Global Connected Home Medical Sensor Device Market

Market Size in USD Billion

USD

2.97 Billion

USD

9.27 Billion

2024

2032

USD

2.97 Billion

USD

9.27 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.97 Billion | |

| USD 9.27 Billion | |

| % | |

|

Connected Home Medical Sensor Device Market Size

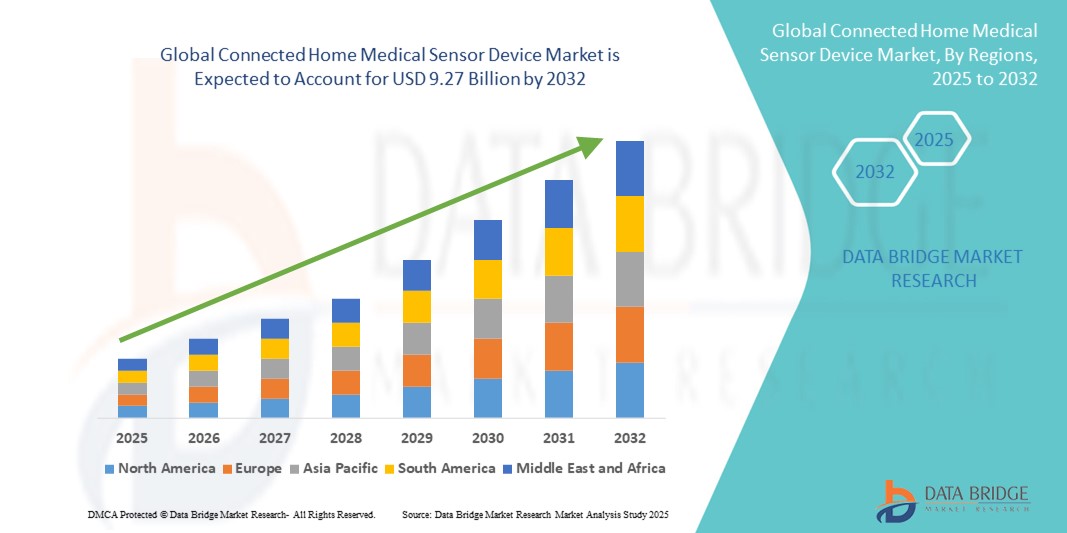

- The global connected home medical sensor device market size was valued at USD 2.97 billion in 2024 and is expected to reach USD 9.27 billion by 2032, at a CAGR of 15.30% during the forecast period

- The market growth is largely fueled by the increasing adoption of home-based healthcare solutions, advancements in wearable and remote monitoring technologies, and the rising integration of IoT and digital health platforms

- Furthermore, growing consumer focus on preventive healthcare, chronic disease management, and convenient remote monitoring is driving demand for connected home medical sensor devices, establishing them as essential tools in modern home healthcare. These converging factors are accelerating the adoption of these devices, thereby significantly boosting the industry’s growth

Connected Home Medical Sensor Device Market Analysis

- Connected home medical sensor devices, including wearable monitors, stationary devices, and implantable sensors, are increasingly vital components of modern home healthcare and remote patient monitoring systems in both residential and clinical settings due to their ability to provide continuous health tracking, early disease detection, and seamless integration with telehealth platforms

- The escalating demand for connected home medical sensor devices is primarily fueled by the growing adoption of digital health solutions, increasing prevalence of chronic diseases, aging populations, and a rising preference for convenient home-based health monitoring

- North America dominated the connected home medical sensor device market with the largest revenue share of 42.1% in 2024, characterized by advanced healthcare infrastructure, high adoption of digital health technologies, and a strong presence of key industry players, with the U.S. experiencing substantial growth in wearable and remote monitoring device installations, driven by innovations in AI-powered analytics and integration with telemedicine platforms

- Asia-Pacific is expected to be the fastest growing region in the connected home medical sensor device market during the forecast period due to increasing healthcare awareness, rising disposable incomes, and government initiatives promoting digital health solutions

- Wearable devices dominated the connected home medical sensor device market with a market share of 45.5% in 2024, driven by their convenience, non-invasive monitoring capabilities, and rapid adoption among tech-savvy consumers and patients managing chronic conditions

