Global Crigler Najjar Syndrome Treatment Market

Market Size in USD Million

USD

150.50 Million

USD

232.72 Million

2024

2032

USD

150.50 Million

USD

232.72 Million

2024

2032

| 2025 - 2032 | |

| USD 150.50 Million | |

| USD 232.72 Million | |

| % | |

|

Crigler-Najjar Syndrome Treatment Market Size

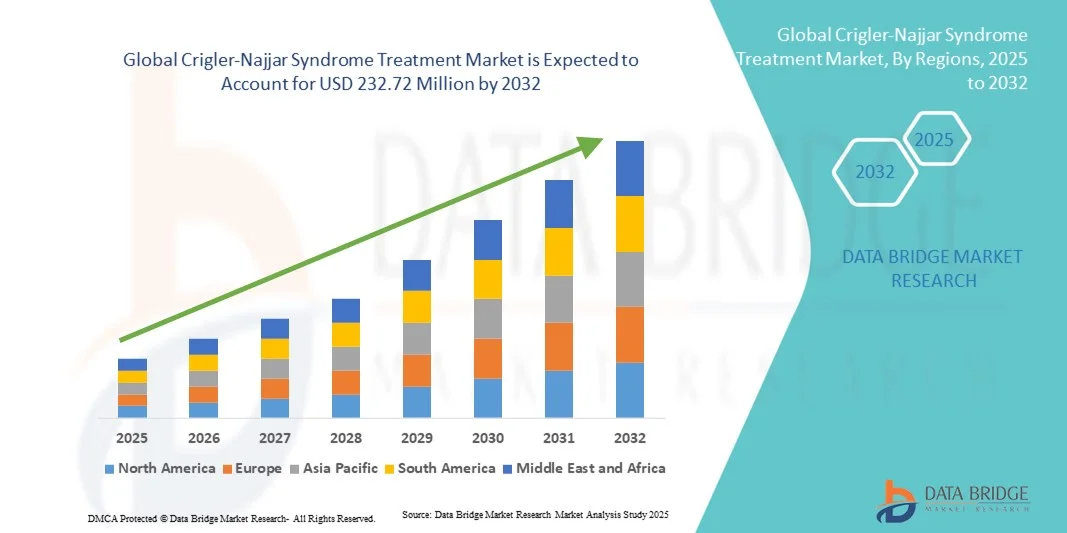

- The global Crigler-Najjar Syndrome treatment market size was valued at USD 150.50 million in 2024 and is expected to reach USD 232.72 million by 2032, at a CAGR of 5.60% during the forecast period

- The market growth is largely fueled by advancements in medical research, increasing awareness about the syndrome, and the development of innovative treatment approaches, including gene therapy and enzyme replacement therapy

- Furthermore, rising demand for effective therapies and supportive care for patients with Crigler-Najjar Syndrome is driving investments in novel medications and treatment modalities, accelerating the uptake of CNS treatments and significantly boosting the industry's growth

Crigler-Najjar Syndrome Treatment Market Analysis

- Crigler-Najjar Syndrome (CNS) treatments, including medications and liver transplantation options, are increasingly critical in managing this rare genetic disorder characterized by high levels of unconjugated bilirubin, with treatments improving patient survival and quality of life across pediatric and adult populations

- The escalating demand for CNS treatments is primarily driven by advancements in medical research, rising awareness about the syndrome, and the development of innovative therapies such as gene therapy and enzyme replacement therapy

- North America dominated the CNS treatment market in 2024 with the largest revenue share of 43%, supported by high healthcare expenditure, advanced medical infrastructure, and a strong presence of key pharmaceutical and biotech players developing targeted therapies for rare diseases

- Asia-Pacific is expected to be the fastest-growing region in the CNS treatment market during the forecast period, due to increasing healthcare investments, government initiatives for rare disease management, and improved access to specialized treatment centers

- Medication segment dominated the CNS treatment market in 2024 with a market share of 58.2%, driven by the use of bilirubin-lowering drugs and supportive therapies, which are easier to administer and widely adopted in both hospital and homecare settings

