Global Cerebral Edema Treatment Market

Market Size in USD Billion

USD

3.70 Billion

USD

5.67 Billion

2024

2032

USD

3.70 Billion

USD

5.67 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.70 Billion | |

| USD 5.67 Billion | |

| % | |

|

Cerebral Edema Treatment Market Size

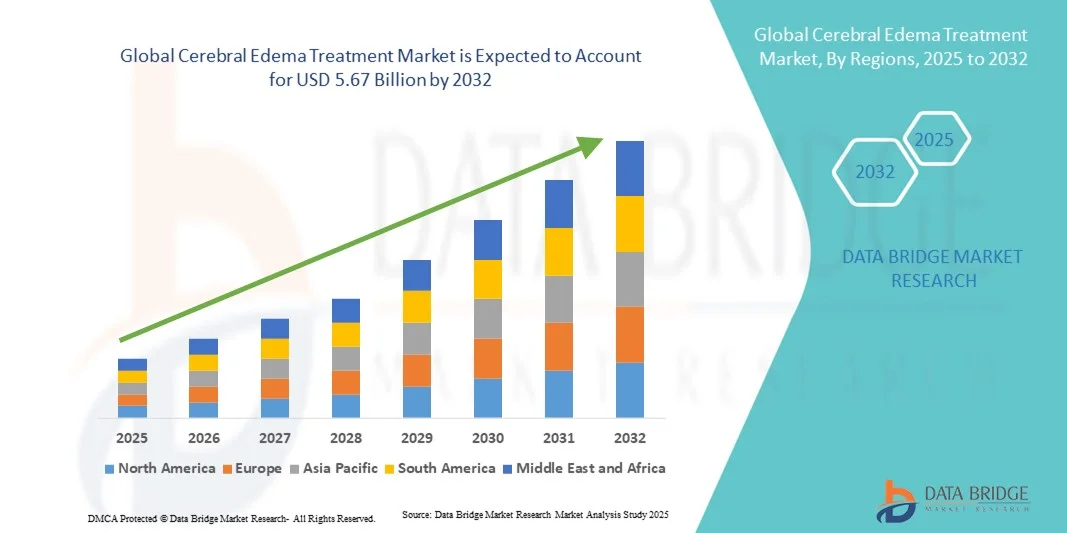

- The global cerebral edema treatment market size was valued at USD 3.70 billion in 2024 and is expected to reach USD 5.67 billion by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is primarily driven by the increasing incidence of neurological disorders such as traumatic brain injury (TBI), stroke, and brain tumors, which are major causes of cerebral edema. Advancements in medical technology and rising healthcare expenditures are further contributing to the demand for effective treatment solutions

- In addition, the aging global population and expanding research and development activities are establishing cerebral edema treatment as a critical component of neurological care. These converging factors are accelerating the uptake of cerebral edema treatment solutions, thereby significantly boosting the industry's growth

Cerebral Edema Treatment Market Analysis

- Cerebral edema treatments, including medications, osmotherapy, and surgical interventions, are increasingly vital components of modern neurological care in both hospitals and specialized clinics due to their critical role in reducing intracranial pressure, preventing brain damage, and improving patient outcomes

- The escalating demand for cerebral edema treatments is primarily fueled by the rising incidence of neurological disorders such as traumatic brain injuries, strokes, and brain tumors, coupled with advancements in medical technologies and growing healthcare expenditure

- North America dominated the cerebral edema treatment market with the largest revenue share of 39.2% in 2024, characterized by early adoption of advanced treatment methods, high healthcare spending, and a strong presence of key industry players, with the U.S. experiencing substantial growth in the use of pharmacological and surgical interventions, driven by innovations from both established pharmaceutical companies and neurosurgical device manufacturers

- Asia-Pacific is expected to be the fastest-growing region in the cerebral edema treatment market during the forecast period due to increasing healthcare infrastructure, rising disposable incomes, and growing awareness of advanced treatment options, with countries such as India and China investing heavily in neurology care facilities

- Medication segment dominated the cerebral edema treatment market with a market share of 46.1% in 2024, driven by the widespread use of osmotic diuretics and corticosteroids, which are preferred for their non-invasive nature and effectiveness in controlling brain swelling

Report Scope and Cerebral Edema Treatment Market Segmentation

|

Attributes |

Cerebral Edema Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cerebral Edema Treatment Market Trends

Advancements in AI-Assisted Monitoring and Minimally Invasive Procedures

- A significant and accelerating trend in the global cerebral edema treatment market is the incorporation of AI-assisted neuro-monitoring and minimally invasive surgical interventions, improving patient outcomes and treatment precision

