Global Corneal Opacity Market

Market Size in USD Million

USD

468.90 Million

USD

694.36 Million

2024

2032

USD

468.90 Million

USD

694.36 Million

2024

2032

| 2025 - 2032 | |

| USD 468.90 Million | |

| USD 694.36 Million | |

| % | |

|

Corneal Opacity Market Size

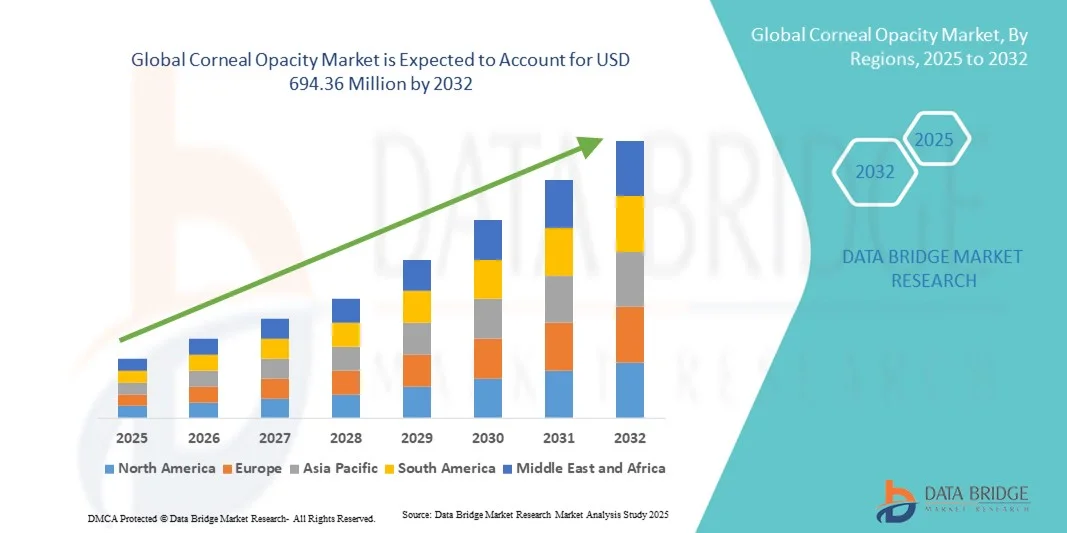

- The global corneal opacity market size was valued at USD 468.90 million in 2024 and is expected to reach USD 694.36 million by 2032, at a CAGR of 5.03% during the forecast period

- The market growth is largely fueled by the increasing prevalence of corneal diseases, advancements in treatment options, and rising awareness about eye health, leading to improved diagnosis and management of vision-impairing conditions

- Furthermore, the availability of various treatment modalities, including surgery, medication, and emerging therapies, is driving adoption across hospitals, specialty clinics, and ophthalmic centers. These converging factors are accelerating the uptake of corneal opacity solutions, thereby significantly boosting the industry's growth

Corneal Opacity Market Analysis

- Corneal opacity, characterized by clouding or scarring of the cornea, leads to impaired vision and is increasingly recognized as a significant cause of visual impairment and blindness worldwide. The market is driven by the growing prevalence of corneal diseases, advancements in diagnostic technologies, and improved access to ophthalmic care across both developed and developing regions

- The escalating demand for corneal opacity treatments is primarily fueled by rising patient awareness, increasing healthcare expenditure, and technological innovations in surgical procedures, contact lenses, and pharmacological therapies that improve patient outcomes

- North America dominated the corneal opacity market with the largest revenue share of 39.2% in 2024, attributed to advanced healthcare infrastructure, higher adoption of cutting-edge surgical solutions, and strong presence of key ophthalmic companies, with the U.S. leading in corneal transplant procedures and adoption of innovative vision-restoring technologies

- Asia-Pacific is expected to be the fastest-growing region in the corneal opacity market during the forecast period due to a high patient population, rising healthcare access, growing ophthalmologist availability, and increasing government initiatives for eye care in countries such as India, China, and Japan

- Surgery segment dominated the corneal opacity market with a market share of 45.7% in 2024, driven by its established efficacy in restoring vision, widespread adoption in hospitals and specialty eye clinics, and continuous advancements in minimally invasive and laser-assisted corneal surgeries

