Global Cataplexy Treatment Market

Market Size in USD Billion

USD

4.15 Billion

USD

7.18 Billion

2025

2033

USD

4.15 Billion

USD

7.18 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.15 Billion | |

| USD 7.18 Billion | |

| % | |

|

Cataplexy Treatment Market Size

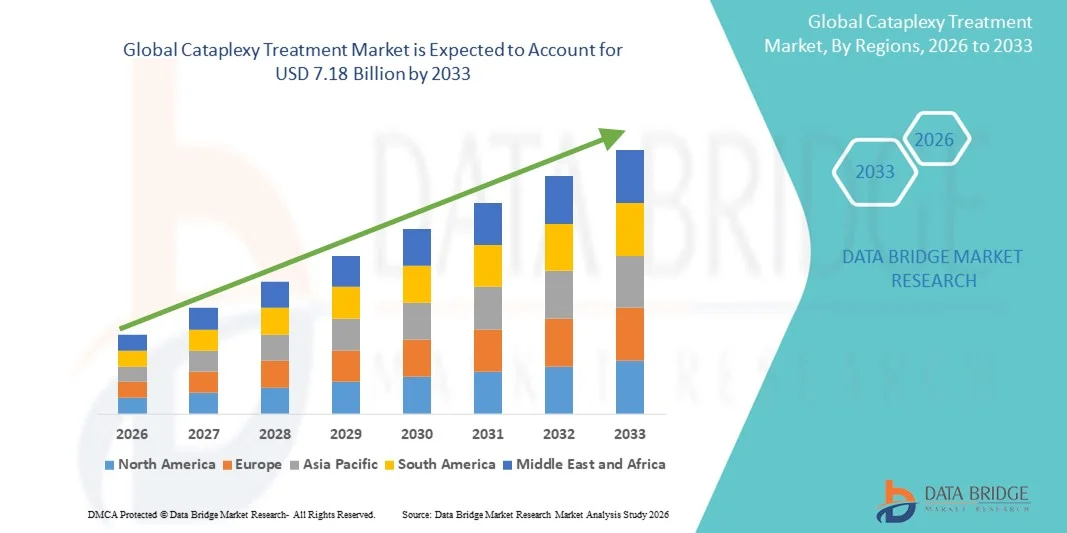

- The global cataplexy treatment market size was valued at USD 4.15 billion in 2025 and is expected to reach USD 7.18 billion by 2033, at a CAGR of 7.10% during the forecast period

- The market growth is largely fueled by rising awareness of sleep disorders, technological and pharmacological advances in therapies targeting cataplexy, and increasing diagnosis rates in both developed and emerging markets

- Furthermore, rising patient demand for more effective, safer, and convenient treatment options for cataplexy is establishing advanced therapies as the preferred choice. These converging factors are accelerating the uptake of cataplexy treatment solutions, thereby significantly boosting the industry's growth

Cataplexy Treatment Market Analysis

- Cataplexy treatments, including pharmacological therapies such as sodium oxybate, antidepressants, and emerging novel agents, are increasingly vital components of managing narcolepsy type 1, improving patient quality of life by reducing sudden muscle‑weakness episodes and enhancing daytime alertness in both adult and pediatric populations

- The escalating demand for cataplexy treatments is primarily fueled by growing awareness of sleep disorders, increasing diagnosis rates, and rising patient preference for safer, more effective, and convenient treatment options

- North America dominated the cataplexy treatment market with the largest revenue share of 42.7% in 2025, characterized by high healthcare spending, advanced healthcare infrastructure, and strong presence of key pharmaceutical players, with the U.S. experiencing substantial growth in cataplexy therapy adoption, driven by innovations in next‑generation therapies and increased access to specialist sleep clinic

- Asia-Pacific is expected to be the fastest growing region in the cataplexy treatment market during the forecast period due to improving healthcare infrastructure, rising awareness of sleep disorders, and increasing patient access to modern treatment options

- Sodium oxybate segment dominated the cataplexy treatment market with a market share of 38.9% in 2025, driven by its established efficacy in reducing cataplexy attacks and improving overall sleep quality in patients with narcolepsy type 1

Report Scope and Cataplexy Treatment Market Segmentation

|

Attributes |

Cataplexy Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cataplexy Treatment Market Trends

Rise of Novel Targeted Therapies and Digital Monitoring

- A significant and accelerating trend in the global cataplexy treatment market is the development of novel, targeted therapies, including next-generation sodium oxybate formulations and selective antidepressants, which are improving symptom control and patient adherence

- For instance, newer extended-release sodium oxybate therapies allow reduced dosing frequency, improving convenience and quality of life for narcolepsy patients with cataplexy

