Global Cancer Vaccine Platforms Market

Market Size in USD Billion

USD

3.46 Billion

USD

10.59 Billion

2024

2032

USD

3.46 Billion

USD

10.59 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.46 Billion | |

| USD 10.59 Billion | |

| % | |

|

Cancer Vaccine Platforms Market Size

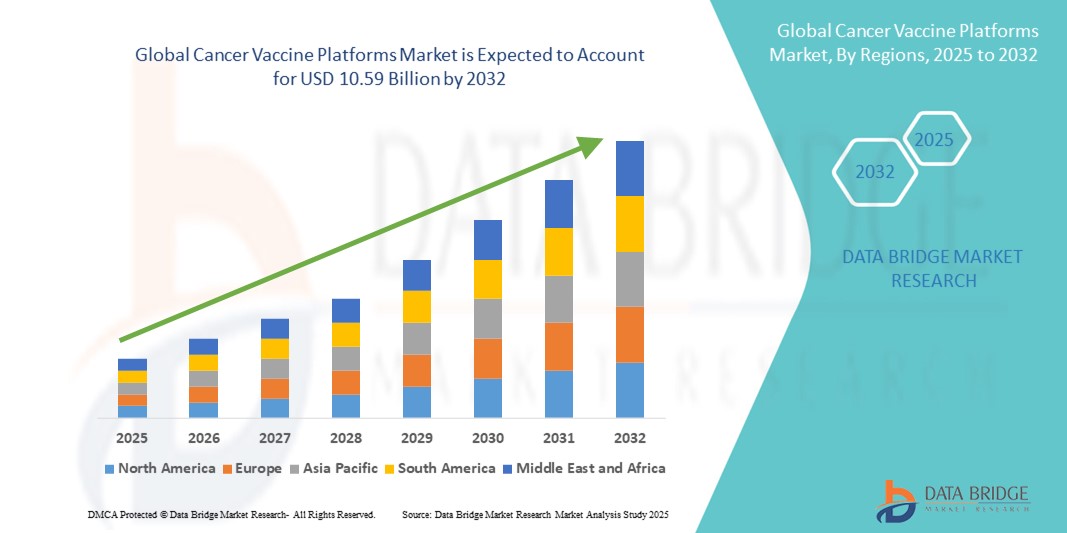

- The global cancer vaccine platforms market size was valued at USD 3.46 billion in 2024 and is expected to reach USD 10.59 billion by 2032, at a CAGR of 15.00% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress in biotechnology and immunotherapy, which are driving the development and deployment of novel cancer vaccine platforms across various oncology applications. This has led to increased digitalization and precision in cancer care delivery, especially in developed healthcare settings

- Furthermore, rising demand for targeted, personalized, and immune-boosting therapies among patients and oncologists is positioning cancer vaccine platforms as a critical component in the modern oncology treatment ecosystem. These converging factors are accelerating the uptake of cancer vaccine platform solutions, thereby significantly boosting the industry's growth

Cancer Vaccine Platforms Market Analysis

- Cancer vaccine platforms, which provide targeted immunological strategies to prevent or treat cancer, are becoming increasingly essential in modern oncology due to their potential to stimulate the body’s immune system to recognize and combat tumor cells, offering a safer and more effective alternative to traditional therapies

- The rising demand for cancer vaccine platforms is primarily driven by the growing global cancer burden, increased investments in immuno-oncology research, rising demand for personalized medicine, and technological advancements in mRNA and dendritic cell-based vaccine development

- North America dominated the global cancer vaccine platforms market with the largest revenue share of 31.17% in 2024, attributed to a well-established biopharmaceutical ecosystem, high healthcare expenditure, and robust R&D activities. The U.S. is a major contributor to regional dominance, supported by strong government funding, early adoption of mRNA-based cancer vaccines, and presence of key players such as Moderna, BioNTech, and Gritstone Bio

- Asia-Pacific is projected to witness the fastest growth in the global cancer vaccine platforms market during the forecast period, owing to rising cancer incidence, increasing healthcare infrastructure development, growing awareness of immunotherapies, and expanding biotechnology investments in countries such as China, Japan, India, and South Korea

- The Injectable route dominated the global cancer vaccine platforms market with a substantial revenue share of 74.2% in 2024. Injectable vaccines remain the standard due to their established delivery infrastructure, high bioavailability, and proven efficacy in eliciting potent immune responses

