Global Compartment Syndrome Treatment Market

Market Size in USD Million

USD

211.94 Million

USD

294.55 Million

2024

2032

USD

211.94 Million

USD

294.55 Million

2024

2032

| 2025 - 2032 | |

| USD 211.94 Million | |

| USD 294.55 Million | |

| % | |

|

Compartment Syndrome Treatment Market Size

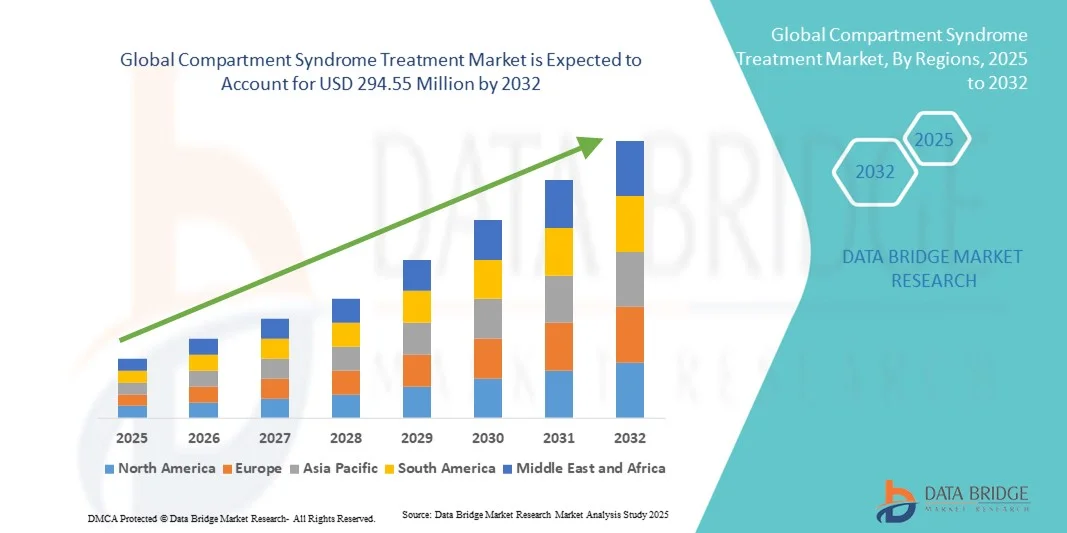

- The global Compartment Syndrome treatment market size was valued at USD 211.94 million in 2024 and is expected to reach USD 294.55 million by 2032, at a CAGR of 4.20% during the forecast period

- The market growth is largely driven by the rising prevalence of traumatic injuries, fractures, and vascular disorders, alongside increasing awareness of early diagnosis and timely intervention for compartment syndrome

- Furthermore, growing advancements in surgical procedures, minimally invasive techniques, and innovative treatment modalities, coupled with rising demand for improved patient outcomes in both emergency and elective care settings, are positioning effective compartment syndrome treatments as critical in modern healthcare. These converging factors are accelerating the adoption of advanced treatment options, thereby significantly boosting the industry's growth

Compartment Syndrome Treatment Market Analysis

- Compartment Syndrome treatments, encompassing surgical interventions such as fasciotomy and adjunctive therapies, are becoming increasingly critical in managing elevated intracompartmental pressures to prevent tissue necrosis and long-term disability in both traumatic and non-traumatic cases

- The rising prevalence of fractures, crush injuries, and vascular complications, along with growing awareness among healthcare professionals about early diagnosis and timely intervention, is driving the demand for effective compartment syndrome treatment solutions

- North America dominated the compartment syndrome treatment market with the largest revenue share of 38.5% in 2024, supported by advanced healthcare infrastructure, high adoption of innovative surgical techniques, and strong presence of key medical device and pharmaceutical companies, with the U.S. leading in fasciotomy procedures and adoption of minimally invasive treatment technologies

- Asia-Pacific is expected to be the fastest growing region in the compartment syndrome treatment market during the forecast period, attributed to increasing trauma incidence, improving healthcare access, and rising investments in emergency care facilities

- Surgery segment dominated the compartment syndrome treatment market with a market share of 47.2% in 2024, driven by its critical role in immediate pressure relief and prevention of permanent tissue damage in high-risk patients

Report Scope and Compartment Syndrome Treatment Market Segmentation

|

Attributes |

Compartment Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Compartment Syndrome Treatment Market Trends

