Global Cockayne Syndrome Market

Market Size in USD Million

USD

102.50 Million

USD

143.54 Million

2024

2032

USD

102.50 Million

USD

143.54 Million

2024

2032

| 2025 - 2032 | |

| USD 102.50 Million | |

| USD 143.54 Million | |

| % | |

|

Cockayne Syndrome Market Size

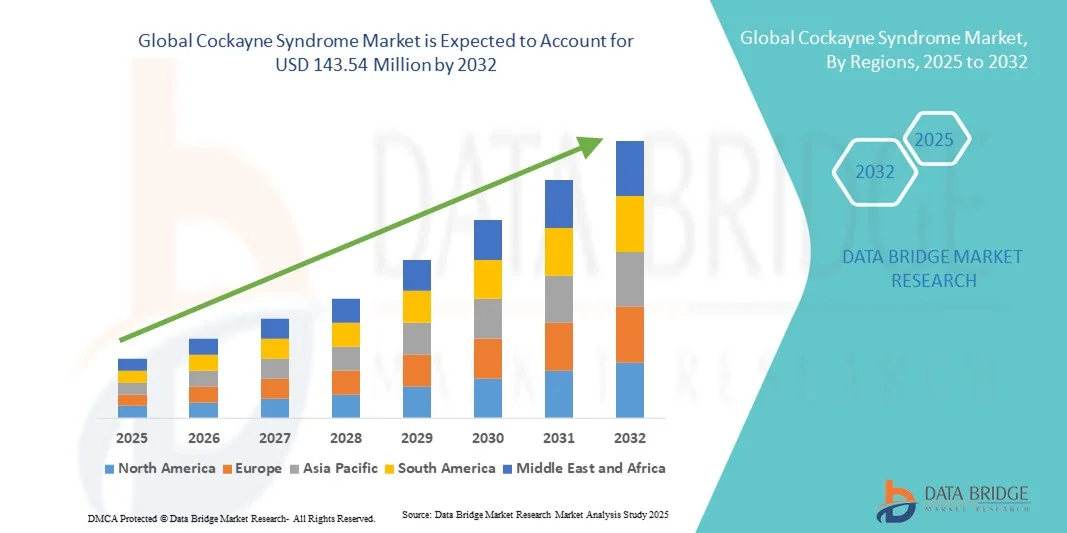

- The global Cockayne Syndrome market size was valued at USD 102.50 million in 2024 and is expected to reach USD 143.54 million by 2032, at a CAGR of 4.30% during the forecast period

- The market growth is primarily driven by rising research initiatives and advancements in genetic and molecular therapies, aiming to improve diagnosis and treatment outcomes for rare genetic disorders such as Cockayne Syndrome

- Furthermore, increasing government support for orphan drug development and growing awareness among healthcare professionals and patient organizations are accelerating early diagnosis and therapeutic innovation, thereby strengthening the overall growth of the Cockayne Syndrome market

Cockayne Syndrome Market Analysis

- Cockayne Syndrome, a rare autosomal recessive neurodegenerative disorder, is witnessing growing research attention, with efforts focusing on improved genetic diagnosis, molecular understanding, and potential gene-based therapies to address its severe developmental and neurological symptoms

- The rising demand for advanced diagnostic tools and specialized treatment options is primarily driven by increasing awareness of rare diseases, government support for orphan drug programs, and expanding collaborations among research institutes and biotech firms

- North America dominated the Cockayne Syndrome market with a revenue share of 39% in 2024, supported by strong healthcare infrastructure, active participation of leading genetic research organizations, and favorable regulatory frameworks encouraging rare disease research and clinical trials

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, driven by increasing investments in healthcare research, growing awareness of rare genetic disorders, and improving access to genetic testing and specialized treatment facilities in countries such as Japan, China, and South Korea

- The gene therapy segment dominated the market in 2024 with a share of 41.8%, driven by rapid advancements in genomic technologies, early adoption of molecular diagnostic platforms, and the growing pipeline of gene-based therapies targeting the underlying genetic mutations associated with Cockayne Syndrome

Report Scope and Cockayne Syndrome Market Segmentation

|

Attributes |

Cockayne Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cockayne Syndrome Market Trends

Advancements in Gene Therapy and Molecular Diagnosis

- A significant and accelerating trend in the global Cockayne Syndrome market is the growing focus on gene therapy and molecular diagnostic innovations, which aim to correct or identify the underlying genetic mutations responsible for the disorder, thereby improving treatment precision and patient outcomes

