Global Dna Markers Market

Market Size in USD Billion

USD

207.57 Billion

USD

475.25 Billion

2025

2033

USD

207.57 Billion

USD

475.25 Billion

2025

2033

| 2026 - 2033 | |

| USD 207.57 Billion | |

| USD 475.25 Billion | |

| % | |

|

DNA Markers Market Size

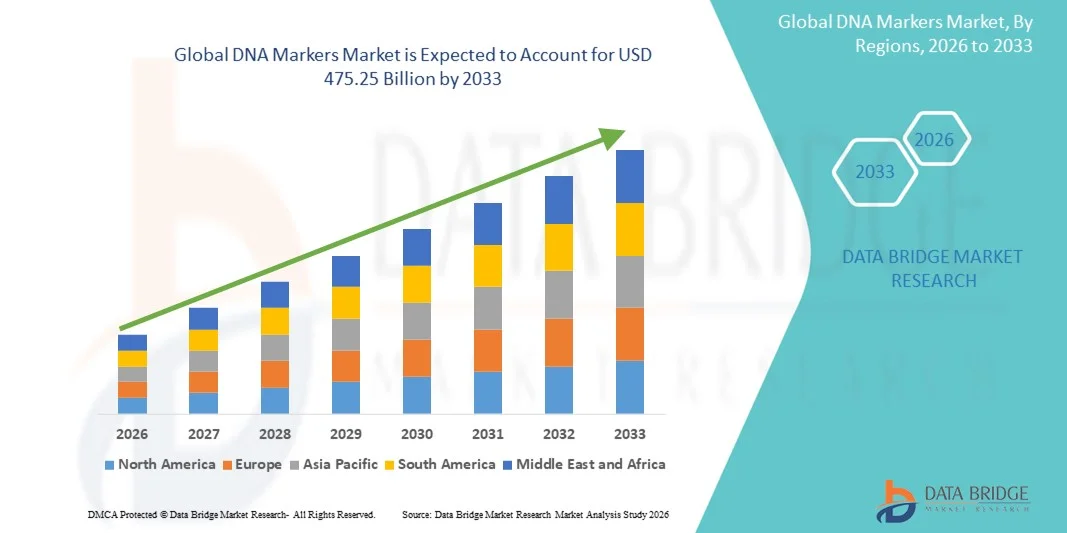

- The global DNA markers market size was valued at USD 207.57 billion in 2025 and is expected to reach USD 475.25 billion by 2033, at a CAGR of 10.91% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced molecular biology techniques and the growing emphasis on genetic research, diagnostics, and personalized medicine, leading to heightened demand for precise and reliable DNA marker solutions

- Furthermore, rising investment in genomics, biotechnology research, and forensic applications is driving the need for high-quality DNA markers, thereby significantly boosting the growth of the DNA Markers market

DNA Markers Market Analysis

- DNA markers, used for identifying genetic variations and profiling in research, diagnostics, agriculture, and forensic applications, are increasingly vital tools in modern genomics due to their precision, reproducibility, and broad applicability across multiple disciplines

- The escalating demand for DNA markers is primarily driven by rising investments in genomics research, personalized medicine, and molecular diagnostics, as well as growing applications in agricultural biotechnology and forensic science

- North America dominated the DNA Markers market, accounting for approximately 36% of the global revenue share in 2025, supported by strong research infrastructure, high biotechnology R&D spending, and early adoption of advanced genomic technologies such as microarrays and next-generation sequencing platforms, which frequently rely on DNA markers for calibration and validation

- Asia-Pacific is expected to be the fastest-growing region, projected to register a higher growth CAGR over the forecast period due to increasing government support for genomics initiatives, expanding biotechnology research, and rising adoption of molecular diagnostics in countries such as China, India, and Japan.

