Global Data Centre Open Frame Rack Market

Market Size in USD Billion

USD

5.42 Billion

USD

10.89 Billion

2025

2033

USD

5.42 Billion

USD

10.89 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.42 Billion | |

| USD 10.89 Billion | |

| % | |

|

What is the Global Data Centre Open Frame Rack Market Size and Growth Rate?

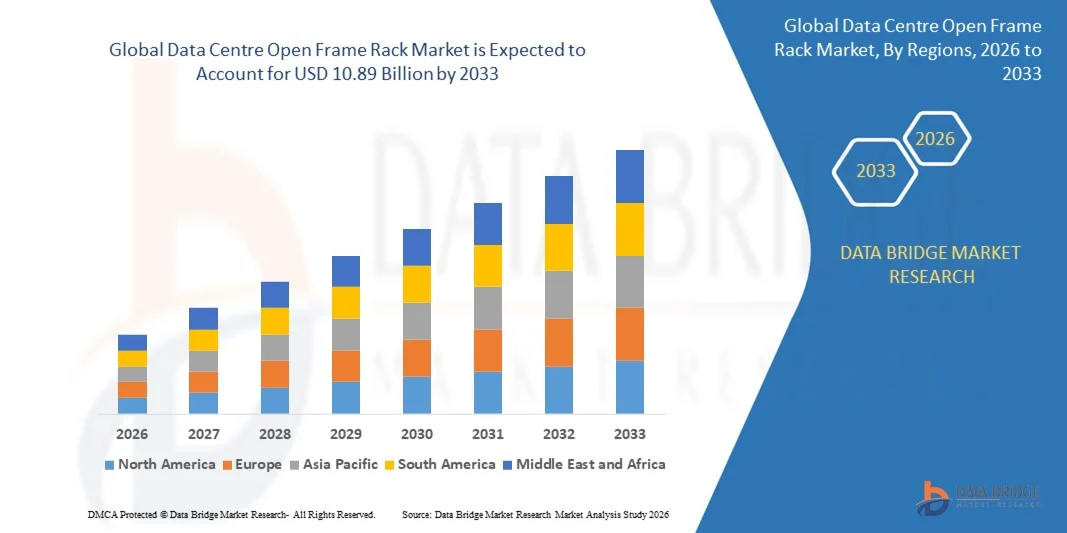

- The global data centre open frame rack market size was valued at USD 5.42 billion in 2025 and is expected to reach USD 10.89 billion by 2033, at a CAGR of9.10% during the forecast period

- Increasing proliferation of data centre colocation facilities across the globe, availability of low-cost rack solutions, increasing adoption of data centre solutions that enables easy and efficient management of data centre networks, rising usages of the solutions to support various servers in a secure environment along with increasing server density are some of the major as well as vital factors which will likely to augment the growth of the data centre open frame rack market

What are the Major Takeaways of Data Centre Open Frame Rack Market?

- Surging levels of investment for the development of durable rack enclosures along with increasing hyperscale deployments, prevalence of innovative monitoring solutions that enable remote monitoring of racks and equipment hosted in the racks which will further contribute by generating massive opportunities that will lead to the growth of the data centre open frame rack market

- North America dominated the data centre open frame rack market with a 43.69% revenue share in 2025, driven by rapid expansion of cloud infrastructure, hyperscale facilities, edge computing deployments, and rising adoption of high-density IT hardware across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 8.69% from 2026 to 2033, driven by rapid digitalization, cloud expansion, 5G rollout, edge computing adoption, and strong investments in new data centre facilities across China, Japan, India, Singapore, and South Korea

- The Solutions segment dominated the market with a 68.4% revenue share in 2025, driven by rising demand for high-density racks, cable-optimized structures, tool-less designs, PDUs, and mounting accessories essential for modern data centre buildouts

Report Scope and Data Centre Open Frame Rack Market Segmentation

|

Attributes |

Data Centre Open Frame Rack Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Data Centre Open Frame Rack Market?

Growing Adoption of High-Density, Scalable, and Cable-Optimized Open Frame Racks

- The data centre open frame rack market is witnessing rising adoption of high-density, scalable, and airflow-optimized rack systems designed to support modern IT loads, edge computing, and multi-rack deployments

- Manufacturers are introducing multi-purpose, tool-less, and modular rack designs that improve cable management, enhance cooling efficiency, and simplify server integration across hyperscale and enterprise facilities

- Increasing demand for cost-efficient, space-saving, and easily accessible rack structures is driving usage in colocation centres, enterprise data rooms, and cloud-native infrastructures

- For instance, Vertiv, Schneider Electric, Rittal, and Dell have expanded their open-frame rack portfolios with improved load-bearing capacity, enhanced PDUs, and integrated cable pathways for high-density deployments

- Growing need for faster installation, reduced operational complexity, and improved airflow management is accelerating the adoption of open-frame architectures

- As data centres shift toward scalable, modular, and high-density IT environments, Data Centre Open Frame Racks are expected to remain central to infrastructure modernization and efficient hardware integration

What are the Key Drivers of Data Centre Open Frame Rack Market?

