Global Chronic Granulomatous Disease Treatment Market

Market Size in USD Billion

USD

1.27 Billion

USD

1.77 Billion

2024

2032

USD

1.27 Billion

USD

1.77 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.27 Billion | |

| USD 1.77 Billion | |

| % | |

|

Chronic Granulomatous Disease Treatment Market Size

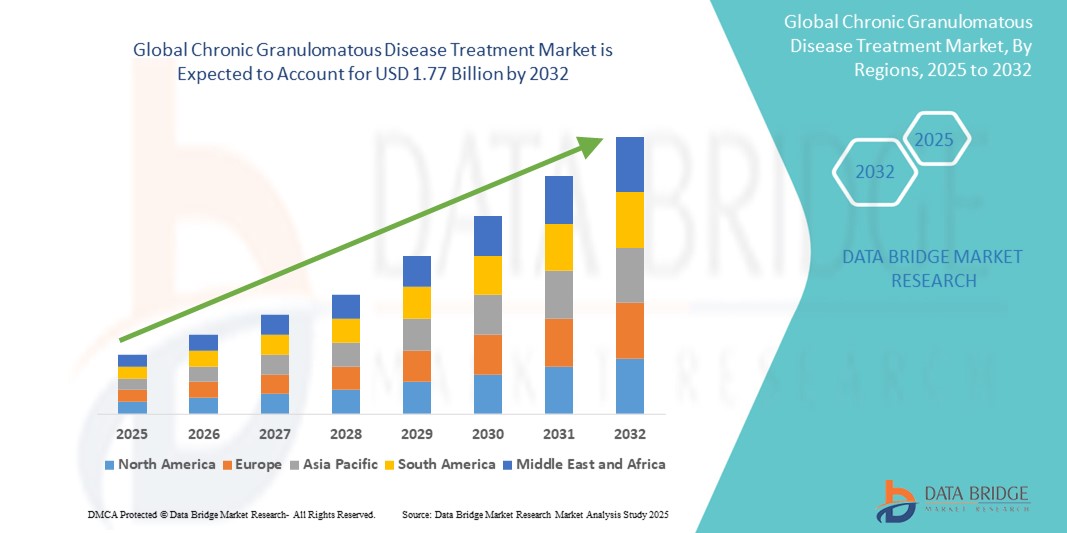

- The Global Chronic Granulomatous Disease Treatment Market size was valued at USD 1.27 billion in 2024 and is expected to reach USD 1.77 billion by 2032, at a CAGR of 4.20% during the forecast period

- The market growth is primarily driven by increasing awareness, early diagnosis, and rising prevalence of primary immunodeficiency disorders. Advances in genetic testing and a growing emphasis on personalized medicine are also enabling timely and targeted therapeutic interventions

- Moreover, expanding research in gene therapy, stem cell transplantation, and the development of advanced biologics are reshaping the treatment landscape. These innovations, coupled with improved diagnostic capabilities and access to specialized healthcare, are expected to accelerate the global demand for CGD treatment solutions, supporting steady market expansion over the coming years

Chronic Granulomatous Disease Treatment Market Analysis

- Chronic Granulomatous Disease (CGD) treatment comprises a range of therapies including infection management, stem cell transplantation, interferon-gamma, and emerging gene therapies, aimed at correcting immune deficiencies and reducing the frequency and severity of life-threatening infections. The increasing integration of advanced diagnostics and targeted therapies is enhancing patient outcomes and supporting long-term disease management.

- The growing demand for CGD treatment is primarily driven by rising awareness of primary immunodeficiency disorders, increasing availability of genetic and prenatal testing, and advancements in life-saving treatments such as bone marrow transplants and gene therapy innovations. In addition, global support for rare disease research and expanding access to specialty clinics are further boosting treatment uptake.

- North America dominates the CGD treatment market with the largest revenue share, projected at 42.3% in 2025, supported by early disease diagnosis, advanced healthcare infrastructure, and the presence of leading research institutions focusing on immunodeficiency disorders. The U.S., in particular, is seeing an increase in clinical trials and FDA-approved therapies targeting rare genetic diseases like CGD.

- Asia-Pacific is expected to be the fastest-growing region in the CGD treatment market during the forecast period, driven by improving healthcare access, rising public-private investment in rare disease awareness, and a growing patient pool in countries such as China and India.

- The infection management segment is expected to lead the CGD treatment market with a market share of 35.6% in 2025, due to its critical role in immediate disease control and broad availability across healthcare settings. Meanwhile, gene therapy is gaining momentum as a transformative long-term solution, though still in the clinical development phase in many regions.