- The Nucleic Acid Applications segment dominated the largest market revenue share of 54.2% in 2025, driven by the widespread use of DNA markers in genetic mapping, PCR, sequencing, and genotyping workflows

Report Scope and DNA Markers Market Segmentation

|

Attributes |

DNA Markers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Thermo Fisher Scientific (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

DNA Markers Market Trends

Rising Adoption of Advanced Genetic Analysis Techniques

- A key trend in the global DNA markers market is the increasing adoption of advanced genetic analysis techniques, including PCR-based markers, SNP genotyping, and next-generation sequencing (NGS) applications

- Researchers and biotech companies are leveraging DNA markers for applications such as plant and animal breeding, disease diagnostics, forensic analysis, and personalized medicine

- For instance, in 2024, several agricultural research institutes in Europe and North America adopted SNP markers for precision breeding, enabling faster selection of high-yielding and disease-resistant crops

- The growing demand for high-throughput and cost-effective genotyping technologies is driving the development of automated platforms and multiplex assays, which allow simultaneous analysis of multiple markers

- The trend is also supported by increasing investment in genomics research and the integration of DNA markers into bioinformatics pipelines for better data analysis and interpretation

DNA Markers Market Dynamics

Driver

Increasing Demand for Improved Breeding and Diagnostic Accuracy

- Rising need for precise genetic analysis in agriculture, animal husbandry, healthcare, and forensic applications is a primary growth driver for DNA markers

- DNA markers help accelerate crop and livestock improvement programs by identifying desirable traits and enhancing selection efficiency

- For instance, in 2025, a leading livestock breeding company in the U.S. implemented microsatellite and SNP markers, enabling faster identification of high-performance breeding stock

- In addition, DNA markers are crucial in diagnostics, helping identify genetic disorders, susceptibility to diseases

- Patient-specific treatment options, thus enhancing the quality and efficiency of healthcare interventions

Restraint/Challenge

High Costs and Technical Expertise Requirements

- High costs of advanced DNA marker technologies and associated reagents can limit adoption, particularly in developing regions or smaller research labs

- Operation of DNA marker platforms often requires skilled personnel and specialized training, which can be a barrier for widespread implementation

- For instance, a 2023 survey in India reported that several small biotech labs delayed implementing NGS-based SNP marker platforms due to high setup costs (~USD 100,000–150,000 per system) and lack of trained staff

- Limited access to affordable, high-quality reagents and instruments can also slow down market growth, while standardization challenges across laboratories may affect reproducibility and reliability of results

- Overcoming these barriers through cost-effective kits, automated platforms, and training programs will be essential for sustained adoption and growth in the DNA Markers market

DNA Markers Market Scope

The market is segmented on the basis of product, type, application, and end users.

- By Product

On the basis of product, the DNA Markers market is segmented into Below 50 bp, 50 bp to 100 bp, 100 bp to 1 Kb, 1 Kb to 5 Kb, and Above 5 Kb. The 100 bp to 1 Kb segment dominated the largest market revenue share of 44.1% in 2025, driven by its versatility and high utility across various molecular biology applications. This segment is widely used in PCR, genotyping, sequencing, and cloning experiments, making it indispensable in research laboratories and biotechnology companies. The availability of ready-to-use commercial markers enhances adoption. High reproducibility, cost-effectiveness, and compatibility with multiple analytical techniques further drive preference. Academic and research institutions favor this segment for routine genetic analysis. Pharmaceutical and biotechnology companies adopt these markers for drug discovery, molecular diagnostics, and genetic screening. The segment benefits from established supply chains and regulatory approvals. Rising investments in genomics and personalized medicine boost usage. Technological improvements in marker design improve accuracy and reliability. High adoption in nucleic acid and proteomics applications sustains market dominance. Growing demand for high-throughput analysis enhances market penetration. The segment’s versatility ensures it remains the dominant choice globally.

