Global Cardiovascular Information Systems Market

Market Size in USD Billion

USD

1.31 Billion

USD

2.49 Billion

2025

2033

USD

1.31 Billion

USD

2.49 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.31 Billion | |

| USD 2.49 Billion | |

| % | |

|

Cardiovascular Information Systems Market Size

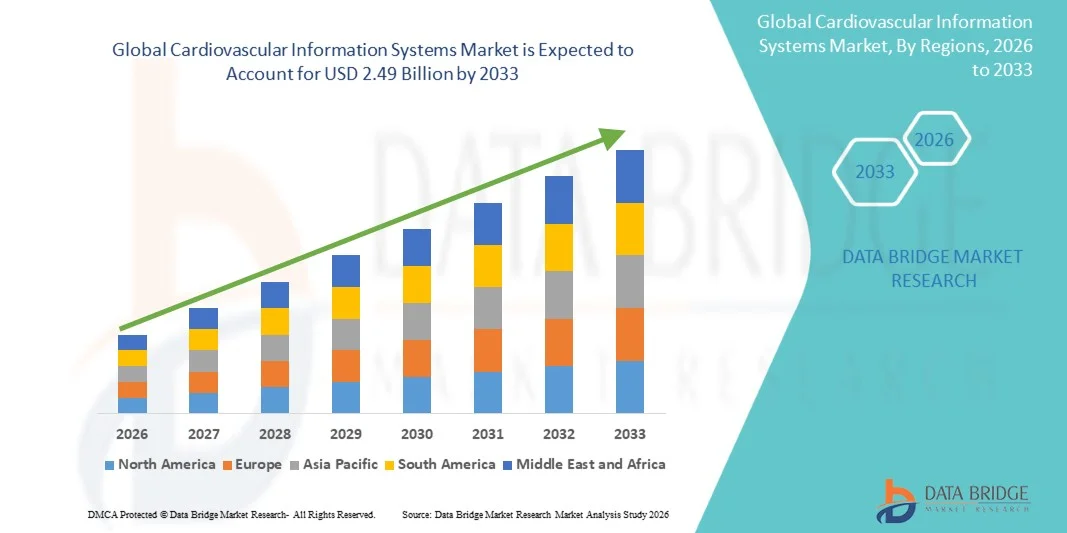

- The global cardiovascular information systems market size was valued at USD 1.31 billion in 2025 and is expected to reach USD 2.49 billion by 2033, at a CAGR of 8.4% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital healthcare infrastructure and the integration of advanced IT solutions within cardiology departments, enabling efficient storage, retrieval, and analysis of cardiovascular data across healthcare facilities

- Furthermore, rising demand for improved patient outcomes, interoperability between healthcare systems, and the need for streamlined workflow management in cardiac care settings is driving the adoption of cardiovascular information systems, thereby significantly supporting the industry’s expansion

Cardiovascular Information Systems Market Analysis

- Cardiovascular information systems, which enable the digital management, storage, and integration of cardiac data such as images, reports, and patient records, are becoming essential in modern healthcare settings, particularly in hospitals and cardiology centers, due to their ability to improve workflow efficiency, data accessibility, and clinical decision-making

- The escalating demand for cardiovascular information systems is primarily driven by the increasing prevalence of cardiovascular diseases, the growing need for efficient management of large volumes of diagnostic data, and the rising adoption of electronic health records and integrated healthcare IT solutions

- North America dominated the cardiovascular information systems market with the largest revenue share of 42.6% in 2025, supported by advanced healthcare infrastructure, high adoption of digital health technologies, and the presence of key market players, with the U.S. witnessing strong implementation across hospitals and specialty cardiac centers driven by ongoing technological advancements and regulatory support for healthcare digitization

- Asia-Pacific is expected to be the fastest-growing region in the cardiovascular information systems market during the forecast period, driven by increasing healthcare investments, rapid urbanization, expanding patient population with cardiovascular diseases, and growing adoption of digital healthcare infrastructure across emerging economies

- The Web- based CVIS segment dominated the cardiovascular information systems market with a substantial market share of 45.8% in 2025, owing to its ease of deployment, scalability, remote accessibility, and seamless integration with existing hospital information systems and cloud-based healthcare platforms

Report Scope and Cardiovascular Information Systems Market Segmentation

|

Attributes |

Cardiovascular Information Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cardiovascular Information Systems Market Trends

“Enhanced Interoperability Through Cloud and AI Integration”

