Global Clinical Communication Software Market

Market Size in USD Billion

CAGR :

%

USD

2.31 Billion

USD

5.51 Billion

2025

2033

USD

2.31 Billion

USD

5.51 Billion

2025

2033

| 2026 –2033 | |

| USD 2.31 Billion | |

| USD 5.51 Billion | |

| % | |

|

Clinical Communication Software Market Size

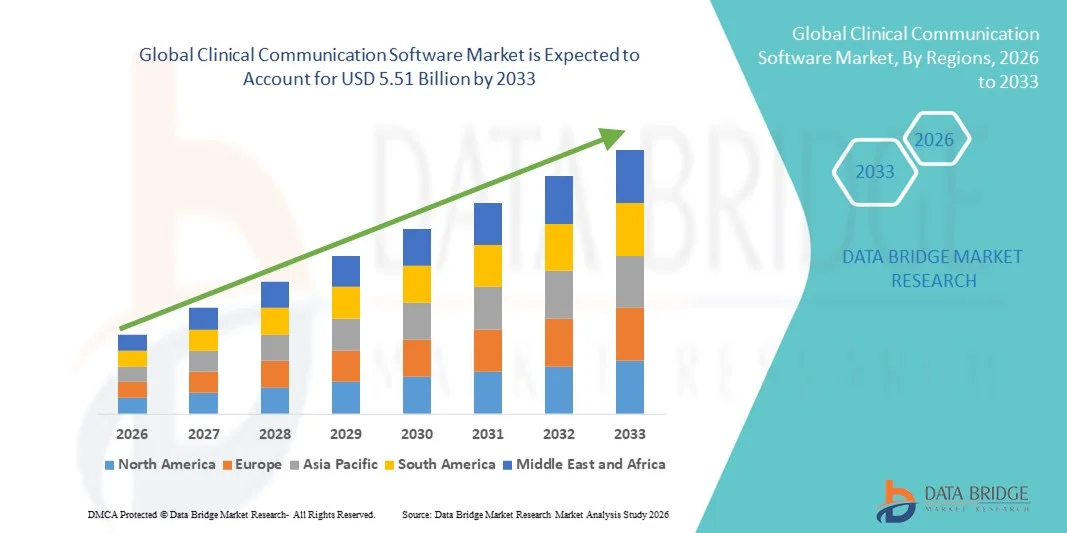

- The global clinical communication software market size was valued at USD 2.31 billion in 2025 and is expected to reach USD 5.51 billion by 2033, at a CAGR of 11.50% during the forecast period

- The market growth is largely fueled by increasing adoption of digital communication tools in healthcare, rising demand for efficient care coordination, real‑time clinical messaging, and the integration of advanced technologies such as AI, cloud computing, and mobile platforms to enhance collaboration among healthcare professionals

- Furthermore, growing emphasis on improving patient outcomes, streamlining clinical workflows, and supporting telehealth and remote monitoring solutions is driving healthcare providers and facilities to adopt clinical communication software as a modern communication and collaboration solution. These converging factors are accelerating the uptake of clinical communication software solutions, thereby significantly boosting the industry’s growth

Clinical Communication Software Market Analysis

- Clinical communication software, providing secure messaging, real-time alerts, and workflow management for healthcare teams, is becoming an essential tool in modern healthcare facilities due to its ability to improve care coordination, patient safety, and operational efficiency

- The escalating demand for clinical communication software is primarily fueled by the increasing adoption of digital health solutions, rising pressure to enhance patient outcomes, and growing need for seamless collaboration among physicians, nurses, and other healthcare professionals

- North America dominated the clinical communication software market with the largest revenue share of 39.7% in 2025, driven by early adoption of healthcare IT solutions, high healthcare expenditure, and a strong presence of key industry players, with the U.S. witnessing substantial growth in hospital and clinic deployments, particularly in large multi-hospital networks, supported by innovations in AI-driven communication, mobile apps, and integrated EHR systems

- Asia-Pacific is expected to be the fastest growing region in the clinical communication software market during the forecast period due to expanding healthcare infrastructure, increasing digitalization in hospitals, and rising investments in telehealth and remote patient monitoring solutions

- Cloud-based segment dominated the clinical communication software market with a market share of 44.1% in 2025, driven by its scalability, ease of deployment, remote accessibility, and reduced IT infrastructure costs, making it the preferred choice for hospitals, large enterprises, and SMEs

Report Scope and Clinical Communication Software Market Segmentation

|

Attributes |

Clinical Communication Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Clinical Communication Software Market Trends

