Global Chronic Pancreatitis Treatment Market

Market Size in USD Billion

USD

4.96 Billion

USD

8.52 Billion

2024

2032

USD

4.96 Billion

USD

8.52 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.96 Billion | |

| USD 8.52 Billion | |

| % | |

|

Chronic Pancreatitis Treatment Market Size

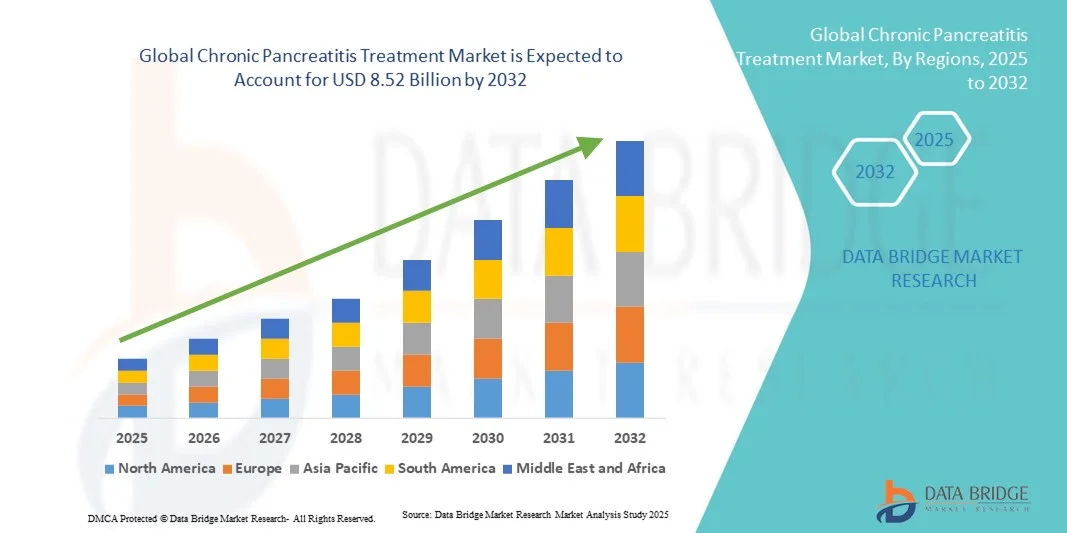

- The global chronic pancreatitis treatment market size was valued at USD 4.96 billion in 2024 and is expected to reach USD 8.52 billion by 2032, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic pancreatitis, advancements in treatment options such as enzyme replacement therapy, pain management medications, and surgical interventions, as well as improved diagnostic techniques and growing awareness about the disease

- Furthermore, rising demand for effective, safe, and patient-friendly treatment solutions in both hospitals and specialized clinics is establishing chronic pancreatitis therapies as essential in modern gastroenterology care. These converging factors are accelerating the adoption of advanced treatment approaches, thereby significantly boosting the industry's growth

Chronic Pancreatitis Treatment Market Analysis

- Chronic pancreatitis treatments, including pain-relieving medications, intravenous (IV) fluids, surgery, endoscopy, and other therapeutic interventions, are increasingly vital components of modern gastroenterology care in both hospitals and specialized clinics due to their effectiveness in managing symptoms, preventing complications, and improving patient quality of life

- The escalating demand for chronic pancreatitis treatments is primarily fueled by the rising prevalence of the disease, growing awareness among patients and healthcare providers, and advancements in minimally invasive procedures, personalized therapy approaches, and improved diagnostic techniques

- North America dominated the chronic pancreatitis treatment market with the largest revenue share of 38.3% in 2024, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key pharmaceutical and medical device companies, with the U.S. experiencing substantial growth in adoption of advanced treatment options, particularly in specialized gastroenterology centers

- Asia-Pacific is expected to be the fastest growing region in the chronic pancreatitis treatment market during the forecast period due to increasing healthcare expenditure, expanding medical facilities, and growing awareness about disease management

- Pain-relieving medications segment dominated the chronic pancreatitis treatment market with a market share of 42.2% in 2024, driven by their established efficacy in managing abdominal pain, improving patient comfort, and supporting overall treatment adherence

Report Scope and Chronic Pancreatitis Treatment Market Segmentation

|

Attributes |

Chronic Pancreatitis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Chronic Pancreatitis Treatment Market Trends

Advancements in Minimally Invasive and Personalized Therapies

- A significant and accelerating trend in the global chronic pancreatitis treatment market is the increasing adoption of minimally invasive procedures and personalized therapies tailored to patient-specific disease profiles. This approach is significantly enhancing treatment efficacy and patient comfort