- A significant and accelerating trend in the global cardiovascular information systems market is the growing integration of cloud computing and artificial intelligence (AI) with hospital information systems and imaging platforms, enabling seamless data exchange, advanced analytics, and improved clinical workflows across healthcare networks

- For instance, cloud-based cardiovascular information systems allow cardiologists to access and share patient records, imaging data, and diagnostic reports in real time across multiple facilities, improving collaboration and continuity of care

- AI integration in cardiovascular information systems enables features such as automated image analysis, pattern recognition in cardiac scans, and predictive analytics for early detection of cardiovascular diseases, thereby supporting more accurate and timely clinical decisions

- The seamless integration of cardiovascular information systems with electronic health records (EHR), picture archiving and communication systems (PACS), and hospital information systems (HIS) facilitates centralized data management and streamlined workflows for healthcare providers

- This trend towards intelligent, interoperable, and data-driven cardiovascular platforms is reshaping clinical expectations, as healthcare institutions increasingly adopt integrated solutions that enhance efficiency, reduce errors, and support value-based care

- The demand for advanced cardiovascular information systems with cloud connectivity and AI-enabled capabilities is growing rapidly across hospitals and specialty cardiac centers, as providers prioritize efficient data handling, improved diagnostics, and scalable digital infrastructure

- Moreover, the rising focus on cybersecurity-enhanced cloud platforms is encouraging vendors to incorporate advanced encryption and compliance features, ensuring secure handling of sensitive cardiovascular patient data while maintaining system accessibility and scalability

Cardiovascular Information Systems Market Dynamics

Driver

“Growing Need Due to Rising Cardiovascular Disease Burden and Healthcare Digitalization”

- The increasing prevalence of cardiovascular diseases globally, coupled with the accelerating adoption of digital healthcare infrastructure, is a significant driver for the heightened demand for cardiovascular information systems

- For instance, in 2025, several healthcare institutions expanded investments in integrated cardiac IT solutions to streamline patient data management and improve diagnostic efficiency across cardiology departments

- As healthcare providers face growing volumes of cardiac data from imaging modalities such as echocardiography, angiography, and ECG systems, cardiovascular information systems offer advanced capabilities for data storage, retrieval, and analysis, supporting better clinical outcomes

- Furthermore, the shift toward value-based care and the need for coordinated treatment approaches are making cardiovascular information systems an essential tool for improving workflow efficiency and enhancing collaboration among healthcare professionals

- The convenience of centralized data access, automated reporting, and integration with other healthcare IT systems is driving adoption in hospitals and diagnostic centers, while the increasing use of telecardiology and remote monitoring further contributes to market growth

- In addition, government initiatives promoting healthcare digitization and the implementation of electronic health records are encouraging healthcare providers to adopt integrated cardiovascular information systems for improved data management

- Moreover, the growing demand for precision medicine and data-driven clinical decision-making is further accelerating the deployment of advanced cardiovascular IT solutions across healthcare institutions

Restraint/Challenge

“High Implementation Costs and Data Security Concerns”

- Concerns surrounding high initial implementation and maintenance costs of cardiovascular information systems, along with challenges in system integration and infrastructure requirements, pose a significant barrier to broader market adoption

- For instance, smaller healthcare facilities and clinics often face budget constraints that limit their ability to deploy advanced cardiovascular IT systems with full interoperability and cloud-based functionalities

- In addition, cybersecurity risks associated with the storage and transmission of sensitive patient data present another major challenge, as cardiovascular information systems rely heavily on network connectivity and digital platforms

- Addressing these concerns through robust encryption, compliance with healthcare data regulations, and secure authentication protocols is essential to ensure patient data protection and build trust among healthcare providers

- While technological advancements and vendor innovations are gradually improving affordability and security features, the perceived complexity and cost of deployment can still hinder adoption, particularly in resource-limited settings and emerging markets

- Furthermore, interoperability challenges between legacy healthcare systems and modern cardiovascular information platforms can create integration issues, leading to additional implementation time and costs

- In addition, the shortage of skilled IT personnel and training requirements for healthcare staff to effectively operate advanced cardiovascular information systems can further slow down adoption rates across institutions

Cardiovascular Information Systems Market Scope

The market is segmented on the basis of system type, component, mode of operation, end-users, application, and mode of workflow.