- For instance, research institutions and biotech firms are developing adeno-associated viral (AAV)-based gene therapies targeting DNA repair pathways, showing promising preclinical results in restoring cellular function in Cockayne Syndrome models

- The integration of next-generation sequencing (NGS) technologies in diagnostic workflows enables faster and more accurate detection of genetic variants, reducing diagnostic delays and supporting personalized treatment approaches

- Furthermore, advancements in bioinformatics and molecular pathology are enhancing understanding of disease mechanisms, helping identify novel therapeutic targets and potential biomarkers for early detection and intervention

- The growing use of patient-derived stem cell models in laboratory studies allows researchers to test the efficacy of new drugs and therapies in a controlled environment, accelerating discovery and translational research outcomes

- This trend toward genetic precision medicine and targeted therapy development is reshaping rare disease management, driving collaboration between academic researchers, biotech startups, and pharmaceutical companies to translate breakthroughs into clinical treatments

Cockayne Syndrome Market Dynamics

Driver

Increasing Research Funding and Orphan Drug Development Support

- The growing global commitment to rare disease research, combined with rising government and private funding for orphan drug development, is a major driver fueling the Cockayne Syndrome market growth

- For instance, the U.S. FDA and EMA have expanded orphan drug designations, providing incentives such as tax credits, research grants, and market exclusivity to companies developing therapies for rare genetic disorders, including Cockayne Syndrome

- As awareness of genetic conditions increases, research collaborations between universities, hospitals, and biotechnology firms are fostering the creation of targeted therapies and innovative molecular treatment approaches

- Furthermore, the increasing number of genetic testing initiatives and newborn screening programs is facilitating earlier detection, improving patient management, and expanding the potential treatment-eligible population

- The availability of advanced genomic sequencing infrastructure in leading research nations such as the U.S., U.K., and Japan is accelerating the development of disease-modifying therapies and companion diagnostics for rare neurodegenerative disorders

- The continuous evolution of international research networks and patient advocacy groups is enhancing data sharing, patient recruitment for clinical trials, and overall progress in drug development for Cockayne Syndrome

Restraint/Challenge

Limited Patient Population and High Research Costs

- The ultra-rare nature of Cockayne Syndrome, with a very small patient population worldwide, poses a significant challenge to commercial viability and large-scale clinical trial recruitment for new therapies

- For instance, the high cost and extended timelines of gene therapy and molecular research programs make it difficult for smaller biotech firms to sustain development without external funding or partnerships

- Moreover, the limited availability of standardized diagnostic protocols and registries hampers consistent data collection and slows the identification of eligible patients for experimental treatments

- Furthermore, regulatory complexities associated with orphan drug approvals and the need for robust long-term safety data increase both cost and time-to-market for potential therapies

- The lack of specialized treatment centers and awareness in developing regions restricts access to early diagnosis and participation in ongoing clinical studies, impeding global treatment reach

- Overcoming these challenges will require greater international collaboration, increased investment in rare disease infrastructure, and policies encouraging public-private partnerships to support sustainable therapy development for Cockayne Syndrome

Cockayne Syndrome Market Scope

The market is segmented on the basis of type, symptoms, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Cockayne Syndrome market is segmented into Classical Form Type I (Type A), Congenital Form Type II (Type B), and Late Onset Type III (Type C). The Classical Form Type I (Type A) segment dominated the market in 2024 with the largest revenue share, attributed to its higher prevalence and well-established clinical recognition. Type A patients often exhibit moderate disease severity and longer survival compared to Type B, leading to higher representation in registries and ongoing studies. Enhanced genetic screening programs are improving early detection rates for Type A cases. Moreover, continued emphasis on supportive management—such as physical therapy, nutritional interventions, and neurological monitoring—further consolidates this segment’s dominance. Growing awareness among pediatric neurologists and increased diagnostic capabilities at tertiary care centers also contribute to its strong position in the global market.

The Congenital Form Type II (Type B) segment is projected to witness the fastest growth rate during the forecast period, driven by growing research initiatives aimed at severe phenotypic presentations. Rising adoption of neonatal genetic testing and expansion of clinical genetic databases have improved identification of Type B cases at birth. Several ongoing preclinical studies are targeting early-stage molecular correction therapies, which could benefit this severe subtype. Increased government and private funding for rare congenital disorders are further propelling research activity in this area. The growing number of genetic counseling programs also aids in raising awareness and early intervention, making this the fastest-growing subtype segment.