- For instance, endoscopic ultrasound-guided drainage allows targeted intervention for pancreatic duct obstructions, reducing recovery time compared to conventional surgery. Similarly, personalized enzyme replacement therapy dosages improve nutrient absorption for individual patient needs

- Integration of digital health tools, such as treatment monitoring apps and AI-assisted symptom tracking, enables healthcare providers to adjust therapy plans dynamically, providing more precise management of chronic pancreatitis symptoms

- These advanced therapies facilitate better coordination between gastroenterologists, nutritionists, and pain management specialists, creating a comprehensive care pathway for patients

- This trend towards minimally invasive, personalized, and digitally supported treatment strategies is fundamentally reshaping patient expectations for chronic pancreatitis care. Consequently, companies such as Nestlé Health Science are developing targeted enzyme formulations and therapy monitoring solutions for improved patient outcomes

- The demand for advanced, patient-centric chronic pancreatitis treatment solutions is growing rapidly across both hospitals and specialized clinics, as healthcare providers increasingly prioritize efficacy and quality of life improvements

Chronic Pancreatitis Treatment Market Dynamics

Driver

Rising Disease Prevalence and Awareness Among Healthcare Providers

- The increasing prevalence of chronic pancreatitis worldwide, coupled with growing awareness among healthcare providers, is a significant driver for the heightened demand for advanced treatment solutions

- For instance, in 2024, major gastroenterology centers in North America reported rising enrollment in chronic pancreatitis management programs, focusing on early diagnosis and integrated care plans. Such initiatives by key healthcare institutions are expected to drive market growth in the forecast period

- As more patients are diagnosed earlier, treatment options such as pain management, enzyme replacement, and endoscopic interventions become essential, offering improved patient outcomes

- Furthermore, the growing knowledge of disease progression and complications is making comprehensive chronic pancreatitis care an integral component of modern gastroenterology, improving adoption of innovative therapies

- The availability of convenient therapy options, combination treatment plans, and patient education programs are key factors propelling adoption in both hospitals and specialized clinics. The trend towards multidisciplinary care models and integration of digital monitoring tools further contributes to market expansion

Restraint/Challenge

Limited Awareness, Underdiagnosis, and High Treatment Costs

- Concerns surrounding underdiagnosis, limited awareness among patients, and relatively high costs of advanced therapies pose a significant challenge to broader market penetration. As treatments involve specialized procedures and enzyme formulations, many patients face barriers to accessing appropriate care

- For instance, reports from Asia-Pacific healthcare surveys indicate delayed diagnosis of chronic pancreatitis due to lack of symptom recognition, leading to progression before treatment initiation

- Addressing these challenges through patient education, earlier diagnostic programs, and insurance coverage improvements is crucial for increasing access. Companies such as AbbVie and Takeda emphasize affordability programs and outreach initiatives in their strategies to reassure potential patients

- In addition, the complexity of managing diverse symptoms and tailoring therapies to individual needs can hinder standardization of treatment approaches, limiting broader adoption

- Overcoming these challenges through awareness campaigns, improved diagnostic access, and cost-effective therapy options will be vital for sustained market growth

Chronic Pancreatitis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the chronic pancreatitis market is segmented into pain-relieving medications, intravenous (IV) fluids, surgery, endoscopy, and others. The pain-relieving medications segment dominated the market with the largest revenue of 42.2% share in 2024, driven by their established efficacy in managing abdominal pain and enhancing patient comfort. Pain-relieving therapies are widely prescribed across hospitals and clinics due to their ability to improve patient adherence and quality of life. The segment benefits from advancements in targeted analgesics and combination therapies that reduce side effects. Furthermore, growing awareness among healthcare providers about symptom management in chronic pancreatitis reinforces adoption. Pain-relieving medications also see high demand because they form the first-line treatment for most diagnosed patients. Integration with personalized treatment plans has further strengthened their market position.

The endoscopy segment is anticipated to witness the fastest growth rate from 2025 to 2031, fueled by increasing preference for minimally invasive procedures. Endoscopic interventions offer effective management of pancreatic duct obstructions and pseudocysts with reduced recovery times compared to traditional surgery. The adoption of advanced imaging and guidance techniques improves procedural accuracy and patient outcomes. Hospitals and specialized clinics increasingly adopt endoscopic solutions as part of integrated care models. In addition, endoscopy reduces hospitalization duration, lowering overall treatment costs. The procedure’s growing popularity in emerging regions also contributes to its rapid market expansion.