Advancements in Minimally Invasive and Diagnostic Technologies

- A significant and accelerating trend in the global compartment syndrome treatment market is the adoption of minimally invasive surgical techniques and point-of-care diagnostic tools, improving patient outcomes and reducing recovery time

- For instance, handheld intracompartmental pressure monitors allow real-time assessment in emergency and orthopedic settings, enabling quicker decision-making for fasciotomy procedures

- Integration of imaging technologies such as near-infrared spectroscopy and continuous pressure monitoring systems facilitates early detection of compartment syndrome, helping clinicians prevent irreversible tissue damage

- These technologies allow healthcare providers to precisely identify high-risk compartments, track changes over time, and tailor interventions based on individual patient profiles

- The trend towards more rapid, accurate, and less invasive diagnostic and treatment approaches is reshaping clinical expectations for compartment syndrome management. Consequently, companies such as Stryker are developing advanced pressure monitoring and surgical systems to support timely interventions

- The demand for integrated, minimally invasive, and real-time diagnostic solutions is growing rapidly across trauma centers and orthopedic departments, as hospitals increasingly prioritize efficiency, patient safety, and improved post-operative outcomes

Compartment Syndrome Treatment Market Dynamics

Driver

Rising Trauma Incidence and Awareness of Early Intervention

- The increasing prevalence of traumatic injuries, fractures, and crush incidents, combined with growing awareness among clinicians about the importance of early intervention, is a significant driver of the compartment syndrome treatment market

- For instance, in March 2024, Stryker launched an advanced intracompartmental pressure monitoring system aimed at improving early diagnosis in emergency care settings

- As healthcare providers recognize the critical need for timely fasciotomy and other interventions, demand for specialized surgical equipment and monitoring devices is rising

- Furthermore, improved training and awareness campaigns for emergency and orthopedic teams are making timely diagnosis and treatment more feasible, reducing long-term disability risks

- Increasing investment in trauma care infrastructure, especially in emerging economies, is boosting the availability of advanced compartment syndrome treatment solutions

- For instance, hospitals in India and Southeast Asia are upgrading emergency care units with modern monitoring and surgical equipment to manage high-risk trauma cases effectively.

- The ability to monitor high-risk patients continuously and intervene quickly, combined with increasing hospital adoption of advanced treatment solutions, is propelling market growth in both developed and emerging regions

Restraint/Challenge

Limited Awareness in Emerging Regions and High Treatment Costs

- The lack of awareness about compartment syndrome and delayed presentation of patients in emerging regions pose significant challenges to market expansion. Early detection is often missed due to insufficient monitoring resources in rural or low-resource hospitals

- For instance, delayed diagnosis in remote trauma cases can result in higher rates of complications, limiting the adoption of advanced treatment technologies

- High costs associated with specialized surgical instruments, pressure monitoring systems, and hospital interventions can also restrict widespread access in price-sensitive region

- While awareness and training programs are gradually increasing, the gap in knowledge among general practitioners and emergency personnel can delay treatment initiation

- Addressing these challenges through targeted educational initiatives, cost-effective treatment solutions, and wider distribution of minimally invasive technologies will be critical for sustained growth of the compartment syndrome treatment market

- Variability in clinical guidelines and lack of standardized treatment protocols in some regions can hinder adoption of advanced compartment syndrome solutions

- For instance, differing pressure thresholds and intervention timings across hospitals can create uncertainty in implementing new monitoring technologies

Compartment Syndrome Treatment Market Scope

The market is segmented on the basis of type, drug type, application, treatment type, route of administration, mode of purchase, and distribution channel.

- By Type

On the basis of type, the compartment syndrome treatment market is segmented into acute and chronic. The acute compartment syndrome segment dominated the market with the largest revenue share in 2024, driven by its immediate threat to life and limb, requiring urgent medical intervention. Hospitals and trauma centers prioritize rapid diagnosis and surgical intervention, such as fasciotomy, to prevent permanent tissue damage. The high prevalence of fractures, crush injuries, and post-surgical complications ensures consistent demand. Clinical guidelines and awareness campaigns further reinforce its dominance. In addition, advanced monitoring devices and surgical equipment are widely adopted for acute cases, strengthening its market share.

The chronic compartment syndrome segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing cases among athletes and individuals engaged in repetitive physical activities. such as acute cases, chronic cases develop gradually, creating demand for non-invasive diagnostics and physiotherapy-based treatments. Rising awareness about early detection and preventive care in sports medicine and rehabilitation centers is accelerating adoption. Wearable monitoring devices and minimally invasive interventions further drive growth. The growing preference for home-based management and supportive care enhances market uptake, making it the fastest-growing type segment.