Report Scope and Crigler-Najjar Syndrome Treatment Market Segmentation

|

Attributes |

Crigler-Najjar Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Crigler-Najjar Syndrome Treatment Market Trends

Advancements in Gene Therapy and Personalized Medicine

- A significant and accelerating trend in the global CNS treatment market is the development of gene therapy and personalized medicine approaches, aiming to provide long-term or curative solutions by targeting the underlying UGT1A1 enzyme deficiency

- For instance, investigational therapies such as ENTR-101 and AAV-mediated gene replacement therapies are showing promising early-stage clinical results, offering potential one-time treatments for patients with CNS Type I

- Personalized medicine approaches, including tailored dosing of bilirubin-lowering drugs based on patient genotype, are enhancing treatment efficacy and reducing adverse effects, improving patient outcomes

- The integration of precision medicine with conventional therapies allows clinicians to optimize treatment plans, combining medications, phototherapy, and transplantation when necessary, creating a more effective care pathway

- This trend toward gene-based and individualized treatment solutions is reshaping expectations for CNS management, encouraging pharmaceutical companies to focus on rare disease innovation

- The growing interest in curative and precision therapies is driving investment in research and development, with multiple biotech firms actively pursuing clinical trials and regulatory approvals

Crigler-Najjar Syndrome Treatment Market Dynamics

Driver

Increasing Awareness and Early Diagnosis of Rare Diseases

- The rising awareness of Crigler-Najjar Syndrome among healthcare providers and patients is a key driver of market growth, facilitating early diagnosis and timely intervention to prevent severe complications

- For instance, specialized rare disease centers and awareness programs in North America and Europe are improving early screening for bilirubin levels in neonates, leading to higher treatment adoption rates

- As patients and caregivers become more informed about available therapies, demand for both conventional and emerging treatments increases, driving market expansion

- Government initiatives and rare disease advocacy campaigns are also promoting better access to CNS treatment options, particularly in regions with growing healthcare infrastructure

- Early diagnosis coupled with treatment accessibility ensures improved patient outcomes, motivating further research and investment by pharmaceutical and biotech companies

- Expansion of telemedicine and digital health platforms is enabling remote consultation and monitoring, increasing treatment reach for patients in underserved areas

- Strategic partnerships between pharmaceutical companies and healthcare providers are enhancing patient support programs, ensuring better adherence to therapy and long-term disease management

Restraint/Challenge

High Treatment Costs and Limited Accessibility

- The high cost of advanced therapies, including gene therapy and liver transplantation, poses a significant barrier to widespread adoption of CNS treatments, particularly in developing countries

- For instance, the estimated cost of gene therapy for CNS can exceed several hundred thousand USD per patient, making it inaccessible to many families without insurance or government support

- Limited availability of specialized treatment centers and trained healthcare professionals in certain regions restricts patient access to optimal care

- While conventional medications and phototherapy are more affordable, they often require lifelong management and frequent hospital visits, which can be burdensome for families

- Addressing these challenges through cost reduction strategies, expanded healthcare coverage, and development of more accessible treatment facilities is crucial for sustained market growth

- Regulatory hurdles and lengthy approval processes for novel gene therapies can delay market entry, limiting patient access to innovative treatments

- Supply chain constraints for specialized medications and biologics can impact treatment availability, particularly in regions with underdeveloped healthcare logistics

Crigler-Najjar Syndrome Treatment Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the CNS treatment market is segmented into Crigler-Najjar Syndrome Type I and Crigler-Najjar Syndrome Type II. The CNS Type I segment dominated the market in 2024 with the largest revenue share of 61%, due to its severe clinical manifestation, including complete absence of UGT1A1 enzyme activity. Patients with Type I require continuous therapies such as phototherapy, liver transplantation, and emerging gene therapies, increasing treatment adoption. The high morbidity risk associated with untreated Type I drives demand for specialized care and continuous monitoring. Pharmaceutical and biotech companies focus heavily on this segment due to its higher unmet medical need. Early diagnosis and specialized treatment centers in North America and Europe reinforce its dominance. In addition, Type I’s complexity creates opportunities for novel treatment development and clinical trials.

