Global Cardiac Computed Tomography Cct Market

Market Size in USD Billion

USD

8.38 Billion

USD

14.69 Billion

2024

2032

USD

8.38 Billion

USD

14.69 Billion

2024

2032

| 2025 - 2032 | |

| USD 8.38 Billion | |

| USD 14.69 Billion | |

| % | |

|

Cardiac Computed Tomography (CCT) Market Size

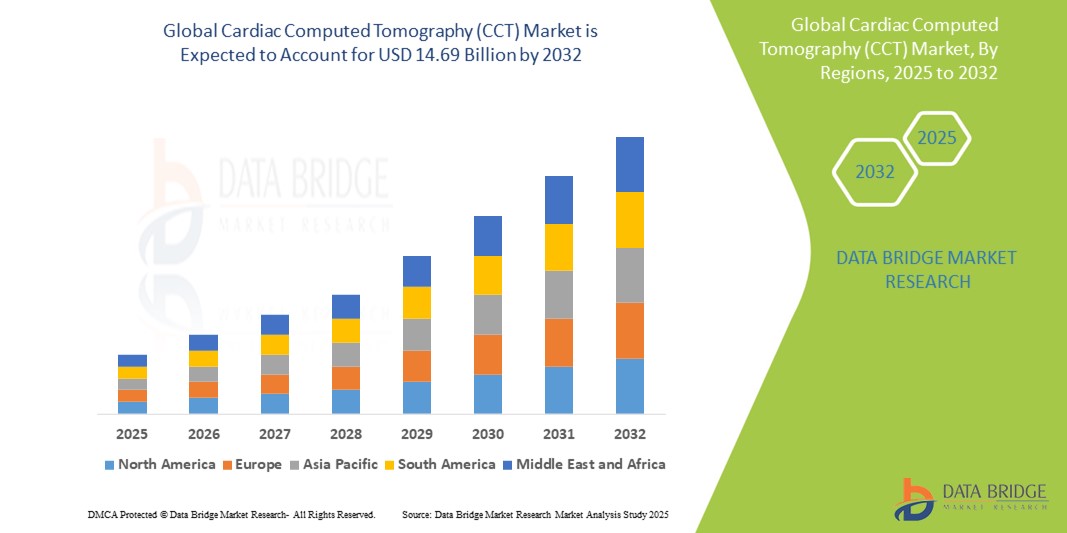

- The global cardiac computed tomography (CCT) market size was valued at USD 8.38 billion in 2024 and is expected to reach USD 14.69 billion by 2032, at a CAGR of 7.26% during the forecast period

- The market growth is primarily driven by the rising prevalence of cardiovascular diseases (CVDs) and the increasing demand for non-invasive diagnostic tools, which has led to the broader adoption of advanced cardiac imaging technologies such as CCT

- In addition, technological advancements such as faster scanning speeds, enhanced image quality, and integration with AI-based diagnostic platforms are contributing to increased diagnostic accuracy and workflow efficiency. These trends are positioning CCT as a critical tool in modern cardiology, significantly propelling market expansion

Cardiac Computed Tomography (CCT) Market Analysis

- Cardiac computed tomography (CCT), a non-invasive imaging technique that visualizes coronary arteries and cardiac structures, is becoming an essential diagnostic modality in cardiology due to its rapid scan times, high-resolution imaging, and ability to detect coronary artery disease at early stages

- The increasing prevalence of cardiovascular disorders, demand for early and accurate diagnosis, and preference for less invasive procedures are key drivers fueling the demand for CCT across hospitals and diagnostic centers

- North America dominated the cardiac computed tomography (CCT) market with the largest revenue share of 40.1% in 2024, characterized by high adoption of cutting-edge diagnostic technologies, and increasing awareness of preventive cardiac care, especially in the U.S., where cardiac CT is routinely used for risk stratification and pre-surgical planning

- Asia-Pacific is expected to be the fastest growing region in the cardiac computed tomography (CCT) market during the forecast period due to expanding healthcare access, rising incidence of heart disease, and government investments in diagnostic imaging infrastructure

