Global Digital Pathology Solutions For Oncology Market

Market Size in USD Million

USD

960.60 Million

USD

2,000.85 Million

2024

2032

USD

960.60 Million

USD

2,000.85 Million

2024

2032

| 2025 - 2032 | |

| USD 960.60 Million | |

| USD 2,000.85 Million | |

| % | |

|

Digital Pathology Solutions for Oncology Market Analysis

The global digital pathology solutions for oncology market is expanding due to the rising global cancer burden, with an estimated 19.3 million new cases and 10 million deaths in 2020. The demand for digital pathology is driven by the need for faster, more accurate cancer diagnoses and the integration of AI technologies for tumor detection. Digital pathology also supports telepathology, addressing the shortage of pathologists in certain regions. These advancements are transforming oncology diagnostics and research, enhancing efficiency and accuracy in cancer care.

Digital Pathology Solutions for Oncology Market Size

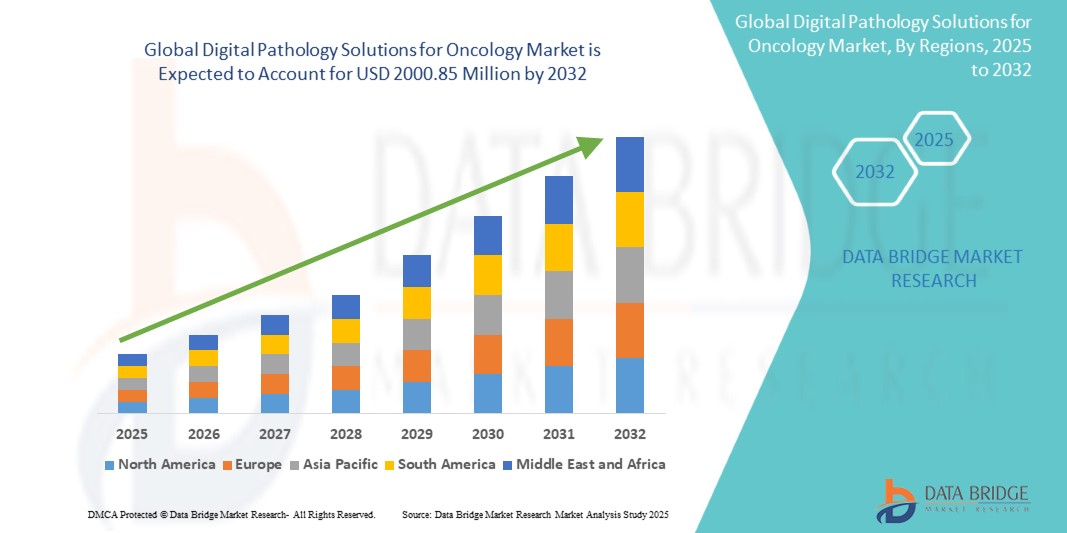

Global digital pathology solutions for oncology market size was valued at USD 960.60 million in 2024 and is projected to reach USD 2000.85 million by 2032, with a CAGR of 9.60% during the forecast period of 2025 to 2032. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

Digital Pathology Solutions for Oncology Market Trends

“Shift to Whole Slide Imaging (WSI)”

The shift to Whole Slide Imaging (WSI) is a prominent trend in the digital pathology space, where WSI technology is increasingly being adopted as the gold standard for analyzing tissue samples. WSI enables the capture of entire tissue slides in high resolution, offering a more detailed and comprehensive view compared to traditional microscopy. This advancement allows pathologists to perform more accurate tumor analysis, enhancing diagnostic capabilities. As WSI becomes more prevalent, reliance on traditional, time-consuming microscopy methods is diminishing, further streamlining the diagnostic process and improving the overall quality of cancer diagnosis.

Report Scope and Digital Pathology Solutions for Oncology Market Segmentation

|

Attributes |

Digital Pathology Solutions for Oncology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

U.S., Canada, Mexico, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa, Brazil, Argentina, Rest of South America |

|

Key Market Players |

Koninklijke Philips N.V. (Netherlands), GE HealthCare (U.S.), FUJIFILM Corporation (Japan), Hamamatsu Photonics K.K. (Japan), F. Hoffmann-La Roche Ltd (U.S.), Leica Biosystems (Germany), Indica Labs (U.S.), PathAI (U.S.), Apollo Pathology (India), Visiopharm (Denmark), CureMetrix (U.S.), Thermo Fisher Scientific Inc. (U.S.), Agilent Technologies (U.S.), Microscan Systems, Inc. (U.S.), and Quip Labs (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Digital Pathology Solutions for Oncology Market Definition

Digital pathology solutions for oncology refer to advanced technologies and systems that digitize traditional pathology processes, enabling the acquisition, management, analysis, and sharing of high-resolution images of cancer tissue samples. These solutions support accurate tumor diagnosis, grading, and research by leveraging tools such as whole slide imaging (WSI), image analysis software, artificial intelligence (AI), and telepathology platforms.