- By Diagnosis

On the basis of diagnosis, the chronic pancreatitis market is segmented into blood tests, abdominal ultrasound, computerized tomography (CT) scan, magnetic resonance imaging (MRI), endoscopic ultrasound, and stool tests. The CT scan segment dominated the market with the largest revenue share in 2024 due to its widespread availability and effectiveness in detecting structural pancreatic abnormalities. CT scans are preferred for evaluating disease severity, complications, and guiding therapeutic decisions. Radiologists and gastroenterologists often rely on CT imaging for its high resolution and detailed visualization. The method is compatible with both inpatient and outpatient diagnostic workflows. High adoption rates in North America and Europe further support market dominance. Continuous technological advancements, such as low-dose CT, enhance diagnostic accuracy while minimizing radiation exposure.

The endoscopic ultrasound segment is expected to witness the fastest growth rate during the forecast period due to its minimally invasive nature and ability to combine diagnostic imaging with therapeutic interventions. Endoscopic ultrasound provides detailed imaging of pancreatic tissue and ducts, enabling early detection and accurate staging. Its dual diagnostic-therapeutic capability reduces the need for multiple procedures. Increasing availability in tertiary hospitals and specialized gastroenterology centers drives adoption. Endoscopic ultrasound is also preferred for patients unsuitable for traditional imaging methods. Rising clinician awareness and training programs further accelerate market penetration.

- By Symptoms

On the basis of symptoms, the chronic pancreatitis market is segmented into abdominal pain, vomiting, nausea, weight loss, oily or fatty stools, diarrhea, and others. The abdominal pain segment dominated the market with the largest share in 2024, as pain is the most common and debilitating symptom of chronic pancreatitis. Effective pain management remains a priority for clinicians, driving prescription of analgesics and integrated treatment plans. Chronic pain significantly impacts patient quality of life, prompting repeated clinical visits and continuous treatment. Hospitals and outpatient centers emphasize comprehensive pain monitoring protocols. Pain severity guides therapy selection, influencing treatment intensity and follow-up care. Increasing patient awareness regarding symptom management supports continued dominance of this segment.

The weight loss segment is anticipated to witness the fastest growth rate during the forecast period due to increasing recognition of malnutrition and exocrine pancreatic insufficiency in patients. Treatment strategies targeting nutritional support, enzyme replacement therapy, and dietary interventions are gaining traction. Weight monitoring and management are becoming standard in chronic pancreatitis care pathways. Clinicians are emphasizing early intervention to prevent severe complications. Awareness campaigns and clinical guidelines promote patient adherence to nutritional plans. Growth is particularly strong in emerging markets where malnutrition is prevalent.

- By Dosage

On the basis of dosage, the chronic pancreatitis market is segmented into tablet, injection, and others. The tablet segment dominated the market with the largest revenue share in 2024 due to ease of administration, patient compliance, and widespread prescription of oral therapies. Tablets are commonly used for both pain-relieving medications and enzyme replacement therapy. Their convenience supports outpatient treatment and home care management. Pharmaceutical companies continue to innovate formulations to improve bioavailability and reduce gastrointestinal side effects. Patient familiarity and affordability further strengthen this segment. Tablets also integrate easily into personalized care regimens.

The injection segment is expected to witness the fastest growth rate during the forecast period due to increasing use of injectable analgesics and supportive therapies for severe acute episodes. Injectable formulations offer rapid symptom relief, which is critical in hospital or emergency settings. Adoption is growing in specialized gastroenterology centers for patients unresponsive to oral medications. Technological improvements in delivery systems enhance patient safety and ease of administration. The segment benefits from rising hospital-based treatment volume. Training programs for clinicians on injection protocols further accelerate adoption.

- By Route of Administration

On the basis of route of administration, the chronic pancreatitis market is segmented into oral, intravenous, and others. The oral segment dominated the market with the largest share in 2024, driven by convenience, patient adherence, and compatibility with outpatient care. Oral administration is common for pain medications and enzyme replacement therapy. Widespread patient acceptance and lower administration costs support dominance. Hospitals and clinics favor oral therapy as a primary treatment for mild to moderate symptoms. Integration with personalized therapy plans further strengthens its market position. Continuous formulation improvements enhance efficacy and tolerability.