Report Scope and Cancer Vaccine Platforms Market Segmentation

|

Attributes |

Cancer Vaccine Platforms Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cancer Vaccine Platforms Market Trends

Enhanced Convenience Through Platform Advancements in Cancer Vaccines

- A significant and accelerating trend in the global cancer vaccine platforms market is the increasing sophistication and personalization of vaccine delivery mechanisms, enabled by advances in platform technologies such as mRNA, recombinant proteins, dendritic cell-based vaccines, and viral vectors

- These platforms are improving convenience, efficacy, and response rates in both prophylactic and therapeutic cancer vaccines, by enabling customized antigen targeting, faster development timelines, and enhanced immune system activation against cancer-specific antigens

- For instance, mRNA cancer vaccine platforms offer greater flexibility and rapid adaptability, allowing for near real-time development of personalized cancer vaccines tailored to the patient's tumor mutational landscape. This approach significantly reduces the time between biopsy and vaccine administration, enhancing clinical efficiency

- Recombinant vector-based vaccines, such as those utilizing adenovirus or modified vaccinia Ankara (MVA), are gaining popularity for their ability to present tumor antigens effectively and induce robust T-cell responses. These platforms are being optimized to improve immune memory and reduce toxicity

- Dendritic cell (DC) vaccine platforms are also gaining traction, particularly in personalized medicine, as they allow direct antigen presentation to T-cells, leading to improved immune response in hard-to-treat cancers like glioblastoma and melanoma

- The integration of next-generation sequencing (NGS) and bioinformatics algorithms into these platforms enables faster identification of tumor neoantigens, improving patient selection and vaccine matching. This is particularly evident in companies developing neoantigen-based personalized cancer vaccines

- The growing demand for platforms that support combination therapies—such as checkpoint inhibitors and adoptive cell transfer—is further reshaping the landscape. Cancer vaccine platforms that can be co-administered or designed to synergize with immunotherapies are expected to dominate future pipelines

- Companies such as Moderna, BioNTech, and Gritstone Bio are leading innovations in this domain by building modular and scalable platforms that not only enhance vaccine efficacy but also streamline clinical development and regulatory approval pathways

- These advancements are transforming the Cancer Vaccine Platforms Market by prioritizing speed, specificity, patient adaptability, and multi-cancer versatility, all of which are critical as oncology care increasingly shifts toward personalized, immune-targeted interventions

Cancer Vaccine Platforms Market Dynamics

Driver

Growing Need Due to Rising Cancer Incidence and Unmet Therapeutic Demands

- The increasing global burden of cancer and the rising demand for targeted, less invasive treatments are significantly driving the need for innovative cancer vaccine platforms. These platforms are being developed to induce or enhance the body’s immune response to tumor-associated antigens, offering a promising alternative or complement to conventional therapies such as chemotherapy and radiation

- For instance, in April 2024, BioNTech SE announced advancements in its mRNA-based personalized cancer vaccine platform in collaboration with Genentech (a member of the Roche Group), entering Phase II trials for multiple solid tumors, which is expected to significantly boost the Cancer Vaccine Platforms Market

- As patients and oncologists seek more effective and less toxic cancer therapies, cancer vaccines offer a tailored immunological approach that could lead to prolonged survival with fewer side effects

- Furthermore, increasing research funding, public-private partnerships, and the success of mRNA technology during the COVID-19 pandemic have sparked renewed interest and investment in cancer vaccine development, accelerating clinical pipelines globally

- The potential for cancer vaccines to be used as both therapeutic and preventive tools is driving adoption across multiple cancer types, including melanoma, non-small cell lung cancer (NSCLC), and prostate cancer. Recent developments in peptide-based, viral vector-based, and dendritic cell-based platforms further add to the diversity of promising options

- As pharmaceutical companies focus on developing scalable, customizable cancer vaccine solutions, their application across both monotherapy and combination treatment regimens is expected to expand, supporting growth across both developed and emerging markets

Restraint/Challenge

Concerns Regarding Clinical Efficacy, Delivery Complexities, and High Development Costs

- Despite the enthusiasm surrounding cancer vaccine platforms, several key challenges persist that could hinder broader market adoption. Notably, concerns remain regarding the clinical efficacy of certain vaccine candidates in large, late-stage trials, as the immune system’s ability to recognize and destroy cancer cells varies significantly across individuals and tumor types