Digital Pathology Solutions for Oncology Market Dynamics

Drivers

- Rising Prevalence of Cancer

The rising global cancer burden is a significant driver of the digital pathology solutions for oncology market, as the increasing prevalence of cancer necessitates more efficient and accurate diagnostic tools. According to the World Health Organization (WHO), there were over 19.3 million new cancer cases and 10 million cancer-related deaths globally in 2020. This alarming rate of cancer incidence has heightened the demand for advanced technologies that enable early detection, precise diagnosis, and effective treatment planning. Digital pathology, with its ability to provide high-resolution imaging, remote consultation through telepathology, and integration of AI for tumor analysis, addresses these needs by improving diagnostic accuracy and reducing delays. Furthermore, as the global healthcare system adapts to manage this growing burden, hospitals and laboratories are increasingly adopting digital pathology to enhance workflow efficiency and optimize patient outcomes, making it an essential tool in modern oncology care. For Instance, in February 2024, according to an article published by WHO, in 2022, there were around 20 million new cancer cases and 9.7 million deaths, with 53.5 million people living five years after diagnosis. About 1 in 5 people develop cancer, and 1 in 9 men and 1 in 12 women die from it. The rising cancer burden is expected to drive the demand for advanced diagnostic solutions, such as digital pathology, to improve early detection and treatment outcomes.

- Increasing Adoption of Telepathology

The increasing adoption of telepathology is a key driver in the digital pathology solutions for oncology market, addressing the growing demand for remote diagnostics and expert opinions. Telepathology involves the digital transmission of high-resolution pathology images, allowing pathologists to analyze and diagnose cases remotely. This is particularly crucial in regions facing a shortage of skilled pathologists or where geographical barriers limit access to expert cancer care. By enabling seamless collaboration between pathologists, clinicians, and oncologists worldwide, telepathology reduces diagnostic delays and enhances the accuracy of cancer diagnoses. It also supports second opinions, improving confidence in treatment decisions and outcomes. As healthcare systems prioritize efficiency and accessibility, telepathology is becoming integral in oncology, helping hospitals and laboratories manage increasing cancer cases more effectively. The technology not only expands the reach of quality care but also improves workflows, making cancer diagnostics more streamlined and widely available. In November 2024, according to an article published by Signify Research, Signify Research is entering the telepathology services market, with Inify Laboratories announcing plans to expand into the UK, initially focusing on prostate cancer diagnostics. The company aims to open a lab by early 2026 and has secured SEK 150 million in funding to develop AI-driven services for gastrointestinal diagnostics. This expansion is expected to drive growth in telepathology services, addressing high sample volumes and diverse clinical needs.

Opportunities

- Increasing Integration with Artificial Intelligence (AI)

The integration of artificial intelligence (AI) in digital pathology is creating significant opportunities in the oncology field by revolutionizing tumor detection, classification, and prognostic analysis. AI-powered algorithms can analyze high-resolution pathology images with exceptional accuracy, identifying subtle patterns that may be missed by traditional methods. These advancements not only improve diagnostic precision but also significantly enhance the efficiency of workflows, enabling faster and more reliable cancer diagnoses. AI's ability to process large datasets supports detailed biomarker analysis, which is crucial for developing personalized oncology treatments tailored to individual patients. Additionally, AI-driven tools assist pathologists by automating routine tasks, allowing them to focus on complex cases and improving overall clinical decision-making. As healthcare systems globally adopt personalized medicine approaches, the demand for AI-integrated digital pathology solutions continues to grow, making it a transformative opportunity to elevate the quality and accessibility of cancer care worldwide.

- Increasing Partnerships with Healthcare Providers

Partnerships between digital pathology solution providers and healthcare institutions, such as hospitals, laboratories, and research institutes, present significant opportunities to expand the adoption of digital pathology technologies in oncology. These collaborations allow providers to integrate digital pathology systems into clinical settings, enhancing diagnostic workflows, improving accuracy, and reducing turnaround times. By working closely with healthcare providers, digital pathology companies can tailor their solutions to meet specific needs, ensuring better alignment with clinical practices. Research institutes benefit by gaining access to advanced technologies for cancer research and biomarker discovery, which can lead to new insights and treatment strategies. Furthermore, these partnerships can facilitate training programs for pathologists and medical professionals, ensuring a smooth transition to digital solutions. As a result, both parties can accelerate the adoption of cutting-edge technology, improve patient outcomes, and expand market reach, while also fostering innovation in cancer care. For Instance, in November 2024, according to an article published by Sectra AB, Sectra's digital pathology solution will be adopted by CH Béziers in France, becoming the third hospital in the region to choose Sectra. The platform will improve workflow efficiency, reduce variability in pathology reviews, and enhance patient care. This adoption offers Sectra an opportunity to further expand its presence in the French healthcare market and strengthen its role in digital pathology.