- By Drug Type

On the basis of drug type, the market is segmented into opioids, non-opioids, and NSAIDs. The opioids segment dominated the market in 2024 due to their effectiveness in managing severe pain associated with acute and post-surgical cases. Hospitals and trauma centers rely on opioids for immediate analgesic needs, reinforcing their market share. Prescription-based distribution ensures controlled use, and their widespread adoption by clinicians strengthens their position. High efficacy and clinician familiarity make opioids the preferred choice in acute care scenarios. Regulatory oversight further supports their continued dominance in treatment protocols.

The NSAIDs segment is expected to witness the fastest growth from 2025 to 2032, driven by rising awareness of non-opioid pain management and anti-inflammatory benefits. NSAIDs are increasingly adopted in both acute supportive care and chronic compartment syndrome cases. Over-the-counter availability in some regions enhances accessibility, while new formulations improve efficacy and safety. Growing integration of NSAIDs into multimodal treatment plans supports recovery and reduces long-term dependency on opioids. The focus on outpatient care and home-based therapies contributes to rapid market growth for NSAIDs.

- By Application

On the basis of application, the market is segmented into head trauma and cardiology. The head trauma segment dominated the market with the largest revenue share in 2024, driven by the high incidence of traumatic brain injuries and associated compartment syndrome. Elevated intracranial pressures require urgent intervention, often using surgical decompression and supportive pharmacological therapies. Hospitals and trauma centers are equipped with advanced monitoring systems to manage these cases efficiently. Awareness campaigns and clinical guidelines further strengthen the segment’s dominance. The critical nature of head trauma ensures continuous demand for specialized treatment solutions, securing its largest market share.

The cardiology segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing cases of compartment syndrome following cardiac surgeries and catheter-based interventions. Rising awareness among cardiologists and post-operative care units about early detection and pressure monitoring is driving adoption. Minimally invasive monitoring techniques and supportive therapies enhance growth. Expansion of cardiac centers in emerging markets further accelerates uptake. Integration of non-invasive interventions and post-operative rehabilitation strengthens the segment’s rapid growth trajectory.

- By Treatment Type

On the basis of treatment type, the market is segmented into surgery, supportive treatment, anti-inflammatory medications, and physiotherapy. The surgery segment dominated the market in 2024, driven by its critical role in preventing permanent tissue damage in acute cases. Hospitals invest in surgical instruments and monitoring systems to ensure precise and timely interventions such as fasciotomy. High success rates, clinician familiarity, and clinical guidelines reinforce its dominance. Adoption across both developed and emerging regions further strengthens the segment. Patient outcomes and emergency protocol adherence contribute to its largest revenue share.

The anti-inflammatory medications segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by rising adoption of non-invasive management strategies for chronic cases and post-surgical care. Increasing awareness of inflammation control and pain management drives uptake. Novel drug formulations with improved efficacy and safety profiles support growth. Integration into multimodal treatment protocols enhances compliance and recovery. Outpatient and home-based therapy trends further accelerate adoption, positioning anti-inflammatory medications as the fastest-growing treatment type.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and intravenous. The intravenous (IV) segment dominated the market in 2024 due to rapid therapeutic effects required in acute and critical cases. IV administration is preferred in hospitals for delivering analgesics, anti-inflammatory drugs, and supportive fluids. Controlled environments and clinician expertise ensure efficacy and safety. High adoption in trauma and surgical wards reinforces dominance. The ability to administer multiple drugs simultaneously makes IV administration essential in emergency care, ensuring the largest market share.

The oral segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its convenience for chronic management and outpatient care. Oral NSAIDs and other medications are increasingly used for long-term pain and inflammation control. Rising awareness of self-administered therapies and home-based care is boosting adoption. Telemedicine and remote monitoring solutions further support oral treatment uptake. Accessibility, ease of administration, and patient compliance contribute to its rapid growth trajectory, making oral administration the fastest-growing segment.

- By Mode of Purchase

On the basis of mode of purchase, the market is segmented into prescription and over-the-counter (OTC). The prescription segment dominated the market in 2024 due to the need for medical supervision for surgical interventions, opioids, and advanced pharmacological treatments. Controlled distribution channels and regulatory requirements reinforce dominance. Hospitals, trauma centers, and clinics ensure safe prescription practices, particularly in acute and post-surgical cases. Professional oversight enhances efficacy and patient safety. Consequently, prescription-based distribution accounts for the largest revenue share in the market.