The CNS Type II segment is anticipated to witness the fastest growth rate of 8.9% from 2025 to 2032, fueled by rising awareness, improved diagnostic capabilities, and expanding healthcare access in emerging markets. Although milder, Type II patients benefit from pharmacological interventions such as bilirubin-lowering drugs. Awareness programs and government initiatives are increasing diagnosis rates and treatment uptake. The lower treatment burden compared to Type I allows adoption in homecare and outpatient settings. Emerging therapies and ongoing research in Type II management further accelerate market growth. Growing patient registries support improved treatment outcomes and adoption.

- By Treatment

On the basis of treatment, the CNS market is segmented into medication and surgery. The medication segment dominated the market in 2024 with a share of 58.2%, driven by widespread use of bilirubin-lowering drugs, ursodeoxycholic acid, and supportive therapies. Medications are preferred due to their non-invasive nature, ease of administration, and suitability for hospital and homecare settings. Phototherapy combined with pharmacological treatments improves outcomes and delays transplantation in some cases. Several established drug manufacturers focus on rare disease therapies, strengthening this segment’s share. Continuous patient monitoring and availability of oral medications enhance adherence and convenience. The segment benefits from increasing awareness of rare disease pharmacotherapy.

The surgery segment, including liver transplantation, is expected to witness the fastest growth rate of 9.2% from 2025 to 2032, driven by advances in transplant techniques, higher survival rates, and increased accessibility in emerging regions. Surgery is the definitive treatment for severe Type I cases. Awareness among healthcare providers about long-term benefits is increasing. Expansion of specialized transplant centers and rising insurance coverage support adoption. Surgical innovation, including minimally invasive liver transplant methods, boosts patient acceptance. Government initiatives and NGO programs also facilitate access in developing countries.

- By Route of Administration

On the basis of route of administration, the CNS treatment market is segmented into oral and injectable. The oral segment dominated the market in 2024 with a share of 65%, due to convenience in administering bilirubin-lowering drugs at home. Oral therapies improve patient adherence, reduce hospital visits, and are widely preferred for long-term management. Hospitals and retail pharmacies facilitate easy distribution. Oral medications are suitable for both Type I and Type II patients. The segment benefits from strong patient support programs. Continuous product development ensures improved efficacy and safety.

The injectable segment is expected to witness the fastest growth rate of 10.1% from 2025 to 2032, fueled by novel enzyme replacement therapies and gene therapy delivery systems. Injectable treatments offer higher efficacy for severe Type I patients. Adoption is increasing in specialized centers. Growing clinical trials for biologics and gene therapies accelerate segment growth. Injectable therapy provides options for patients not responding to oral medications. Regulatory approvals for advanced injectables support market expansion.

- By End-Users

On the basis of end-users, the CNS treatment market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market in 2024 with a 58% share, driven by the need for specialized care, continuous phototherapy, monitoring of bilirubin levels, and complex therapies such as liver transplantation. Hospitals provide comprehensive care including diagnostics, emergency intervention, and long-term treatment. Hospitals are equipped with trained specialists for rare diseases. This makes them the primary choice for severe Type I patients. Centralized care ensures better outcomes and higher treatment adherence. Hospital-based patient support programs further strengthen this segment.

The homecare segment is expected to witness the fastest growth rate of 11.3% from 2025 to 2032, due to portable phototherapy units, oral medications, and telehealth monitoring solutions. Homecare reduces patient burden and lowers treatment costs. It increases accessibility in regions with limited hospital infrastructure. Caregiver training and patient education programs support treatment adherence. Remote monitoring ensures safety and effectiveness. Expanding e-health platforms facilitate growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the CNS treatment market is segmented into hospital pharmacies, retail pharmacies, and others. The hospital pharmacies segment dominated the market in 2024 with a share of 62%, as most medications and therapies are dispensed in hospitals with continuous monitoring. Hospital pharmacies ensure proper storage, compliance, and access to new or experimental therapies. Centralized distribution facilitates patient adherence. The presence of specialist pharmacists enhances treatment guidance. Hospitals remain the primary point for rare disease medication access. Patient support programs strengthen this segment’s dominance.