AI and Mobile-First Communication Enhancing Care Coordination

- A significant and accelerating trend in the global clinical communication software market is the integration of artificial intelligence (AI) and mobile-first platforms, enabling real-time alerts, predictive analytics, and seamless workflow management across healthcare teams

- For instance, Vocera Badge integrates AI-driven messaging and voice recognition to streamline nurse-to-physician communication, while PerfectServe mobile apps provide context-aware notifications for timely clinical decision-making

- AI integration in clinical communication software enables features such as predictive patient deterioration alerts, intelligent prioritization of messages, and automated escalation protocols to ensure urgent matters are addressed promptly

- The seamless integration of these platforms with electronic health records (EHRs), telehealth tools, and hospital IT systems facilitates centralized management of clinical workflows, enabling healthcare staff to coordinate care more efficiently

- This trend towards more intelligent, mobile-accessible, and interconnected communication systems is fundamentally reshaping expectations for care delivery, driving vendors such as TigerConnect to develop AI-enabled platforms with predictive alerts, secure messaging, and role-based notifications

- The demand for clinical communication solutions that offer AI-driven insights and mobile-first accessibility is growing rapidly across hospitals, large enterprises, and SMEs, as healthcare providers increasingly prioritize workflow efficiency and patient safety

- Rising demand for multi-language support and accessibility features in clinical communication tools is creating opportunities to expand adoption in diverse healthcare settings globally, catering to multinational hospital networks and multilingual staff

Clinical Communication Software Market Dynamics

Driver

Increasing Need for Efficient Care Coordination and Digital Health Adoption

- The rising focus on improving patient outcomes, combined with the accelerating adoption of digital health tools, is a significant driver for the heightened demand for clinical communication software

- For instance, in March 2025, Cerner Corporation expanded its cloud-based messaging solutions to integrate predictive analytics, improving coordination in multi-hospital networks

- As healthcare facilities face pressure to reduce medical errors and optimize staff workflows, clinical communication software offers features such as secure messaging, real-time alerts, and automated escalation protocols, providing a clear advantage over traditional communication methods

- Furthermore, the growing adoption of telehealth, remote patient monitoring, and connected care programs is making clinical communication software a critical component of modern healthcare delivery, facilitating seamless collaboration across teams and locations

- Mobile accessibility, AI-enabled prioritization, and integration with existing hospital IT systems are key factors propelling adoption in hospitals, large enterprises, and SMEs, while the push for standardized digital workflows further contributes to market growth

- Expansion of value-based care models and population health management initiatives is driving hospitals to adopt clinical communication software for better care coordination, efficiency, and patient outcome tracking

- The increasing shortage of healthcare staff and rising workloads in hospitals worldwide is encouraging the use of automated communication platforms to reduce manual follow-ups and streamline clinical task assignments

Restraint/Challenge

Data Security Concerns and Integration Complexity

- Concerns regarding patient data privacy, HIPAA compliance, and cybersecurity vulnerabilities pose significant challenges to broader adoption of clinical communication software

- For instance, high-profile incidents of healthcare data breaches have made some hospitals cautious about implementing fully connected messaging and alert systems

- Addressing these concerns through end-to-end encryption, secure authentication, and compliance with regulatory standards is crucial for building provider trust. Vendors such as TigerConnect and Vocera emphasize advanced security protocols and audit capabilities in their solutions

- In addition, the complexity of integrating new communication software with existing EHRs, legacy IT systems, and telehealth platforms can hinder adoption, particularly in facilities with limited technical resources

- While cloud-based and mobile solutions reduce deployment challenges, perceived implementation costs and the need for staff training remain barriers, especially for SMEs or resource-constrained hospitals, requiring robust onboarding and support programs for sustained adoption

- Limited standardization across hospital systems and software vendors may result in interoperability challenges, slowing the adoption of unified clinical communication solutions

- Resistance to change among healthcare professionals accustomed to traditional communication methods can impact adoption rates, necessitating change management strategies and continuous training programs

Clinical Communication Software Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the clinical communication software market is segmented into cloud-based and web-based solutions. The cloud-based segment dominated the market with the largest revenue share of 44.1% in 2025, driven by its scalability, ease of deployment, and remote accessibility. Cloud-based solutions allow hospitals, clinics, and SMEs to access real-time messaging, alerts, and workflow management without investing heavily in IT infrastructure. Healthcare providers also prefer cloud-based platforms for their automatic updates, secure data storage, and compatibility with mobile devices, enabling staff to communicate efficiently across departments. The growing adoption of telehealth, remote patient monitoring, and multi-hospital networks has further reinforced the preference for cloud-based solutions. Cloud-based systems also facilitate interoperability with electronic health records (EHRs), predictive analytics tools, and AI-enabled modules, providing a comprehensive digital healthcare experience.