- Coronary CT Angiography segment dominated the cardiac computed tomography (CCT) market with a market share of 45.6% in 2024, driven by its growing use as a frontline test for evaluating coronary artery disease, offering a safer and quicker alternative to invasive angiography

Report Scope and Cardiac Computed Tomography (CCT) Market Segmentation

|

Attributes |

Cardiac Computed Tomography (CCT) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cardiac Computed Tomography (CCT) Market Trends

“Technological Advancements Driving Precision and Accessibility”

- A major and evolving trend in the global cardiac computed tomography (CCT) market is the continuous advancement in imaging technology, including improvements in spatial resolution, reduced scan times, and lower radiation exposure enhancing diagnostic accuracy while improving patient safety and comfort

- For instance, next-generation CCT systems from companies such as GE HealthCare and Siemens Healthineers feature dual-source and spectral CT capabilities, enabling clearer visualization of coronary arteries, even in patients with high heart rates or heavy calcification

- AI integration in CCT is transforming cardiac imaging by enabling automated segmentation, enhanced image reconstruction, and intelligent detection of coronary artery disease. For example, Canon Medical’s AI-assisted CCT tools improve workflow efficiency and offer high-precision measurements for risk assessment and treatment planning

- The adoption of CCT as a frontline diagnostic tool is expanding in response to the growing emphasis on early detection and preventive cardiology, particularly for asymptomatic individuals at moderate risk of coronary artery disease. Initiatives promoting cardiac CT calcium scoring are becoming common in routine health evaluations across advanced healthcare systems

- The integration of CCT with other imaging modalities, such as PET or SPECT, is creating hybrid imaging solutions that combine anatomical and functional cardiac data in a single session, enhancing the accuracy of diagnosis and treatment strategy formulation

- This trend towards more precise, intelligent, and accessible cardiac imaging is fundamentally reshaping clinical expectations in cardiology. Consequently, companies are increasingly developing advanced CCT platforms with AI-powered analytics, low-dose protocols, and faster scanning capabilities to meet the rising demand from hospitals, imaging centers, and specialized cardiac facilities

Cardiac Computed Tomography (CCT) Market Dynamics

Driver

“Rising Cardiovascular Disease Burden and Demand for Non-Invasive Diagnostics”

- The increasing global burden of cardiovascular diseases (CVDs), along with the rising demand for accurate and non-invasive diagnostic tools, is a significant driver accelerating the adoption of cardiac computed tomography (CCT) systems

- For instance, in February 2024, Siemens Healthineers launched its new photon-counting CT platform, NAEOTOM Alpha, which enhances cardiac imaging capabilities by delivering ultra-high resolution and lower radiation doses. Such innovations are expected to drive CCT adoption during the forecast period

- As heart disease remains the leading cause of death worldwide, healthcare providers are seeking advanced imaging solutions that can detect coronary artery disease early and guide preventive care strategies. CCT offers detailed visualization of coronary anatomy, enabling clinicians to assess plaque burden and stenosis without invasive procedures

- Furthermore, the shift towards value-based healthcare models and preventive cardiology is reinforcing the need for efficient, patient-friendly diagnostic solutions. CCT addresses this need by offering rapid scan times, high diagnostic accuracy, and minimal patient discomfort

- The increasing integration of CCT with AI-powered platforms for automated analysis and risk stratification, along with the growing use of coronary CT angiography (CCTA) in routine cardiac evaluations, is significantly boosting the uptake of CCT in hospitals, cardiac centers, and outpatient diagnostic facilities worldwide

Restraint/Challenge

“High Cost and Radiation Exposure Concerns”

- Despite its diagnostic advantages, the high cost associated with cardiac computed tomography (CCT) systems and procedures presents a notable restraint to broader market adoption, particularly in low- and middle-income countries. The upfront investment in advanced CT equipment, along with the operational costs of maintenance and skilled personnel, can limit accessibility in resource-constrained healthcare settings

- For instance, premium systems with dual-source or spectral CT capabilities can cost significantly more than conventional scanners, making them less feasible for small hospitals or standalone diagnostic centers