- Digital health and remote monitoring tools are increasingly integrated into treatment plans, enabling physicians to track cataplexy episodes, medication adherence, and sleep patterns more accurately

- For instance, wearable sleep trackers and mobile apps are being used alongside therapy to provide real-time feedback, allowing personalized dose adjustments and better management of daily symptoms

- The trend towards combining pharmacological innovation with digital monitoring is fundamentally enhancing patient-centric care, supporting improved outcomes and greater engagement in long-term management

- For instance, companies such as Jazz Pharmaceuticals are exploring app-based monitoring in clinical programs to complement pharmacotherapy and optimize cataplexy management

- Integration of AI-driven analytics in sleep monitoring is emerging to predict cataplexy attacks and optimize therapy schedules for individual patients

Cataplexy Treatment Market Dynamics

Driver

Increasing Awareness and Diagnosis of Sleep Disorders

- The growing awareness of sleep disorders, especially narcolepsy with cataplexy, coupled with increased access to specialist care, is a major driver for market growth

- For instance, public health campaigns and patient advocacy programs in North America and Europe are improving early diagnosis and treatment initiation for cataplexy patients

- Rising diagnosis rates are encouraging adoption of both established and emerging therapies, driving overall revenue growth in the market. For instance, initiatives by sleep clinics to screen patients with excessive daytime sleepiness have led to higher identification of narcolepsy type 1 cases

- Patient preference for safer, effective, and convenient treatment options, including oral and extended-release formulations, further supports adoption of advanced cataplexy therapies

- For instance, patient surveys indicate strong demand for once-nightly sodium oxybate formulations due to improved ease of use and reduced sleep disruption

- Increasing research collaborations and clinical trials are accelerating development of innovative therapies for cataplexy, opening new treatment avenues

- For instance, multinational pharmaceutical companies are conducting global trials on novel GABA-B agonists and anti-cataplectic compounds to expand treatment options

Restraint/Challenge

High Treatment Costs and Limited Access in Emerging Markets

- The relatively high cost of cataplexy therapies, especially branded sodium oxybate and novel treatments, poses a significant challenge to widespread adoption, particularly in price-sensitive regions

- For instance, patients in Asia-Pacific and Latin America may have limited access due to affordability barriers or insufficient insurance coverage for advanced therapies

- Availability of specialist sleep clinics and trained healthcare providers is limited in certain regions, further restricting patient access to treatment. For instance, rural areas in developing countries often lack certified sleep centers for proper diagnosis and therapy management

- Addressing these challenges through cost reduction strategies, patient assistance programs, and broader healthcare infrastructure development is crucial for market expansion

- For instance, pharmaceutical companies are increasingly offering patient support programs and working with local health authorities to improve access and affordability of cataplexy treatments

- Regulatory hurdles and slow drug approvals in certain countries can delay the launch of new cataplexy therapies, limiting patient options

- For instance, some emerging markets require extensive local clinical data before approval, delaying availability of innovative treatments despite global regulatory clearance

Cataplexy Treatment Market Scope

The market is segmented on the basis of treatment, dosage, route of administration, diagnosis, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the cataplexy treatment market is segmented into sodium oxybate, tricyclic antidepressants, amphetamines, selective serotonin reuptake inhibitors (SSRIs), and modafinil. The Sodium Oxybate segment dominated the market with the largest market revenue share of 38.9% in 2025, driven by its established efficacy in reducing cataplexy attacks and improving overall sleep quality in narcolepsy patients. Physicians often prioritize Sodium Oxybate for patients with frequent and severe cataplexy episodes, as it directly addresses the symptom while improving nocturnal sleep. The market also sees strong demand due to ongoing product innovations, such as extended-release formulations, and its broad acceptance among regulatory authorities globally. Patient adherence and improvements in quality of life further make Sodium Oxybate a preferred therapy in both adult and pediatric populations. Widespread clinical use and high efficacy rates reinforce its dominant position across major markets worldwide.

The Tricyclic Antidepressants segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing off-label usage for cataplexy management and rising awareness among clinicians about their efficacy in reducing muscle weakness episodes. These therapies are increasingly prescribed where Sodium Oxybate is unavailable or contraindicated. Growing clinical evidence and published studies highlighting benefits and tolerability improvements are contributing to rapid adoption. Rising demand in emerging markets where cost-effective options are preferred also supports this segment’s growth. In addition, combination therapies with other narcolepsy medications are encouraging broader usage. The segment’s flexibility in dosing and availability in generic forms further enhances accessibility for patients.