The web-based segment is anticipated to witness the fastest growth rate of 13.8% from 2026 to 2033, fueled by increasing adoption among hospitals and large enterprises that require centralized management of clinical communication. Web-based platforms offer flexibility, browser-based access, and compatibility with existing IT infrastructure, making them suitable for facilities with strict IT policies or multi-location operations. They are also preferred for temporary setups or SMEs seeking affordable solutions without extensive mobile device integration. The continuous improvement in web technologies, security protocols, and user-friendly interfaces is further driving adoption in healthcare settings. In addition, the ability to integrate web-based platforms with cloud storage and AI analytics ensures that web-based solutions remain competitive and increasingly attractive for digital transformation in healthcare.

- By Application

On the basis of application, the clinical communication software market is segmented into hospitals, physicians, clinical laboratories, large enterprises, and SMEs. The hospital segment dominated the market with the largest revenue share of 49.3% in 2025, driven by the need for seamless communication among physicians, nurses, administrative staff, and allied healthcare professionals. Hospitals leverage clinical communication software for real-time alerts, secure messaging, task management, and integration with EHRs and monitoring systems, ensuring improved patient safety and operational efficiency. The adoption is particularly strong in large multi-specialty hospitals and academic medical centers, where timely coordination of care is critical. Hospitals are also increasingly investing in AI-enabled and mobile-accessible platforms to reduce response times and optimize clinical workflows. Furthermore, regulatory pressures to reduce medical errors and enhance reporting standards are encouraging hospitals to adopt robust communication solutions.

The SME segment is expected to witness the fastest growth rate of 14.5% from 2026 to 2033, fueled by increasing digitization in smaller clinics, outpatient centers, and specialty practices. SMEs are adopting clinical communication software to streamline internal workflows, improve collaboration among limited staff, and maintain compliance with patient safety regulations. Cloud-based and web-based solutions provide cost-effective options for SMEs, allowing them to implement advanced digital tools without heavy infrastructure investment. The rising emphasis on telehealth, remote consultations, and mobile accessibility in small practices is further accelerating adoption. In addition, SMEs benefit from scalable solutions that can expand with their operations, making clinical communication software a strategic investment for improving care quality and staff efficiency.

Clinical Communication Software Market Regional Analysis

- North America dominated the clinical communication software market with the largest revenue share of 39.7% in 2025, driven by early adoption of healthcare IT solutions, high healthcare expenditure, and a strong presence of key industry players

- Healthcare providers in the region prioritize efficient care coordination, secure messaging, and real-time alerts, leveraging clinical communication software to improve patient outcomes, reduce medical errors, and streamline hospital workflows

- This widespread adoption is further supported by advanced IT infrastructure, a digitally inclined healthcare workforce, and increasing investments in telehealth and remote patient monitoring, establishing clinical communication software as a preferred solution for hospitals, large enterprises, and multi-location healthcare facilities

The U.S. Clinical Communication Software Market Insight

The U.S. clinical communication software market captured the largest revenue share of 42% in 2025 within North America, driven by the early adoption of healthcare IT solutions and high healthcare expenditure. Hospitals and large healthcare networks are increasingly prioritizing real-time messaging, secure alerts, and workflow management to improve patient outcomes and reduce medical errors. The growing integration of telehealth, remote patient monitoring, and AI-enabled predictive analytics is further propelling market adoption. Moreover, the widespread availability of advanced IT infrastructure and a digitally adept healthcare workforce supports seamless deployment and utilization of clinical communication platforms. The rising demand for mobile-accessible, cloud-based solutions enhances coordination among care teams across multiple facilities.

Europe Clinical Communication Software Market Insight

The Europe clinical communication software market is projected to expand at a substantial CAGR during the forecast period, primarily driven by government initiatives supporting digital health transformation and increasing focus on patient safety. Hospitals and large healthcare facilities are adopting these solutions to improve care coordination and operational efficiency. Growing awareness of telemedicine and interoperability standards, alongside investments in hospital IT systems, fosters adoption. European healthcare providers are also seeking secure, compliant solutions to meet stringent data protection regulations. The market is witnessing strong growth in both public and private hospitals, with solutions being integrated into EHRs, lab systems, and clinical workflows.

U.K. Clinical Communication Software Market Insight

The U.K. clinical communication software market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing adoption of digital health platforms and the demand for improved patient care coordination. Hospitals and clinics are adopting secure messaging and real-time alert systems to enhance operational efficiency. Concerns about medical errors and patient safety are prompting healthcare providers to implement comprehensive communication solutions. The U.K.’s strong IT infrastructure, government support for healthcare digitization, and widespread use of mobile health technologies are expected to continue stimulating market growth. The integration of communication software with telehealth and EHR systems enhances collaboration among healthcare teams.