The over-the-counter (OTC) segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing availability of NSAIDs and non-opioid analgesics for self-managed chronic pain and supportive care. Rising consumer awareness about early symptom management is enhancing adoption. OTC accessibility and affordability are accelerating penetration in developed and emerging markets. Integration into home-based recovery strategies supports market growth. Consequently, OTC purchase is witnessing the fastest growth among mode-of-purchase options.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The hospital pharmacies segment dominated the market in 2024, driven by the direct link to acute care, surgical procedures, and trauma treatment. Hospitals ensure timely availability of medications, surgical tools, and supportive care products, enhancing patient outcomes. Integration with hospital inventory and treatment protocols strengthens dominance. The presence of skilled healthcare professionals ensures proper administration and adherence to clinical guidelines. High-volume procurement and centralized supply chains further reinforce hospital pharmacies’ leading position.

The online pharmacies segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing digital healthcare adoption and home delivery of medications. Growing preference for convenient, doorstep delivery of chronic pain management drugs and supportive care products is driving adoption. Telemedicine consultations and prescription fulfillment via online platforms enhance accessibility. Rising internet penetration and mobile healthcare applications contribute to growth. The ease of ordering medications from home and broader availability of OTC products make online pharmacies the fastest-growing distribution channel.

Compartment Syndrome Treatment Market Regional Analysis

- North America dominated the compartment syndrome treatment market with the largest revenue share of 38.5% in 2024, supported by advanced healthcare infrastructure, high adoption of innovative surgical techniques, and strong presence of key medical device and pharmaceutical companies, with the U.S. leading in fasciotomy procedures and adoption of minimally invasive treatment technologies

- Hospitals and trauma centers in the region are equipped with state-of-the-art surgical instruments, monitoring systems, and pharmacological therapies, ensuring timely and effective management of both acute and chronic cases

- This widespread adoption is further supported by a well-trained medical workforce, strong presence of key medical device and pharmaceutical companies, and rising investments in emergency care and post-operative rehabilitation, establishing North America as a leading market for compartment syndrome treatment

U.S. Compartment Syndrome Treatment Market Insight

The U.S. compartment syndrome treatment market captured the largest revenue share within North America in 2024, fueled by advanced healthcare infrastructure, high incidence of traumatic injuries, and growing awareness of early diagnosis and timely intervention. Hospitals and trauma centers are equipped with state-of-the-art surgical instruments, monitoring devices, and pharmacological treatments, ensuring effective management of both acute and chronic cases. Rising preference for minimally invasive procedures, point-of-care diagnostics, and evidence-based treatment protocols further drives market growth. In addition, increasing investment in emergency care, rehabilitation centers, and physician training programs supports adoption. The U.S. continues to lead the region due to strong research initiatives, robust healthcare expenditure, and a high focus on improving patient outcomes.

Europe Compartment Syndrome Treatment Market Insight

The Europe compartment syndrome treatment market is projected to grow at a substantial CAGR during the forecast period, primarily driven by improved healthcare infrastructure, increasing trauma cases, and rising awareness about early intervention. Stringent regulatory standards for patient care and post-surgical management are fostering adoption of advanced treatment solutions, including surgical and pharmacological therapies. Growing urbanization, high-quality hospital networks, and increasing adoption of minimally invasive procedures are further supporting market growth. European healthcare providers are emphasizing enhanced recovery protocols and continuous patient monitoring, leading to higher demand for compartment syndrome treatments across both acute and chronic cases.

U.K. Compartment Syndrome Treatment Market Insight

The U.K. compartment syndrome treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising trauma incidence, growing awareness among healthcare professionals, and the increasing adoption of advanced monitoring and surgical techniques. Hospitals and emergency care units are prioritizing early diagnosis and intervention to prevent complications. The demand for physiotherapy, anti-inflammatory medications, and supportive care for chronic cases is also increasing. Investments in modern trauma care facilities, combined with the adoption of telemedicine and point-of-care diagnostic tools, are expected to stimulate market growth. The country’s strong healthcare system and focus on patient safety support sustained expansion of the compartment syndrome treatment market.

Germany Compartment Syndrome Treatment Market Insight

The Germany compartment syndrome treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of timely diagnosis, advanced surgical techniques, and non-invasive monitoring technologies. Germany’s well-developed healthcare infrastructure, high healthcare expenditure, and emphasis on innovation in patient care promote adoption. Hospitals and specialized trauma centers are increasingly incorporating advanced pressure monitoring systems and minimally invasive interventions. In addition, the preference for evidence-based treatment protocols and post-operative rehabilitation solutions is contributing to market growth. Rising research initiatives and strong presence of medical device manufacturers further reinforce Germany’s market position.