- In addition, concerns about radiation exposure, although mitigated with modern low-dose technologies, remain a point of caution for some clinicians and patients. While CCT offers valuable non-invasive imaging, the cumulative radiation dose in repeat scans—especially in younger patients continues to raise clinical and ethical considerations

- Moreover, reimbursement policies for CCT procedures vary across regions and may not adequately cover advanced imaging, impacting both provider adoption and patient affordability. This disparity in insurance support can limit access to CCT in regions with underdeveloped healthcare reimbursement infrastructures

- Addressing these challenges through the development of cost-effective imaging solutions, enhanced dose reduction techniques, and wider education on the risk-benefit ratio of CCT will be crucial for expanding adoption and ensuring equitable access across global healthcare markets

Cardiac Computed Tomography (CCT) Market Scope

The market is segmented on the basis of offerings, product type, application, end user, and distribution channel.

- By Offerings

On the basis of offerings, the cardiac computed tomography (CCT) market is segmented into system, service, and software. The system segment dominated the market with the largest revenue share in 2024, attributed to the increasing demand for high-performance CT scanners that deliver rapid, high-resolution cardiac imaging. The adoption of advanced systems—such as dual-source and spectral CT—continues to rise in hospitals and cardiac centers to support early diagnosis and preventive cardiology.

The software segment is expected to witness the fastest growth from 2025 to 2032, driven by the rising integration of AI-powered tools for image reconstruction, coronary artery segmentation, and automated diagnostic assistance. Software solutions are increasingly favored for their role in streamlining workflows and improving clinical decision-making accuracy.

- By Product Type

On the basis of product type, the cardiac computed tomography (CCT) market is categorized into single source CT, dual source cardiac CT, and spectral CT. The single source CT segment held the largest market share in 2024 due to its widespread availability, cost-effectiveness, and adequacy for routine cardiac evaluations and calcium scoring.

The dual source cardiac CT segment is anticipated to grow at the fastest CAGR during the forecast period, driven by its superior temporal resolution and capability to capture high-quality images even at high heart rates without beta-blockers. Dual source CT is becoming increasingly preferred for advanced coronary CT angiography (CCTA) procedures.

- By Application

On the basis of application, the cardiac computed tomography (CCT) cardiac CT market is segmented into calcium scoring, coronary CT angiography, device implantation, pulmonary vein isolation, and left atrial appendage occlusion. The coronary CT angiography segment dominated the market with a share of 45.6% in 2024 owing to its critical role in the non-invasive evaluation of coronary artery disease (CAD) and increasing adoption in frontline cardiac diagnostics. The ability of CCTA to deliver detailed coronary anatomy assessments with high sensitivity is enhancing its use in both inpatient and outpatient settings.

The calcium scoring segment is projected to witness notable growth during forecast period, as healthcare systems increasingly adopt preventive cardiology approaches. Routine calcium scoring for asymptomatic individuals helps in early identification of cardiovascular risks and improves long-term outcomes.

- By End User

On the basis of end user, the cardiac computed tomography (CCT) market is segmented into hospitals, specialty centers, diagnostic & imaging centers, and others. The hospital segment accounted for the largest share in 2024, supported by large-scale investments in advanced imaging infrastructure and the integration of cardiac CT into multi-specialty care pathways. Hospitals benefit from high patient volumes, insurance coverage, and the ability to deliver comprehensive cardiac care.

The diagnostic & imaging centers segment is projected to grow rapidly from 2025 to 2032 due to the increasing trend toward decentralized healthcare, cost-efficiency, and shorter patient turnaround times. These centers are leveraging compact and high-speed CT units to meet the demand for specialized cardiac imaging.

- By Distribution Channel

On the basis of distribution channel, the cardiac computed tomography (CCT) market is segmented into direct tender and third-party distributor. The direct tender segment held the dominant share in 2024, particularly driven by large-scale purchases from government hospitals, academic institutions, and corporate healthcare chains seeking to modernize diagnostic capabilities through centralized procurement.

