Global Whole Slide Imaging Market

Market Size in USD Billion

USD

1.20 Billion

USD

3.92 Billion

2024

2032

USD

1.20 Billion

USD

3.92 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.20 Billion | |

| USD 3.92 Billion | |

| % | |

|

Whole Slide Imaging Market Size

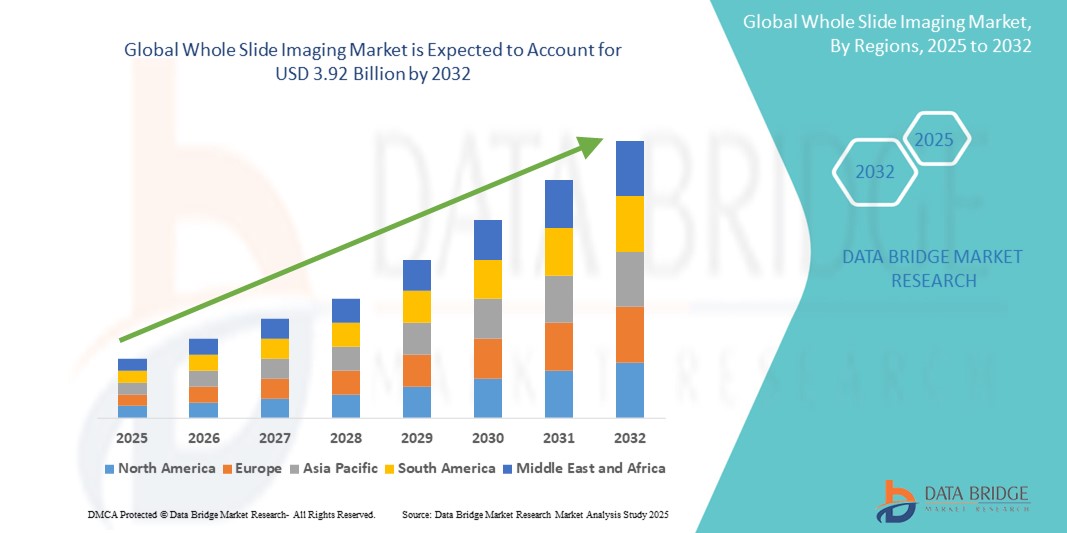

- The global whole slide imaging market size was valued at USD 1.20 billion in 2024 and is expected to reach USD 3.92 billion by 2032, at a CAGR of 15.90% during the forecast period

- The market growth is largely driven by the increasing adoption of digital pathology solutions, advancements in imaging technology, and the growing emphasis on precision diagnostics and remote pathology

- Furthermore, rising demand for efficient and high-throughput diagnostic workflows, combined with increasing investments in healthcare digitization and AI-based analysis tools, is establishing whole slide imaging as a central component in modern pathology practices. These converging factors are accelerating the adoption of WSI systems, thereby significantly boosting the industry's growth

Whole Slide Imaging Market Analysis

- Whole slide imaging (WSI), which enables high-resolution digitization of entire pathology slides, is becoming an essential tool in modern diagnostic workflows across clinical, research, and educational settings due to its efficiency, accuracy, and support for remote analysis

- The accelerating demand for whole slide imaging is primarily driven by the rising adoption of digital pathology, growing prevalence of chronic diseases requiring histopathological diagnosis, and increasing integration of AI and image analysis software in pathology labs

- North America dominated the whole slide imaging market with the largest revenue share of 60.3% in 2024, attributed to the early implementation of digital pathology systems, favorable regulatory frameworks, and strong healthcare infrastructure, with the U.S. leading in terms of technological adoption and investment in advanced diagnostic solutions.

- Asia-Pacific is expected to be the fastest growing region in the whole slide imaging market during the forecast period due to expanding healthcare access, increasing investments in medical infrastructure, and rising awareness of digital pathology’s benefits in diagnostic accuracy and workflow efficiency

- Telepathology segment dominated the whole slide imaging market with a market share of 40.5% in 2024, driven by its ability to enable remote diagnosis, expert consultations, and rapid sharing of pathology slides across geographic locations

Report Scope and Whole Slide Imaging Market Segmentation

|

Attributes |

Whole Slide Imaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Whole Slide Imaging Market Trends

“AI-Powered Pathology and Remote Diagnostics”