- By Symptoms

On the basis of symptoms, the market is segmented into growth retardation, photosensitivity, progeria, and others. The Growth Retardation segment dominated the market in 2024, as this remains one of the earliest and most consistent clinical markers for Cockayne Syndrome. Most patients exhibit impaired physical development, which triggers early diagnostic testing and medical intervention. The segment’s dominance is further supported by the need for ongoing nutritional and endocrine management therapies throughout the patient’s lifespan. Hospitals and pediatric centers emphasize growth tracking and metabolic assessments, leading to sustained demand for supportive treatment products. Increased awareness among pediatricians and early growth monitoring in genetic screening programs are further consolidating this segment’s leading position.

The Photosensitivity segment is expected to record the fastest CAGR during the forecast period, attributed to deeper research into the UV-induced DNA repair dysfunction that underlies the condition. Patients with photosensitivity are increasingly being identified through dermatological assessments, expanding clinical detection rates. The development of targeted protective therapies such as UV-blocking formulations and advanced photoprotection protocols is enhancing clinical management. Additionally, ongoing research into nucleotide excision repair pathways is such asly to yield molecular-level interventions for photosensitive patients. Increasing emphasis on preventive dermatological care is supporting this segment’s rapid expansion.

- By Treatment

On the basis of treatment, the Cockayne Syndrome market is segmented into surgery, genetic therapy, drugs, and others. The Gene Therapy segment dominated the market in 2024 with a share of 41.8%, owing to significant progress in gene-editing and molecular repair technologies such as CRISPR-Cas9 and AAV-based delivery systems. This dominance is supported by active research focused on correcting mutations in the ERCC6 (CSB) and ERCC8 (CSA) genes responsible for the disorder. Several biotech firms and academic institutes are conducting preclinical and early-stage clinical trials aimed at restoring DNA repair functions in Cockayne Syndrome patients. Governments and private investors are increasing funding for orphan genetic diseases, fueling development in this segment. The gene therapy approach offers a long-term or potentially curative treatment pathway, positioning it as the most promising and clinically transformative segment of the market.

The Drugs segment is anticipated to witness the fastest growth from 2025 to 2032, driven by ongoing advancements in antioxidant, anti-inflammatory, and neuroprotective compounds. These therapies remain crucial for symptom management and improving patient quality of life, especially in cases where gene therapy access is limited. Additionally, the growing focus on developing small-molecule drugs targeting mitochondrial dysfunction is accelerating R&D investments. Supportive pharmacological treatments also continue to dominate pediatric and chronic management plans, making this the fastest-growing treatment segment during the forecast period

- By Route of Administration

On the basis of route of administration, the Cockayne Syndrome market is segmented into parenteral and others. The Parenteral segment dominated the market in 2024, owing to its central role in delivering investigational gene and enzyme replacement therapies. Parenteral administration ensures precise dosing, faster systemic absorption, and high bioavailability, which are essential in rare and severe cases. Hospitals and clinical research centers prefer this route for advanced therapeutic administration due to enhanced safety monitoring capabilities. Additionally, most ongoing clinical trials for gene and molecular therapies employ parenteral delivery systems. Increased investment in infusion-based biologics is expected to maintain this segment’s leading position. The growing number of hospital-based infusion facilities also supports consistent use of parenteral routes.

The Others segment, which includes oral, topical, and alternative delivery routes, is expected to record the fastest CAGR during the forecast period. Researchers are exploring non-invasive administration methods to improve patient comfort and treatment adherence. Oral antioxidant formulations, dietary supplements, and experimental topical treatments for photosensitivity are gaining attention. The focus on reducing hospital visits and improving accessibility for chronic management supports the adoption of these alternative routes. The rising trend of patient-centric drug delivery systems is expected to strengthen growth in this segment.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, and others. The Hospitals segment dominated the market in 2024 with the largest revenue share, as hospitals remain the central hubs for diagnosis, treatment, and multidisciplinary care for Cockayne Syndrome. Hospitals are equipped with advanced diagnostic laboratories and genetic testing facilities, ensuring accurate and timely diagnosis. The presence of neurology, genetics, and pediatric departments allows for comprehensive management under one setting. Hospitals also play a vital role in clinical trials and therapy development programs, making them indispensable in rare disease research. The availability of trained specialists and access to emergency care further strengthens this segment’s dominance.