- For instance, AI-enabled intracranial pressure monitors provide real-time data to clinicians, helping optimize therapy and predict potential complications, while minimally invasive decompressive procedures reduce recovery time

- AI integration enables features such as predictive modeling of cerebral swelling progression and personalized medication dosing, while surgical robotics support precise interventions with minimal tissue damage

- The integration of these technologies facilitates coordinated patient care, allowing multidisciplinary teams to monitor, treat, and adjust therapy in real-time through a centralized system

- This trend toward intelligent, precise, and less invasive treatment solutions is reshaping clinical expectations and patient management strategies, prompting companies such as Medtronic and DePuy Synthes to develop AI-enabled neuro-monitoring devices

- The demand for cerebral edema treatments with AI-assisted monitoring and minimally invasive options is growing across hospitals and specialized neurology centers, as clinicians increasingly prioritize precision, safety, and improved patient recovery

Cerebral Edema Treatment Market Dynamics

Driver

Rising Neurological Disorders and Expanding Healthcare Infrastructure

- The increasing prevalence of neurological disorders such as traumatic brain injuries, strokes, and brain tumors, coupled with expanding healthcare infrastructure, is a significant driver of cerebral edema treatment adoption

- For instance, in March 2024, a leading hospital network in the U.S. implemented AI-assisted cerebral edema management systems to improve patient monitoring and therapeutic outcomes, reflecting growing market uptake

- As the global patient population becomes more susceptible to neurological complications, treatments offering rapid intervention, precise monitoring, and effective symptom management are in higher demand

- Furthermore, rising investments in hospitals and specialized neurology clinics are making advanced treatments more accessible, promoting adoption of pharmacological and surgical interventions

- The growing awareness among clinicians regarding the criticality of timely intervention and the effectiveness of combined pharmacological and minimally invasive approaches is also propelling market growth

- Healthcare policies supporting modern neurological care and increasing funding for critical care infrastructure further reinforce the adoption of advanced cerebral edema treatments

Restraint/Challenge

High Treatment Costs and Regulatory Compliance Hurdles

- The high cost of advanced pharmacological agents and minimally invasive surgical devices poses a challenge to market expansion, especially in developing regions and budget-constrained healthcare facilities

- For instance, reports of high-priced neuro-monitoring systems have caused hesitation among smaller hospitals and clinics to adopt state-of-the-art cerebral edema solutions

- Strict regulatory approvals for drugs and surgical devices, along with the need for clinical trial validation, can delay product launches and market penetration

- Addressing these concerns through patient assistance programs, cost-effective treatment models, and streamlined regulatory compliance is essential for wider adoption

- Although generic medications and standardized surgical protocols are gradually reducing overall treatment costs, advanced technologies such as AI-assisted monitoring still carry premium pricing that may hinder uptake

- Overcoming these challenges through improved cost accessibility, clinician training, and regulatory support will be critical for sustained growth in the cerebral edema treatment market

Cerebral Edema Treatment Market Scope

The market is segmented on the basis of type, treatment, diagnosis, dosage, route of administration, symptoms, end-users, and distribution channel

- By Type

On the basis of type, the cerebral edema treatment market is segmented into cytotoxic, vasogenic, interstitial, hydrostatic, and osmotic. The vasogenic segment dominated the market with the largest revenue share in 2024, driven by its prevalence in patients with brain tumors, abscesses, or trauma-induced edema. Vasogenic edema causes blood-brain barrier disruption, requiring prompt medical intervention, which boosts the demand for effective treatments. The segment sees strong adoption due to established pharmacological therapies such as corticosteroids that specifically target vasogenic swelling. Hospitals and neurology clinics often prioritize vasogenic edema treatments for their critical role in preventing neurological deterioration. Continuous R&D and clinical protocols further reinforce the preference for vasogenic-focused therapies. Increasing awareness among clinicians about early intervention benefits also contributes to the segment’s dominance.

The cytotoxic segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by the rising incidence of ischemic strokes and hypoxic injuries. Cytotoxic edema results from cellular swelling due to energy failure, requiring targeted treatment strategies such as osmotherapy and neuroprotective agents. Growth is supported by innovations in drugs that mitigate cell swelling and reduce secondary brain injury. Improved diagnostic capabilities allow early detection, increasing adoption in critical care units. Hospitals are incorporating cytotoxic-focused treatment protocols for better patient outcomes. In addition, the growing geriatric population prone to ischemic conditions supports rapid market expansion for cytotoxic edema management.