- A significant and accelerating trend in the global whole slide imaging (WSI) market is the integration of artificial intelligence (AI) and cloud-based telepathology platforms, which is revolutionizing how pathological data is interpreted, shared, and stored. These technologies are enhancing diagnostic accuracy, turnaround time, and collaboration among healthcare professionals across geographies

- For instance, platforms such as Proscia’s Concentriq and Paige.AI’s digital pathology tools utilize AI-powered algorithms to assist pathologists in detecting cancerous tissues, reducing interpretation errors and expediting workflows

- AI in WSI enables real-time quantification of biomarkers, pattern recognition in tissue morphology, and predictive diagnostics, which are proving especially beneficial in oncology and research settings. Some systems also allow for automated case prioritization based on slide abnormalities, improving lab efficiency

- Telepathology capabilities are further enhanced by high-resolution slide viewers and cloud integration, which allow seamless remote consultations and second opinions, particularly in underserved or rural regions

- The combination of WSI with digital health platforms and AI analytics is creating a unified pathology ecosystem where clinicians, researchers, and institutions can collaborate more efficiently

- This trend toward intelligent, remote-access pathology is driving demand for scalable, interoperable, and regulatory-compliant WSI solutions across both clinical and research domains, with major vendors such as Leica Biosystems and Philips focusing on AI-integrated imaging workflows

Whole Slide Imaging Market Dynamics

Driver

“Rising Demand for Digital Pathology in Precision Diagnostics”

- The growing need for accurate, efficient, and high-throughput diagnostic workflows is a major driver of the whole slide imaging market. The demand is particularly high in oncology, where pathologists require detailed tissue analysis to inform treatment decisions

- For instance, in 2024, Roche expanded its digital pathology portfolio with AI-powered WSI tools designed to support precision diagnostics in cancer care. These tools assist in faster and more reproducible slide interpretation, enhancing diagnostic confidence

- Increasing adoption of telemedicine, particularly post-pandemic, has further emphasized the need for digital pathology solutions such as WSI that support remote access and diagnostic collaboration

- The ongoing digitization of healthcare and the need for data-driven decisions are positioning WSI as a foundational technology in modern pathology labs. Integration with electronic medical records (EMRs), AI, and laboratory information systems (LIS) is making WSI more attractive for clinical use

- Furthermore, the educational and research utility of WSI in academic institutions and pharmaceutical R&D is expanding its footprint, as it enables long-term slide archiving, sharing, and annotation for collaborative study

Restraint/Challenge

“High Cost and Regulatory Hurdles for Clinical Adoption”

- One of the primary challenges hindering the wider adoption of whole slide imaging is the high initial cost of scanners and associated digital infrastructure, making it less accessible for smaller labs or institutions in developing regions

- In addition, regulatory complexities such as obtaining FDA or CE approval for clinical diagnostic use can delay market entry and limit usage to research settings in some countries

- Data security and patient privacy concerns associated with the digital storage and transmission of pathology images further compound these challenges. Institutions must invest in HIPAA-compliant, encrypted platforms to ensure compliance

- Another hurdle is the lack of standardization across WSI platforms, which can result in interoperability issues between devices and software from different vendors

- Addressing these challenges requires regulatory clarity, cost reduction through scalable solutions, and collaboration among industry stakeholders to develop interoperable standards and secure platforms. As companies such as 3DHISTECH and Hamamatsu push toward affordable, AI-ready systems, broader adoption is expected across global markets

- Furthermore, the lack of interoperability and standardization between different WSI platforms and software often leads to workflow inefficiencies and integration issues in multi-vendor environments

- Overcoming these challenges will require greater collaboration between manufacturers, healthcare regulators, and IT providers to develop cost-effective, secure, and clinically validated WSI solutions that are easier to adopt across diverse healthcare settings

Whole Slide Imaging Market Scope

The market is segmented on the basis of technology, application, and end user.

- By Technology

On the basis of technology, the whole slide imaging market is segmented into scanners, IT infrastructure, viewers, and image management systems. The scanners segment dominated the market with the largest revenue share of 22.0% in 2024, driven by the rising need for high-resolution slide digitization in diagnostic and research settings. Scanners are fundamental to WSI as they enable rapid, automated, and accurate digitization of pathology slides, which is critical for telepathology, AI-based diagnostics, and remote collaboration. Increasing demand for high-throughput scanners with features such as z-stacking, batch scanning, and real-time preview has strengthened the segment’s dominance.