Report Scope and Corneal Opacity Market Segmentation

|

Attributes |

Corneal Opacity Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Corneal Opacity Market Trends

Advancements in Minimally Invasive and Laser-Assisted Surgeries

- A significant and accelerating trend in the global corneal opacity market is the adoption of minimally invasive and laser-assisted surgical procedures that improve visual outcomes and reduce recovery time

- For instance, femtosecond laser-assisted keratoplasty allows surgeons to perform precise corneal transplants with reduced risk of complications and faster healing compared to conventional techniques

- Integration of advanced imaging and diagnostic tools with surgical platforms enables ophthalmologists to customize treatment for individual patients, improving success rates and overall satisfaction

- The use of real-time intraoperative guidance systems facilitates precise surgical interventions, minimizing damage to surrounding tissues and enhancing post-operative visual acuity

- This trend towards more precise, safe, and patient-friendly surgical solutions is fundamentally reshaping treatment protocols for corneal opacity. Consequently, companies such as Alcon and Bausch & Lomb are developing advanced surgical devices with improved laser precision and patient monitoring capabilities

- The demand for advanced surgical and laser-assisted solutions is growing rapidly across both hospitals and specialty eye clinics, as patients and surgeons increasingly prioritize efficacy, safety, and faster visual recovery

Corneal Opacity Market Dynamics

Driver

Increasing Prevalence of Corneal Diseases and Eye Health Awareness

- The rising incidence of corneal diseases, coupled with growing awareness about eye health, is a significant driver for the heightened demand for corneal opacity treatments

- For instance, in 2024, the World Health Organization reported that corneal opacity is among the top causes of blindness worldwide, prompting increased screening and treatment initiatives

- As patients become more aware of vision-threatening conditions and available treatment options, demand for surgical, pharmacological, and contact lens therapies continues to rise

- Furthermore, healthcare infrastructure improvements and insurance coverage expansion in developed and emerging markets are making treatments more accessible and affordable for patients

- Increasing collaborations between ophthalmic research institutes and industry players are accelerating the development of novel therapies and improving treatment standards globally

- Rising government initiatives for blindness prevention and eye care programs in emerging markets are further boosting patient outreach and treatment adoption rates

- Availability of diverse treatment options such as corneal transplantation, medications, and advanced contact lenses provides ophthalmologists with flexible solutions to meet varying patient needs, further fueling market growth

Restraint/Challenge

High Cost of Advanced Treatments and Limited Access in Emerging Regions

- The high cost of advanced corneal opacity treatments and limited availability of skilled ophthalmologists in certain regions pose significant challenges to market expansion

- For instance, advanced laser-assisted keratoplasty or stem cell-based therapies often involve expensive equipment and highly trained surgeons, limiting accessibility in low-income areas

- Addressing these affordability and accessibility issues through government initiatives, insurance support, and training programs is essential to expand treatment reach

- In addition, patient hesitation due to perceived surgical risks or lack of awareness about non-invasive alternatives can hinder adoption, particularly in rural or underserved populations

- Overcoming these challenges through cost reduction strategies, awareness campaigns, and expansion of ophthalmic care facilities will be vital for sustained market growth

- Regulatory hurdles and stringent clinical trial requirements for new treatments can delay product launches and limit availability, impacting overall market growth

- Limited infrastructure for corneal transplantation and post-operative care in developing regions continues to restrict treatment adoption and market penetration

Corneal Opacity Market Scope

The market is segmented on the basis of type, onset, treatment type, presentation, age, and end user.

- By Type

On the basis of type, the corneal opacity market is segmented into nebula, macula, and leucoma. The Leucoma segment dominated the market with the largest revenue share in 2024, driven by its severe vision-impairing nature that often necessitates surgical intervention. Patients with leucoma frequently experience significant scarring of the cornea, leading to blindness or highly reduced visual acuity, making treatment critical. Hospitals and specialty clinics prioritize leucoma cases for corneal transplantation and advanced laser therapies, contributing to its higher market share. Moreover, awareness campaigns and early diagnosis programs have increased patient inflow for severe opacity types, supporting segment dominance. The Leucoma segment’s prevalence in both developed and emerging regions further reinforces its market leadership. In addition, the demand for effective surgical outcomes and post-operative care has made leucoma management a key revenue driver for ophthalmic centers.

