Global Cholesterol Management Devices Market

Market Size in USD Billion

USD

3.55 Billion

USD

6.62 Billion

2025

2033

USD

3.55 Billion

USD

6.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.55 Billion | |

| USD 6.62 Billion | |

| % | |

|

Cholesterol Management Devices Market Size

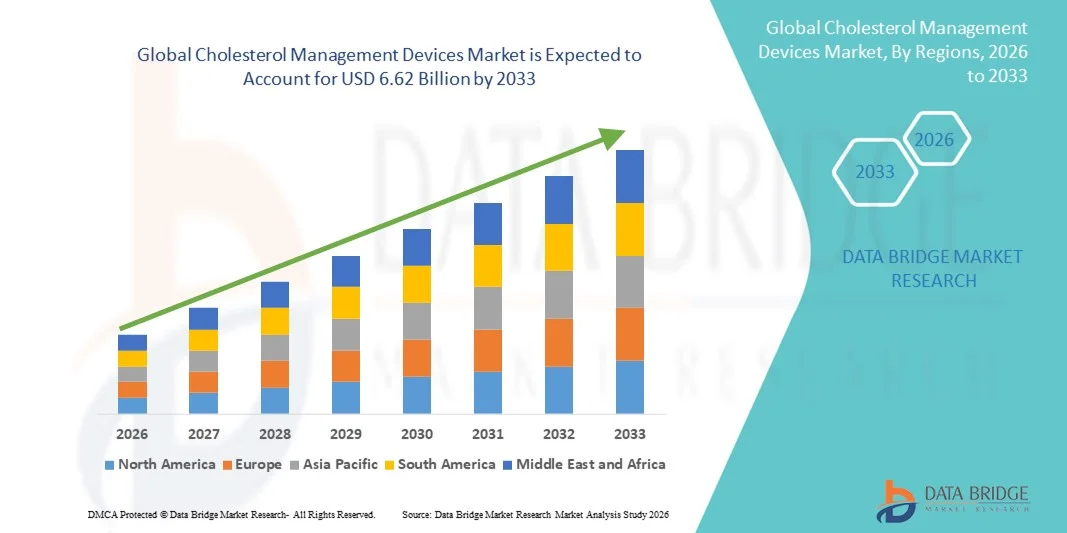

- The global cholesterol management devices market size was valued at USD 3.55 billion in 2025 and is expected to reach USD 6.62 billion by 2033, at a CAGR of 8.12% during the forecast period

- The market growth is largely fueled by increasing prevalence of cardiovascular diseases, rising health awareness, and technological advancements in diagnostic and monitoring solutions that empower proactive management of cholesterol levels across clinical and home settings

- Furthermore, growing demand for user‑friendly, portable, and connected cholesterol monitoring devices, combined with expanding preventive healthcare adoption and integration with digital health platforms, is propelling market uptake and establishing cholesterol management solutions as essential tools for both patients and healthcare providers

Cholesterol Management Devices Market Analysis

- Cholesterol management devices, including monitors, wrist monitors, small portable instruments, meters, and wireless systems, are becoming essential in preventive cardiovascular healthcare, enabling real-time monitoring and management of cholesterol levels for both clinical and home settings

- The rising demand for cholesterol management devices is primarily driven by the increasing prevalence of hypercholesterolemia, growing health awareness, and a preference for convenient, at-home or clinic-based testing solutions that support proactive management of cardiovascular risks

- North America dominated the cholesterol management devices market with the largest revenue share of 38.9% in 2025, owing to early adoption of advanced digital health technologies, high healthcare spending, and the presence of major players offering innovative connected and user-friendly cholesterol monitoring solutions

- Asia-Pacific is expected to be the fastest growing region during the forecast period due to rising prevalence of cholesterol-related disorders, expanding preventive healthcare initiatives, increasing disposable incomes, and government programs promoting cardiovascular health

- Monitors segment dominated the market with a share of 42.4% in 2025, driven by its accuracy, ease of use, and suitability for both home healthcare and clinical applications

Report Scope and Cholesterol Management Devices Market Segmentation

|

Attributes |

Cholesterol Management Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cholesterol Management Devices Market Trends

Advancement Through Connected and Portable Monitoring Devices

- A significant and accelerating trend in the global cholesterol management devices market is the integration of connected monitoring solutions, portable meters, and wireless systems that allow real-time tracking of cholesterol levels and seamless data sharing with healthcare providers

- For instance, the CardioChek Plus system offers wireless connectivity to smartphones and cloud-based platforms, enabling patients to track lipid profiles and receive automated feedback for preventive care