- By Dosage

On the basis of dosage, the market is segmented into tablet, solution, capsule, and others. The Solution segment dominated the market in 2025, primarily due to the widespread use of sodium oxybate oral solution, which provides precise dosing and better absorption for effective cataplexy control. Physicians and patients often prefer solution-based dosing for its rapid action, dose flexibility, and ease of administration, especially in children and older adults. The market also benefits from well-established clinical protocols favoring liquid formulations. High patient adherence rates and regulatory approvals contribute to sustained demand. The solution form is also commonly used in hospital settings for monitored administration. Furthermore, growing awareness among caregivers about dosing convenience reinforces its dominant position.

The Tablet segment is anticipated to witness the fastest growth from 2026 to 2033, driven by the development of extended-release and fixed-dose tablet formulations that enhance convenience and improve patient compliance. Tablets are easier to transport, store, and consume, appealing to patients with active lifestyles. Pharmaceutical companies are expanding offerings in both emerging and mature markets. Innovations in combination tablet formulations further boost adoption. Increased patient preference for once-daily dosing schedules strengthens market potential. Awareness campaigns emphasizing adherence benefits are also supporting growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and other routes. The Oral segment dominated the market in 2025, as most approved cataplexy therapies including Sodium Oxybate, SSRIs, and Tricyclic Antidepressants are administered orally for systemic absorption and rapid onset of action. Oral administration ensures ease of use, patient adherence, and flexible dosing, making it the preferred route in both clinics and hospitals. Hospitals and clinics often incorporate oral therapy in standard treatment protocols. The convenience and familiarity of oral administration further reinforce its dominance. Regulatory approvals and wide availability of oral formulations support consistent market demand. Physicians frequently recommend oral therapies for their reliable pharmacokinetics.

The Other route segment is expected to witness the fastest growth during the forecast period, driven by ongoing R&D into alternative delivery systems such as sublingual or intranasal formulations. These alternatives aim to provide faster relief, improved bioavailability, and convenience for patients who may have difficulty with traditional oral administration. Clinical trials exploring these novel delivery methods are increasing adoption potential. Emerging patient-friendly devices encourage growth in this segment. Regulatory support for innovative formulations is improving market confidence. Education and awareness campaigns highlight benefits of alternative routes for better symptom control.

- By Diagnosis

On the basis of diagnosis, the market is segmented into physical evaluation, written evaluation, polysomnogram, and multiple sleep latency test (MSLT). The Polysomnogram segment dominated the market in 2025 due to its high accuracy in confirming narcolepsy type 1 and identifying cataplexy-related sleep abnormalities. Hospitals and sleep clinics heavily rely on this overnight test to develop personalized treatment plans. Polysomnogram-based diagnosis enables physicians to monitor therapy effectiveness over time. It is widely regarded as the gold standard for clinical evaluation. Patient outcomes improve with precise identification of sleep disruptions. The segment benefits from increasing awareness among clinicians and adoption in established sleep centers.

The Multiple Sleep Latency Test (MSLT) segment is expected to witness the fastest growth during the forecast period, as it allows quicker assessment of daytime sleepiness and narcolepsy severity. Growing awareness among clinicians of the importance of early diagnosis and integration of MSLT into routine evaluations drives adoption. It provides objective measurement of sleep propensity in controlled settings. Emerging sleep clinics are increasingly adopting MSLT protocols. Patient-friendly adaptations and telehealth-enabled testing solutions further boost growth. Research publications highlighting MSLT’s accuracy support its rapid market uptake.

- By Symptoms

On the basis of symptoms, the market is segmented into drooping eyelids, jaw tremor, facial twitching, flickering, speech difficulty, and others. The Drooping Eyelids segment dominated the market in 2025, as this symptom is among the most common and visually apparent manifestations of cataplexy, prompting early medical consultation and therapy initiation. Early recognition of eyelid drooping accelerates treatment adoption. Physicians often prioritize therapy initiation based on this visible symptom. Drooping eyelids facilitate clinical tracking of symptom improvement. Patient adherence improves when progress is observable. The segment benefits from strong awareness campaigns among caregivers and physicians. Its prevalence reinforces the dominant market share.

The Speech Difficulty segment is expected to witness the fastest growth during the forecast period, driven by increasing recognition of less obvious cataplexy manifestations and heightened clinician awareness. Advances in diagnostic techniques and patient reporting apps enable better tracking of subtle symptoms. Rising publications and case studies highlight the clinical importance of managing speech-related cataplexy effects. Improved symptom monitoring supports earlier therapy adoption. Awareness among patients and caregivers encourages reporting and treatment initiation. Telemedicine platforms further facilitate growth in this segment.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The Hospital segment dominated the market in 2025 due to comprehensive care, specialist sleep clinics, and access to advanced therapies such as Sodium Oxybate. Hospitals integrate diagnosis, treatment, and follow-up for optimal outcomes. They provide direct access to prescription-based medications. Managed care protocols and monitoring ensure patient safety. Hospitals often lead in clinical trials for innovative therapies. Their established infrastructure supports long-term therapy adherence.