The intravenous segment is expected to witness the fastest growth rate during the forecast period, as IV fluids and injectable medications are critical in hospital settings for severe cases or acute exacerbations. IV administration allows rapid symptom relief and hydration management. Adoption is increasing in inpatient care and emergency interventions. Healthcare providers rely on IV routes for precise dosing and immediate therapeutic effect. Growth is supported by increasing hospital admissions and acute case management. Training and protocol standardization enhance the safe use of intravenous therapies.

- By End-Users

On the basis of end-users, the chronic pancreatitis market is segmented into clinics, hospitals, and others. The hospital segment dominated the market with the largest revenue share in 2024, due to the availability of advanced treatment options, specialized gastroenterology units, and integration of multidisciplinary care. Hospitals provide comprehensive management including diagnostics, medications, endoscopy, and surgery. High patient volumes and access to advanced therapies reinforce dominance. Continuous investment in infrastructure and skilled staff further supports the segment. Hospitals often serve as referral centers, strengthening market share. Coordination between departments ensures optimal patient outcomes.

The clinic segment is expected to witness the fastest growth rate during the forecast period, driven by increasing outpatient care, specialized gastroenterology practices, and early-stage symptom management. Clinics offer convenient access for patients and support long-term monitoring and therapy adherence. Growth is accelerated by telemedicine integration and home-based care support. Clinics also provide personalized nutritional counseling and follow-up for chronic pancreatitis patients. Expansion in urban and semi-urban areas further fuels adoption. Patient education programs and preventive care strategies enhance clinic utilization.

- By Distribution Channel

On the basis of distribution channel, the chronic pancreatitis market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2024, as hospitals dispense most prescribed medications, enzyme therapies, and supportive care products directly to inpatients. This ensures timely access, adherence to physician prescriptions, and monitoring of therapy. Hospital pharmacies are preferred for complex treatment regimens requiring close clinical supervision. Institutional procurement contracts strengthen dominance. Integration with hospital information systems streamlines dispensing and inventory management. Continuous collaboration with clinicians enhances patient satisfaction and outcomes.

The online pharmacy segment is expected to witness the fastest growth rate during the forecast period due to increasing e-commerce adoption, convenience of home delivery, and availability of subscription-based medication services. Patients can access enzyme replacement therapies, pain medications, and nutritional supplements without visiting hospitals or retail outlets. Online platforms offer cost comparisons, repeat order management, and educational resources. Growth is particularly strong in urban areas with high internet penetration. Telemedicine integration supports online pharmacy utilization for prescription fulfillment. Convenience and accessibility drive accelerated adoption.

Chronic Pancreatitis Treatment Market Regional Analysis

- North America dominated the chronic pancreatitis treatment market with the largest revenue share of 38.3% in 2024, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key pharmaceutical and medical device companies

- Patients and healthcare providers in the region highly value effective pain management, enzyme replacement therapies, and minimally invasive interventions, which improve patient outcomes and quality of life

- This widespread adoption is further supported by advanced healthcare infrastructure, high awareness among clinicians, well-established diagnostic facilities, and strong reimbursement policies, establishing North America as a key market for chronic pancreatitis treatments

U.S. Chronic Pancreatitis Treatment Market Insight

The U.S. chronic pancreatitis treatment market captured the largest revenue share of 82% in North America in 2024, fueled by the rising prevalence of chronic pancreatitis and the expanding adoption of advanced treatment options. Patients and healthcare providers are increasingly prioritizing effective pain management, enzyme replacement therapy, and minimally invasive procedures. The growing trend of early diagnosis programs, along with integration of digital health tools for monitoring symptoms and treatment adherence, further propels market growth. Moreover, well-established healthcare infrastructure and strong reimbursement policies are significantly contributing to the market's expansion.

Europe Chronic Pancreatitis Treatment Market Insight

The Europe chronic pancreatitis treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing disease awareness and stringent healthcare regulations. The rise in specialized gastroenterology centers, coupled with growing adoption of advanced therapies, is fostering market growth. European patients are also drawn to treatment options that enhance quality of life and reduce hospital stays. The region is witnessing significant uptake across hospitals, clinics, and outpatient care settings, with therapies being incorporated into both standard care protocols and preventive management programs.

U.K. Chronic Pancreatitis Treatment Market Insight

The U.K. chronic pancreatitis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing prevalence of chronic pancreatitis and a rising emphasis on patient-centered care. In addition, concerns regarding symptom management, nutritional deficiencies, and complications are encouraging both hospitals and clinics to adopt comprehensive treatment strategies. The U.K.’s robust healthcare system and growing use of telemedicine platforms are expected to continue to stimulate market growth.