Report Scope and Connected Home Medical Sensor Device Market Segmentation

|

Attributes |

Connected Home Medical Sensor Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Connected Home Medical Sensor Device Market Trends

Enhanced Convenience Through AI-Enabled Monitoring and Remote Health Management

- A significant and accelerating trend in the global connected home medical sensor device market is the integration of artificial intelligence (AI) and digital health platforms, enabling real-time health monitoring, predictive analytics, and remote patient management. This fusion of technologies is significantly enhancing user convenience and improving health outcomes

- For instance, devices such as the Withings ScanWatch and iHealth Wireless Blood Pressure Monitor can automatically sync data with mobile apps and cloud-based platforms, allowing users and healthcare providers to track vital signs seamlessly. Similarly, AI-powered wearables can detect irregular heart rhythms, provide personalized alerts, and even suggest early interventions

- AI integration enables devices to learn individual health patterns over time, improving measurement accuracy and generating intelligent insights. For example, some Biobeat devices use AI to enhance continuous monitoring of heart rate and oxygen levels, sending alerts if anomalies are detected

- The seamless integration of medical sensor devices with telehealth platforms allows centralized health management, where patients can monitor multiple metrics such as glucose, blood pressure, and activity levels through a single interface. This fosters a unified, automated approach to home healthcare

- This trend towards intelligent, predictive, and interconnected health monitoring systems is reshaping user expectations for home healthcare. Companies such as iHealth, Withings, and Biobeat are developing AI-enabled devices with continuous monitoring, remote notifications, and integration with telemedicine platforms

- The demand for connected medical sensor devices with AI-enabled insights and remote management capabilities is growing rapidly, driven by consumers’ increasing focus on preventive care, chronic disease management, and convenient home-based health monitoring

Connected Home Medical Sensor Device Market Dynamics

Driver

Rising Healthcare Awareness and Growing Telehealth Adoption

- The awareness about chronic diseases, preventive care, and the convenience of home-based monitoring, coupled with the rapid adoption of telehealth solutions, is a key driver of demand for connected home medical sensor devices

- For instance, in March 2024, Biobeat announced the expansion of its AI-powered remote monitoring platform for hospital-at-home programs, enhancing patient care and enabling early detection of health issues. Such initiatives by major players are expected to fuel market growth during the forecast period

- As patients seek more control over their health and convenience in managing medical conditions, connected devices offer features such as real-time alerts, activity tracking, and seamless data sharing with healthcare providers, providing a compelling alternative to traditional in-person monitoring

- Furthermore, the growing penetration of smartphones, mobile apps, and cloud platforms enables effortless integration of medical sensor devices into daily routines, encouraging widespread adoption in both residential and clinical settings

- The ease of use, real-time insights, and remote monitoring capabilities make connected medical sensor devices an essential component of modern home healthcare, with adoption increasing across both individual consumers and healthcare institutions

Restraint/Challenge

Data Privacy Concerns and Regulatory Compliance Hurdles

- Concerns surrounding data privacy, cybersecurity, and regulatory compliance pose significant challenges to the adoption of connected home medical sensor devices. As these devices collect sensitive health information, there is heightened risk of data breaches, making some consumers hesitant to adopt these technologies

- For instance, high-profile reports of vulnerabilities in connected health devices have raised consumer anxiety regarding the security of personal health data

- Addressing these concerns through robust encryption, secure authentication protocols, and compliance with health regulations such as HIPAA or GDPR is crucial for building trust. Companies such as iHealth and Withings emphasize privacy features and secure data transmission in their devices to reassure users

- In addition, the relatively high cost of advanced medical sensor devices compared to traditional health monitoring tools can be a barrier, particularly in developing regions. While entry-level devices are becoming more affordable, premium features such as AI-based analytics, continuous monitoring, or multi-metric tracking often come with a higher price tag

- Overcoming these challenges through enhanced cybersecurity, consumer education on data safety, and development of more cost-effective solutions will be vital for sustained market growth

Connected Home Medical Sensor Device Market Scope

The market is segmented on the basis of device type, application, technology, function, and end user.