The third-party distributor segment is expected to register substantial growth during forecast period, owing to expanding access to advanced imaging systems across emerging markets, where local distributors play a key role in equipment sales, maintenance, and service delivery.

Cardiac Computed Tomography (CCT) Market Regional Analysis

- North America dominated the cardiac computed tomography (CCT) market with the largest revenue share of 40.1% in 2024, driven by high adoption of cutting-edge diagnostic technologies, and increasing awareness of preventive cardiac care

- The region's leadership is further bolstered by the presence of major medical imaging companies, rising clinical awareness about the benefits of early cardiac imaging, and the growing integration of CCT into standard diagnostic protocols for coronary artery disease

- In addition, North America's robust investment in healthcare technology, ongoing research in cardiovascular diagnostics, and the adoption of AI-powered imaging solutions contribute significantly to regional market growth, reinforcing its status as a leading hub for CCT adoption across hospitals, diagnostic centers, and cardiac specialty clinics

U.S. Cardiac Computed Tomography (CCT) Market Insight

The U.S. cardiac computed tomography (CCT) market captured the largest revenue share within North America in 2024, driven by the country's advanced healthcare infrastructure and high adoption of non-invasive imaging technologies. The rising prevalence of cardiovascular diseases and a strong focus on preventive cardiology are propelling demand for CCT systems. The U.S. is also witnessing increased integration of AI and image analysis software into CT workflows, improving diagnostic accuracy and efficiency. Moreover, the support from reimbursement programs and clinical guidelines recommending coronary CT angiography (CCTA) as a frontline diagnostic tool is further accelerating market expansion.

Europe Cardiac Computed Tomography (CCT) Market Insight

The Europe cardiac computed tomography (CCT) market is projected to grow at a substantial CAGR throughout the forecast period, propelled by stringent healthcare regulations, rising cardiovascular risk awareness, and technological advancement in CT imaging. Many countries in the region are embracing spectral and dual-source CT technologies to enable enhanced cardiac imaging at reduced radiation doses. In addition, government investments in upgrading diagnostic infrastructure and increasing use of CCT in both public and private hospitals are boosting adoption. The shift towards value-based healthcare and early diagnosis initiatives further supports the growing use of CCT across Europe.

U.K. Cardiac Computed Tomography (CCT) Market Insight

The U.K. cardiac computed tomography (CCT) market is expected to grow at a noteworthy CAGR during the forecast period, driven by growing emphasis on early detection of coronary artery disease and national guidelines supporting the use of coronary CT angiography (CCTA). With NHS initiatives targeting reduced waiting times and improved cardiac diagnostics, hospitals are investing in advanced CT systems. Moreover, partnerships between imaging equipment providers and academic research centers are accelerating innovation and adoption of AI-enabled cardiac CT workflows.

Germany Cardiac Computed Tomography (CCT) Market Insight

The Germany cardiac computed tomography (CCT) market is anticipated to expand at a considerable CAGR during the forecast period, supported by high healthcare spending, technological leadership, and a proactive approach to cardiac health. Germany’s emphasis on clinical precision and innovation promotes the integration of spectral and AI-enhanced CT systems in cardiology departments. Increased awareness of early cardiovascular screening and strong hospital infrastructure further drive the market, especially within academic and urban healthcare institutions.

Asia-Pacific Cardiac Computed Tomography (CCT) Market Insight

The Asia-Pacific cardiac computed tomography (CCT) market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare expenditure, rising incidence of heart diseases, and growing adoption of advanced diagnostic imaging in countries such as China, Japan, and India. Government efforts to modernize healthcare infrastructure and the presence of cost-effective manufacturers are enhancing accessibility to CCT technologies. Furthermore, initiatives promoting AI-driven diagnostics and early disease detection are fueling demand across urban and semi-urban regions.

