Global Cerumenolytic Agents Market

Market Size in USD Million

USD

68.65 Million

USD

106.96 Million

2025

2033

USD

68.65 Million

USD

106.96 Million

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 68.65 Million |

Market Size (Forecast Year) |

USD 106.96 Million |

CAGR |

% |

Major Markets Players |

|

Cerumenolytic Agents Market Size

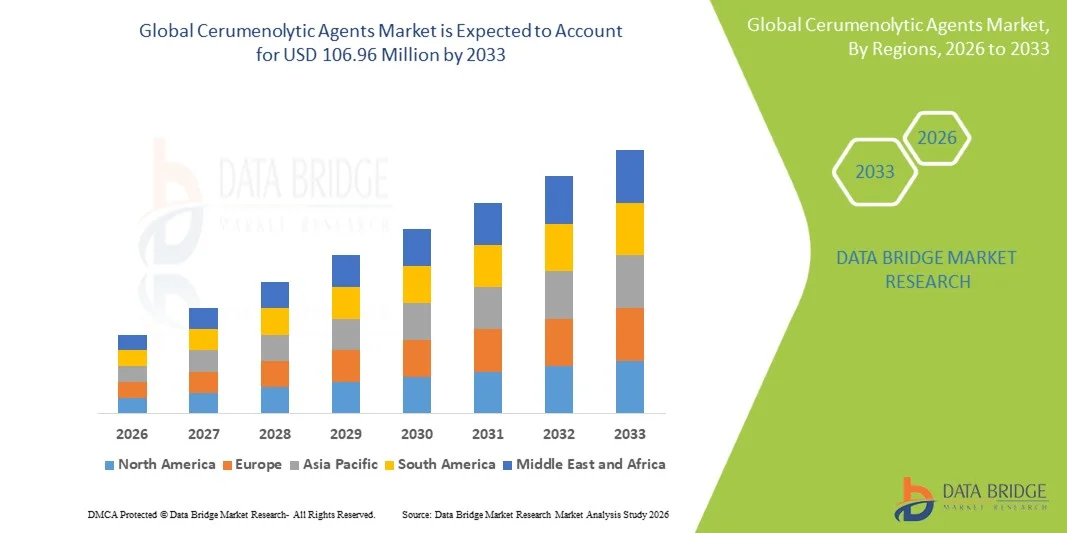

- The global Cerumenolytic Agents market size was valued at USD 68.65 million in 2025 and is expected to reach USD 106.96 million by 2033, at a CAGR of 5.70% during the forecast period

- The market growth is primarily driven by the increasing prevalence of earwax impaction and related hearing complications, along with rising awareness regarding ear hygiene and preventive ENT care, contributing to higher adoption of cerumen removal solutions in clinical and homecare settings

- Furthermore, growing demand for safe, effective, and easy-to-administer ear care products, coupled with advancements in formulation technologies such as oil-based, water-based, and surfactant-based agents, is strengthening product availability and patient compliance, thereby significantly supporting market expansion

Cerumenolytic Agents Market Analysis

- Cerumenolytic agents, used for softening and dissolving earwax to facilitate safe removal, are important therapeutic and preventive ENT products across hospitals, specialty clinics, and homecare settings, with formulations including Debrox and others, based on chemical classes such as urea compounds and hydrogen peroxide, and available in gel and solution dosage forms administered primarily via topical and oral routes

- The escalating demand for cerumenolytic agents is primarily driven by the rising prevalence of cerumen impaction, increasing geriatric population prone to earwax accumulation, and growing preference for non-invasive, easy-to-use topical treatments supported by expanding self-care and OTC healthcare trends

- North America dominated the cerumenolytic agents market with the largest revenue share of 38.6% in 2025, supported by high awareness of ear health, strong ENT care infrastructure, widespread OTC availability of products such as Debrox, and high adoption across hospitals and homecare settings, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the cerumenolytic agents market during the forecast period due to improving healthcare access, rising disposable incomes, increasing awareness of ear hygiene, and expanding availability of affordable ear care formulations in both urban and semi-urban populations

- The topical segment dominated the cerumenolytic agents market with a significant market share of 72.4% in 2025, driven by its direct effectiveness in earwax dissolution, ease of application, high patient compliance, and widespread use of gel and solution-based formulations in both clinical and homecare environments

Report Scope and Cerumenolytic Agents Market Segmentation

|

Attributes |

Cerumenolytic Agents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cerumenolytic Agents Market Trends

