cancer stem cells (CSCs) for preclinical studies, drug screening, and clinical applications, making it a fundamental component of CSC therapy development. The segment benefits from continuous technological innovations in culture media, bioreactors, and automated systems that improve cell yield, viability, and functionality. Moreover, its established presence in research laboratories and biotech companies ensures a steady demand. Regulatory approvals and standardized protocols in cell culturing further enhance its dominance by reducing variability and supporting reproducibility across studies. The segment is widely adopted across developed regions such as North America and Europe, where advanced research infrastructure facilitates large-scale CSC cultivation.

The cell separation segment is anticipated to witness the fastest growth rate of 22.1% from 2026 to 2033, fueled by increasing demand for highly purified and targeted CSC populations. Separation technologies such as fluorescence-activated cell sorting (FACS) and magnetic-activated cell sorting (MACS) are critical for isolating CSCs from heterogeneous tumor samples, ensuring therapeutic efficacy and safety. Growth is further driven by the rising focus on personalized therapies and precision medicine, where pure cell populations are essential for developing patient-specific treatments. Continuous innovation in microfluidic and automated separation platforms is also enhancing throughput and efficiency. In addition, expansion of clinical trials targeting isolated CSCs supports rapid adoption. The segment is gaining traction in Asia-Pacific and emerging markets due to rising investments in advanced biotech facilities.

- By Cancer Forms

On the basis of cancer forms, the market is segmented into breast cancer, blood cancer, lung cancer, brain cancer, colorectal cancer, pancreatic cancer, bladder cancer, liver cancer, and other cancers. The blood cancer segment dominated the market with a share of 32.8% in 2025, primarily due to the proven clinical success of stem cell-based therapies in hematologic malignancies such as leukemia and lymphoma. Blood cancers have well-established protocols for CSC isolation, expansion, and reinfusion, making them a primary application area for CSC therapies. Extensive ongoing clinical trials, favorable regulatory guidance, and strong physician adoption support sustained market dominance. In addition, patient outcomes in blood cancer treatment improve significantly with CSC-targeted approaches, driving demand. The high prevalence of hematologic cancers in developed countries and availability of specialized treatment centers further consolidate the segment’s leading position.

The lung cancer segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing incidence rates and urgent need for innovative therapies to overcome therapy resistance. CSC-targeted therapies are showing promise in preclinical and early clinical studies for lung tumors, particularly in reducing recurrence and metastasis. Technological advances in imaging, molecular profiling, and CSC identification are accelerating development in this segment. The rising focus on combining CSC therapies with conventional treatments such as chemotherapy and immunotherapy also fuels growth. Expansion of oncology research in Asia-Pacific and emerging economies contributes to rapid market adoption in this segment.

- By Application

On the basis of application, the market is segmented into stem cell-based cancer therapy and targeted CSCs. The stem cell-based cancer therapy segment dominated the market with a share of 40.2% in 2025, driven by its proven efficacy in treating resistant tumors and minimizing relapse. Stem cell-based approaches enable regeneration of normal tissues and targeted elimination of cancer stem cells, making them a comprehensive therapeutic strategy. Clinical adoption is strong due to a growing body of research supporting improved patient outcomes, particularly in blood and solid tumors. In addition, regulatory approvals and collaborations between biotech companies and hospitals enhance accessibility and commercial adoption. The segment is well-established in North America and Europe, supported by advanced healthcare infrastructure and high R&D investment.

The targeted CSCs segment is anticipated to witness the fastest growth rate of 23.4% from 2026 to 2033, fueled by rising interest in precision oncology and therapies that specifically inhibit CSC signaling pathways. Targeted approaches improve treatment specificity and reduce side effects compared to conventional therapies. Innovations in molecular profiling, biomarker discovery, and drug delivery systems are enhancing the effectiveness of targeted CSC treatments. Increasing clinical trials, government funding, and growing partnerships between research institutions and biotech firms also support rapid adoption. The segment is gaining traction globally as personalized medicine becomes a central focus in cancer treatment.

Cancer Stem Cell Therapy Market Regional Analysis

- North America dominated the cancer stem cell therapy market with the largest revenue share of 38.7% in 2025, driven by advanced healthcare infrastructure, significant R&D investment, early adoption of novel therapies, and the strong presence of key market players in the U.S., supported by favorable regulatory frameworks that accelerate clinical translation

- Patients and clinicians in the region prioritize personalized and targeted treatment options, supported by the availability of cutting-edge research centers, specialized hospitals, and experienced oncology professionals

- This widespread adoption is further reinforced by favorable regulatory frameworks, high healthcare expenditure, and the strong presence of key market players, establishing North America as the leading hub for both clinical applications and research of cancer stem cell therapies

U.S. Cancer Stem Cell Therapy Market Insight

The U.S. cancer stem cell therapy market captured the largest revenue share of 82% in 2025 within North America, fueled by advanced healthcare infrastructure and early adoption of innovative CSC therapies. Patients and clinicians are increasingly prioritizing personalized and targeted treatments that improve outcomes and reduce recurrence. The growing investment in R&D, coupled with the presence of leading biotech companies and clinical trial centers, further propels market growth. Moreover, regulatory support from the FDA for expedited CSC therapy approvals is significantly contributing to the market’s expansion. High patient awareness and adoption of novel therapeutic approaches are also driving widespread acceptance across oncology centers.