Report Scope and Chronic Granulomatous Disease Treatment Market Segmentation

|

Attributes |

Chronic Granulomatous Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Chronic Granulomatous Disease Treatment Market Trends

“Enhanced Convenience Through AI and Voice Integration”

- A significant and evolving trend in the global CGD treatment market is the advancement and growing adoption of gene therapy and personalized medicine. As CGD is a rare genetic immune disorder, the focus is shifting toward curative, gene-based approaches rather than symptom management alone. These advancements are enhancing long-term outcomes and offering hope for sustained disease remission or cure.

- For instance, Orchard Therapeutics and Généthon are pioneering gene therapy research targeting X-linked CGD, where a single administration can potentially correct the defective gene responsible for the disease. Early-phase clinical trials have demonstrated promising safety and efficacy results, with ongoing development aimed at regulatory approval and commercialization.

- Personalized medicine is gaining traction as a complementary trend, driven by improvements in genomic sequencing and diagnostic tools. With early genetic testing, clinicians can tailor treatment regimens based on disease subtype (e.g., X-linked or autosomal recessive), severity, and patient-specific response profiles.

- The integration of biomarkers and patient-specific immunological data into treatment decision-making is further accelerating individualized therapy approaches. Stem cell transplantation and interferon-gamma therapies are being optimized based on patient characteristics to minimize rejection and enhance effectiveness

- This trend towards targeted, precision therapies and curative gene treatments is transforming the CGD landscape from reactive care to proactive, patient-centric solutions. Companies like Bluebird Bio and MaxCyte are contributing to this shift by investing in next-generation gene-editing technologies and delivery systems tailored for rare immunodeficiencies like CGD

- The growing clinical and regulatory acceptance of gene therapy, combined with increasing funding for rare disease R&D, is expected to unlock new treatment avenues and reshape the CGD treatment paradigm over the next decade.

Chronic Granulomatous Disease Treatment Market Dynamics

Driver

“Increasing Awareness and Advancements in Rare Disease Diagnostics”

- The growing awareness about primary immunodeficiency disorders, combined with advances in diagnostic tools, is a major driver fueling the global CGD treatment market. Increased physician education, patient advocacy, and support programs are leading to earlier and more accurate diagnosis of CGD in children and young adults.

- For instance, government-supported newborn screening programs and access to advanced genetic testing have improved early detection rates in several countries, particularly in North America and Europe, enabling timely initiation of life-saving treatments such as antibiotic prophylaxis, stem cell transplants, and gene therapies.

- The rise of specialty clinics and tertiary care centers focused on rare diseases has further contributed to better patient management and treatment adherence. These facilities offer multidisciplinary care approaches, increasing the efficacy of complex interventions like bone marrow transplants.

- Moreover, collaborations between research institutions and biopharmaceutical companies are accelerating innovation pipelines, making CGD treatments more accessible and clinically effective. Organizations such as the Immune Deficiency Foundation (IDF) and NIH Rare Diseases Program have played pivotal roles in supporting education, funding, and patient registry development.

- As the general population becomes more informed about immune-related conditions, the demand for effective, long-term CGD treatment options is expected to rise steadily.

Restraint/Challenge

“High Cost and Limited Access to Advanced Therapies”

- One of the primary challenges in the CGD treatment market is the high cost of advanced therapies such as gene therapy, stem cell transplantation, and long-term biologic treatments. These interventions, though effective, require sophisticated healthcare infrastructure and substantial financial investment, limiting their accessibility in many regions.

- For instance, gene therapies currently under development or in early commercialization phases can cost upwards of USD 500,000 to USD 1 million per patient, posing reimbursement challenges for both public and private payers. Additionally, stem cell transplants involve intensive pre- and post-operative care, adding to the financial burden on families and healthcare systems.

- Limited access in low- and middle-income countries (LMICs) further compounds the problem. These regions often lack advanced diagnostic capabilities, donor registries for transplants, or clinical facilities for gene therapy administration, resulting in delayed or suboptimal care for CGD patients.

- Furthermore, the rarity of the disease makes it less commercially attractive for some pharmaceutical companies, leading to limited treatment availability and slower innovation cycles compared to more common conditions.

- Addressing these challenges will require policy reforms, global access initiatives, and cost-optimization strategies, including tiered pricing models and partnerships with health ministries or global health organizations. Without such interventions, disparities in treatment access will continue to hinder global market expansion.