- By Treatment

On the basis of treatment, the cerebral edema treatment market is segmented into medication, osmotherapy, intravenous fluids, hyperventilation, hypothermia, surgery, ventriculostomy, and others. The medication segment dominated the market with the largest share of 46.1% in 2024, driven by the widespread use of corticosteroids, osmotic diuretics, and other neuroprotective drugs. Medications are often preferred due to their non-invasive nature, ease of administration, and proven efficacy in reducing brain swelling. Hospitals and neurology centers prioritize pharmacological intervention for early-stage edema management. The segment benefits from continuous development of new drugs and dosage formulations that improve patient safety and therapeutic outcomes. Medication-based therapies are also cost-effective compared to surgical alternatives in many clinical settings.

The surgery segment is expected to witness the fastest growth during the forecast period, fueled by increasing adoption of minimally invasive decompressive procedures and neuro-surgical interventions. Surgical treatments are critical in severe cases where intracranial pressure cannot be managed pharmacologically. Advancements in surgical techniques and robotics have improved precision, reduced recovery time, and enhanced patient survival rates. Rising availability of neurosurgical facilities in emerging markets is driving adoption. Hospitals and specialized clinics are expanding their surgical capabilities to accommodate increasing demand. Surgical intervention remains a key growth driver in severe cerebral edema cases.

- By Diagnosis

On the basis of diagnosis, the cerebral edema treatment market is segmented into computed tomography (CT) scan, magnetic resonance imaging (MRI), blood tests, lumbar puncture, physical exam, neurologic exam, and others. The CT scan segment dominated the market with the largest revenue share in 2024, driven by its rapid imaging capability, accessibility, and effectiveness in detecting cerebral swelling. CT scans are widely used in emergency and critical care settings for quick decision-making. Hospitals and clinics rely on CT imaging to assess the extent of edema and guide immediate treatment. The segment benefits from technological improvements that enhance image clarity and reduce radiation exposure. Routine use in trauma and stroke cases reinforces its dominance.

The MRI segment is anticipated to witness the fastest growth during the forecast period due to its superior imaging resolution, ability to detect early edema, and non-invasive nature. MRI is increasingly adopted for monitoring subtle brain changes in critical and post-operative patients. Rising availability of MRI scanners in emerging countries and hospitals supports faster adoption. MRI helps in personalized treatment planning, contributing to improved patient outcomes. Technological advancements such as functional MRI are further enhancing its application.

- By Dosage

On the basis of dosage, the cerebral edema treatment market is segmented into tablet, injection, and others. The injection segment dominated the market with the largest share in 2024, driven by the need for rapid drug delivery in acute cerebral edema cases. Intravenous or intramuscular injections allow immediate therapeutic effects, especially in emergency or ICU settings. Hospitals and emergency care units prefer injections for critically ill patients. The segment benefits from the development of novel injectable formulations with better bioavailability and reduced side effects. Continuous clinical adoption and inclusion in standard treatment protocols reinforce its dominance.

The tablet segment is expected to witness the fastest growth during the forecast period, fueled by increasing outpatient treatment and maintenance therapy for patients with chronic or post-surgical edema. Tablets offer convenience, ease of administration, and patient compliance for long-term care. Rising awareness among patients and physicians about home-based management supports growth. Pharmaceutical companies are innovating extended-release tablets to improve efficacy. Tablets are increasingly integrated into treatment plans for mild-to-moderate edema cases.

- By Route of Administration

On the basis of route of administration, the cerebral edema treatment market is segmented into oral, intravenous, and others. The intravenous segment dominated the market with the largest revenue share in 2024, driven by its efficacy in delivering rapid therapeutic effects in acute cerebral edema scenarios. Intravenous therapy is critical in ICU and emergency care settings for precise drug control. Hospitals prioritize IV administration for osmotic diuretics, corticosteroids, and other agents. The segment benefits from standardized clinical protocols supporting IV use. IV administration also allows combination therapy, improving patient outcomes.

The oral segment is anticipated to witness the fastest growth during the forecast period due to increasing adoption in outpatient care and chronic edema management. Oral medications provide convenience for home-based therapy and post-discharge management. Rising patient preference for non-invasive treatment supports market expansion. Pharmaceutical innovations in orally bioavailable drugs enhance efficacy. Oral administration is increasingly incorporated in long-term care strategies for mild-to-moderate edema patients.