Asia-Pacific Compartment Syndrome Treatment Market Insight

The Asia-Pacific compartment syndrome treatment market is poised to grow at the fastest CAGR during the forecast period, driven by increasing trauma incidence, rapid urbanization, and expanding healthcare infrastructure in countries such as China, India, and Japan. Government initiatives aimed at improving emergency care and post-trauma management are accelerating adoption. Rising awareness about early detection, minimally invasive interventions, and supportive care solutions is further driving market expansion. The region’s large patient pool, increasing hospital investments, and growing number of specialized trauma care units are supporting demand. Moreover, improving access to diagnostic devices, medications, and surgical tools is enabling wider market penetration across APAC.

Japan Compartment Syndrome Treatment Market Insight

The Japan compartment syndrome treatment market is gaining momentum due to the country’s advanced healthcare infrastructure, high-tech hospital systems, and emphasis on rapid, accurate diagnosis and treatment. The growing prevalence of trauma cases, coupled with an aging population requiring specialized care, is increasing demand for minimally invasive procedures and supportive therapies. Integration of advanced monitoring systems in hospitals, along with rehabilitation and post-surgical care programs, is fueling market growth. In addition, Japan’s focus on preventive healthcare and evidence-based treatment protocols supports the adoption of compartment syndrome management solutions across residential and clinical settings.

India Compartment Syndrome Treatment Market Insight

The India compartment syndrome treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare infrastructure, rising trauma cases, and increasing awareness of early intervention. Hospitals are increasingly equipped with modern surgical instruments, monitoring systems, and pharmacological solutions to manage both acute and chronic cases effectively. Government initiatives aimed at improving emergency and post-trauma care, along with rising investments in rehabilitation centers, support market growth. Growing adoption of minimally invasive procedures, physiotherapy, and point-of-care diagnostic tools is accelerating demand. The availability of affordable treatment options and the presence of domestic medical device manufacturers further propel market expansion in India.

Compartment Syndrome Treatment Market Share

The Compartment Syndrome Treatment industry is primarily led by well-established companies, including:

- Zimmer Biomet. (U.S.)

- Stryker (U.S.)

- Smith & Nephew (U.K.)

- B. Braun SE (Germany)

- Medtronic (Ireland)

- CONMED Corporation (U.S.)

- 3M (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- Bioventus Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- Arthrex, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- BD (U.S.)

- C2Dx, Inc. (U.S.)

- Accuryn Medical (U.S.)

- Medline Industries, Inc. (U.S.)

- MY01, Inc. (U.S.)

- Convatec Inc. (U.K.)

- RAUMEDIC AG (Germany)

What are the Recent Developments in Global Compartment Syndrome Treatment Market?

- In April 2025, a multicenter, non-randomized, prospective study was conducted across six Level-I trauma centers to evaluate a new compartment pressure monitor that reports continuous pressures. This device aims to enhance the diagnosis of Acute Compartment Syndrome (ACS) by providing real-time pressure measurements, potentially improving patient outcomes through timely intervention

- In March 2025, a study published in Arthroscopy Techniques discussed the outcomes of open four-compartment fasciotomy for chronic exertional compartment syndrome. The study highlighted the procedure's effectiveness in relieving symptoms and improving long-term recovery for patients, particularly athletes, by addressing the underlying muscle compartment pressures

- In January 2025, a unique case of acute compartment syndrome affecting the pectoralis muscle was reported in the Critical Care Medicine Journal. This rare occurrence underscores the importance of considering compartment syndrome in atypical anatomical locations, broadening the scope of diagnosis and treatment strategies beyond the commonly affected limbs

- In December 2024, a review article in the Journal of Orthopaedic Case Reports explored conservative management strategies for paraspinal compartment syndrome, a rare clinical condition. The review suggests that in certain cases, conservative approaches may be considered, highlighting the need for individualized treatment plans based on patient-specific factors and the severity of the condition

- In August 2024, a meta-analysis published in PubMed examined post-fasciotomy complications in lower extremity acute compartment syndrome. The analysis emphasized the critical role of early fasciotomy, particularly within six hours of injury, in reducing the risk of complications such as amputation, thereby reinforcing the need for prompt surgical intervention

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.