“Growing Shift Toward Advanced OTC Ear Care Formulations”

- A significant and accelerating trend in the global cerumenolytic agents market is the increasing shift toward advanced over-the-counter (OTC) ear care formulations such as fast-acting gels and stabilized hydrogen peroxide-based solutions that enhance efficacy and patient comfort in cerumen removal

- For instance, widely used products such as Debrox utilize carbamide peroxide-based formulations that safely break down earwax, enabling effective at-home treatment without the need for clinical intervention

- Advancements in formulation science are enabling improved safety profiles with reduced irritation risk and enhanced penetration efficiency, while newer gel-based systems provide prolonged contact time for better cerumen softening and removal effectiveness

- Furthermore, the growing availability of user-friendly applicators, single-dose packaging formats, and preservative-free variants is improving ease of use, safety, and hygiene compliance, particularly in homecare settings where self-administration is increasingly preferred

- Additionally, rising product diversification by manufacturers into sensitive-ear and pediatric-friendly formulations is expanding the consumer base and improving adoption among vulnerable patient groups

- This trend toward more effective, convenient, and patient-friendly cerumenolytic solutions is reshaping consumer expectations in ear health management, with companies focusing on improving tolerability and rapid action formulations such as hydrogen peroxide and urea compound blends

- The demand for advanced OTC cerumenolytic agents is growing rapidly across both developed and emerging markets, as consumers increasingly prioritize safe, accessible, and non-invasive earwax management solutions

Cerumenolytic Agents Market Dynamics

Driver

“Rising Prevalence of Cerumen Impaction and Growing Self-Care Adoption”

- The increasing prevalence of cerumen impaction and related hearing discomfort, coupled with the accelerating adoption of self-care and OTC healthcare practices, is a significant driver for the heightened demand for cerumenolytic agents globally

- For instance, the rising use of OTC products such as carbamide peroxide-based ear drops in homecare settings reflects growing consumer preference for non-invasive and easily accessible earwax management solutions

- As awareness of ear hygiene and preventive ENT care increases, cerumenolytic agents are becoming a first-line approach for managing mild to moderate earwax buildup without the need for clinical procedures

- Furthermore, the expanding aging population, which is more prone to earwax accumulation and hearing-related issues, is significantly contributing to higher product utilization across hospitals and homecare environments

- The convenience of topical application, combined with the availability of widely accessible OTC brands and improved healthcare awareness campaigns, is strongly propelling market adoption in both developed and emerging economies

- Additionally, increasing penetration of e-commerce and pharmacy retail channels is improving accessibility of cerumenolytic products, further boosting consumer adoption rates

- Moreover, rising ENT consultations and preventive hearing screenings are encouraging early-stage treatment using cerumenolytic agents, reducing reliance on mechanical ear cleaning procedures

- The trend toward self-medication and home-based treatment is further reinforcing demand for safe and effective cerumenolytic formulations across global healthcare systems

Restraint/Challenge

“Limited Awareness and Risk of Improper Self-Administration Practices”

- Limited awareness regarding proper ear care practices and potential risks associated with improper self-administration of cerumenolytic agents pose a significant challenge to broader market penetration and safe usage outcomes

- For instance, misuse of hydrogen peroxide-based ear drops or excessive self-cleaning attempts can lead to ear canal irritation or potential damage, raising concerns among healthcare professionals

- The lack of standardized consumer education on correct dosage, frequency, and application methods often results in inconsistent treatment outcomes and reduced product effectiveness

- Furthermore, regulatory variations across regions regarding OTC ear care products can create barriers for manufacturers in ensuring uniform product labeling, approval, and distribution compliance

- The presence of low-cost, unregulated alternatives in certain markets can also impact consumer trust and limit adoption of clinically validated cerumenolytic formulations

- Additionally, limited physician recommendation in mild cases reduces early adoption of cerumenolytic agents, as many consumers rely on non-medical or traditional ear cleaning practices

- Moreover, concerns regarding potential contraindications in patients with perforated eardrums or chronic ear conditions further restrict widespread self-use without professional guidance

- Addressing these challenges through improved patient education, clearer usage guidelines, and stronger regulatory oversight will be essential for ensuring safe and sustained market growth

Cerumenolytic Agents Market Scope

The market is segmented on the basis of drug, chemical class, application, dosage, route of administration, end-users, and distribution channel.