- By Symptoms

On the basis of symptoms, the cerebral edema treatment market is segmented into seizures, vomiting, nausea, memory problems, vision loss, dizziness, neck pain, difficulty speaking, difficulty moving, headache, loss of consciousness, and others. The headache segment dominated the market with the largest revenue share in 2024, driven by its high prevalence as an initial and ongoing symptom of cerebral edema. Headache severity often correlates with intracranial pressure, prompting timely treatment. Hospitals and clinics prioritize patients reporting persistent headaches for immediate diagnostic evaluation. The segment benefits from established treatment protocols targeting symptom relief and edema reduction. Clinical awareness about headache as a critical indicator reinforces its dominance.

The seizures segment is expected to witness the fastest growth during the forecast period due to rising incidence in patients with trauma-induced or tumor-associated edema. Seizure management often requires integrated pharmacological and critical care approaches. Hospitals and neurology centers are increasingly adopting seizure-focused treatment strategies. Advanced monitoring and anti-epileptic therapies support faster recovery. Seizures also drive early diagnosis, increasing adoption of cerebral edema management solutions.

- By End-Users

On the basis of end-users, the cerebral edema treatment market is segmented into clinic, hospital, and others. The hospital segment dominated the market with the largest revenue share in 2024, driven by the high patient inflow, availability of specialized neurology units, and intensive care facilities. Hospitals handle both acute and chronic cerebral edema cases, necessitating advanced treatment solutions. The segment benefits from technological adoption, such as AI-assisted monitoring and minimally invasive interventions. Hospitals prioritize rapid intervention strategies and protocol-driven care. Continuous medical staff training and infrastructure investments reinforce market dominance.

The clinic segment is anticipated to witness the fastest growth during the forecast period due to increasing outpatient care adoption and accessibility in urban and semi-urban regions. Clinics provide early-stage treatment, follow-ups, and maintenance therapy for cerebral edema patients. Rising awareness and preventive neurology programs support clinic growth. Clinics increasingly adopt portable diagnostic and treatment tools. Growing patient preference for localized care enhances segment expansion.

- By Distribution Channel

On the basis of distribution channel, the cerebral edema treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2024, driven by the critical nature of cerebral edema requiring immediate access to medications and emergency supplies. Hospital pharmacies ensure availability of essential drugs and therapeutic agents at the point of care. The segment benefits from streamlined hospital procurement systems and integration with treatment protocols. Continuous supply chain support reinforces market dominance. Hospitals prefer in-house pharmacy access to reduce treatment delays.

The online pharmacy segment is expected to witness the fastest growth during the forecast period, fueled by rising e-pharmacy adoption, convenience, and home delivery services. Online pharmacies provide access to medications for post-discharge patients or those in remote locations. Increasing internet penetration and smartphone usage support this growth. Digital platforms also allow subscription-based delivery of chronic medications. Patients benefit from cost-effectiveness and accessibility, enhancing online pharmacy adoption.

Cerebral Edema Treatment Market Regional Analysis

- North America dominated the cerebral edema treatment market with the largest revenue share of 39.2% in 2024, characterized by early adoption of advanced treatment methods, high healthcare spending, and a strong presence of key industry players

- Healthcare providers and hospitals in the region prioritize early intervention and advanced monitoring, including AI-assisted neuro-monitoring, minimally invasive surgical procedures, and pharmacological therapies, to improve patient outcomes

- This widespread adoption is further supported by high healthcare expenditure, advanced neurology care facilities, and continuous R&D by key players, establishing cerebral edema treatments as a preferred solution in both hospital and specialized neurology clinic settings

U.S. Cerebral Edema Treatment Market Insight

The U.S. cerebral edema treatment market captured the largest revenue share of 82% in 2024 within North America, fueled by the rising incidence of neurological disorders such as stroke, traumatic brain injury, and brain tumors. Hospitals and specialized neurology centers are increasingly prioritizing early intervention using pharmacological therapies, minimally invasive surgeries, and AI-assisted monitoring. The growing preference for advanced treatment protocols, combined with the integration of cutting-edge diagnostic tools such as MRI and CT scans, further propels the cerebral edema treatment industry. Moreover, continuous R&D efforts by key players and government support for neuro-critical care infrastructure are significantly contributing to the market's expansion.

Europe Cerebral Edema Treatment Market Insight

The Europe cerebral edema treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of neurological health, stringent healthcare regulations, and the rising prevalence of brain injuries. The increase in hospital infrastructure and advanced neuro-care facilities is fostering the adoption of cerebral edema treatments. European clinicians are also drawn to the convenience and efficacy of modern pharmacological and minimally invasive surgical interventions. The region is witnessing significant growth across hospitals and specialty neurology clinics, with treatments being incorporated into both acute care and post-surgical rehabilitation programs.