Chronic Granulomatous Disease Treatment Market Scope

The market is segmented on the basis of type, diagnosis, treatment, route of administration, end user, and distribution channel.

- By Type

On the basis of type, the CGD treatment market is segmented into X-Linked Chronic Granulomatous Disease and Autosomal Recessive Chronic Granulomatous Disease. The X-Linked CGD segment dominates the market with the largest revenue share of 67.5% in 2025, attributed to its significantly higher prevalence compared to the autosomal recessive form. As the most common and severe variant, X-linked CGD typically presents early in childhood and demands continuous, intensive treatment, including prophylactic antimicrobials, interferon-gamma, and potentially curative options such as hematopoietic stem cell transplantation (HSCT) and gene therapy.

The Autosomal Recessive CGD segment is projected to record the fastest compound annual growth rate (CAGR) of 5.8% from 2025 to 2032, driven by growing global awareness, improved access to genetic diagnostics, and higher prevalence in regions with elevated consanguinity rates (e.g., parts of the Middle East, North Africa, and South Asia). These factors are leading to earlier diagnosis, improved clinical intervention, and expanded treatment availability in developing regions.

• By Diagnosis

On the basis of diagnosis, the market is segmented into Neutrophil Function Tests, Genetic Testing, Prenatal Testing, and Others. Neutrophil Function Tests accounted for the largest market revenue share in 2025 due to their foundational role in confirming the diagnosis of CGD by assessing the oxidative burst capability of neutrophils. These tests, such as the dihydrorhodamine (DHR) flow cytometry test, are routinely used in both developed and developing regions.

The Genetic Testing segment is expected to witness the fastest CAGR from 2025 to 2032, owing to the growing shift toward precision medicine and the availability of next-generation sequencing platforms. Genetic confirmation allows for subtype classification and informs family counseling and treatment planning, especially in high-income countries.

• By Treatment

On the basis of treatment, the market is segmented into Infection Management, Interferon-gamma, Stem Cell Transplantation, Medication, Bone Marrow Transplant, Gene Therapy, and Others. Infection Management held the largest revenue share in 2025, supported by its widespread use as a first-line approach to control the recurring bacterial and fungal infections that are hallmark symptoms of CGD. This includes long-term prophylactic use of antibiotics and antifungals to reduce infection-related morbidity.

Gene Therapy is projected to witness the fastest CAGR from 2025 to 2032, driven by the increasing number of clinical trials and potential for long-term curative outcomes. As a cutting-edge treatment targeting the root genetic cause of CGD, gene therapy is expected to significantly transform disease management in the future.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Injectable, and Others. The Oral segment dominated the market in 2025, supported by the widespread use of oral antibiotics and antifungal agents for prophylactic infection control. The ease of administration and high patient compliance further contribute to its large share.

The Injectable segment is anticipated to register the fastest growth from 2025 to 2032, driven by the use of interferon-gamma injections, stem cell infusions, and gene therapy delivery platforms. Injectable routes offer systemic efficacy and are integral to advanced treatment protocols in moderate to severe CGD cases.

• By End User

On the basis of end user, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. Hospitals accounted for the largest market share in 2025, due to their central role in CGD diagnosis, treatment administration, and post-transplant care. Hospitals serve as the hub for multidisciplinary management including immunologists, hematologists, and genetic counselors.

Specialty Clinics are projected to grow at the fastest CAGR from 2025 to 2032, supported by increasing investments in rare disease centers and personalized treatment setups. These clinics often provide focused and long-term care, enhancing outcomes and patient quality of life.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, Retail Pharmacy, and Others. Hospital Pharmacies dominated the market in 2025, attributed to their direct role in supplying specialized medications such as interferon-gamma, injectable antibiotics, and gene-modifying therapies administered in inpatient or outpatient hospital settings.

Online Pharmacies are expected to witness the fastest CAGR from 2025 to 2032, due to the growing digitalization of healthcare, improved access to chronic medications, and expanding e-prescription infrastructure. This channel is particularly beneficial for patients managing CGD from home under long-term infection control regimens.

Chronic Granulomatous Disease Treatment Market Regional Analysis

- North America dominates the CGD treatment market with the largest revenue share of 42.3% in 2024, driven by early disease diagnosis, robust healthcare infrastructure, and the availability of advanced therapeutic options such as stem cell transplantation and gene therapy.

- Patients in the region benefit from greater access to immunology specialists, comprehensive insurance coverage, and specialized rare disease centers, which support consistent monitoring and tailored treatment plans for CGD.