The Nebula segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing detection of mild to moderate corneal opacities in routine eye screenings. Nebula presents less severe vision impairment but often progresses to more serious conditions if untreated, creating a growing patient pool for early intervention treatments such as medication, patching, or temporary contact lenses. Rising awareness about preventive eye care and accessibility to ophthalmic centers are accelerating adoption of non-surgical treatments. Technological advancements in diagnostic imaging allow ophthalmologists to detect nebula more accurately, encouraging timely treatment and reducing the risk of progression. The Nebula segment also benefits from government-funded eye care programs in emerging markets, expanding its reach. Moreover, patient preference for less invasive treatments compared to surgery contributes to its rapid uptake.

- By Onset

On the basis of onset, the corneal opacity market is segmented into congenital and acquired. The Acquired segment dominated the market with the largest revenue share in 2024 due to higher incidence rates caused by infections, trauma, and inflammatory conditions. Acquired corneal opacities frequently require immediate clinical intervention, creating steady demand for surgical and therapeutic treatments in hospitals and specialty clinics. Post-injury or post-infection cases often necessitate follow-up care and advanced interventions, increasing treatment adoption. The segment benefits from growing awareness about eye health and access to ophthalmic care in both urban and semi-urban regions. In addition, advancements in corneal transplant technologies and non-surgical interventions contribute to the dominance of acquired opacity treatments. High patient inflow and recurring care needs further sustain revenue growth in this segment.

The Congenital segment is expected to witness the fastest growth rate from 2025 to 2032, driven by improved neonatal screening and early diagnosis programs. Early detection of congenital corneal opacity allows timely intervention with medications, patching, or surgeries, minimizing long-term visual impairment. Advances in pediatric ophthalmology and specialized care units in hospitals are supporting market growth. Awareness campaigns and government initiatives targeting childhood blindness are expanding the patient pool for congenital corneal opacity management. Technological innovations such as pediatric-friendly contact lenses and laser-assisted corrective procedures enhance treatment adoption. Early intervention strategies, combined with increased parental awareness, are propelling the segment’s rapid growth.

- By Treatment Type

On the basis of treatment type, the corneal opacity market is segmented into patching, temporary contact lens, medication, surgery, and others. The Surgery segment dominated the market with the largest revenue share of 45.7% in 2024, driven by its high efficacy in restoring vision in severe cases such as Leucoma or advanced Macula. Corneal transplantation and laser-assisted surgeries are widely adopted in hospitals and ophthalmic centers, making surgery the primary revenue-generating segment. Continuous technological advancements and high success rates of modern surgical procedures strengthen this segment’s market position. In addition, post-operative care and follow-up treatments increase service adoption, further contributing to revenue. Surgical interventions remain the preferred treatment for patients with significant vision loss, supporting segment dominance.

The Medication segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing preference for non-invasive treatments in early-stage or mild corneal opacities. Growing awareness about eye health and availability of advanced pharmacological therapies encourage adoption in both pediatric and adult populations. Rising investments in research and development for anti-inflammatory and anti-fibrotic eye medications are expanding treatment options. Patients and ophthalmologists increasingly opt for medication as a first-line therapy to delay or prevent the need for surgery. Moreover, improved accessibility of medications in emerging regions is driving adoption and accelerating segment growth.

- By Presentation

On the basis of presentation, the corneal opacity market is segmented into blindness, blurred vision, and glare. The Blindness segment dominated the market with the largest revenue share in 2024, driven by the critical need for vision-restoring interventions. Patients presenting with complete or near-complete vision loss are prioritized for surgical treatment, increasing revenue for hospitals and specialty clinics. The segment’s dominance is also supported by government initiatives for blindness prevention and rehabilitation programs. High prevalence of severe corneal opacities in aging populations and post-trauma cases contributes to steady market demand. Advanced surgical technologies and post-operative care services further reinforce revenue generation in this segment.

The Blurred Vision segment is expected to witness the fastest growth rate from 2025 to 2032 due to rising early diagnosis and intervention efforts. Patients with mild to moderate visual impairment seek corrective therapies, including medications, patching, and contact lenses, before conditions worsen. Increased awareness and regular eye screenings encourage early treatment adoption. Growth in outpatient ophthalmic clinics and teleophthalmology platforms also supports this segment. The focus on preserving vision and delaying progression to blindness drives rapid adoption of treatments for blurred vision. Technological innovations and non-invasive therapies further enhance market growth.