- Rising demand for cost-effective, flexible, and easily configurable rack systems to support rapid IT equipment deployment across small, medium, and large data centres

- For instance, in 2025, Schneider Electric, Cisco, and Rittal enhanced their rack offerings to support edge computing equipment, hybrid cloud workloads, and AI-ready data environments

- Growing global expansion of cloud services, colocation facilities, and digital transformation initiatives is boosting rack installation across the U.S., Europe, and Asia-Pacific

- Advancements in rack design, material strength, thermal management, and mounting technologies have improved load capacity, equipment accessibility, and cooling efficiency

- Rising adoption of IoT devices, 5G infrastructure, and AI-driven workloads is creating demand for high-density, open-frame structures for quick deployment and improved accessibility

- With ongoing investments in data centre construction, product innovation, partnerships, and global distribution, the Data Centre Open Frame Rack market is expected to continue strong upward growth

Which Factor is Challenging the Growth of the Data Centre Open Frame Rack Market?

- High implementation costs associated with premium, heavy-duty, and high-load open-frame racks limit adoption among cost-sensitive enterprises and small data rooms

- For instance, during 2024–2025, fluctuations in steel prices, raw materials, and supply chain delays impacted rack production costs for several global manufacturers

- Strict data centre safety, load-rating, and infrastructure compliance requirements increase complexity for manufacturers and facility operators

- Limited awareness in emerging markets regarding rack standards, airflow requirements, and structured data centre design restricts optimal deployment

- Strong competition from enclosed racks, micro-data centre cabinets, and pre-configured modular solutions creates pressure on pricing and product differentiation

- To overcome these challenges, companies are focusing on cost-optimized manufacturing, regulatory compliance, user training, and scalable production models to expand global adoption of high-performance Data Centre Open Frame Racks

How is the Data Centre Open Frame Rack Market Segmented?

The market is segmented on the basis of component, rack height, rack width, data centre size, vertical, application, rack units, and end user.

- By Component

On the basis of component, the data centre open frame rack market is segmented into Solutions and Services. The Solutions segment dominated the market with a 68.4% revenue share in 2025, driven by rising demand for high-density racks, cable-optimized structures, tool-less designs, PDUs, and mounting accessories essential for modern data centre buildouts. Enterprises, colocation providers, and hyperscale operators are increasingly adopting advanced open-frame rack systems to support cloud computing, AI servers, edge workloads, and hybrid IT infrastructure. These racks provide better airflow, reduced installation time, and improved scalability—making them a preferred choice for new builds as well as data centre expansions.

The Services segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by increasing requirement for installation, integration, maintenance, remote monitoring, and lifecycle management. Growing complexity in high-density deployments and edge data centres continues to boost demand for professional services globally.

- By Rack Height

On the basis of rack height, the market is segmented into 42U and Below, 43U Up to 52U, and Above 52U. The 43U Up to 52U segment dominated the market with a 54.2% share in 2025, as it remains the industry standard for enterprise data centres, colocation facilities, and telecom rooms. These racks offer optimal height for cable routing, power distribution, and ease of maintenance, making them suitable for a wide range of servers, switches, and storage devices. Their balance of accessibility, load capacity, and compatibility with cooling systems drives extensive deployment across multi-rack environments.

The Above 52U segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by hyperscale and high-density data centres focused on maximizing floor efficiency, reducing footprint, and supporting dense AI, GPU, and cloud workloads. This trend aligns with growing rack-level optimization and modular data centre expansion.

- By Rack Width

On the basis of rack width, the market is segmented into 19 Inch, 23 Inch, and Others. The 19-inch segment dominated the market with a 61.7% share in 2025, as it remains the global industry standard for most IT, telecom, network, and server equipment. Its widespread compatibility, universal mounting design, and strong adoption across enterprise and colocation facilities drive significant demand. Manufacturers prefer 19-inch racks for ease of integration, standardized layouts, and cost-efficient deployment, making them the preferred choice across multiple infrastructure environments.

The 23-inch segment is projected to register the fastest CAGR from 2026 to 2033, supported by the need for enhanced cable management space, improved airflow pathways, and high-capacitance equipment accommodation. Growing adoption in telecom data centres, edge nodes, and facilities deploying larger power distribution units (PDUs) is boosting demand for wider open-frame rack configurations.