The Clinic segment is expected to witness the fastest growth during the forecast period, driven by the increasing establishment of outpatient sleep clinics and telemedicine services that provide easier access to treatment. Clinics offer convenience, reduced waiting times, and personalized care. Adoption of modern therapies in clinics is increasing. Patient education initiatives enhance therapy compliance. Expansion of clinics in semi-urban and urban regions fuels growth. Collaboration with specialists and local hospitals accelerates market penetration.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market in 2025 due to direct access to specialty medications such as Sodium Oxybate and integration with patient monitoring. Hospital pharmacies ensure safe dispensing and adherence tracking. They often provide counseling for therapy management. Availability of advanced therapies reinforces dominance. Hospitals maintain inventory for critical patients. Regulatory compliance and quality standards support hospital pharmacy leadership.

The Online Pharmacy segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing e-pharmacy adoption, improved logistics, and convenience of home delivery. Online platforms support refill reminders, patient education, and subscription models. The COVID-19 pandemic accelerated acceptance of online delivery for chronic conditions. Patients in remote or underserved areas benefit from improved access. Telepharmacy services enhance adherence monitoring. Growing trust in digital healthcare ecosystems fuels rapid adoption.

Cataplexy Treatment Market Regional Analysis

- North America dominated the cataplexy treatment market with the largest revenue share of 42.7% in 2025, characterized by high healthcare spending, advanced healthcare infrastructure, and strong presence of key pharmaceutical players

- Patients and physicians in the region highly value the availability of advanced therapies such as Sodium Oxybate, selective antidepressants, and novel formulations, which provide effective management of cataplexy symptoms and improve quality of life

- This widespread adoption is further supported by high healthcare spending, strong insurance coverage, and growing research initiatives, establishing North America as a key market for both established and emerging cataplexy treatment solutions in adult and pediatric populations

U.S. Cataplexy Treatment Market Insight

The U.S. cataplexy treatment market captured the largest revenue share of 83% in 2025 within North America, fueled by the increasing diagnosis of narcolepsy type 1 and rising awareness of cataplexy symptoms. Patients are increasingly prioritizing access to advanced therapies such as Sodium Oxybate, SSRIs, and Tricyclic Antidepressants for effective symptom management. The growing adoption of specialist sleep clinics, coupled with strong insurance coverage and government support programs, further propels the market. In addition, integration of digital health tools and patient monitoring apps is enhancing treatment adherence and personalized care. The U.S. market also benefits from ongoing clinical trials and pharmaceutical innovations targeting improved safety and efficacy. Robust healthcare infrastructure and high per capita healthcare spending continue to sustain market expansion.

Europe Cataplexy Treatment Market Insight

The Europe cataplexy treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of sleep disorders and government initiatives promoting early diagnosis and treatment. Rising prevalence of narcolepsy type 1 and the availability of advanced therapies in major European countries are fostering market adoption. Patients and clinicians are also drawn to improved quality-of-life outcomes and better management of daytime sleepiness and cataplexy episodes. The region is witnessing growth across hospitals, clinics, and outpatient sleep centers, with therapy uptake in both new diagnoses and long-term care. In addition, reimbursement policies and healthcare infrastructure improvements are further supporting market growth. Increasing physician training and patient education campaigns are strengthening treatment acceptance.

U.K. Cataplexy Treatment Market Insight

The U.K. cataplexy treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising patient awareness and early intervention initiatives for narcolepsy and cataplexy. Concerns about quality of life, workplace productivity, and safety are motivating both patients and physicians to seek timely therapy. The U.K.’s strong healthcare infrastructure, coupled with accessible NHS programs and private sleep clinics, continues to support market growth. Adoption of both established and emerging therapies, along with digital monitoring tools, is further stimulating the market. In addition, growing interest in patient-centric care models and telemedicine platforms is facilitating therapy accessibility. The integration of evidence-based treatment protocols into clinical practice is also strengthening overall adoption.

Germany Cataplexy Treatment Market Insight

The Germany cataplexy treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of narcolepsy type 1 and growing demand for advanced pharmacological therapies. Germany’s robust healthcare system and emphasis on innovation support access to therapies such as Sodium Oxybate and emerging antidepressant-based treatments. Hospitals and specialized sleep centers are increasingly integrating digital tools to monitor patient adherence and symptom improvement. In addition, patients are becoming more aware of the benefits of timely intervention for cataplexy, contributing to therapy uptake. The strong focus on privacy, patient safety, and evidence-based care aligns with local expectations and promotes adoption. Continuous R&D and clinical studies are also encouraging market growth.