Germany Clinical Communication Software Market Insight

The Germany clinical communication software market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of digital health, data security, and efficiency in patient care. Hospitals and multi-location healthcare providers are increasingly adopting integrated communication platforms to streamline workflows. Germany’s emphasis on innovation, sustainability, and regulatory compliance promotes adoption, particularly for cloud-based and AI-enabled solutions. Integration with hospital IT systems and EHRs ensures seamless communication across departments. In addition, the demand for secure, privacy-focused messaging platforms aligns with local healthcare regulations and consumer expectations.

Asia-Pacific Clinical Communication Software Market Insight

The Asia-Pacific clinical communication software market is poised to grow at the fastest CAGR of 18% during the forecast period of 2026 to 2033, driven by expanding healthcare infrastructure, increasing digitalization, and rising adoption of telehealth in countries such as China, India, and Japan. Hospitals and healthcare networks are implementing solutions for real-time alerts, secure messaging, and workflow optimization. Government initiatives promoting smart hospitals and healthcare IT adoption are fueling growth. In addition, the rising patient population and the shortage of healthcare staff are creating demand for platforms that improve coordination and efficiency. Cloud-based solutions and mobile accessibility make these platforms increasingly accessible to hospitals of all sizes.

Japan Clinical Communication Software Market Insight

The Japan clinical communication software market is gaining momentum due to the country’s high-tech healthcare environment, rapid urbanization, and focus on improving patient outcomes. Hospitals and clinics are adopting communication platforms integrated with EHRs, AI-driven alerts, and telehealth systems. The aging population is driving demand for easier-to-use, reliable solutions that enhance patient safety and staff efficiency. Integration with mobile devices and connected hospital systems supports streamlined workflows. The market also benefits from government incentives for digital health transformation and ongoing investments in smart hospital initiatives.

India Clinical Communication Software Market Insight

The India clinical communication software market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s growing healthcare infrastructure, rapid digitization, and rising demand for quality patient care. Hospitals, clinics, and SMEs are increasingly adopting cloud-based and mobile communication platforms to improve workflow efficiency and care coordination. Government initiatives promoting telemedicine, digital health, and smart hospital programs are driving adoption. The availability of affordable solutions and local software providers is further supporting market growth. The rising number of private hospitals, specialty clinics, and multi-location healthcare networks is also expanding the need for secure, real-time communication solutions.

Clinical Communication Software Market Share

The Clinical Communication Software industry is primarily led by well-established companies, including:

- TigerConnect (U.S.)

- QliqSOFT (U.S.)

- Cisco Systems, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Ascom Holding AG (Switzerland)

- Epic Systems Corporation (U.S.)

- Cerner Corporation (U.S.)

- PerfectServe, LLC (U.S.)

- Qventus (U.S.)

- Veradigm Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Spok, Inc. (U.S.)

- Everbridge, Inc. (U.S.)

- Baxter (U.S.)

- Avaya Holdings Corp (U.S.)

- Symplr, Inc. (U.S.)

- NEC Corporation (Japan)

- Pulsara LLC (U.S.)

- Mobile Heartbeat, Inc. (U.S.)

What are the Recent Developments in Global Clinical Communication Software Market?

- In October 2025, KPJ Healthcare’s rollout of the NetSfere encrypted communication platform was covered by regional healthcare media, highlighting the implementation of end‑to‑end encryption and advanced IT controls designed to support seamless and compliant clinical collaboration across multiple hospital locations

- In September 2025, TigerConnect launched TigerConnect Transfer, a purpose‑built clinical communication and coordination product designed to streamline interfacility patient transfers and discharge transport by unifying bed sourcing, transport scheduling, and messaging into a single platform to improve care transitions and hospital throughput

- In May 2025, OpenText announced it would showcase new secure communications innovations at HIMSS 2025, including OpenText Core Messaging, a unified communications platform aimed at helping healthcare providers deliver secure, multimodal messaging (email, SMS, fax, voice) and streamline clinical workflows while maintaining compliance

- In March 2025, Vocera announced a strategic partnership to integrate its secure clinical communications platform with Epic Systems’ EHR workflows, enabling clinicians to access secure messaging, paging, and alerts directly within the Epic environment, streamlining real‑time collaboration and reducing communication friction at the point of care

- In February 2025, TigerConnect announced at HIMSS that it would launch new Pre‑Hospital and Transfer communication solutions to streamline emergency medical services (EMS), emergency department workflows, and clinical collaboration between EMS and hospital teams

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.