The Specialty Clinics segment is projected to grow at the fastest CAGR during the forecast period, driven by the increasing number of rare disease-focused centers and genetic counseling units. These clinics offer personalized treatment plans, long-term follow-up, and precision therapy options for affected patients. Collaborations between specialty clinics and biotech research companies are increasing to facilitate gene therapy trials and molecular studies. Growing patient preference for specialized care outside large hospitals is supporting this trend. The expansion of rare disease networks in regions such as Europe and North America will further contribute to this segment’s accelerated growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and others. The Hospital Pharmacy segment dominated the market in 2024, as most advanced therapies including gene therapies and supportive infusions—are dispensed within hospital settings. Hospital pharmacies ensure strict monitoring of drug administration, storage, and patient safety. Their close integration with clinical departments facilitates efficient coordination in treatment planning. Hospital-based pharmacies also manage clinical trial drug supplies and orphan drug distribution, ensuring regulatory compliance. The reliance of patients on hospital facilities for critical therapy administration underlines this segment’s dominance.

The Retail Pharmacy segment is anticipated to witness the fastest growth rate through 2032, driven by the increasing availability of symptomatic medications and nutritional supplements for home-based care. Expansion of e-pharmacy platforms and partnerships with specialty distributors are improving access to rare disease medications. Retail pharmacies are increasingly offering genetic counseling support kits and specialized nutraceutical products. The convenience of online purchasing and delivery for chronic management medications is also encouraging adoption. As awareness of rare disorders expands, retail pharmacies are expected to play a greater role in the patient care continuum.

Cockayne Syndrome Market Regional Analysis

- North America dominated the Cockayne Syndrome market with a revenue share of 39% in 2024, supported by strong healthcare infrastructure, active participation of leading genetic research organizations, and favorable regulatory frameworks encouraging rare disease research and clinical trials

- The region’s market growth is further supported by the presence of leading biotechnology firms and academic collaborations focusing on gene and molecular therapies for DNA repair disorders

- High adoption of advanced diagnostic techniques, increased patient registries, and early diagnosis programs contribute to North America’s dominant position in the global Cockayne Syndrome market

U.S. Cockayne Syndrome Market Insight

The U.S. Cockayne Syndrome market captured the largest revenue share of 82% in 2024 within North America, driven by advanced genetic research facilities, strong clinical trial activity, and increased government funding for rare disease studies. The presence of leading biopharmaceutical companies and academic institutions focusing on DNA repair disorders is accelerating innovation in treatment options. The U.S. also benefits from robust orphan drug legislation that incentivizes R&D for ultra-rare conditions. Moreover, heightened awareness among clinicians, improved diagnostic capabilities, and active patient advocacy networks are supporting early detection and clinical management. These combined factors position the U.S. as the global leader in Cockayne Syndrome research and therapeutic development.

Europe Cockayne Syndrome Market Insight

The Europe Cockayne Syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong public health initiatives and increasing support for orphan and ultra-rare disease research. Countries such as Germany, France, and the U.K. are prioritizing genetic testing and rare disease registries to facilitate earlier diagnosis and treatment. European research networks such as EJP RD (European Joint Programme on Rare Diseases) are fostering collaboration across laboratories and biotech firms. Moreover, rising adoption of advanced gene therapies and supportive reimbursement frameworks across Western Europe are propelling market expansion. The increasing focus on cross-border clinical trials further strengthens Europe’s position in global rare disease management.

U.K. Cockayne Syndrome Market Insight

The U.K. Cockayne Syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by a robust healthcare infrastructure and growing emphasis on genomic medicine. The National Health Service (NHS) Genomic Medicine Service is enabling early identification of rare genetic disorders, improving patient outcomes. The U.K.’s investment in gene therapy and research programs such as Genomics England is accelerating the development of novel interventions. Moreover, awareness among pediatric and neurology specialists about Cockayne Syndrome continues to improve, promoting timely diagnosis. Collaborative efforts between universities, hospitals, and biotech companies are expected to further enhance therapeutic advancements.