- For instance, several peptide-based cancer vaccines have shown limited therapeutic benefit in clinical trials due to tumor immune evasion mechanisms and poor immunogenicity. This has led to increased emphasis on personalized vaccine strategies and neoantigen identification, which in turn increases R&D complexity and costs

- The development of cancer vaccines often requires sophisticated delivery mechanisms, such as lipid nanoparticles or dendritic cell manipulation, which adds to the logistical and manufacturing challenges, especially in resource-limited settings

- In addition, the overall cost of personalized cancer vaccines remains high, particularly for mRNA-based platforms that require individualized sequencing, synthesis, and formulation. This limits accessibility in low- and middle-income countries and may slow market penetration in cost-sensitive healthcare systems

- Moreover, regulatory uncertainty surrounding combination therapies involving cancer vaccines, immuno-oncology drugs, and checkpoint inhibitors adds further hurdles to approval timelines and reimbursement strategies

- Overcoming these barriers through sustained investment in R&D, improving delivery technologies, expanding regulatory clarity, and ensuring cost-effective manufacturing will be critical to ensuring long-term growth of the Cancer Vaccine Platforms Market

Cancer Vaccine Platforms Market Scope

The market is segmented on the basis of type, technology, route of administration, cancer type, and end user.

- By Type

On the basis of type, the cancer vaccine platforms market is segmented into preventive cancer vaccines, therapeutic cancer vaccines, personalized cancer vaccines, and others. The therapeutic cancer vaccines segment dominated the market with the largest revenue share of 47.5% in 2024, primarily due to their rising use in treating advanced or metastatic cancers. These vaccines stimulate the body’s immune system to target and destroy cancer cells. Growing R&D investments, especially in combination therapies with checkpoint inhibitors, are boosting adoption in clinical and commercial settings.

The personalized cancer vaccines segment is anticipated to witness the fastest CAGR of 21.3% from 2025 to 2032, driven by increased focus on individualized treatment based on genetic profiles, supported by advancements in genomics and next-generation sequencing technologies.

- By Technology

On the basis of cancer vaccine platforms market is segmented based into various vaccine technologies, including DNA-based Vaccines, mRNA-based Vaccines, dendritic cell vaccines, viral vector vaccines, tumor cell vaccines, protein/peptide-based vaccines, and others. Among these, mRNA-based Vaccines accounted for the largest market share of 36.9% in 2024. This significant share is largely attributed to the groundbreaking success of mRNA technology during the COVID-19 pandemic, which accelerated its adoption in the oncology field. The ability of mRNA vaccines to be rapidly designed, their scalability for mass production, and their capacity to elicit strong and specific immune responses have positioned them as a leading platform in cancer vaccine development pipelines globally.

In contrast, the Dendritic Cell Vaccines segment is forecasted to exhibit the fastest CAGR of 19.6% from 2025 to 2032. This growth is driven by the distinct mechanism of dendritic cell vaccines, which effectively present cancer antigens to T-cells, thereby enhancing the body’s immune surveillance. Encouraging clinical trial outcomes in challenging cancers such as glioblastoma, prostate cancer, and melanoma have further fueled interest and investment in dendritic cell vaccine technology.

- By Route of Administration

On the basis of cancer vaccine platforms market is segmented based into the route through which cancer vaccines are administered, segmented into injectable, oral, and intranasal vaccines. The Injectable route dominated the market with a substantial revenue share of 74.2% in 2024. Injectable vaccines remain the standard due to their established delivery infrastructure, high bioavailability, and proven efficacy in eliciting potent immune responses. Their widespread clinical acceptance and regulatory approvals make them the preferred method for administering most cancer vaccines.

Oral vaccines are expected to witness the fastest growth, with a projected CAGR of 18.4% from 2025 to 2032. This growth is attributed to ongoing research focusing on mucosal immunity and a growing patient preference for non-invasive administration options that enhance compliance and comfort. Despite their promising outlook, oral vaccines face challenges related to ensuring stability of the active components and effective absorption through the gastrointestinal tract, which are active areas of research and development.