- The market is further supported by significant investments in clinical research, widespread use of genetic testing, and the presence of leading pharmaceutical companies focused on rare diseases. These factors collectively contribute to North America’s leadership in the CGD treatment space, particularly in the U.S., where awareness and early intervention continue to improve patient outcomes.

U.S. Chronic Granulomatous Disease (CGD) Treatment Market Insight

The U.S. CGD treatment market captured the largest revenue share of over 78% within North America in 2025, driven by early diagnosis, advanced treatment availability, and strong healthcare infrastructure. The presence of established rare disease centers, access to cutting-edge gene therapies and bone marrow transplants, and robust insurance coverage contribute significantly to market growth. Ongoing clinical trials, increased newborn screening programs, and patient advocacy groups such as the Immune Deficiency Foundation are further propelling awareness and treatment adoption across the country.

Europe Chronic Granulomatous Disease (CGD) Treatment Market Insight

The European CGD treatment market is projected to grow at a steady CAGR during the forecast period, supported by improved genetic screening programs, public healthcare funding, and access to advanced therapeutic protocols. Countries such as Germany, France, and the U.K. are investing in rare disease research and enhancing diagnostic capabilities, leading to earlier detection and intervention. The growing collaboration between research institutes and pharmaceutical companies is also strengthening the treatment pipeline across Europe, especially in pediatric immunology.

U.K. Chronic Granulomatous Disease (CGD) Treatment Market Insight

The U.K. CGD treatment market is expected to expand at a noteworthy CAGR, driven by the NHS’s emphasis on rare disease management and genetic testing. Increased funding for gene therapy research and improved access to tertiary care hospitals are enabling timely intervention for CGD patients. The U.K.'s active involvement in European and global rare disease registries enhances data collection and personalized treatment approaches, fostering improved clinical outcomes and long-term disease control.

Germany Chronic Granulomatous Disease (CGD) Treatment Market Insight

The German CGD treatment market is anticipated to grow at a considerable CAGR, supported by strong investment in biotechnology and academic research institutions focused on immunodeficiencies. Germany’s advanced diagnostic laboratories, early adoption of innovative therapies, and comprehensive health insurance policies facilitate access to stem cell transplantation and biologics. Additionally, the country’s structured approach to rare disease management promotes multidisciplinary treatment strategies for CGD.

Asia-Pacific Chronic Granulomatous Disease (CGD) Treatment Market Insight

The Asia-Pacific CGD treatment market is expected to grow at the fastest CAGR of over 6.4% in 2025, fueled by rising awareness of primary immunodeficiencies, expanding diagnostic infrastructure, and improving access to healthcare. Countries such as China, Japan, and India are witnessing increased adoption of genetic testing and infection management protocols. Regional government initiatives and international collaborations are helping build rare disease registries and training immunologists to meet the growing patient demand.

Japan Chronic Granulomatous Disease (CGD) Treatment Market Insight

The Japan CGD treatment market is gaining momentum due to the nation’s advanced medical technology, early disease detection capabilities, and public health initiatives supporting rare disease patients. High penetration of genetic testing and the availability of specialty care centers are contributing to increased treatment rates. Japan’s aging yet tech-savvy population and universal healthcare coverage provide a strong platform for the adoption of both conventional and advanced CGD therapies, including clinical trials for gene therapy.

China Chronic Granulomatous Disease (CGD) Treatment Market Insight

The China CGD treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by increased investment in healthcare infrastructure, government-backed rare disease programs, and growing access to genetic diagnostics. China’s strong domestic pharmaceutical manufacturing capabilities and participation in international clinical research are accelerating the availability of stem cell therapy and other advanced treatments. Public-private partnerships are also expanding access to essential CGD medications and improving overall disease management across major urban centers.

Chronic Granulomatous Disease Treatment Market Share

The Chronic Granulomatous Disease Treatment industry is primarily led by well-established companies, including:

- Clinigen Group plc (U.K.)

- Orchard Therapeutics plc (U.K.)

- Généthon (France)

- Horizon Therapeutics plc (U.S.)

- ViroMed Co., Ltd (South Korea)

- Bellicum Pharmaceuticals, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Lonza (Switzerland)

- GlaxoSmithKline plc (U.K.)

- Eli Lilly and Company (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Merck KGaA (Germany)

- Smith & Nephew (U.K.)

- JCR Pharmaceuticals Co., Ltd (Japan)

- MaxCyte, Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Sun Pharmaceutical Industries Ltd. (India)

- Antares Pharma (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.