Asia-Pacific Cataplexy Treatment Market Insight

The Asia-Pacific cataplexy treatment market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by rising awareness of sleep disorders and improving healthcare infrastructure in countries such as China, Japan, and India. The region’s growing urbanization and increasing disposable incomes are enabling broader access to specialized sleep clinics and therapies. Government initiatives promoting digital health and patient monitoring tools are further accelerating market adoption. In addition, partnerships between international pharmaceutical companies and local distributors are increasing therapy availability. Telemedicine platforms and mobile health apps are supporting patient engagement and adherence. Expansion of clinical research and educational campaigns on narcolepsy and cataplexy are also contributing to rapid growth.

Japan Cataplexy Treatment Market Insight

The Japan cataplexy treatment market is gaining momentum due to the country’s advanced healthcare infrastructure, high patient awareness, and growing emphasis on quality of life. Adoption of therapies is supported by the increasing number of specialist sleep clinics and digital health monitoring tools. The integration of cataplexy management with broader chronic disease care is encouraging patient adherence. In addition, Japan’s aging population is driving demand for easier-to-use, safe, and effective treatments in both residential and hospital settings. Pharmaceutical innovations and ongoing clinical trials are further supporting market expansion. Government-led initiatives and public awareness campaigns are strengthening diagnosis and treatment adoption.

India Cataplexy Treatment Market Insight

The India cataplexy treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to increasing awareness of sleep disorders, rising urbanization, and expanding access to specialty healthcare services. The market is being propelled by availability of both generic and branded therapies and growing patient preference for modern treatment options. Telemedicine and mobile health platforms are improving access in semi-urban and rural areas. In addition, educational initiatives by healthcare providers and patient advocacy groups are encouraging early diagnosis and therapy initiation. Strong partnerships between local distributors and international pharmaceutical companies are increasing therapy reach. Government support for digital health and chronic disease management is further bolstering market growth.

Cataplexy Treatment Market Share

The Cataplexy Treatment industry is primarily led by well-established companies, including:

- Jazz Pharmaceuticals, Inc. (U.S.)

- Avadel (Ireland)

- Axsome Therapeutics, Inc. (U.S.)

- Harmony Biosciences Management, Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- NLS Pharmaceutics Ltd. (Switzerland)

- Amneal Pharmaceuticals LLC (U.S.)

- Alkermes (Ireland)

- Idorsia Pharmaceuticals Ltd (Switzerland)

- BIOPROJET (France)

- Eisai Co., Ltd. (Japan)

- UCB S.A. (Belgium)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Sosei Heptares Ltd. (U.K.)

- Sunovion Pharmaceuticals Inc. (U.S.)

- Recordati S.p.A. (Italy)

- Aptinyx, Inc. (U.S.)

What are the Recent Developments in Global Cataplexy Treatment Market?

- In September 2025, Amneal Pharmaceuticals received FDA approval for a generic oral solution form of sodium oxybate for cataplexy or EDS in narcolepsy patients. This development will such asly increase access and affordability of sodium oxybate therapy, thereby expanding the patient pool that can be treated

- In September 2025, Eisai Co., Ltd. disclosed clinical study results for its investigational orexin receptor agonist E2086 in narcolepsy type 1 showing potential for once‑daily dosing and improved daytime wakefulness. This represents a potentially paradigm‑shifting mechanism targeting the orexin/hypocretin system, which underpins the underlying pathophysiology of narcolepsy

- In October 2024, the FDA expanded the label for LUMRYZ to include pediatric patients aged 7 years and older with narcolepsy experiencing cataplexy or EDS. This pediatric indication is especially important because children with narcolepsy often face greater disruption from dosing schedules and require tailored therapies

- In March 2024, Axsome Therapeutics announced that its investigational drug AXS‑12 had achieved its primary endpoint in a Phase 3 study in narcolepsy patients with cataplexy, significantly reducing the frequency of cataplexy attacks compared to placebo

- In May 2023, LUMRYZ (extended‑release once‑nightly sodium oxybate) from Avadel Pharmaceuticals received approval from the U.S. Food & Drug Administration (FDA) for the treatment of cataplexy or excessive daytime sleepiness (EDS) in patients with narcolepsy aged 16 years and older. This approval marked a meaningful shift from the previous twice‑nightly oxybate dosing regimen toward a once‑nightly option, improving convenience and adherence for patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.