- By Drug

On the basis of drug, the cerumenolytic agents market is segmented into Debrox and others. The Debrox segment dominated the market with the largest revenue share of 41.8% in 2025, driven by its strong brand recognition, widespread OTC availability, and proven efficacy in carbamide peroxide-based earwax removal. Consumers and healthcare providers often prefer Debrox due to its established clinical reliability and ease of use in homecare settings. Its strong retail penetration across pharmacies and online channels further reinforces its dominant position. Additionally, continuous marketing and trust built over years have made it a first-choice product for cerumen impaction management. The segment also benefits from high adoption in developed markets where self-care trends are strong.

The others segment is expected to witness the fastest growth rate of 8.9% from 2026 to 2033, fueled by increasing entry of generic and herbal-based cerumenolytic formulations. Rising demand for cost-effective alternatives in emerging markets is accelerating adoption of non-branded products. Furthermore, innovation in natural oil-based and preservative-free formulations is expanding consumer interest. Growing awareness of chemical sensitivity is also encouraging users to explore alternative drug options beyond traditional brands.

- By Chemical Class

On the basis of chemical class, the market is segmented into urea compounds and hydrogen peroxide. The hydrogen peroxide segment dominated the market with the largest revenue share of 57.3% in 2025, driven by its strong cerumen-busting efficacy through oxygen release that helps break down hardened earwax. It is widely used in OTC products due to its fast-acting nature and cost-effectiveness. Hydrogen peroxide-based formulations are commonly recommended in mild to moderate cerumen impaction cases. Its broad availability in both branded and generic ear drops further supports dominance. Additionally, long-standing clinical familiarity with this compound strengthens physician and consumer confidence.

The urea compound segment is expected to witness the fastest growth rate of 9.4% from 2026 to 2033, driven by its gentle action and suitability for sensitive ear conditions. Urea-based formulations provide controlled softening of cerumen, reducing irritation risks compared to stronger oxidizing agents. Increasing preference for safer, pediatric-friendly, and geriatric-safe ear care solutions is boosting adoption. Furthermore, advancements in stabilized urea peroxide formulations are improving product effectiveness and shelf life.

- By Application

On the basis of application, the market is segmented into cerumen impaction and others. The cerumen impaction segment dominated the market with the largest revenue share of 78.6% in 2025, driven by the high global prevalence of earwax blockage leading to hearing discomfort and ENT consultations. It remains the primary medical indication for cerumenolytic agents across hospitals and homecare use. Growing awareness of untreated earwax-related hearing loss is increasing product adoption. Additionally, aging populations are significantly contributing to higher incidence rates. The segment benefits from strong clinical guidelines recommending non-invasive earwax removal as first-line therapy.

The others segment is expected to witness the fastest growth rate of 7.8% from 2026 to 2033, driven by increasing use of cerumenolytics for preventive ear hygiene and pre-procedural ear cleaning. Rising awareness of routine ear care in pediatric and occupational health settings is expanding usage beyond impaction cases. Additionally, growing adoption in audiology and hearing aid preparation procedures is supporting demand. Preventive healthcare trends are accelerating this segment’s expansion.

- By Dosage

On the basis of dosage, the market is segmented into gel and solution. The solution segment dominated the market with the largest revenue share of 64.1% in 2025, driven by its easy administration, rapid dispersion in the ear canal, and strong compatibility with hydrogen peroxide-based formulations. Liquid solutions are widely preferred in OTC products due to fast cerumen softening action. They are also more cost-effective and widely available across pharmacies. High consumer familiarity with drop-based application further supports dominance. Additionally, solutions are commonly recommended by healthcare professionals for initial treatment.

The gel segment is expected to witness the fastest growth rate of 10.2% from 2026 to 2033, driven by its longer retention time in the ear canal, improving contact with hardened wax. Gel formulations reduce leakage and enhance targeted action, making them suitable for sensitive users. Increasing demand for improved comfort and reduced irritation is boosting adoption. Furthermore, innovation in bioadhesive gel systems is enhancing product effectiveness and patient compliance. Improved stability and extended action duration further strengthen this segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and topical. The topical segment dominated the market with the largest revenue share of 72.4% in 2025, driven by its direct action on earwax and high safety profile compared to systemic alternatives. Topical drops and gels are the standard treatment method for cerumen removal. They allow localized treatment without systemic side effects. Strong OTC availability and ease of self-administration further reinforce dominance. Additionally, clinical guidelines strongly favor topical cerumenolytics as first-line therapy.