Germany Cockayne Syndrome Market Insight

The Germany Cockayne Syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing investment in molecular biology and precision medicine. Germany’s focus on developing advanced diagnostic tools and genetic screening technologies supports early detection of Cockayne Syndrome. Additionally, public and private research institutions are actively participating in clinical studies exploring mitochondrial and DNA repair pathways. The country’s strong pharmaceutical manufacturing base, combined with active participation in EU rare disease programs, underpins steady market growth. Germany’s patient-centric approach and regulatory efficiency continue to attract biopharma collaborations for orphan disease therapies.

Asia-Pacific Cockayne Syndrome Market Insight

The Asia-Pacific Cockayne Syndrome market is poised to grow at the fastest CAGR of 24.3% from 2025 to 2032, driven by rising awareness of genetic diseases, expanding healthcare infrastructure, and increasing R&D investments in emerging economies such as China, Japan, and India. Governments are promoting rare disease diagnosis and treatment through national registries and supportive healthcare policies. Additionally, advancements in molecular diagnostics and next-generation sequencing are making early detection more accessible. Growing collaboration between Western biotech firms and Asian research centers is fostering technology transfer and clinical progress. The availability of specialized care centers and expansion of genetic testing services are expected to sustain rapid market growth.

Japan Cockayne Syndrome Market Insight

The Japan Cockayne Syndrome market is gaining momentum due to the country’s technological leadership in genomic and molecular diagnostics. Japan’s healthcare system emphasizes early detection and management of rare genetic diseases, supported by strong government funding and public research programs. The integration of Cockayne Syndrome testing within broader newborn screening initiatives is improving early intervention rates. Furthermore, partnerships between academic institutions and biotechnology firms are driving gene therapy research. The market’s growth is also supported by Japan’s proactive approach to aging and pediatric care, enhancing patient monitoring and clinical support systems.

India Cockayne Syndrome Market Insight

The India Cockayne Syndrome market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the expanding genetic testing industry, increased awareness of rare disorders, and government efforts to promote early diagnosis through initiatives such as the National Policy for Rare Diseases. India’s rapidly developing healthcare infrastructure and growing participation in international clinical trials are strengthening its market presence. Domestic biotech companies are increasingly collaborating with global organizations to advance genetic research and develop cost-effective treatment options. Additionally, the rise of pediatric specialty hospitals and advocacy groups is improving patient access to diagnostics and care, fueling sustained market growth.

Cockayne Syndrome Market Share

The Cockayne Syndrome industry is primarily led by well-established companies, including:

- Andelyn Biosciences (U.S.)

- Riaan Research Initiative (U.S.)

- Share & Care Cockayne Syndrome Network (U.S.)

- Regents of the University of Minnesota (U.S.)

- University of Massachusetts Chan Medical School (U.S.)

- LMU München (Germany)

- Leiden University Medical Center (Netherlands)

- The Cockayne Syndrome Foundation (U.S.)

- Boston Children’s Hospital (U.S.)

- University of Arizona (U.S.)

- Sarepta Therapeutics (U.S.)

- REGENXBIO Inc. (U.S.)

- uniQure N.V. (Netherlands)

- Catalent Inc. (U.S.)

- Charles River Laboratories International Inc. (U.S.)

- Lonza (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- ReproCELL Inc. (Japan)

What are the Recent Developments in Global Cockayne Syndrome Market?

- In June 2025, a pre-print study published on bioRxiv announced the development of a promising AAV-based gene therapy for Cockayne Syndrome, delivering the functional ERCC8/CSA gene in a mouse model and demonstrating strong therapeutic potential for future clinical translation

- In June 2024, UMass Chan Medical School received a USD 2.2 million donation from the Riaan Research Initiative to partner with Andelyn Biosciences for GMP-grade AAV9-CSA vector manufacturing marking a key step toward a first-in-human gene therapy trial for Cockayne Syndrome

- In April 2024, researchers at Ludwig-Maximilians-Universität München (LMU) uncovered a novel function of CSA and CSB proteins in repairing DNA-protein crosslinks during transcription, providing critical insight into the molecular basis of Cockayne Syndrome and revealing potential new therapeutic targets

- In January 2023, UMass Chan researchers achieved a major milestone in gene therapy for Cockayne Syndrome using an adeno-associated virus (AAV) vector, which extended lifespan and normalized growth in a Cockayne Syndrome mouse model, advancing progress toward clinical testing

- In October 2021, the Riaan Research Initiative announced funding for a gene-replacement therapy project at UMass Chan Medical School focused on correcting mutations in the CSA/ERCC8 gene, supporting the early development of vector-based therapeutic strategies for Cockayne Syndrome

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.