- By Cancer Type

On the basis of cancer vaccine platforms market is segmented into various cancer types, including lung cancer, prostate cancer, breast cancer, cervical cancer, melanoma, colorectal cancer, and others. Among these, lung cancer held the largest market share of 24.7% in 2024. This dominance is largely due to the high global incidence and mortality rates associated with lung cancer, alongside a robust pipeline of immunotherapeutic vaccine candidates specifically designed to target lung cancer antigens such as MAGE-A3 and NY-ESO-1. The extensive research focus and urgent clinical need have propelled significant advancements in vaccine development for this indication.

Melanoma is anticipated to witness the fastest growth, with a CAGR of 20.9% projected from 2025 to 2032. This rapid growth can be attributed to melanoma’s highly immunogenic characteristics, which make it particularly responsive to vaccine-based immunotherapies. Numerous personalized vaccine trials targeting melanoma have reported promising clinical outcomes, fueling optimism for this segment’s expansion. The growing awareness about melanoma’s immunotherapy potential and its rising incidence in several regions further contribute to the segment’s strong growth trajectory.

- By End User

On the basis of cancer vaccine platforms market is segmented into Hospitals, cancer research institutes, specialty clinics, and others. Hospitals accounted for the largest market share of 52.8% in 2024. This can be attributed to hospitals serving as the primary healthcare facilities where cancer vaccines are administered, and where comprehensive patient management—including diagnosis, treatment, and follow-up—is conducted. Hospitals also play a critical role in managing complex oncology cases and are frequently involved in clinical trials, which further drives demand for advanced cancer vaccine platforms.

Cancer research institutes are expected to record the fastest CAGR of 17.2% between 2025 and 2032. These institutes are instrumental in driving translational research and early-stage clinical development of novel cancer vaccines. Supported by increasing public-private partnerships, funding initiatives, and academic collaborations, cancer research institutes continue to expand their role in innovating and validating next-generation vaccine technologies. Their pivotal function in bridging laboratory discoveries with clinical application ensures their significant contribution to market growth in the coming years.

Cancer Vaccine Platforms Market Regional Analysis

- North America dominated the cancer vaccine platforms market with the largest revenue share of 31.17% in 2024, driven by the growing demand for precision oncology, favorable government initiatives supporting cancer immunotherapies, and increased investments in cancer vaccine R&D

- The regional growth is underpinned by a strong biotechnology infrastructure, increasing cancer incidence, and expanding clinical trials landscape, particularly in the U.S.

- In addition, strategic collaborations between pharmaceutical companies and research institutions are accelerating the development and commercialization of novel cancer vaccine platforms in North America

U.S. Cancer Vaccine Platforms Market Insight

The U.S. cancer vaccine platforms market captured the largest revenue share of 86% in 2024 within North America, propelled by the robust oncology research ecosystem, early adoption of mRNA-based and DNA-based vaccine platforms, and FDA support for breakthrough therapies. The country's growing investment in personalized medicine and preventive oncology has significantly increased the demand for therapeutic cancer vaccines, particularly in melanoma, lung, and prostate cancers. Furthermore, public and private funding for next-generation vaccine technologies — including neoantigen-based and dendritic cell vaccines — is contributing to the rapid commercialization of cancer vaccine platforms.

Europe Cancer Vaccine Platforms Market Insight

The Europe cancer vaccine platforms market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing prevalence of cancer, strategic policy frameworks (such as Europe's Beating Cancer Plan), and rising investments in immunotherapy innovation. Countries like Germany, France, and the U.K. are leading the charge in clinical trials, with biotech firms focused on personalized and tumor-specific vaccines. Moreover, the rising demand for off-the-shelf cancer vaccines and early detection programs are expected to accelerate adoption across European oncology centers.

U.K. Cancer Vaccine Platforms Market Insight

The U.K. cancer vaccine platforms market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by government-backed research programs such as Cancer Research UK's Grand Challenge. Innovations in RNA-based therapeutics and increasing focus on preventative vaccines, especially for virus-induced cancers (e.g., HPV-related cervical cancer), are key market drivers. In addition, the National Health Service (NHS) is working toward integrating personalized cancer vaccines into mainstream treatment pathways, providing a scalable platform for market expansion.