The oral segment is expected to witness the fastest growth rate of 6.5% from 2026 to 2033, driven by limited but emerging use in adjunct ear hygiene therapies and systemic conditions affecting earwax production. Research into oral mucolytic agents and supportive therapies is gradually expanding this segment. However, growth remains niche due to lower direct effectiveness compared to topical agents. Ongoing pharmaceutical research may enhance its future role. Growth is primarily driven by experimental and supportive therapeutic use.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, homecare, and others. The homecare segment dominated the market with the largest revenue share of 49.7% in 2025, driven by increasing preference for self-care, OTC availability, and convenience of at-home earwax management. Consumers prefer non-invasive treatment without clinical visits for mild cerumen impaction. Rising awareness of ear hygiene and easy access to pharmacy products further supports dominance. Additionally, aging populations increasingly rely on home-based care solutions. Strong e-commerce penetration is also accelerating product adoption.

The specialty clinics segment is expected to witness the fastest growth rate of 9.1% from 2026 to 2033, driven by increasing ENT consultations and rising demand for professional ear cleaning procedures. Clinics are increasingly adopting cerumenolytic agents as pre-treatment before mechanical removal or audiology assessments. Growth is also supported by rising hearing aid usage requiring professional ear canal preparation. Expansion of ENT infrastructure in emerging markets further accelerates this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The retail pharmacy segment dominated the market with the largest revenue share of 46.8% in 2025, driven by strong OTC product availability and high consumer reliance on pharmacist recommendations for ear care solutions. Retail pharmacies serve as the primary access point for cerumenolytic agents, especially in urban and semi-urban regions. Easy product visibility and immediate purchase convenience further strengthen dominance. Additionally, trusted pharmacist guidance enhances consumer confidence in product selection.

The online pharmacy segment is expected to witness the fastest growth rate of 11.3% from 2026 to 2033, driven by increasing digital health adoption and rising e-commerce penetration for OTC healthcare products. Consumers prefer online platforms for discreet purchasing, wider product variety, and doorstep delivery. Additionally, discounts and subscription models are encouraging repeat purchases. Growing smartphone penetration and telehealth integration are further accelerating this segment’s expansion.

Cerumenolytic Agents Market Regional Analysis

- North America dominated the cerumenolytic agents market with the largest revenue share of 38.6% in 2025, supported by high awareness of ear health, strong ENT care infrastructure, widespread OTC availability of products such as Debrox, and high adoption across hospitals and homecare settings, particularly in the U.S.

- Consumers in the region highly value the accessibility, clinical reliability, and ease of use offered by cerumenolytic agents such as Debrox and hydrogen peroxide-based solutions, which are widely available across retail and online pharmacies

- This widespread adoption is further supported by a large aging population prone to cerumen impaction, high healthcare expenditure, and strong preference for non-invasive home-based ear care solutions, establishing cerumenolytic agents as a standard OTC treatment option for earwax management

U.S. Cerumenolytic Agents Market Insight

The U.S. cerumenolytic agents market captured the largest revenue share of 81% in North America in 2025, driven by strong consumer awareness of ear hygiene and high adoption of OTC healthcare products. The country benefits from widespread availability of leading brands such as Debrox across retail and online pharmacies. Consumers increasingly prefer self-care and home-based earwax removal solutions supported by easy-to-use formulations. High prevalence of age-related cerumen impaction further strengthens demand. Additionally, strong healthcare spending and frequent ENT consultations contribute to sustained market growth.

Europe Cerumenolytic Agents Market Insight

The Europe cerumenolytic agents market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by rising awareness of ear hygiene and increasing adoption of preventive ENT care. The region benefits from well-structured healthcare systems and strong pharmacy networks that facilitate easy access to OTC ear care products. Consumers in Europe are increasingly inclined toward safe, non-invasive, and clinically tested formulations for cerumen removal. Additionally, growing geriatric population and higher incidence of hearing-related issues are supporting demand. The market is also witnessing rising adoption across hospitals and specialty clinics, particularly in urban healthcare centers.

U.K. Cerumenolytic Agents Market Insight

The U.K. cerumenolytic agents market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing awareness of ear health and rising preference for self-care-based treatment options. Concerns related to hearing loss and earwax buildup are encouraging consumers to adopt OTC cerumenolytic solutions. The presence of a strong pharmacy retail network and expanding online healthcare platforms is further supporting market accessibility. Additionally, growing ENT consultations and preventive ear care practices are boosting product demand. Rising aging population in the country is also contributing significantly to market expansion.