- By Data Centre Size

On the basis of data centre size, the market is segmented into Small and Mid-Sized Data Centres and Large Data Centres. The Large Data Centres segment dominated with a 58.9% share in 2025, driven by rapid expansion of hyperscale facilities, cloud providers, and large colocation operators investing heavily in scalable rack infrastructure. Open-frame racks support efficient cable management, optimized airflow, and cost-effective high-density server deployment, making them widely preferred in high-capacity facilities.

The Small and Mid-Sized Data Centres segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing digitalization among SMEs, rising adoption of edge computing, and the need for compact, easy-to-install rack systems. The growth of distributed data centre models and micro-data centre setups is further accelerating demand for modular open-frame racks.

- By Vertical

On the basis of vertical, the market is segmented into BFSI, Information Technology & Telecom, Government and Defence, Retail, Manufacturing, Healthcare, Energy & Utilities, and Others. The IT & Telecom segment dominated the market with a 33.7% share in 2025, supported by continuous data traffic growth, cloud expansion, 5G rollouts, and high-density server deployments. Open-frame racks are widely used to host networking, switching, and data processing equipment, making them essential in telecom hubs and core data centres.

The BFSI segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising investments in secure, scalable, and high-availability infrastructure to support digital banking, fintech integration, and AI-enabled analytics. BFSI institutions increasingly prefer open-frame racks for faster installation, efficient cabling, and reduced operational overhead.

• By Application

On the basis of application, the market is segmented into Networking, Servers, and Others. The Servers segment dominated with a 57.6% share in 2025, driven by large-scale deployment of compute nodes, AI servers, GPU racks, and storage systems across enterprise and hyperscale data centres. Open-frame racks are preferred for server workloads due to better airflow, accessibility, and flexibility in high-density environments.

The Networking segment is projected to record the fastest CAGR from 2026 to 2033, as edge facilities, telecom operators, and cloud service providers continue expanding routing, switching, and fibre distribution infrastructure. Rising adoption of SD-WAN, 5G core equipment, and multi-cloud environments further enhances demand for networking-focused open-frame racks.

- By Rack Units

On the basis of rack units, the market is segmented into Small, Medium, and Large. The Medium segment dominated with a 49.3% share in 2025, supported by its balanced configuration suitable for enterprise IT rooms, edge deployments, and colocation facilities. Medium rack units offer optimal load capacity, simplified cabling, and compatibility with networking, storage, and compute hardware.

The Large segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by hyperscale and cloud data centres demanding high-density server mounts for advanced workloads such as AI, deep learning, and real-time data analytics. Growing rack-level power density is further accelerating adoption.

- By End User

On the basis of end user, the market is segmented into Colocation Data Centres and Enterprise Data Centres. The Colocation Data Centres segment dominated with a 55.8% share in 2025, driven by rising demand for scalable IT space, multi-tenant infrastructure, and high-density server environments. Open-frame racks are preferred due to their airflow efficiency, flexibility, and cost-effectiveness for shared hosting environments.

The Enterprise Data Centres segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by increasing digital transformation, cloud-hybrid deployments, and modernization of legacy IT rooms. Enterprises are adopting open-frame racks to optimize floor space, reduce cooling costs, and enable faster hardware deployment.

Which Region Holds the Largest Share of the Data Centre Open Frame Rack Market?

- North America dominated the data centre open frame rack market with a 43.69% revenue share in 2025, driven by rapid expansion of cloud infrastructure, hyperscale facilities, edge computing deployments, and rising adoption of high-density IT hardware across the U.S. and Canada. Strong investments in AI-driven workloads, multi-cloud architectures, and digital transformation initiatives continue to accelerate rack installations across both enterprise and colocation environments

- Leading players are expanding open-frame rack portfolios through innovations in airflow optimization, cable management, modular assembly, and compatibility with AI/GPU servers. Regulatory emphasis on energy-efficient data centres, sustainability, and green IT infrastructure further strengthens regional market leadership

- High IT spending, strong network modernization initiatives, and rapid migration toward cloud-native architectures continue to fuel long-term growth

U.S. Data Centre Open Frame Rack Market Insight

The U.S. is the largest contributor in North America, supported by large-scale hyperscale data centre development from major cloud providers, growing enterprise modernization, and rising demand for rack-level scalability. Investments in AI training clusters, edge data centres, and colocation expansions are driving adoption of open-frame racks due to their superior cooling efficiency, ease of integration, and cost-effectiveness. Strong digital infrastructure, advanced manufacturing capabilities, and extensive retail/e-commerce penetration further boost market growth.