Germany Chronic Pancreatitis Treatment Market Insight

The Germany chronic pancreatitis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of pancreatic diseases and demand for technologically advanced diagnostic and therapeutic solutions. Germany’s well-developed healthcare infrastructure, emphasis on early diagnosis, and adoption of minimally invasive procedures promote the uptake of chronic pancreatitis treatments. Integration of digital monitoring tools and personalized therapy plans is also becoming increasingly prevalent, aligning with local patient expectations for effective disease management.

Asia-Pacific Chronic Pancreatitis Treatment Market Insight

The Asia-Pacific chronic pancreatitis treatment market is poised to grow at the fastest CAGR of 25% during 2025–2031, driven by increasing prevalence of chronic pancreatitis, rising healthcare expenditure, and expansion of specialized gastroenterology facilities in countries such as China, Japan, and India. The region's growing awareness of early diagnosis, along with government initiatives to improve healthcare access, is driving treatment adoption. Furthermore, increasing availability of advanced therapies and affordable options is expanding accessibility to a wider patient base.

Japan Chronic Pancreatitis Treatment Market Insight

The Japan chronic pancreatitis treatment market is gaining momentum due to high disease awareness, an aging population, and increasing demand for minimally invasive procedures. The market places significant emphasis on early detection and management of complications, with adoption driven by hospitals and specialized gastroenterology centers. Integration of digital monitoring and symptom tracking tools with treatment regimens is fueling growth. Moreover, Japan’s focus on patient-centric care is expected to spur demand for comprehensive chronic pancreatitis management solutions.

India Chronic Pancreatitis Treatment Market Insight

The India chronic pancreatitis treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare infrastructure, increasing prevalence of chronic pancreatitis, and rising awareness among patients. India is witnessing growing adoption of advanced treatments, including enzyme replacement therapy, pain management medications, and endoscopic interventions, in hospitals and clinics. Government initiatives promoting healthcare access and affordability, alongside rising urbanization, are key factors propelling the market in India.

Chronic Pancreatitis Treatment Market Share

The chronic pancreatitis treatment industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Aptalis Pharma Inc. (Canada)

- McNeil Consumer Healthcare (U.S.)

- Sun Biopharma Inc. (U.S.)

- Radboud University (Netherlands)

- University Medicine Greifswald (Germany)

- University of Alabama (U.S.)

- Camurus AB (Sweden)

- Cypralis Ltd. (U.K.)

- Ionis Pharmaceuticals Inc. (U.S.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Mission: Cure (U.S.)

- ChiRhoClin Inc. (U.S.)

- D-Pharm Ltd. (Israel)

- Exalenz Bioscience Ltd. (Israel)

- SCM Lifescience Co. Ltd. (South Korea)

- Talphera Inc. (U.S.)

- Far North Surgery (U.S.)

- Dmitri Alden MD, FACS (U.S.)

- Cedars-Sinai Medical Center (U.S.)

What are the Recent Developments in Global Chronic Pancreatitis Treatment Market?

- In July 2025, a private hospital in Pune, India, inaugurated a comprehensive one-stop centre dedicated to the diagnosis and treatment of pancreatic diseases, including chronic pancreatitis. This facility aims to streamline patient care by offering coordinated services, from diagnostics to therapy, under one roof, enhancing accessibility and efficiency for patients

- In June 2025, a study published in Current Pain and Headache Reports highlighted the adoption of precision medicine in managing chronic pancreatitis (CP). This approach tailors treatment based on individual pain mechanisms, moving away from the traditional trial-and-error method. By identifying specific pain pathways, clinicians can administer more targeted and effective interventions, potentially reducing reliance on opioids and improving patient outcomes

- In May 2025, the American Society for Gastrointestinal Endoscopy (ASGE) released updated guidelines on endoscopic care for chronic pancreatitis. These guidelines provide clarity on when and how endoscopic treatments, such as endoscopic retrograde cholangiopancreatography (ERCP), are most effective for CP patients. The aim is to standardize care and improve patient outcomes through evidence-based practices

- In December 2024, a study published in Pancreatology introduced a core outcome set for chronic pancreatitis (CP) and recurrent acute pancreatitis (RAP). The research, conducted through a Delphi poll involving patients, healthcare providers, and researchers, identified key domains for future clinical trials

- In June 2024, researchers from Northwestern University developed a new antioxidant biomaterial that shows promise in providing relief to individuals with chronic pancreatitis. This biomaterial aims to address oxidative stress, a key factor in CP progression, potentially offering a novel therapeutic avenue for managing the condition

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.