Germany Cerumenolytic Agents Market Insight

The Germany cerumenolytic agents market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing focus on preventive healthcare and demand for clinically effective ear care solutions. Germany’s strong pharmaceutical infrastructure and high healthcare standards support the adoption of safe and tested cerumenolytic formulations. Consumers show strong preference for hydrogen peroxide and urea-based products due to their effectiveness and safety profile. Additionally, rising awareness of ear hygiene among aging populations is driving demand. Integration of OTC ear care solutions into pharmacy recommendations further strengthens market growth.

Asia-Pacific Cerumenolytic Agents Market Insight

The Asia-Pacific cerumenolytic agents market is poised to grow at the fastest CAGR of 9.8% during the forecast period of 2026 to 2033, driven by rising healthcare awareness, increasing disposable incomes, and growing prevalence of ear-related disorders. The region is witnessing rapid adoption of OTC healthcare products supported by expanding retail pharmacy and e-commerce channels. Government initiatives promoting healthcare access and awareness are further encouraging market growth. Additionally, large aging populations in countries such as China and Japan are increasing demand for earwax management solutions. Improving healthcare infrastructure is also enabling wider availability of cerumenolytic products.

Japan Cerumenolytic Agents Market Insight

The Japan cerumenolytic agents market is gaining momentum due to the country’s aging population, strong healthcare system, and high awareness of preventive ear care. Demand is driven by increasing prevalence of cerumen impaction among elderly individuals requiring safe and effective earwax removal solutions. Consumers prefer clinically tested and gentle formulations such as hydrogen peroxide-based products. Additionally, widespread pharmacy accessibility and physician recommendations support market adoption. The integration of OTC cerumenolytic agents into routine ear care practices is further boosting growth.

India Cerumenolytic Agents Market Insight

The India cerumenolytic agents market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expanding middle-class population, and increasing awareness of personal hygiene. The country is witnessing strong adoption of OTC ear care products in both urban and semi-urban regions. Growing availability of affordable cerumenolytic formulations through retail and online pharmacies is supporting market penetration. Additionally, rising healthcare awareness campaigns and increasing ENT consultations are driving demand. The expansion of domestic pharmaceutical manufacturing is further enhancing product accessibility and affordability.

Cerumenolytic Agents Market Share

The Cerumenolytic Agents industry is primarily led by well-established companies, including:

- Prestige Consumer Healthcare Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Bayer AG (Germany)

- Haleon plc (U.K.)

- Reckitt Benckiser Group plc (U.K.)

- Medline Industries, LP (U.S.)

- Perrigo Company plc (Ireland)

- Viatris Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Limited (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Novartis AG (Switzerland)

- Sanofi (France)

- Bausch Health (Canada)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Church & Dwight Co., Inc. (U.S.)

- Similasan AG (Switzerland)

What are the Recent Developments in Global Cerumenolytic Agents Market?

- In December 2025, updated ENT clinical guidance reinforced water-based cerumenolytic agents such as hydrogen peroxide, saline, and sodium bicarbonate as primary treatment options for earwax impaction. Medical recommendations increasingly support non-invasive chemical dissolution methods before irrigation or manual removal

- In November 2025, Debrox (carbamide peroxide 6.5%) updated its OTC drug labeling and product packaging information under FDA OTC drug monograph compliance updates. The update reinforced its classification as a standard earwax removal aid for cerumen impaction management, maintaining its OTC accessibility in the U.S. market

- In October 2025, comparative clinical studies published in ENT journals highlighted ongoing evaluation of sodium bicarbonate and carbamide peroxide as leading cerumenolytic agents. Research demonstrated measurable differences in wax clearance efficiency among commonly used formulations

- In June 2024, medical safety advisories from ENT-focused publications emphasized proper controlled use of OTC hydrogen peroxide ear drops due to irritation risks and misuse concerns. Authorities highlighted that improper concentrations or overuse can lead to ear canal irritation or discomfort

- In March 2024, clinical development studies evaluated carbamide peroxide (Debrox-type formulations) against alternative cerumenolytics for improved wax dissolution efficiency. Research confirmed carbamide peroxide as a highly effective cerumen-softening agent with strong degradation performance compared to other topical agents

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.