- By Age

On the basis of age, the corneal opacity market is segmented into children and adults. The Adults segment dominated the market with the largest revenue share in 2024, due to higher prevalence of acquired corneal opacities resulting from trauma, infections, or age-related conditions. Adults are more such asly to require surgical intervention and continuous follow-up care, driving revenue in hospitals and specialty clinics. Increased health awareness and disposable income enable adults to seek advanced treatment options. Post-operative care, repeat procedures, and pharmacological therapies further strengthen market dominance.

The Children segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by neonatal screening programs and rising awareness of congenital corneal opacity. Early interventions such as patching, medications, and pediatric surgeries are increasingly adopted to prevent long-term vision impairment. Pediatric ophthalmology advancements and government initiatives targeting childhood blindness expand treatment accessibility. Growth in specialized pediatric eye clinics and teleophthalmology services supports segment growth. Early detection and non-invasive treatment adoption contribute to rapid expansion of the children’s segment.

- By End User

On the basis of end user, the corneal opacity market is segmented into hospitals, specialty clinics, ophthalmic centres, and ambulatory surgical centres. The Hospitals segment dominated the market with the largest revenue share in 2024, driven by availability of advanced surgical facilities, trained ophthalmologists, and post-operative care services. Hospitals cater to a high volume of patients with severe corneal opacities requiring complex interventions. Comprehensive care and rehabilitation services further reinforce the segment’s dominance.

The Specialty Clinics segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing adoption of outpatient and minimally invasive treatments. Specialty clinics offer personalized care, faster appointment scheduling, and focused ophthalmic expertise. Rising patient preference for convenient and specialized services supports segment growth. Teleophthalmology integration and advanced diagnostic tools further enhance treatment accessibility. In addition, government programs and awareness campaigns channel patients to specialty clinics for early-stage management, accelerating market expansion.

Corneal Opacity Market Regional Analysis

- North America dominated the corneal opacity market with the largest revenue share of 39.2% in 2024, attributed to advanced healthcare infrastructure, higher adoption of cutting-edge surgical solutions, and strong presence of key ophthalmic companies

- Patients and healthcare providers in the region prioritize timely diagnosis, advanced surgical interventions, and post-operative care, contributing to the high adoption of corneal opacity treatments in hospitals and specialty clinics

- This widespread adoption is further supported by higher healthcare expenditure, a well-established network of ophthalmologists, and the presence of key market players offering innovative corneal transplant and laser-assisted surgical solutions, establishing the region as a leader in corneal opacity management for both congenital and acquired cases

U.S. Corneal Opacity Market Insight

The U.S. corneal opacity market captured the largest revenue share in 2024 within North America, fueled by advanced healthcare infrastructure and high awareness of eye care. Patients increasingly prioritize early diagnosis and access to specialized treatments such as corneal transplantation and laser-assisted surgeries. The growing prevalence of acquired corneal opacities, coupled with high healthcare expenditure, further propels the market. Moreover, the availability of experienced ophthalmologists and advanced surgical technologies significantly contributes to market expansion. The strong presence of key players offering innovative solutions also reinforces the U.S. market leadership.

Europe Corneal Opacity Market Insight

The Europe corneal opacity market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of corneal diseases and rising awareness of eye health. Urbanization, better access to ophthalmic care, and government-supported vision screening programs are fostering the adoption of treatment options. European patients are also drawn to advanced surgical procedures and minimally invasive therapies. The region is experiencing significant growth across hospitals, specialty clinics, and ophthalmic centers, with treatments being incorporated into both new patient programs and follow-up care protocols.

U.K. Corneal Opacity Market Insight

The U.K. corneal opacity market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising patient awareness and the increasing trend of early intervention for vision impairment. Concerns regarding vision loss and quality of life are encouraging both adults and parents of children with congenital opacity to seek timely treatment. The U.K.’s adoption of advanced ophthalmic technologies, alongside strong healthcare infrastructure and government-supported eye health programs, is expected to continue stimulating market growth.