- By System Type

On the basis of system type, the cardiovascular information systems market is segmented into CVIS and CPACS. The CVIS segment dominated the market with the largest market revenue share of 65% in 2025, driven by its comprehensive capabilities in managing cardiovascular data, including integration with multiple modalities, reporting tools, and workflow management across cardiology departments. Hospitals and large healthcare systems widely prefer CVIS due to its ability to consolidate patient data from various diagnostic systems into a unified platform, improving clinical efficiency and decision-making. CVIS solutions are also increasingly integrated with EHR and PACS systems, further strengthening their adoption in advanced healthcare settings. The growing need for centralized cardiovascular data management and interoperability continues to support the dominance of this segment.

The CPACS segment is expected to witness the fastest growth rate during the forecast period, driven by increasing demand for specialized imaging-focused solutions that efficiently manage cardiovascular images and related data. CPACS is particularly gaining traction in diagnostic centers and hospitals with high imaging volumes, where seamless storage, retrieval, and sharing of cardiac images is critical. The rising adoption of advanced imaging modalities such as CT angiography and cardiac MRI is further boosting demand for CPACS. In addition, CPACS solutions are increasingly being integrated with cloud-based platforms, enabling remote access and improved collaboration among healthcare professionals, which is accelerating their adoption.

- By Component

On the basis of component, the cardiovascular information systems market is segmented into software, services, and hardware. The software segment dominated the market with the largest revenue share of 55% in 2025, owing to its critical role in managing, analyzing, and integrating cardiovascular data across healthcare systems. Software platforms form the core of CVIS and CPACS solutions, enabling functionalities such as reporting, data visualization, workflow automation, and interoperability with other hospital systems. The increasing deployment of cloud-based and AI-enabled software solutions is further driving the dominance of this segment. Healthcare providers prefer software solutions due to their scalability, upgradability, and ability to support evolving clinical requirements.

The services segment is expected to witness the fastest growth rate during the forecast period, driven by the rising need for implementation, integration, maintenance, and support services associated with cardiovascular information systems. As healthcare organizations adopt complex IT infrastructures, demand for consulting, training, and system customization services is increasing. In addition, ongoing maintenance, upgrades, and cybersecurity support are essential for ensuring system performance and data protection, contributing to the growth of the services segment. The shift toward cloud-based deployments is also increasing reliance on managed services, further accelerating segment expansion.

- By Mode of Operation

On the basis of mode of operation, the cardiovascular information systems market is segmented into web-based CVIS, onsite CVIS, and cloud-based CVIS. The web-based CVIS segment dominated the market with the largest share of 45.8% in 2025, driven by its ease of deployment, remote accessibility, and compatibility with existing hospital IT infrastructure. Web-based systems allow healthcare professionals to access cardiovascular data from multiple locations without requiring extensive on-premise installations. Their ability to integrate with EHR, PACS, and other systems makes them highly preferred in hospitals and multi-site healthcare networks.

The cloud-based CVIS segment is expected to witness the fastest growth rate during the forecast period, driven by increasing adoption of scalable, cost-effective, and flexible healthcare IT solutions. Cloud-based systems enable real-time data sharing, remote collaboration, and centralized data storage, which are particularly beneficial for large healthcare organizations and telecardiology applications. The growing emphasis on digital transformation in healthcare, along with improved data security measures in cloud platforms, is accelerating adoption. In addition, cloud-based CVIS reduces the need for significant upfront infrastructure investment, making it attractive for both developed and emerging markets.

- By End-Users

On the basis of end-users, the cardiovascular information systems market is segmented into hospitals and diagnostic centers. The hospital segment dominated the market with the largest revenue share of 70% in 2025, driven by the high volume of cardiovascular procedures and the need for integrated systems to manage complex patient data. Hospitals require comprehensive CVIS solutions to handle multiple departments such as catheterization labs, electrophysiology labs, and imaging units, making them the primary adopters. The increasing prevalence of cardiovascular diseases and the growing number of hospital-based cardiac procedures further support this dominance.

The diagnostic centers segment is expected to witness the fastest growth rate during the forecast period, driven by the rising demand for specialized cardiac diagnostic services and the expansion of outpatient care facilities. Diagnostic centers are increasingly adopting CPACS and CVIS solutions to efficiently manage imaging data and improve reporting accuracy. The growing trend toward early diagnosis and preventive cardiac care is also contributing to increased utilization of diagnostic centers. In addition, advancements in portable imaging technologies and the expansion of independent diagnostic chains are accelerating adoption in this segment.