- Connected devices allow features such as trend analysis, personalized alerts for abnormal readings, and integration with digital health platforms to support long-term disease management. For instance, some LipidPro monitors can sync results with telemedicine apps, enabling clinicians to remotely adjust treatments based on patient data

- The combination of portability, connectivity, and real-time monitoring facilitates easier adherence to prescribed treatment plans, empowering users to proactively manage cholesterol alongside other cardiovascular risk factors

- This trend towards more intelligent, convenient, and connected cholesterol monitoring systems is reshaping patient expectations for preventive healthcare. Consequently, companies such as Roche and Abbott are developing wireless and portable cholesterol monitoring devices that integrate with health management apps

- The demand for connected and portable cholesterol management devices is growing rapidly across both home healthcare and clinical sectors, as patients increasingly prioritize continuous monitoring, convenience, and remote care options

- Partnerships between device manufacturers and telehealth platforms are creating opportunities for remote patient monitoring programs, enabling proactive clinical interventions and personalized care plans

Cholesterol Management Devices Market Dynamics

Driver

Rising Cardiovascular Disease Prevalence and Health Awareness

- The increasing incidence of hypercholesterolemia and cardiovascular diseases, coupled with rising awareness about preventive healthcare, is a major driver for the growing demand for cholesterol management devices

- For instance, in March 2025, Abbott launched a portable cholesterol testing device aimed at home healthcare users, highlighting the importance of early detection and ongoing monitoring for cardiovascular risk management

- As patients become more proactive in managing their health, devices offering real-time cholesterol monitoring, trend analysis, and automated alerts provide a compelling advantage over traditional laboratory testing alone

- Furthermore, the rising adoption of home healthcare solutions and digital health platforms makes portable and connected cholesterol monitors increasingly integral to patient care, enabling clinicians and patients to collaborate effectively

- Convenience of self-testing, real-time feedback, and remote access to clinical guidance are key factors propelling adoption, while expanding availability of user-friendly monitoring devices further supports market growth

- Government initiatives promoting preventive healthcare and early detection of cardiovascular diseases are boosting demand for cholesterol monitoring solutions in both developed and emerging markets

- Increasing integration of cholesterol management devices with health insurance and wellness programs incentivizes regular monitoring, driving adoption among health-conscious consumers

Restraint/Challenge

Accuracy Concerns and Regulatory Compliance Hurdles

- Concerns regarding the accuracy and reliability of portable cholesterol management devices pose significant challenges to broader market adoption, as patients and clinicians rely on precise readings for effective treatment

- For instance, reports of inconsistent results in some low-cost portable meters have made certain consumers hesitant to adopt home-based cholesterol monitoring solutions

- Ensuring compliance with regulatory standards, such as FDA or CE approvals, is crucial to building trust among patients and healthcare providers, and companies must continually validate device accuracy. For instance, Roche and CardioChek emphasize regulatory certification and clinical validation in their marketing to reassure users

- In addition, relatively high costs of advanced portable and wireless devices can be a barrier for price-sensitive consumers or emerging markets, despite affordability improvements in basic devices

- Overcoming these challenges through enhanced clinical validation, consumer education on proper testing procedures, and development of cost-effective yet accurate monitoring solutions will be vital for sustained market growth

- Limited awareness and training among some users on proper device usage can result in inaccurate readings and reduced confidence in home-based cholesterol monitoring solutions

- Data privacy and cybersecurity concerns related to cloud-connected devices can hinder adoption, as consumers and healthcare providers seek secure storage and transmission of sensitive health information

Cholesterol Management Devices Market Scope

The market is segmented on the basis of type, application, and end users.

- By Type

On the basis of type, the cholesterol management devices market is segmented into monitors, wrist monitors, small portable instruments, meters, and wireless systems. The monitors segment dominated the market with the largest revenue share of 42.4% in 2025, driven by their widespread adoption in hospitals, clinics, and diagnostic laboratories for routine cholesterol screening and lipid profile assessment. These devices are preferred due to their high accuracy, clinical validation, and ability to provide comprehensive cholesterol readings. Healthcare professionals rely heavily on monitors for diagnosing hypercholesterolemia and monitoring treatment effectiveness. Their integration into established clinical workflows and compatibility with laboratory information systems further support dominance. In addition, rising cardiovascular disease prevalence has increased routine cholesterol testing volumes in clinical settings. Strong trust among physicians and regulatory approvals continue to reinforce the segment’s leading position.