- By Device Type

On the basis of device type, the connected home medical sensor device market is segmented into wearable devices, stationary devices, and internally embedded devices. The wearable devices segment dominated the market with the largest revenue share of 45.5% in 2024, driven by their convenience, non-invasive monitoring capabilities, and rapid adoption among tech-savvy consumers and patients managing chronic conditions. Wearables such as smartwatches, fitness trackers, and smart patches are highly compatible with mobile apps and telehealth platforms, providing real-time health insights. These devices also allow continuous tracking of vital signs such as heart rate, oxygen saturation, and sleep quality. Additionally, the growing trend of preventive healthcare and fitness monitoring among millennials and elderly users further strengthens demand for wearables. Their portability, ease of use, and integration with AI-based analytics enhance patient engagement and long-term adherence to health monitoring routines.

The stationary devices segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by increasing adoption of at-home monitoring systems such as blood pressure monitors, pulse oximeters, and glucose meters. These devices offer precise measurements and continuous monitoring for chronic disease management, particularly among elderly patients and individuals requiring frequent health tracking. Home-based stationary devices are preferred for their larger displays, ease of data logging, and ability to integrate with cloud-based platforms for remote monitoring by healthcare providers. Furthermore, stationary devices support multi-user households, enabling family members to monitor health collectively. The ongoing rise of telemedicine and remote patient management initiatives further accelerates the adoption of stationary devices in residential and clinical settings.

- By Application

On the basis of application, the connected home medical sensor device market is segmented into chronic disease management, wellness & prevention, and acute care monitoring. The chronic disease management segment held the largest market share in 2024, driven by rising prevalence of conditions such as diabetes, hypertension, and cardiovascular disorders. Patients increasingly prefer remote monitoring solutions to reduce hospital visits and improve quality of care. Connected devices provide real-time alerts to both patients and physicians, enabling timely interventions. Moreover, the integration of chronic disease monitoring devices with mobile apps and telehealth platforms enhances patient adherence to treatment plans. This segment also benefits from healthcare reimbursement initiatives that encourage home-based monitoring for chronic conditions.

The wellness & prevention segment is expected to witness the fastest growth during the forecast period due to increasing consumer focus on preventive healthcare, fitness tracking, and general health monitoring. Devices such as wearable fitness bands, smart scales, and environmental health sensors are gaining traction. Consumers are increasingly aware of the importance of lifestyle data for early detection of potential health issues. Integration with smartphone apps and cloud analytics allows users to track progress, set health goals, and receive personalized recommendations. Corporate wellness programs and insurance incentives further drive adoption.

- By Technology

On the basis of technology, the connected home medical sensor device market is segmented into Bluetooth Low Energy (BLE), Wi-Fi, cellular connectivity, and near-field communication (NFC). The Wi-Fi segment held the largest revenue share in 2024, supported by widespread availability of home internet networks and seamless integration with cloud-based health platforms. Wi-Fi-enabled devices allow remote monitoring by healthcare professionals and real-time data transfer. They also support multi-device connectivity, enabling patients to use multiple sensors simultaneously. Home networks provide stable data transmission, ensuring accuracy in patient monitoring. Moreover, Wi-Fi integration allows AI-based predictive analytics for chronic disease and wellness tracking.

The Bluetooth Low Energy segment is expected to witness the fastest CAGR from 2025 to 2032, due to its low power consumption, reliable short-range connectivity, and compatibility with smartphone apps. BLE devices are ideal for wearable sensors and localized monitoring solutions that require energy efficiency. They allow seamless synchronization of data to mobile devices without draining battery life. Bluetooth-enabled devices are also cost-effective, portable, and user-friendly. BLE facilitates secure data transfer and integration with broader healthcare ecosystems. The increasing adoption of health-focused mobile applications further drives demand for BLE-enabled connected medical sensors.