The Above 5 Kb segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by increasing demand for long-range DNA markers in advanced research and next-generation sequencing (NGS) applications. Long-range markers enable detailed structural variation analysis, genome mapping, and complex trait studies. Biotechnology and pharmaceutical firms increasingly adopt these markers for functional genomics and synthetic biology. Academic research centers leverage long markers for in-depth studies of large genomic regions. Rising demand in crop genetics and animal breeding research also fuels growth. Technological advances improve marker stability, accuracy, and ease of use. Growing investment in precision medicine and gene therapy further supports adoption. High demand for custom long-range markers in specialized projects promotes market expansion. Integration with advanced molecular diagnostics workflows boosts preference. These markers are increasingly used for bioinformatics and systems biology studies. Emerging markets show rising adoption due to increased research infrastructure. These factors collectively make Above 5 Kb the fastest-growing product segment.

- By Type

On the basis of type, the market is segmented into Prestained Markers, Unstained Markers, and Specialty Markers. The Prestained Markers segment dominated the largest market revenue share of 49.6% in 2025, driven by their convenience in real-time visualization during gel electrophoresis and nucleic acid analysis. Prestained markers reduce the need for additional staining steps, saving time and minimizing errors. They are widely used in academic research, diagnostic laboratories, and biotech companies. The segment benefits from consistent performance, reproducibility, and compatibility with multiple gel systems. High adoption in routine molecular biology workflows enhances market penetration. Pharmaceutical companies utilize prestained markers for high-throughput screening and quality control. Digital documentation and imaging improvements further increase demand. Increasing focus on laboratory efficiency and error reduction supports segment growth. Rising adoption of gel electrophoresis in proteomics and nucleic acid research fuels preference. Customizable prestained markers improve versatility. The availability of color-coded markers enhances differentiation and accuracy. These factors collectively ensure Prestained Markers maintain dominance.

The Specialty Markers segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by increasing demand in advanced research applications and emerging technologies. Specialty markers are used in high-precision genotyping, molecular diagnostics, and next-generation sequencing. They offer superior sensitivity, stability, and accuracy for complex experimental designs. Adoption is rising in pharmaceutical and biotechnology sectors for drug development and genome editing. Academic research institutes utilize specialty markers for specialized studies in genomics and proteomics. Integration with high-throughput platforms enhances efficiency. Demand is growing for markers compatible with multiplexing and automated workflows. Technological advancements improve marker specificity and reduce cross-reactivity. Specialty markers are increasingly preferred for targeted applications in precision medicine. Expansion of custom marker services supports adoption. Increasing funding for molecular biology research in emerging markets boosts growth. These factors position Specialty Markers as the fastest-growing type segment.

- By Application

On the basis of application, the market is segmented into Nucleic Acid Applications and Proteomics Applications. The Nucleic Acid Applications segment dominated the largest market revenue share of 54.2% in 2025, driven by the widespread use of DNA markers in genetic mapping, PCR, sequencing, and genotyping workflows. Nucleic acid applications benefit from the high reproducibility, accuracy, and ease of use of commercial DNA markers. Academic and research institutes extensively rely on these markers for molecular biology studies. Pharmaceutical and biotechnology companies utilize nucleic acid markers for drug discovery, molecular diagnostics, and biomarker research. Technological advancements in PCR and electrophoresis improve efficiency and reduce errors. The segment’s applicability across multiple experiments supports adoption. Integration with high-throughput sequencing and bioinformatics tools enhances market penetration. Increasing investment in genomics and precision medicine drives growth. Rising demand in agricultural genomics and animal breeding research further supports adoption. Availability of standardized markers ensures reliability and consistency. Market dominance is reinforced by regulatory compliance and global distribution networks. These factors collectively sustain the segment’s leading position.

The Proteomics Applications segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by growing research in protein-DNA interactions, molecular diagnostics, and functional genomics. Proteomics applications require high-resolution DNA markers for accurate quantification and analysis. Biotechnology and pharmaceutical companies are increasingly adopting these markers for biomarker discovery and therapeutic target identification. Academic research centers employ proteomics markers for complex protein expression and interaction studies. Integration with mass spectrometry, high-throughput platforms, and automated workflows boosts adoption. Advances in protein marker chemistry improve accuracy and reproducibility. Rising interest in personalized medicine and molecular diagnostics drives demand. Emerging markets are witnessing increased investment in proteomics infrastructure. Demand for high-sensitivity, customizable markers enhances market potential. Collaboration between research institutes and commercial labs promotes adoption. These factors collectively make Proteomics Applications the fastest-growing application segment.