The image management systems (IMS) segment is anticipated to witness the fastest growth rate from 2025 to 2032, propelled by the growing need for efficient image storage, retrieval, and integration with laboratory information systems (LIS). IMS platforms facilitate centralized access to digitized slides, collaboration among pathologists, and data analytics integration, making them essential for scaling digital pathology across large institutions and research networks.

- By Application

On the basis of application, the whole slide imaging market is segmented into telepathology, cytopathology, immunohistochemistry (IHC), and hematopathology. The telepathology segment dominated the market with the largest market share of 40.5% in 2024, driven by the increasing demand for remote diagnostics, second opinions, and pathology services in underserved areas. Telepathology allows for seamless sharing and review of slides among specialists across geographic locations, which has become crucial post-pandemic and in regions with limited pathology expertise.

The immunohistochemistry (IHC) segment is expected to witness the fastest growth during the forecast period, owing to rising applications in cancer diagnostics, biomarker detection, and companion diagnostics. The use of WSI for quantitative and AI-assisted analysis of IHC-stained slides is expanding rapidly in both clinical and research environments, fueling growth.

- By End User

On the basis of end user, the whole slide imaging market is segmented into hospitals, pharmaceutical and biopharmaceutical companies, laboratories, academic institutes, research centers, and others. The academic and research institutes segment held the largest revenue share of 35.6% in 2024, due to early adoption of digital pathology in education, training, and research. The ability to annotate, archive, and share slides digitally has transformed pathology education and collaborative research, leading to widespread WSI adoption in universities and scientific institutions.

The pharmaceutical and biopharmaceutical companies segment is anticipated to grow at the fastest rate from 2025 to 2032, driven by increasing use of WSI in drug discovery, toxicological assessments, and clinical trial workflows. The integration of digital pathology into drug development pipelines enhances data reproducibility, efficiency, and regulatory compliance, supporting its rapid expansion in the pharmaceutical sector.

Whole Slide Imaging Market Regional Analysis

- North America dominated the whole slide imaging market with the largest revenue share of 60.3% in 2024, attributed to the early implementation of digital pathology systems, favorable regulatory frameworks, and strong healthcare infrastructure

- The region's pathologists and healthcare institutions prioritize precision diagnostics and efficient data management, with WSI systems widely integrated into hospital networks, academic centers, and research labs

- Widespread deployment is further supported by favorable regulatory approvals (such as FDA clearance), significant R&D investments, and a growing shift toward remote pathology and telemedicine, establishing North America as the global leader in WSI adoption across both clinical and research applications

U.S. Whole Slide Imaging Market Insight

The U.S. whole slide imaging market captured the largest revenue share of over 75% within North America in 2024, fueled by robust investment in digital pathology infrastructure and the early regulatory clearance of WSI systems for clinical use. The growing demand for AI-integrated diagnostics, centralized slide management, and remote pathology services is significantly driving adoption. Academic medical centers and pharmaceutical companies in the U.S. are increasingly implementing WSI for research and clinical trials, supported by favorable reimbursement policies and digital health integration.

Europe Whole Slide Imaging Market Insight

The Europe whole slide imaging market is projected to expand at a substantial CAGR during the forecast period, driven by widespread adoption of digital pathology in both clinical and academic settings. The presence of well-established healthcare systems, combined with increasing government initiatives supporting health digitization, fuels market growth. Rising cancer incidence and the region’s emphasis on early, accurate diagnosis are contributing to the uptake of WSI, particularly in hospitals and national pathology labs across countries such as Germany, France, and the Netherlands.

U.K. Whole Slide Imaging Market Insight

The U.K. whole slide imaging market is anticipated to grow at a noteworthy CAGR over the forecast period, supported by the National Health Service's (NHS) ongoing investment in digital pathology and AI-driven diagnostics. The increasing focus on remote diagnostics and collaborative clinical workflows has made WSI adoption more prominent. In addition, research institutions and university hospitals in the U.K. are incorporating WSI into teaching, training, and cancer research initiatives, further driving demand.

Germany Whole Slide Imaging Market Insight

The Germany whole slide imaging market is expected to expand at a considerable CAGR during the forecast period, driven by the country's advanced healthcare infrastructure and leadership in medical technology innovation. Germany’s strong emphasis on precision diagnostics and integration of AI in pathology labs is accelerating WSI adoption. The presence of several academic and research institutions, along with demand for digitized workflows in both public and private labs, is further contributing to market growth.