The retail pharmacies segment is expected to witness the fastest growth rate of 10.5% from 2025 to 2032, driven by increasing availability of oral medications and supportive therapies. Patient preference for convenient access boosts growth. Expansion of pharmacy networks and e-pharmacy platforms facilitates wider distribution. Retail access improves adherence to prescribed therapies. This segment is critical for emerging markets where hospital access is limited. Growth is supported by homecare integration and telehealth adoption.

Crigler-Najjar Syndrome Treatment Market Regional Analysis

- North America dominated the CNS treatment market in 2024 with the largest revenue share of 43%, supported by high healthcare expenditure, advanced medical infrastructure, and a strong presence of key pharmaceutical and biotech players developing targeted therapies for rare diseases

- The region benefits from well-established rare disease centers and specialized hospitals that provide continuous monitoring, phototherapy, and access to liver transplantation, ensuring comprehensive care for CNS patients. Early diagnosis through neonatal screening programs and growing awareness among healthcare providers and patients further supports treatment adoption and improves outcomes.

- Increasing investment in research and development for gene therapy and enzyme replacement therapies is accelerating innovation and expanding the treatment pipeline in North America

U.S. Crigler-Najjar Syndrome Treatment Market Insight

The U.S. CNS treatment market captured the largest revenue share of 38% in 2024, driven by advanced healthcare infrastructure, widespread awareness of rare diseases, and access to specialized treatment centers. Patients benefit from comprehensive care including phototherapy, medication, and liver transplantation, supported by well-established hospitals and neonatal screening programs. Increasing investment in gene therapy and enzyme replacement therapies is accelerating the availability of innovative treatments. Telemedicine and digital health platforms are improving access for patients in remote areas. Strong insurance coverage and reimbursement policies further support treatment affordability. The growing focus on rare disease research and clinical trials is fostering continued market expansion in the U.S.

Europe Crigler-Najjar Syndrome Treatment Market Insight

The Europe CNS treatment market is projected to expand at a substantial CAGR during the forecast period, driven by robust healthcare infrastructure, rare disease awareness programs, and supportive regulatory frameworks. Countries such as Germany, France, and Italy are witnessing growth due to advanced diagnostics and increasing availability of specialized therapies. Government initiatives to improve access to orphan drugs and rare disease management programs are boosting treatment adoption. Hospitals and specialty clinics play a key role in delivering therapies and monitoring patients. The integration of advanced phototherapy units and hospital-based pharmacological care contributes to improved outcomes. Rising patient advocacy and collaborations between pharma companies and healthcare providers support market growth.

U.K. Crigler-Najjar Syndrome Treatment Market Insight

The U.K. CNS treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by increasing awareness of rare diseases, growing access to specialized treatment centers, and strong neonatal screening programs. Homecare and hospital-based phototherapy units are expanding, making treatments more accessible. The government’s support for orphan drugs and rare disease research facilitates access to advanced medications and therapies. Collaboration between hospitals, specialty clinics, and pharmaceutical companies is enhancing patient care and adherence. Increasing focus on early diagnosis and intervention is driving treatment uptake. The rising number of clinical trials in the U.K. also contributes to market momentum.

Germany Crigler-Najjar Syndrome Treatment Market Insight

The Germany CNS treatment market is expected to expand at a considerable CAGR during the forecast period, driven by advanced healthcare facilities, strong R&D capabilities, and awareness of rare diseases. Hospitals and specialty clinics are equipped to deliver comprehensive care including phototherapy, medication, and liver transplantation. Early diagnosis programs and government initiatives to support orphan drugs enhance patient access. Increasing adoption of precision medicine and gene therapy for severe Type I cases is boosting market growth. Germany’s strong healthcare funding and high patient awareness further support treatment uptake. The focus on integrating digital health platforms for monitoring and follow-up care is also accelerating adoption.