- By Function

On the basis of function, the connected home medical sensor device market is segmented into remote patient monitoring, clinical monitoring, and telemedicine. The remote patient monitoring segment dominated the market in 2024, driven by the increasing adoption of home healthcare services and continuous health monitoring. Devices provide real-time vital signs tracking, activity levels, and sleep patterns to physicians. Integration with telehealth platforms enables doctors to make informed decisions without in-person visits. Remote monitoring helps reduce hospital readmissions, improve patient outcomes, and decrease healthcare costs. Insurance coverage and government initiatives for home-based care further boost adoption.

The telemedicine segment is expected to witness robust growth during the forecast period, fueled by rising virtual consultations and demand for real-time diagnostics. Connected sensor devices transmit patient data directly to healthcare professionals during teleconsultations. This function supports remote diagnosis, treatment adjustments, and chronic disease management. Integration with AI and analytics enhances clinical decision-making. Telemedicine-enabled devices empower patients to manage health independently while maintaining professional oversight. The ongoing digital transformation in healthcare systems further accelerates adoption.

- By End User

On the basis of end user, the connected home medical sensor device market is segmented into home monitoring and hospitals & clinics. The home monitoring segment held a substantial market share in 2024, owing to increasing consumer adoption of wearable and stationary monitoring devices for chronic disease management, wellness tracking, and preventive healthcare. Consumers prefer devices that are easy to use, non-invasive, and compatible with mobile applications. Home monitoring allows continuous tracking and timely interventions without hospital visits. Integration with telemedicine platforms enhances patient convenience. The rising elderly population and increasing health awareness also drive segment growth.

The hospitals & clinics segment is anticipated to grow rapidly during the forecast period due to rising demand for integrated remote patient monitoring systems and improved patient management solutions. Connected devices in clinical settings enable staff to monitor multiple patients simultaneously, enhancing efficiency. These devices support early detection of complications and reduce hospital readmissions. Integration with hospital IT systems ensures real-time data availability. Adoption of connected devices in outpatient and inpatient care is increasing, driven by digital transformation and the need for better healthcare outcomes. Hospitals also benefit from operational cost savings and optimized resource utilization.

Connected Home Medical Sensor Device Market Regional Analysis

- North America dominated the connected home medical sensor device market with the largest revenue share of 42.1% in 2024, characterized by advanced healthcare infrastructure, high adoption of digital health technologies, and a strong presence of key industry players

- Consumers and healthcare providers in the region highly value the convenience, real-time health insights, and seamless connectivity offered by medical sensor devices with mobile apps and cloud-based health management systems

- This widespread adoption is further supported by advanced healthcare infrastructure, high digital health awareness, a technologically inclined population, and government initiatives promoting home-based care, establishing connected medical sensor devices as preferred solutions for both residential and clinical settings

U.S. Connected Home Medical Sensor Device Market Insight

The U.S. connected home medical sensor device market captured the largest revenue share of 80% in 2024 within North America, fueled by the rapid adoption of wearable and stationary health monitoring devices and the expanding trend of home healthcare. Consumers are increasingly prioritizing remote patient monitoring, chronic disease management, and wellness tracking through intelligent, connected devices. The growing preference for AI-enabled analytics, smartphone integration, and telehealth platforms further propels the market. Moreover, integration with digital health ecosystems and cloud-based platforms is significantly contributing to market expansion.

Europe Connected Home Medical Sensor Device Market Insight

The Europe connected home medical sensor device market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare awareness, stringent regulations, and the rising need for remote patient monitoring in homes and clinics. Urbanization and the demand for connected healthcare devices are fostering adoption, while European consumers are attracted to the convenience, real-time monitoring, and proactive care these devices provide. Growth is notable across residential, hospital, and assisted-living applications, with devices being incorporated in both new setups and renovation of healthcare facilities.

U.K. Connected Home Medical Sensor Device Market Insight

The U.K. connected home medical sensor device market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising home healthcare adoption, increased focus on chronic disease management, and demand for convenient remote monitoring. Growing awareness of preventive healthcare and the preference for connected devices among tech-savvy consumers are key drivers. Robust telehealth infrastructure and advanced mobile applications are expected to further stimulate market growth.