The wireless systems segment is expected to witness the fastest growth rate during the forecast period, fueled by increasing adoption of digital health and remote patient monitoring solutions. Wireless cholesterol management devices enable seamless data transmission to smartphones, cloud platforms, and telehealth systems. These systems support continuous monitoring and long-term disease management, particularly for high-risk patients. Growing demand for home-based testing and real-time health tracking significantly contributes to rapid adoption. Integration with mobile applications allows personalized insights, reminders, and physician access. Advancements in connectivity and data analytics are further accelerating growth across both developed and emerging markets.

- By Application

On the basis of application, the cholesterol management devices market is segmented into hypercholesterolemia, hypocholesterolemia, and cholesterol testing. The hypercholesterolemia segment dominated the market in 2025, driven by the high global prevalence of elevated cholesterol levels and its strong association with cardiovascular diseases. Hypercholesterolemia is a major risk factor for heart attacks and strokes, leading to widespread screening and monitoring initiatives. Patients diagnosed with high cholesterol require frequent testing to evaluate treatment response and lifestyle interventions. This drives consistent demand for cholesterol management devices across clinical and home settings. Increasing awareness campaigns and preventive healthcare programs further support dominance. Long-term disease management needs make this application segment the largest revenue contributor.

The cholesterol testing segment is projected to grow at the fastest pace during the forecast period, supported by rising emphasis on early diagnosis and preventive healthcare. Growing health-conscious populations are opting for routine cholesterol testing even without diagnosed conditions. Home testing kits and portable devices are encouraging frequent self-monitoring. Employers and insurance providers are increasingly promoting regular cholesterol screening as part of wellness programs. Technological advancements have improved ease of use and affordability of testing devices. These factors collectively drive rapid expansion of the cholesterol testing application segment.

- By End Users

On the basis of end users, the cholesterol management devices market is segmented into home healthcare, hospitals, and clinics. The hospitals segment held the largest market revenue share in 2025, owing to high patient volumes and the central role hospitals play in cardiovascular diagnosis and treatment. Hospitals conduct large-scale cholesterol screenings as part of routine health checkups and emergency care. Availability of skilled healthcare professionals and advanced diagnostic infrastructure supports extensive use of cholesterol monitoring devices. Hospital-based testing is often preferred for its reliability and comprehensive lipid profiling. Integration with electronic medical records enhances data accuracy and continuity of care. These factors collectively contribute to hospitals’ dominance in the market.

The home healthcare segment is expected to register the fastest growth during the forecast period, driven by rising adoption of self-monitoring and remote care solutions. Patients increasingly prefer managing cholesterol levels at home to reduce hospital visits and associated costs. Portable and wireless devices enable convenient, frequent testing with minimal technical expertise. Growth in elderly populations and chronic disease prevalence further supports demand. Telemedicine expansion allows clinicians to remotely track patient data from home devices. This shift toward decentralized healthcare delivery is accelerating growth of the home healthcare end-user segment.

Cholesterol Management Devices Market Regional Analysis

- North America dominated the cholesterol management devices market with the largest revenue share of 38.9% in 2025, owing to early adoption of advanced digital health technologies, high healthcare spending, and the presence of major players offering innovative connected and user-friendly cholesterol monitoring solutions

- Patients and healthcare providers in the region place significant value on accurate, rapid, and user-friendly cholesterol monitoring solutions that support both clinical diagnostics and home-based health management

- This widespread adoption is further supported by high healthcare expenditure, favorable reimbursement frameworks, a technologically advanced healthcare ecosystem, and growing acceptance of home healthcare and remote patient monitoring solutions, positioning cholesterol management devices as essential tools across hospitals, clinics, and home settings

U.S. Cholesterol Management Devices Market Insight

The U.S. cholesterol management devices market captured the largest revenue share within North America in 2025, driven by the high prevalence of cardiovascular diseases and strong emphasis on preventive healthcare. Consumers and healthcare providers increasingly prioritize early detection and continuous monitoring of cholesterol levels to reduce long-term health risks. The growing adoption of home healthcare solutions, supported by advanced portable and wireless monitoring devices, further propels market growth. Moreover, strong healthcare infrastructure, favorable reimbursement policies, and widespread awareness of cholesterol-related risks significantly contribute to market expansion.

Europe Cholesterol Management Devices Market Insight

The Europe cholesterol management devices market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by rising cardiovascular disease burden and strong preventive healthcare frameworks. Increasing aging population and lifestyle-related health risks are fostering demand for regular cholesterol screening across the region. European consumers and healthcare systems value accurate, clinically validated devices for both hospital and home use. Growth is evident across public healthcare systems and private diagnostics, with increasing adoption of portable and digital cholesterol monitoring solutions in routine care.