Japan Cardiac Computed Tomography (CCT) Market Insight

The Japan cardiac computed tomography (CCT) market is gaining traction due to its aging population, advanced technological capabilities, and strong government support for cardiovascular screening. Hospitals are rapidly adopting high-resolution and low-dose cardiac CT systems, integrated with AI to assist in clinical decision-making. Japan’s healthcare institutions prioritize patient safety and diagnostic accuracy, making CCT a preferred modality for non-invasive coronary imaging. Ongoing research collaborations are also enhancing the development of next-generation CT technologies in the country.

India Cardiac Computed Tomography (CCT) Market Insight

The India cardiac computed tomography (CCT) market accounted for the largest market revenue share in Asia Pacific in 2024, fueled by rising cases of heart disease, urbanization, and growing awareness of preventive health. The Indian government’s push towards affordable healthcare and smart hospitals is supporting CCT adoption in tier-1 and tier-2 cities. Private diagnostic chains and specialty hospitals are increasingly investing in cardiac CT infrastructure, while local manufacturers are offering competitively priced systems to expand reach. Integration of tele-radiology and AI also plays a growing role in accelerating adoption in remote regions

Cardiac Computed Tomography (CCT) Market Share

The cardiac computed tomography (CCT) industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Koninklijke Philips N.V (Netherlands)

- Shimadzu Corporation (Japan)

- Samsung Medison Co., Ltd. (South Korea)

- FUJIFILM Healthcare Corporation (Japan)

- Hitachi High-Tech Corporation (Japan)

- Neusoft Medical Systems Co., Ltd. (China)

- Shanghai United Imaging Healthcare Co., LTD (China)

- HeartFlow, Inc. (U.S.)

- Circle Cardiovascular Imaging Inc. (Canada)

- Ziosoft (U.S.)

- Arineta Ltd. (Israel)

- TeraRecon (U.S.)

- Intrasense SA (France)

- ContextVision (Sweden)

- Core Sound Imaging, Inc. (U.S.)

- Imalogix, LLC (U.S.)

- LifeVoxel (U.S.)

What are the Recent Developments in Global Cardiac Computed Tomography (CCT) Market?

- In April 2023, Siemens Healthineers introduced its latest cardiac CT scanner, the SOMATOM Force, designed to deliver ultra-fast, high-resolution imaging with reduced radiation exposure. This advancement is particularly impactful for patients with high heart rates or arrhythmias, improving diagnostic precision for coronary artery disease. Siemens’ innovation reflects its ongoing commitment to enhancing non-invasive cardiac imaging and addressing the global need for accurate, patient-centric diagnostics

- In March 2023, GE HealthCare announced the launch of its TrueFidelity CT image reconstruction technology in cardiovascular imaging applications. The deep-learning-based system enhances image clarity while significantly reducing noise, allowing for improved visualization of coronary arteries. This development marks a crucial step in leveraging artificial intelligence to support early and reliable detection of cardiac conditions and reinforces GE’s leadership in smart imaging solutions

- In March 2023, Canon Medical Systems expanded its cardiac imaging portfolio with the introduction of the Aquilion ONE / PRISM Edition, a spectral CT system offering detailed cardiac imaging with advanced iodine quantification. This system aids clinicians in identifying ischemic regions and assessing myocardial perfusion with greater precision. Canon’s innovation demonstrates its commitment to providing comprehensive cardiac assessments through cutting-edge CT technology

- In February 2023, Philips announced a strategic partnership with the Mayo Clinic to co-develop AI-driven cardiac imaging solutions aimed at optimizing CT workflows and improving diagnostic accuracy. The collaboration focuses on real-time data integration and automated interpretation of cardiac scans, enhancing clinician efficiency and patient outcomes. This initiative underscores the growing importance of AI in advancing CT cardiac diagnostics and streamlining clinical operations

- In January 2023, HeartFlow, Inc. received expanded regulatory approval for its non-invasive FFRct Analysis platform, which integrates seamlessly with standard cardiac CT to assess coronary artery disease. The platform uses machine learning to create 3D models of the coronary arteries and evaluate blood flow, supporting personalized treatment decisions. This milestone highlights the increasing adoption of computational technologies in enhancing the utility of cardiac CT in routine clinical practice

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.