Canada Data Centre Open Frame Rack Market Insight

Canada contributes significantly to regional growth, driven by increasing cloud adoption, government digitalization programs, and expansion of colocation and telecom data centres. Data centre operators are increasingly deploying open-frame racks to support high-density servers, efficient airflow systems, and flexible configurations. Sustainability initiatives, rising electricity costs, and preference for modular, energy-efficient IT infrastructure support strong adoption across hyperscale and enterprise environments.

Asia-Pacific Data Centre Open Frame Rack Market

Asia-Pacific is projected to register the fastest CAGR of 8.69% from 2026 to 2033, driven by rapid digitalization, cloud expansion, 5G rollout, edge computing adoption, and strong investments in new data centre facilities across China, Japan, India, Singapore, and South Korea. Rising demand for scalable, energy-efficient, and cost-effective rack systems is accelerating deployment across hyperscale, enterprise, and telecom infrastructure. Growth in e-commerce, online services, fintech, AI-driven applications, and digital payments further boosts regional adoption of open-frame racks.

China Data Centre Open Frame Rack Market Insight

China is the largest contributor to Asia-Pacific, supported by the world’s fastest-growing data centre ecosystem, government-backed digital initiatives, and large-scale investments in hyperscale cloud regions. Increasing adoption of AI servers, high-density GPU racks, and advanced cooling technologies fuels strong demand for open-frame racks. Local manufacturing capacity and aggressive R&D investments strengthen domestic production and export competitiveness.

Japan Data Centre Open Frame Rack Market Insight

Japan shows steady growth due to rising demand for low-latency cloud services, advanced telecom networks, and modernization of traditional enterprise data centres. Strong focus on premium-quality infrastructure, energy efficiency, and compact designs drives adoption of open-frame racks. Regulatory emphasis on data protection and resilient IT architecture further supports market expansion.

India Data Centre Open Frame Rack Market Insight

India is emerging as a major growth hub, driven by digital infrastructure expansion, hyperscale investments, government cloud initiatives, and rising adoption of enterprise IT solutions. Increasing deployment of colocation and edge facilities boosts demand for flexible, modular open-frame racks. Growth in fintech, e-commerce, telecom, and digital services accelerates widespread adoption.

South Korea Data Centre Open Frame Rack Market Insight

South Korea contributes significantly due to strong demand for high-performance computing, 5G infrastructure, and large-scale digital platforms. Increasing installation of AI servers, data-intensive applications, and cloud-native workloads drives preference for open-frame racks with optimized thermal efficiency and cable routing. Innovation in design, premium IT infrastructure, and technology-driven consumer markets further propel regional growth.

Which are the Top Companies in Data Centre Open Frame Rack Market?

The data centre open frame rack industry is primarily led by well-established companies, including:

- Schneider Electric (France)

- Hewlett Packard Enterprise Development LP (U.S.)

- IBM Corporation (U.S.)

- Dell (U.S.)

- Cisco (U.S.)

- Eaton Corporation plc (Ireland)

- Rittal Systems Ltd. (Germany)

- FUJITSU (Japan)

- Vertiv Group Corp. (U.S.)

- AGC Networks Limited (India)

- LEGRAND Group (France)

- Oracle Corporation (U.S.)

- Belden Inc. (U.S.)

- nVent (U.S.)

- Panduit (U.S.)

- Great Lakes Data Racks & Cabinets (U.S.)

- Tripp Lite (U.S.)

- IMS Engineered Products (U.S.)

- Rahi Systems (U.S.)

- Chatsworth Products (U.S.)

What are the Recent Developments in Global Data Centre Open Frame Rack Market?

- In May 2025, Vertiv introduced an advanced 800 VDC power architecture designed for next-generation AI factories, featuring centralized rectifiers and rack-level converters that significantly reduce copper usage, and this advancement is expected to enhance energy efficiency and lower infrastructure costs

- In April 2025, Legrand launched its Fiber Express Ship Program, offering rapid next-day dispatch of high-bandwidth fiber assemblies to minimize deployment delays, and this initiative is set to help data center operators accelerate network buildouts

- In March 2024, Eaton launched its SmartRack modular data center solution in North America, delivering rapidly deployable units equipped with cooling systems, IT racks, and service enclosures supporting up to 150 kW of IT load, and this development aims to address the increasing demand for edge computing and AI-ready infrastructure

- In August 2022, Vertiv Group Corp. rolled out the Vertiv MegaMod Plus and MegaMod turnkey prefabricated modular data center systems across the EMEA region, offering scalable units of 0.5 or 1 megawatt supporting IT loads up to 2 megawatts or more, and this solution is intended to help organizations expand capacity quickly and efficiently

- In April 2022, Rittal GmbH & Co. KG entered into a U.S. partnership with TD SYNNEX to distribute IT rack enclosures, accessories, and infrastructure solutions to technology customers, and this collaboration is expected to expand Rittal’s reach within the IT ecosystem

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.