U.K. Cholesterol Management Devices Market Insight

The U.K. cholesterol management devices market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by national health initiatives promoting cardiovascular risk assessment and early diagnosis. Rising awareness of hypercholesterolemia and preventive screening programs are encouraging regular cholesterol testing. The expansion of home healthcare and self-monitoring solutions is also supporting demand. In addition, strong primary care networks and increasing use of digital health tools are expected to continue stimulating market growth in the U.K.

Germany Cholesterol Management Devices Market Insight

The Germany cholesterol management devices market is expected to expand at a considerable CAGR during the forecast period, fueled by a well-established healthcare system and high focus on chronic disease management. Germany’s emphasis on precision diagnostics and evidence-based medical devices supports adoption of advanced cholesterol monitoring solutions. Increasing preventive screening among aging populations and patients with cardiovascular risks is driving demand. The market also benefits from strong regulatory standards and high acceptance of clinically validated medical technologies across hospitals and clinics.

Asia-Pacific Cholesterol Management Devices Market Insight

The Asia-Pacific cholesterol management devices market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapidly rising incidence of lifestyle-related diseases and expanding healthcare access. Urbanization, changing dietary habits, and increasing awareness of cardiovascular health are boosting demand for cholesterol monitoring devices. Governments across the region are promoting preventive healthcare and early disease detection, supporting market expansion. In addition, increasing affordability and availability of portable devices are accelerating adoption across both urban and semi-urban populations.

Japan Cholesterol Management Devices Market Insight

The Japan cholesterol management devices market is gaining momentum due to the country’s aging population and strong focus on preventive healthcare. Regular cholesterol monitoring is widely encouraged to manage age-related cardiovascular risks. The Japanese healthcare system places high value on accuracy and reliability, supporting adoption of advanced monitoring devices. Integration of cholesterol management with broader health monitoring systems is also contributing to growth. Furthermore, demand for convenient and easy-to-use devices is increasing among elderly patients and home healthcare users.

India Cholesterol Management Devices Market Insight

The India cholesterol management devices market accounted for a significant revenue share in Asia Pacific in 2025, driven by rising prevalence of cardiovascular diseases and increasing health awareness. Rapid urbanization, lifestyle changes, and growing middle-class populations are increasing demand for regular cholesterol testing. Expansion of private healthcare facilities and diagnostic centers supports market growth. In addition, growing adoption of affordable portable devices and rising emphasis on preventive health checkups are key factors propelling the market in India.

Cholesterol Management Devices Market Share

The Cholesterol Management Devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- ACON Laboratories, Inc. (U.S.)

- PTS Diagnostics (U.S.)

- Randox Laboratories Ltd. (U.K.)

- Nova Biomedical (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Arkray, Inc. (Japan)

- Trinity Biotech plc (Ireland)

- EKF Diagnostics Holdings plc (U.K.)

- Bioptik Technology Inc. (Taiwan)

- PocDoc Ltd (U.K.)

- Menarini Diagnostics (Italy)

- DiaSys Diagnostic Systems GmbH (Germany)

- Human Diagnostics Worldwide (Germany)

- Wiener lab. Group (Argentina)

- Microlife Corporation (Switzerland)

What are the Recent Developments in Global Cholesterol Management Devices Market?

- In July 2025, the U.S. Food and Drug Administration (FDA) approved a label update for Novartis’ inclisiran (Leqvio) allowing its use as a first-line monotherapy to lower LDL-C (bad cholesterol) in adults with hypercholesterolemia alongside diet and exercise, expanding its role in cholesterol management

- In April 2025, an Indian research team developed a novel eco-friendly cholesterol detection sensor using dual optical and electrical sensing, capable of trace-level detection and designed for point-of-care monitoring without electronic waste, marking innovation in cholesterol monitoring technology

- In January 2025, Roche Diagnostics announced that its Tina-quant® Lipoprotein (a) Gen.2 Molarity assay received 510(k) clearance from the U.S. Food and Drug Administration. This is the first FDA-cleared blood test in the U.S. that measures lipoprotein (a), an important cardiovascular risk biomarker, in nanomoles per liter, enabling clinicians to more precisely evaluate lipid metabolism disorders and assess cardiovascular risk

- In September 2024, the Family Heart Foundation launched “Cholesterol Connect®”, a program providing free at-home lipid screening test kits and personalized navigation support to increase awareness and early detection of elevated LDL-C and lipoprotein(a), enhancing reach of cholesterol monitoring outside clinical settings

- In May 2024, Roche Diagnostics’ Tina-quant® lipoprotein Lp(a) RxDx assay was granted Breakthrough Device Designation by the U.S. FDA, marking a regulatory milestone for advanced cholesterol risk stratification tools capable of guiding personalized therapy decisions for patients at elevated cardiovascular risk

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.