- By Application

On the basis of application, the cardiovascular information systems market is segmented into catheterization lab CVIS solutions, echocardiography lab CVIS solutions, electrophysiology lab CVIS solutions, nuclear cardiology CVIS solutions, cardiothoracic center CVIS solutions, ECG/Holter monitoring CVIS solutions, pacemaker/ICD lab CVIS solutions, heart failure center CVIS solutions, outpatient clinic CVIS solutions, and others. The catheterization lab CVIS solutions segment dominated the market with the largest share of 30% in 2025, driven by the high volume of interventional cardiology procedures and the need for real-time data integration, reporting, and workflow optimization in cath labs. These systems enable efficient management of angiographic images, procedure documentation, and hemodynamic data, making them essential in interventional settings.

The heart failure center CVIS solutions segment is expected to witness the fastest growth rate during the forecast period, driven by the rising global burden of heart failure and the increasing need for continuous patient monitoring and data-driven management. These solutions support long-term tracking of patient conditions, integration of remote monitoring data, and personalized treatment planning. The growing adoption of remote patient monitoring and telehealth services is further accelerating demand for CVIS solutions in heart failure management. In addition, healthcare providers are increasingly focusing on chronic disease management, which is boosting the adoption of specialized CVIS applications in this segment.

- By Mode of Workflow

On the basis of mode of workflow, the cardiovascular information systems market is segmented into cardiac catheterization, electrophysiology, vascular catheterization, echocardiography, ECG, cardiac CT, cardiac MRA, and others. The cardiac catheterization segment dominated the market with the largest revenue share of 35% in 2025, driven by the high frequency of interventional procedures and the need for comprehensive data management during diagnostic and therapeutic interventions. CVIS solutions in this workflow support real-time data acquisition, imaging integration, and reporting, making them critical for cath lab operations. The increasing prevalence of coronary artery diseases and the growing number of minimally invasive procedures further support this segment’s dominance.

The cardiac CT and cardiac MRA segment is expected to witness the fastest growth rate during the forecast period, driven by the increasing adoption of advanced non-invasive imaging techniques for early diagnosis of cardiovascular conditions. These modalities generate large volumes of high-resolution imaging data, requiring efficient storage, processing, and integration capabilities provided by CVIS platforms. The growing preference for non-invasive diagnostic methods, along with technological advancements in imaging accuracy and speed, is accelerating the adoption of CVIS solutions in these workflows.

Cardiovascular Information Systems Market Regional Analysis

- North America dominated the cardiovascular information systems market with the largest revenue share of 42.6% in 2025, supported by advanced healthcare infrastructure, high adoption of digital health technologies, and the presence of key market players

- Healthcare providers in the region highly value the integration of cardiovascular information systems with electronic health records, PACS, and hospital information systems, enabling efficient data management, improved interoperability, and enhanced clinical decision-making

- This widespread adoption is further supported by high healthcare expenditure, the presence of leading market players, and favorable regulatory initiatives promoting healthcare digitization, establishing cardiovascular information systems as a critical component in hospitals and specialized cardiac care centers

U.S. Cardiovascular Information Systems Market Insight

The U.S. cardiovascular information systems market captured the largest revenue share within North America in 2025, fueled by the rapid adoption of advanced healthcare IT solutions and the growing burden of cardiovascular diseases. Healthcare providers are increasingly prioritizing integrated cardiovascular platforms to enhance diagnostic accuracy, streamline workflow, and manage large volumes of patient data efficiently. The widespread use of electronic health records, coupled with strong investments in digital health infrastructure, further supports market growth. Moreover, the integration of AI-enabled analytics, cloud-based CVIS platforms, and interoperability with hospital systems is significantly contributing to the market’s expansion.

Europe Cardiovascular Information Systems Market Insight

The Europe cardiovascular information systems market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by government initiatives promoting healthcare digitization and the need for improved interoperability across healthcare systems. The increasing prevalence of cardiovascular diseases and the demand for efficient clinical data management are encouraging the adoption of CVIS solutions across hospitals and diagnostic centers. European healthcare providers are also focusing on value-based care and data-driven decision-making, which is fostering the integration of advanced cardiovascular IT systems. In addition, the region is witnessing significant adoption across both public and private healthcare facilities, supporting steady market growth.

U.K. Cardiovascular Information Systems Market Insight

The U.K. cardiovascular information systems market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the expansion of digital healthcare initiatives and the increasing emphasis on improving patient outcomes. The National Health Service (NHS) is actively promoting the adoption of electronic systems and integrated healthcare platforms, which is accelerating CVIS implementation. Rising cardiovascular disease incidence and the need for efficient management of diagnostic and imaging data are further supporting market growth. In addition, the growing use of telecardiology and remote monitoring solutions is enhancing the demand for cardiovascular information systems in both hospital and outpatient settings.