U.K. Cerebral Edema Treatment Market Insight

The U.K. cerebral edema treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing neurological disorder incidence and a desire for advanced patient care and monitoring. In addition, concerns regarding stroke and traumatic brain injury outcomes are encouraging hospitals and neurology centers to adopt key treatment solutions such as osmotherapy, surgical decompression, and neuro-monitoring systems. The U.K.’s robust healthcare infrastructure and adoption of innovative medical technologies are expected to continue stimulating market growth.

Germany Cerebral Edema Treatment Market Insight

The Germany cerebral edema treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of brain health, investment in advanced healthcare technologies, and the demand for precision medical interventions. Germany’s well-developed hospital and neurology care infrastructure, combined with its emphasis on innovation and clinical research, promotes the adoption of pharmacological and surgical treatment options. Integration of AI-assisted monitoring and minimally invasive procedures is becoming increasingly prevalent, with a strong preference for reliable, high-quality care aligning with local healthcare standards.

Asia-Pacific Cerebral Edema Treatment Market Insight

The Asia-Pacific cerebral edema treatment market is poised to grow at the fastest CAGR of 23% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region's growing focus on neuro-critical care, supported by government initiatives promoting advanced healthcare infrastructure, is driving the adoption of cerebral edema treatments. Furthermore, as APAC emerges as a hub for advanced medical devices and pharmacological therapies, affordability and accessibility of cerebral edema treatment solutions are expanding to a wider patient base.

Japan Cerebral Edema Treatment Market Insight

The Japan cerebral edema treatment market is gaining momentum due to the country’s high-quality healthcare system, rapid urbanization, and focus on patient-centric care. The Japanese market places significant emphasis on neurological health, and the adoption of advanced treatment solutions is driven by an increasing number of hospitals and neuro-critical care units. Integration of AI-assisted monitoring, minimally invasive procedures, and advanced pharmacological therapies is fueling growth. Moreover, Japan's aging population is such asly to spur demand for easier-to-administer and effective treatment solutions in both hospital and clinic settings.

India Cerebral Edema Treatment Market Insight

The India cerebral edema treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country's expanding healthcare infrastructure, increasing incidence of neurological disorders, and high rates of technological adoption. India stands as one of the largest markets for neuro-critical care, and cerebral edema treatments are becoming increasingly popular in hospitals, specialty clinics, and post-surgical care centers. The push towards smart hospitals, increasing access to advanced diagnostic tools, and availability of cost-effective treatment options, alongside strong domestic and international healthcare providers, are key factors propelling the market in India.

Cerebral Edema Treatment Market Share

The cerebral edema treatment industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Abbott (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Bausch Health Companies Inc. (Canada)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Sun Pharmaceutical Industries Ltd. (India)

- Sumitomo Dainippon Pharma Co., Ltd. (Japan)

- Merck KGaA (Germany)

- Cipla Limited (India)

- Glenmark Pharmaceuticals Limited (India)

- Aurobindo Pharma Limited (India)

- Lupin (India)

- Lilly USA, LLC (U.S.)

- LEO Pharma A/S (Denmark)

- Bayer AG (Germany)

What are the Recent Developments in Global Cerebral Edema Treatment Market?

- In August 2025, researchers at Yale University, in collaboration with the National Institutes of Health (NIH), initiated a Phase III clinical trial to evaluate the efficacy of intravenous glyburide in treating cerebral edema following large hemispheric stroke. This trial builds upon previous studies and aims to provide a potential new therapeutic option for managing brain swelling in stroke patients

- In March 2025, the ReFlow External Ventricular Drain (EVD) device received FDA breakthrough device designation. This innovative device is the first of its kind to incorporate a noninvasive, manual flushing mechanism that helps restore and maintain cerebrospinal fluid (CSF) flow, a critical aspect in managing elevated intracranial pressure associated with cerebral edema

- In January 2024, A randomized, double-blind, placebo-controlled trial has been initiated to explore the safety and effectiveness of high-dose glibenclamide in treating cerebral edema after aneurysmal subarachnoid hemorrhage. Initial findings indicate promising results

- In November 2023, Researchers have identified a combination of existing antihypertensive drugs that rapidly reduce brain swelling and improve recovery outcomes in animal models of brain injury. This approach offers a potential new avenue for treating cerebral edema without the need for new drug development

- In November 2023, A study has evaluated the efficacy of CEREBO, a non-invasive, machine learning-powered near-infrared spectroscopy (mNIRS) device, in detecting cerebral edema. The device shows potential for early and accurate identification of brain swelling

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.