Europe Cancer Stem Cell Therapy Market Insight

The Europe cancer stem cell therapy market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising cancer prevalence and government initiatives supporting advanced therapies. Increasing healthcare expenditure, urbanization, and a focus on precision medicine are fostering adoption of CSC therapies. European oncology centers are integrating CSC-targeted approaches into both standard and experimental treatments. Patients and physicians are drawn to the potential for reduced tumor recurrence and improved survival rates. Strong collaborations between academic institutions and biotech firms further support clinical research and commercialization of CSC therapies.

U.K. Cancer Stem Cell Therapy Market Insight

The U.K. cancer stem cell therapy market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for advanced cancer treatments and personalized medicine. Rising awareness among patients and oncologists regarding CSC-targeted therapies encourages adoption in hospitals and research centers. In addition, government funding for cancer research and supportive reimbursement policies are stimulating growth. The U.K.’s robust healthcare infrastructure, combined with a growing number of clinical trials, is expected to continue driving market expansion. The integration of CSC therapies with conventional chemotherapy and immunotherapy regimens also enhances treatment efficacy and uptake.

Germany Cancer Stem Cell Therapy Market Insight

The Germany cancer stem cell therapy market is expected to expand at a considerable CAGR during the forecast period, fueled by high investment in biotech innovation and increasing adoption of precision oncology. German hospitals and research centers are emphasizing advanced CSC therapies to reduce cancer recurrence and improve patient outcomes. Collaboration between local biotech companies and academic institutions is promoting clinical translation of novel therapies. Furthermore, awareness of innovative cancer treatments and a strong regulatory framework supporting safe clinical trials are driving adoption. Germany’s focus on technologically advanced and sustainable healthcare solutions further supports market growth.

Asia-Pacific Cancer Stem Cell Therapy Market Insight

The Asia-Pacific cancer stem cell therapy market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by increasing cancer incidence, rising healthcare expenditure, and expanding research infrastructure in countries such as China, Japan, and India. Growing awareness of CSC therapies among clinicians and patients is driving adoption across both residential and commercial healthcare settings. Government initiatives promoting biotechnology and personalized medicine further boost market growth. The region’s emergence as a hub for clinical trials and stem cell research enhances accessibility and affordability of therapies. Rapid urbanization and technological adoption in healthcare are also contributing to the region’s strong market expansion.

Japan Cancer Stem Cell Therapy Market Insight

The Japan cancer stem cell therapy market is gaining momentum due to the country’s advanced healthcare system, high R&D investment, and focus on personalized medicine. Rising cancer prevalence and increasing number of clinical trials targeting CSCs are fueling adoption. Integration of CSC therapies with conventional treatments and advanced diagnostics improves patient outcomes and reduces recurrence. Japan’s aging population and emphasis on minimally invasive and targeted therapies further drive demand. In addition, supportive regulatory frameworks and government funding for oncology research are facilitating faster commercialization of CSC therapies.

India Cancer Stem Cell Therapy Market Insight

The India cancer stem cell therapy market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing cancer incidence, expanding healthcare infrastructure, and growing awareness among patients and physicians. India is emerging as a significant hub for clinical research and biotechnology innovation, with several domestic companies developing CSC-targeted therapies. Government initiatives promoting cancer care and personalized medicine, alongside affordable therapy options, are propelling market growth. Rapid urbanization, rising disposable income, and access to international collaborations further support adoption across hospitals and research centers.

Cancer Stem Cell Therapy Market Share

The Cancer Stem Cell Therapy industry is primarily led by well-established companies, including:

- Fate Therapeutics, Inc. (U.S.)

- Autolus Therapeutics (U.S.)

- Lineage Cell Therapeutics, Inc. (U.S.)

- BioNTech SE (Germany)

- Gilead Sciences, Inc. (U.S.)

- Adaptimmune Therapeutics PLC (U.K.)

- BeOne Medicines (U.S.)

- AbbVie Inc. (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- Miltenyi Biotec (Germany)

- STEMCELL Technologies Inc. (Canada)

- PromoCell GmbH (Germany)

- Lonza Group AG (Switzerland)

- MacroGenics, Inc. (U.S.)

- OncoMed Pharmaceuticals, Inc. (U.S.)

- FUJIFILM Irvine Scientific (U.S.)

- Sino Biological, Inc. (China)

- Bionomics Ltd (Australia)

- MacroGenics, Inc. (U.S.)

- Imugene Ltd (Australia)

What are the Recent Developments in Global Cancer Stem Cell Therapy Market?

- In August 2025, a small early‑stage Stanford Medicine trial reported that an experimental antibody drug (briquilimab) enabled children needing stem cell transplants to avoid toxic chemotherapy/radiation pre‑conditioning, improving integration of donor cells a potential advance in transplant safety

- In August 2025, the EU authorized dorocubicel (allogeneic umbilical cord‑derived CD34‑ cells, enhanced with UM171) for hematopoietic stem cell transplant use, expanding the global regulatory footprint for next‑generation stem cell therapies in cancer care

- In July 2025, UCLA researchers reported a first‑in‑human clinical trial demonstrating that reprogramming a patient’s blood‑forming stem cells can produce a renewable supply of cancer‑fighting T cells, offering a novel internal immunotherapy platform to combat resistant cancers

- In May 2025, a groundbreaking randomized controlled trial showed that CAR‑T cell immunotherapy helped advanced solid tumour patients live ~40% longer than standard care, marking one of the first successful Car‑T results for solid cancers and signaling potential expansion beyond blood cancers

- In April 2023, the U.S. FDA approved Omisirge (omidubicel‑onlv), a novel allogeneic cord blood‑derived cell therapy, to improve neutrophil recovery and reduce infection risks in adults and pediatric patients with blood cancers undergoing cord blood stem cell transplantation. This represents a key milestone for stem cell‑based cancer therapy availability in the U.S.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.