Germany Corneal Opacity Market Insight

The Germany corneal opacity market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of eye health and demand for technologically advanced ophthalmic solutions. Germany’s well-developed healthcare system, emphasis on medical innovation, and strong ophthalmologist network promote adoption of surgical and non-surgical treatments. Integration of diagnostic imaging, laser-assisted procedures, and advanced post-operative care is becoming increasingly prevalent, with patients showing a preference for precise, safe, and effective treatment solutions.

Asia-Pacific Corneal Opacity Market Insight

The Asia-Pacific corneal opacity market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing prevalence of corneal diseases, rising healthcare awareness, and improving access to ophthalmic care in countries such as China, Japan, and India. The region’s growing inclination towards early diagnosis and modern treatment options, supported by government initiatives for blindness prevention, is driving adoption. Furthermore, as APAC develops advanced ophthalmic facilities and affordable treatment solutions, the accessibility of care is expanding to a wider patient base.

Japan Corneal Opacity Market Insight

The Japan corneal opacity market is gaining momentum due to the country’s advanced healthcare system, aging population, and high demand for quality eye care. The Japanese market places a significant emphasis on early diagnosis and effective intervention, with adoption driven by the increasing number of specialized ophthalmic centers. Integration of modern diagnostic and surgical technologies, along with post-operative care services, is fueling growth. Moreover, Japan’s aging population is such asly to spur demand for precise, patient-friendly treatment options for both congenital and acquired corneal opacity cases.

India Corneal Opacity Market Insight

The India corneal opacity market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding middle class, rising healthcare awareness, and improving access to ophthalmic services. India is one of the largest markets for corneal opacity treatments, with growing adoption across hospitals, specialty clinics, and ophthalmic centers. Government initiatives for blindness prevention, urbanization, and availability of affordable surgical and non-surgical solutions are key factors propelling the market in India. The presence of skilled ophthalmologists and increasing eye care programs further support market growth.

Corneal Opacity Market Share

The Corneal Opacity industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Alcon Inc. (Switzerland)

- Bausch & Lomb (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Zeimer Ophthalmic Systems AG (Switzerland)

- Optovue, Inc. (U.S.)

- Argus Biomedical Pty Ltd (Australia)

- CorNeat Vision Ltd (Israel)

- Presbia (Ireland)

- Keramed (U.S.)

- MB Research Laboratories, Inc. (U.S.)

- AJL Ophthalmic S.A. (Spain)

- Artivion, Inc (U.S.)

- Organogenesis Inc. (U.S.)

- AbbVie Inc (U.S.)

- Glaukos Corporation (U.S.)

- Exactech (U.S.)

- KOHLER GMBH & CO. KG. (Germany)

- Aurolab (India)

What are the Recent Developments in Global Corneal Opacity Market?

- In September 2025, Researchers at the LV Prasad Eye Institute (LVPEI) in Hyderabad, in collaboration with the Indian Institute of Technology Guwahati (IIT-Guwahati), have developed a new technology to grow healthier artificial corneal cells in laboratories. This innovation aims to address the global shortage of donor corneas, potentially enhancing the availability of corneal tissues for transplantation and improving outcomes for patients in need of vision restoration

- In May 2025, Alcon announced that the U.S. Food and Drug Administration (FDA) approved its new eye drop treatment, Tryptyr, for dry eye disease (DED). Tryptyr demonstrated effectiveness in late-stage trials, showing natural tear production as early as the first day of use by stimulating corneal sensory nerves. DED affects approximately 38 million people in the U.S., yet fewer than 10% of diagnosed individuals receive prescription treatments

- In September 2024, Researchers at AIIMS and IIT-Delhi developed a bioengineered cornea using tissue from donor corneas previously deemed unfit for transplantation. This innovation aims to address the shortage of donor corneas and provide a viable alternative for patients requiring corneal transplants

- In June 2024, A 91-year-old man in the UK became the first patient to receive an artificial cornea through a pioneering 'single stitch' surgery. This procedure, involving the attachment of a contact lens-such as artificial cornea with a single stitch and a gas bubble, offers a potential solution to the global shortage of human cornea donors

- In March 2024, A new AI pipeline has been developed to detect corneal opacities using anterior segment video frames. This deep convolutional neural network model enhances diagnostic accuracy and efficiency, facilitating early detection and treatment planning for corneal opacity patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.