Restraints/Challenges

- High Implementation Costs

High implementation costs is a significant restraint in the global digital pathology solutions for oncology market, particularly for smaller healthcare facilities or those in developing regions. Digital pathology systems require substantial initial investments for purchasing high-resolution scanning equipment, software licenses, and infrastructure for data storage and analysis. Additionally, the integration of these systems often requires specialized training for pathologists and technical staff, further increasing costs. For smaller hospitals or clinics, especially in regions with limited healthcare budgets, these expenses can be prohibitively high. As a result, many institutions may delay or forgo adopting digital pathology solutions despite their potential benefits, such as improved diagnostic accuracy and efficiency. This financial barrier limits the reach of digital pathology technologies in underserved markets and may slow down the overall growth of the market. Therefore, cost-effective solutions, including government subsidies or financing options, may be essential to overcome this challenge and promote widespread adoption.

- Data Security and Privacy Concerns

Data security and privacy concerns are a significant challenge for the global digital pathology solutions for oncology market, as these technologies involve the transmission and storage of sensitive patient information, such as pathology images and medical records. Ensuring that these data are protected from cyber threats requires robust cybersecurity measures, including encryption, secure data storage, and frequent system updates. Compliance with stringent data protection regulations, such as HIPAA in the U.S. or GDPR in Europe, is crucial to safeguarding patient privacy and maintaining trust in digital health solutions. Any breach of data security, such as unauthorized access or data leakage, could have serious consequences, including legal penalties and loss of patient confidence. This risk may discourage healthcare providers from adopting digital pathology systems or delay their implementation. Therefore, developing and maintaining secure, compliant platforms is essential to fostering trust and enabling the widespread use of digital pathology solutions in oncology.

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Digital Pathology Solutions for Oncology Market Scope

The market is segmented on the basis of product, technology, application, and end-user. The growth amongst these segments will help you analyze meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Product

- Hardware

- Software

- Services

Technology

- Whole Slide Imaging (WSI)

- Quantitative Digital Pathology

- Artificial Intelligence (AI) in Digital Pathology

- Telepathology

Application

- Clinical Applications

- Research Applications

End-User

- Hospitals and Diagnostic Laboratories

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations (CROs)

Digital Pathology Solutions for Oncology Market Regional Analysis

The market is analyzed and market size insights and trends are provided by country, product, technology, application, and end-user as referenced above.

The countries covered in the market are U.S., Canada, Mexico, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, rest of Asia-Pacific, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, rest of Middle East and Africa, Brazil, Argentina, and rest of South America.

North America is expected to dominate the market due to the high prevalence of cancer, advanced healthcare infrastructure, and early adoption of digital technologies such as AI and telemedicine. Strong investments in research and development further drive innovation, supporting the region’s leadership in healthcare advancements.

Asia-Pacific is expected to be the fastest growing due to the rising cancer burden, increasing healthcare expenditure, growing adoption of digital technologies, and expanding awareness of advanced diagnostic tools.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points such as down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Digital Pathology Solutions for Oncology Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

Digital Pathology Solutions for Oncology Market Leaders Operating in the Market Are:

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- FUJIFILM Corporation (Japan)

- Hamamatsu Photonics K.K. (Japan)

- F. Hoffmann-La Roche Ltd (U.S.)

- Leica Biosystems (Germany)

- Indica Labs (U.S.)

- PathAI (U.S.)

- Apollo Pathology (India)

- Visiopharm (Denmark)

- CureMetrix (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies (U.S.)

- Microscan Systems, Inc. (U.S.)

- Quip Labs (U.S.)

Latest Developments in Digital Pathology Solutions for Oncology Market

- In September 2024, Roche has expanded its digital pathology open environment by integrating over 20 AI algorithms from eight new partners to enhance cancer research and diagnosis. This initiative will support pathologists and scientists with advanced AI tools, positioning Roche to further innovate in the digital pathology space and strengthen its leadership in oncology diagnostics

- In September 2024, Lunit has partnered with Roche to integrate its Lunit SCOPE PD-L1 22C3 TPS into Roche's navify Digital Pathology platform, marking the first deployment of Lunit's AI technology with Roche. This collaboration will provide pathologists and scientists with advanced tools for cancer research, contributing to Roche’s digital pathology ecosystem. For Lunit, this partnership offers an opportunity to expand its AI technology in oncology and strengthen its presence in the global market

- In June 2024, Quest Diagnostics has completed its acquisition of PathAI Diagnostics to accelerate the adoption of AI and digital pathology in cancer and disease diagnosis. This acquisition will enhance Quest’s diagnostic capabilities, enabling more accurate and efficient disease detection through advanced AI technologies

- In February 2024, Roche has signed an agreement with PathAI to exclusively collaborate on developing AI-powered digital pathology algorithms for companion diagnostics through Roche Tissue Diagnostics. This partnership will strengthen Roche's position in the companion diagnostics market, enhancing its AI capabilities in pathology and accelerating innovation in personalized medicine

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.