Asia-Pacific Crigler-Najjar Syndrome Treatment Market Insight

The Asia-Pacific CNS treatment market is poised to grow at the fastest CAGR of 12% during the forecast period of 2025 to 2032, driven by improving healthcare infrastructure, rising awareness of rare diseases, and increasing government initiatives in countries such as China, Japan, and India. Expansion of specialized hospitals, homecare services, and telemedicine platforms is increasing treatment accessibility. Rising disposable incomes and healthcare spending support adoption of innovative therapies, including gene therapy and enzyme replacement treatments. Patient advocacy programs and neonatal screening initiatives are improving early diagnosis rates. Collaboration between domestic pharmaceutical companies and global biotech firms enhances treatment availability. Growth in urban centers and increasing rare disease research also contribute to rapid market expansion.

Japan Crigler-Najjar Syndrome Treatment Market Insight

The Japan CNS treatment market is gaining momentum due to the country’s advanced healthcare system, high patient awareness, and focus on rare disease management. Hospitals and specialty clinics are equipped to deliver phototherapy, medications, and liver transplantation. Integration of digital health solutions for monitoring bilirubin levels improves patient outcomes. The aging population and demand for accessible treatment options are further fueling market growth. Increasing investment in gene therapy and clinical trials supports the development of innovative treatments. Government support for orphan drugs and rare disease policies ensures patient access to advanced therapies.

India Crigler-Najjar Syndrome Treatment Market Insight

The India CNS treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare infrastructure, increasing awareness of rare diseases, and growing adoption of homecare and hospital-based therapies. Rising disposable incomes and government initiatives for rare disease management are enhancing access to medications and phototherapy devices. Domestic pharmaceutical companies are actively developing and distributing affordable therapies. Telemedicine and digital health programs are increasing treatment reach in remote areas. Collaboration between hospitals, specialty clinics, and NGOs is facilitating patient education and therapy adherence. The push toward improving neonatal screening programs is further boosting early diagnosis and treatment uptake.

Crigler-Najjar Syndrome Treatment Market Share

The Crigler-Najjar Syndrome Treatment industry is primarily led by well-established companies, including:

- Genethon (France)

- Hansa Biopharma AB (Sweden)

- Gilead Sciences, Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- AbbVie Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Vertex Pharmaceuticals Incorporated (U.S.)

- Biogen Inc. (U.S.)

- Amgen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

What are the Recent Developments in Global Crigler-Najjar Syndrome Treatment Market?

- In October 2025, Genethon and Hansa Biopharma reported promising data from the GNT-018-IDES trial, demonstrating the feasibility of using imlifidase as a pre-treatment to enable gene therapy in patients with pre-existing antibodies to AAV8. This approach allowed the administration of GNT-0003 gene therapy to a patient who had previously been ineligible due to AAV8 immunity

- In June 2025, during International Crigler-Najjar Day, the AFM-Téléthon organization highlighted the ongoing challenges faced by patients, who often remain under intensive phototherapy. The event also showcased advancements in gene therapy developed by Généthon, offering hope for a life without the need for prolonged UV lamp exposure

- In December 2024, Genethon and Hansa Biopharma initiated a Phase 2 trial (GNT-018-IDES) to evaluate the combination of imlifidase, an antibody-cleaving enzyme, with GNT-0003 gene therapy in patients with pre-existing anti-AAV8 antibodies. This approach aims to overcome immune responses that may hinder the effectiveness of gene therapy, potentially broadening its applicability

- In June 2023, researchers demonstrated that lipid nanoparticle-encapsulated mRNA encoding the UGT1A1 enzyme corrected bilirubin levels in a mouse model of Crigler-Najjar Syndrome. This approach offers a non-viral, potentially scalable alternative to traditional gene therapy, representing a promising avenue for future treatment strategies

- In January 2023, Genethon launched a pivotal clinical trial evaluating GNT-0003, an adeno-associated virus (AAV)-based gene therapy for Crigler-Najjar Syndrome. The open-label trial aims to assess the safety and efficacy of a single infusion of GNT-0003 in patients aged 10 years and older who require phototherapy. This marks a significant step toward providing a potential one-time treatment for this rare genetic disorder

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.