Asia-Pacific Whole Slide Imaging Market Insight

The Asia-Pacific whole slide imaging market is poised to grow at the fastest CAGR of over 11% from 2025 to 2032, driven by increasing healthcare investment, rising demand for digital diagnostics, and expanding pathology education in countries such as China, Japan, and India. The growing burden of chronic diseases, particularly cancer, is pushing demand for advanced diagnostic tools such as WSI. In addition, regional governments are promoting health digitization and telemedicine, making WSI adoption more accessible across both urban and emerging healthcare facilities.

Japan Whole Slide Imaging Market Insight

The Japan whole slide imaging market is gaining momentum due to the nation’s commitment to healthcare innovation and rapid digital transformation. Japan’s focus on high-quality, efficient medical diagnostics is encouraging hospitals and research institutes to adopt WSI systems. With a growing aging population and demand for accurate pathology services, WSI is increasingly being used for early disease detection and remote consultations, particularly in cancer diagnostics and academic research.

India Whole Slide Imaging Market Insight

The India whole slide imaging market accounted for the largest revenue share in Asia Pacific in 2024, driven by rapid digitization in healthcare, a growing number of pathology labs, and increasing investment in medical education. As India expands its network of diagnostic centers and medical colleges, WSI systems are being adopted to enhance training, remote diagnostics, and centralized pathology services. Government-backed smart health initiatives and the presence of cost-effective imaging solutions from local vendors are also propelling growth in the Indian market.

Whole Slide Imaging Market Share

The Whole Slide Imaging industry is primarily led by well-established companies, including:

- Leica Biosystems (Germany)

- Hamamatsu Photonics K.K. (Japan)

- Koninklijke Philips N.V., (Netherlands)

- F. Hoffmann-La Roche Ltd (Switzerland)

- 3DHISTECH Ltd. (Hungary)

- Olympus Corporation (Japan)

- Huron Digital Pathology Inc. (Canada)

- Indica Labs, Inc. (U.S.)

- Sectra AB (Sweden)

- Visiopharm A/S (Denmark)

- Glencoe Software, Inc. (U.S.)

- Proscia Inc. (U.S.)

- Paige.AI Inc. (U.S.)

- Inspirata, Inc. (U.S.)

- Konfoong Biotech International Co., Ltd. (KFBIO) (China)

- OptraSCAN Inc. (U.S.)

- PixCell Medical Technologies Ltd. (Israel)

- PathAI, Inc. (U.S.)

- Motic Digital Pathology (China)

- Pramana, Inc. (U.S.)

What are the Recent Developments in Global Whole Slide Imaging Market?

- In January 2025, Roche received expanded FDA 510(k) clearance for its VENTANA DP 600 digital pathology slide scanner, extending the use of its digital pathology solution in clinical settings. This move demonstrates Roche's ongoing commitment to advancing regulatory-compliant whole slide imaging systems that support precise, AI-assisted diagnostics and seamless workflow integration for pathology labs across the U.S.

- In March 2025, Proscia showcased interoperability capabilities of its Concentriq platform at the DICOM WG26 WSI Connectathon, enabling standards-based integration with multiple scanners and image management systems. This development reinforces Proscia’s position as a leader in AI-powered digital pathology, improving flexibility and cross-platform accessibility in whole slide imaging environments

- In December 2024, PathAI launched PathExplore Fibrosis, an AI-powered solution designed for the quantitative analysis of fibrosis, collagen, and fibers directly from H&E-stained whole slide images. Integrated into its AISight platform, this release emphasizes PathAI’s focus on augmenting disease characterization and diagnostic workflows using intelligent digital tools, particularly in liver and kidney pathology

- In November 2024, Pramana, Inc. partnered with ARUP Laboratories to digitize large-scale pathology archives and develop AI-based hematopathology algorithms. This collaboration marks a significant step toward scalable, edge-AI deployment in whole slide imaging, enabling real-time diagnostic support and improving access to digital pathology services in clinical and research settings

- In October 2024, the U.S. agency ARPA-H launched the IMaging Data EXchange (INDEX) initiative to create a comprehensive platform for sharing high-quality medical imaging data—including whole slide images—to accelerate AI tool development. This initiative highlights the growing importance of whole slide imaging in AI-driven precision diagnostics and underscores government efforts to foster interoperability and data accessibility in digital pathology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.