Germany Cardiovascular Information Systems Market Insight

The Germany cardiovascular information systems market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and increasing investment in digital health technologies. Germany’s focus on data privacy, interoperability, and advanced medical systems is encouraging the adoption of secure and efficient CVIS platforms. Hospitals and specialty cardiac centers are increasingly integrating CVIS with PACS and EHR systems to streamline workflows and improve diagnostic efficiency. Furthermore, the country’s emphasis on innovation and precision medicine is promoting the use of advanced cardiovascular analytics and imaging solutions, supporting sustained market growth.

Asia-Pacific Cardiovascular Information Systems Market Insight

The Asia-Pacific cardiovascular information systems market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare expenditure, rising prevalence of cardiovascular diseases, and rapid digital transformation in healthcare infrastructure across emerging economies such as China, Japan, and India. The region’s growing focus on expanding hospital networks and improving access to advanced diagnostic technologies is accelerating CVIS adoption. Government initiatives supporting healthcare modernization and smart hospital development are further boosting demand. In addition, the availability of cost-effective solutions and increasing investments by global and regional players are expanding the market reach across a broader healthcare base.

Japan Cardiovascular Information Systems Market Insight

The Japan cardiovascular information systems market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong emphasis on technological innovation. The increasing incidence of cardiovascular conditions among the elderly population is driving demand for efficient data management and integrated cardiac care solutions. Japanese healthcare providers are increasingly adopting CVIS platforms to enhance workflow efficiency, support imaging integration, and improve clinical outcomes. Moreover, the integration of cardiovascular systems with IoT-enabled medical devices and hospital IT infrastructure is further fueling market growth in the country.

India Cardiovascular Information Systems Market Insight

The India cardiovascular information systems market accounted for a significant revenue share in Asia Pacific in 2025, attributed to the country’s large patient population, rising burden of cardiovascular diseases, and growing adoption of digital healthcare solutions. India is witnessing increasing investments in hospital infrastructure and diagnostic centers, which is supporting the deployment of CVIS platforms. The government’s push toward digital health initiatives and smart healthcare ecosystems is further accelerating market adoption. In addition, the availability of cost-effective solutions, combined with expanding private healthcare facilities and increasing awareness of advanced cardiac care technologies, is driving the growth of cardiovascular information systems in India.

Cardiovascular Information Systems Market Share

The Cardiovascular Information Systems industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- INFINITT Healthcare (South Korea)

- Novarad (U.S.)

- ScImage, Inc. (U.S.)

- Sectra AB (Sweden)

- Merative (U.S.)

- Change Healthcare (U.S.)

- Ascend Cardiovascular, LLC (U.S.)

- HeartIT (U.S.)

- Digisonics, Inc. (U.S.)

- MIM Software Inc. (Canada)

- Medis Medical Imaging Systems (Netherlands)

- Central Data Networks (Australia)

- LUMEDX (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Agfa HealthCare (Belgium)

- FUJIFILM Holdings Corporation (Japan)

- Esaote SpA (Italy)

What are the Recent Developments in Global Cardiovascular Information Systems Market?

- In November 2025, Hannover Medical School went live with the world’s first clinical integration of GE HealthCare’s MUSE Cardiology Information System and AliveCor technologies, enhancing real-world cardiac data integration and clinical workflow

- In March 2025, Apollo Hospitals entered a new collaboration with Solventum Health Information Systems to integrate its AI-powered cardiovascular disease risk prediction tool with advanced patient classification and quality methodologies, aiming to enhance predictive cardiovascular care

- In July 2024, a leading health IT provider announced the launch of a new cloud-based cardiology information platform designed to offer scalable, flexible solutions for healthcare institutions, featuring remote monitoring, telemedicine integration, and advanced analytics to support growing demand for cloud-enabled cardiovascular data management

- In September 2023, GE HealthCare won a contract to implement a statewide cardiovascular information system for Queensland Health in Australia, rolling out its Centricity Cardio Enterprise (CCE) solution across 11 hospital and health services to replace legacy cardiac catheter laboratory and echocardiography systems and centralize cardiovascular data management

- In March 2022, GE Healthcare and AliveCor collaborated to integrate patient-captured six-lead ECG data into GE’s MUSE Cardiac Management System, enabling physicians to review home-recorded ECGs and improve proactive cardiac patient management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.