Germany Connected Home Medical Sensor Device Market Insight

The Germany connected home medical sensor device market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, increasing digital health adoption, and emphasis on advanced, eco-conscious medical devices. Consumers and healthcare providers favor devices that ensure accuracy, security, and integration with hospital or home monitoring systems. The market growth is supported by Germany’s focus on innovation, sustainability, and connected healthcare solutions.

Asia-Pacific Connected Home Medical Sensor Device Market Insight

The Asia-Pacific connected home medical sensor device market is poised to grow at the fastest CAGR during the forecast period, driven by rising healthcare awareness, urbanization, increasing disposable incomes, and government initiatives promoting digital health solutions in countries such as China, Japan, and India. The region is witnessing strong adoption of wearable devices and home-based monitoring systems, with increasing production and affordability of devices expanding access to a larger consumer base.

Japan Connected Home Medical Sensor Device Market Insight

The Japan connected home medical sensor device market is gaining momentum due to the country’s tech-oriented culture, aging population, and increasing demand for home-based monitoring solutions. Adoption is fueled by the integration of medical sensor devices with telehealth platforms, AI-powered analytics, and IoT-enabled home healthcare systems. The aging population further drives demand for convenient, easy-to-use remote monitoring solutions in both residential and clinical settings.

India Connected Home Medical Sensor Device Market Insight

The India connected home medical sensor device market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, a growing middle class, and high technology adoption. The country is emerging as a significant market for home healthcare solutions, with connected medical sensor devices gaining popularity in residential, commercial, and telehealth applications. Government initiatives promoting smart healthcare and the availability of affordable, locally manufactured devices are key factors propelling market growth.

Connected Home Medical Sensor Device Market Share

The Connected Home Medical Sensor Device industry is primarily led by well-established companies, including:

- Koninklijke Philips N.V. (Netherlands)

- Medtronic (Ireland)

- GE HealthCare (U.S.)

- Abbott (U.S.)

- Omron Healthcare, Inc. (Japan)

- Dexcom, Inc. (U.S.)

- ResMed Inc. (U.S.)

- Masimo Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- Fitbit LLC (U.S.)

- Withings SA (France)

- Garmin Ltd. (U.S.)

- AliveCor, Inc. (U.S.)

- iHealth Labs Inc. (U.S.)

- Nonin Medical, Inc. (U.S.)

- BioTelemetry, Inc. (U.S.)

- Senseonics Holdings, Inc. (U.S.)

- Xiaomi Corporation (China)

- Huawei Technologies Co., Ltd. (China)

- Nanowear, Inc. (U.S.)

What are the Recent Developments in Global Connected Home Medical Sensor Device Market?

- In August 2025, Cardiosense’s wearable heart monitor “CardioTag” obtained FDA clearance, enabling simultaneous, non-invasive capture of ECG, PPG, and seismocardiogram (SCG) signals. The device enhances cardiac monitoring by providing comprehensive, AI-enabled insights into heart function, including metrics such as ventricular ejection time, opening opportunities for more proactive cardiovascular care

- In June 2025, Ultrahuman introduced the Ultrahuman Home, a USD 549 environmental health monitoring system designed to transform residential spaces into holistic wellness ecosystems. Unsuch as traditional wearable trackers, this device focuses on ambient factors such as air quality, temperature, and lighting to assess and enhance overall well-being within the home

- In June 2024, Sheila Concannon from County Galway became the first patient in Ireland to receive an innovative heart failure sensor at University Hospital Galway. The implant continuously monitors fluid levels in heart failure patients, transmitting data daily to clinicians for remote monitoring and timely interventions, reducing hospital readmissions and improving patient care

- In January 2024, Nanowear received FDA 510(k) clearance for SimpleSense-BP, an AI-enabled, cuffless, continuous blood pressure monitoring platform. This wearable solution provides routine cardiopulmonary examinations at home, healthcare facilities, and in clinical research settings using a nanotechnology-driven AI algorithm. SimpleSense-BP represents a major leap in home-based hypertension diagnostics and management

- In November 2023, Researchers at Northwestern University unveiled a wireless broadband acousto-mechanical sensing (BAMS) system for continuous physiological monitoring. This wearable device captures subtle body sounds across multiple locations, enabling real-time health monitoring without the need for traditional sensors

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.