Germany Cancer Vaccine Platforms Market Insight

The Germany cancer vaccine platforms market is expected to expand at a considerable CAGR over the forecast period, driven by advancements in precision immunotherapy, digital health integration, and increasing demand for cancer treatment personalization. Strong clinical research infrastructure and supportive regulatory processes make Germany a central hub for cancer vaccine trials. Biotech startups and major pharma companies alike are exploring individualized vaccine solutions for breast, colorectal, and pancreatic cancers, fostering strong industry growth.

Asia-Pacific Cancer Vaccine Platforms Market Insight

The Asia-Pacific cancer vaccine platforms market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, owing to a rising cancer burden, expanding healthcare access, and growing government funding for biotech innovation. Countries such as China, Japan, and India are rapidly adopting therapeutic and preventive vaccine technologies, with increasing participation in global oncology clinical trials. The region is also witnessing growing partnerships between academic institutions and pharmaceutical companies to drive localized cancer vaccine development.

Japan Cancer Vaccine Platforms Market Insight

The Japan cancer vaccine platforms market is gaining momentum due to the country’s focus on advanced therapeutics, aging population, and strong emphasis on cancer prevention. With government support and streamlined regulatory approval processes, Japanese firms are investing in tumor antigen discovery and personalized vaccine development. The adoption of combination therapies (vaccines with checkpoint inhibitors) is also gaining traction in Japan’s clinical oncology space.

China Cancer Vaccine Platforms Market Insight

The China cancer vaccine platforms market accounted for the largest market revenue share in Asia-Pacific in 2024, supported by a rapidly expanding biotech ecosystem, large patient pool, and substantial government investment in oncology. China's biotech firms are focusing on mRNA, peptide, and neoantigen-based cancer vaccines, with several in late-stage clinical trials. National initiatives like “Made in China 2025” and strong domestic manufacturing capabilities are bolstering innovation and accessibility of cancer vaccine technologies.

Cancer Vaccine Platforms Market Share

The Cancer Vaccine Platforms industry is primarily led by well-established companies, including:

- Moderna, Inc. (U.S.)

- BioNTech SE (Germany)

- Genocea Biosciences, Inc. (U.S.)

- GSK plc (U.K.)

- Amgen Inc. (U.S.)

- Agenus Inc. (U.S.)

- ISA Pharmaceuticals B.V. (Netherlands)

- Vaccitech plc (U.K.)

- Transgene SA (France)

- Inovio Pharmaceuticals, Inc. (U.S.)

Latest Developments in Global Cancer Vaccine Platforms Market

- In April 2023, BioNTech SE announced plans to begin construction of a state-of-the-art mRNA vaccine manufacturing facility in Kigali, Rwanda. This site is part of BioNTech’s long-term strategy to enhance localized production and access to mRNA-based cancer vaccines in Africa. The modular factory, known as “BioNTainers,” will help tackle both infectious diseases and cancer, showcasing the company's commitment to equitable global healthcare and innovation

- In March 2023, Moderna Inc. reported promising data from its Phase IIb trial of the mRNA-4157/V940 personalized cancer vaccine in combination with Keytruda for melanoma patients. The study demonstrated a 44% reduction in recurrence or death compared to Keytruda alone, highlighting the strong potential of mRNA-based platforms in treating cancer. This breakthrough underscores Moderna’s expanding role beyond COVID-19 and into the oncology vaccine market

- In February 2023, Gritstone Bio, Inc. received a USD 20.6 million grant from the Bill & Melinda Gates Foundation to support the development of its self-amplifying mRNA (samRNA) vaccine platform, which includes oncology applications. The funding accelerates Gritstone’s efforts in applying the samRNA platform for personalized cancer immunotherapy, signaling confidence in the technology’s scalability and impact

- In January 2023, CureVac N.V. entered a research collaboration with the University of Texas MD Anderson Cancer Center to develop cancer vaccine candidates using CureVac’s proprietary mRNA technology. The partnership will focus on leveraging CureVac’s vaccine delivery systems and MD Anderson’s cancer biology expertise, aiming to develop next-generation vaccines for hard-to-treat cancers

- In December 2022, Vaccibody AS (now Nykode Therapeutics) shared new clinical data from its Phase I/IIa trial of VB10.NEO, a neoantigen cancer vaccine candidate. The results showed robust CD8+ T-cell responses and tumor regression in some patients with advanced solid tumors. These findings reinforce the clinical potential of personalized neoantigen vaccines in oncology immunotherapy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.