- By End Users

On the basis of end users, the market is segmented into Academic and Research Institutes, Pharmaceutical and Biotechnology Companies, CROs, and Others. The Academic and Research Institutes segment dominated the largest market revenue share of 51.7% in 2025, driven by their high demand for DNA markers in teaching, research, and development activities. These institutes conduct a broad range of genetic and molecular biology experiments requiring reliable and reproducible DNA markers. The segment benefits from funding support for genomics and molecular biology research. Prestained and commercially available DNA markers are preferred for ease of use. Academic laboratories adopt markers for both nucleic acid and proteomics applications. Rising enrollment in biotechnology and molecular biology programs boosts usage. Integration with digital imaging systems enhances workflow efficiency. Standardization and regulatory compliance promote adoption in educational labs. Academic institutes collaborate with biotech companies for translational research, driving marker utilization. Research output and publications further fuel demand. These factors collectively ensure Academic and Research Institutes dominate end-user adoption.

The Pharmaceutical and Biotechnology Companies segment is expected to witness the fastest CAGR of 8.5% from 2026 to 2033, driven by the rising use of DNA markers in drug discovery, genome editing, molecular diagnostics, and personalized medicine. These companies require high-precision markers for high-throughput screening and validation studies. DNA markers play a crucial role in biomarker identification, genetic mapping, and proteomic profiling. Investment in R&D and precision medicine initiatives fuel adoption. Integration with automated workflows and bioinformatics platforms enhances operational efficiency. The segment is driven by growing demand for advanced molecular diagnostics solutions. Specialty markers and long-range DNA markers are increasingly utilized. Regulatory compliance and validation requirements ensure reliability in pharmaceutical applications. Emerging markets show rapid adoption due to expanding biotech infrastructure. Collaboration with academic and contract research organizations promotes utilization. These factors collectively position Pharmaceutical and Biotechnology Companies as the fastest-growing end-user segment.

DNA Markers Market Regional Analysis

- North America dominated the DNA Markers market, accounting for approximately 36% of the global revenue share in 2025, supported by a well-established research infrastructure, high biotechnology and life sciences R&D spending, and early adoption of advanced genomic technologies such as microarrays and next-generation sequencing (NGS)

- The region benefits from widespread use of DNA markers in applications including genetic research, clinical diagnostics, forensic analysis, and drug discovery, with strong funding from government bodies and private research institutions

- The presence of major biotechnology companies, academic research centers, and contract research organizations further strengthens regional demand, positioning DNA markers as essential tools for genomic calibration, validation, and molecular analysis across both research and clinical settings

U.S. DNA Markers Market Insight

The U.S. DNA Markers market captured the largest revenue share within North America in 2025, driven by substantial investments in genomics research, precision medicine, and molecular diagnostics. The country leads in the adoption of high-throughput sequencing platforms, PCR-based technologies, and microarray systems that rely heavily on DNA markers for accurate analysis. Strong federal funding, increasing use of DNA markers in oncology and inherited disease testing, and a robust forensic science ecosystem continue to propel market growth. Additionally, the presence of leading industry players and continuous technological innovation reinforce the U.S. market’s dominance.

Europe DNA Markers Market Insight

The Europe DNA Markers market is projected to expand at a steady CAGR during the forecast period, driven by increasing adoption of genomic testing, expanding biomedical research programs, and supportive regulatory frameworks for molecular diagnostics. European countries are investing heavily in population genomics initiatives and personalized medicine, where DNA markers play a critical role. Growth is further supported by rising demand from academic research institutes, pharmaceutical companies, and forensic laboratories across the region.

U.K. DNA Markers Market Insight

The U.K. DNA Markers market is anticipated to grow at a noteworthy CAGR over the forecast period, supported by strong government funding for genomics research and national initiatives such as large-scale genome sequencing programs. DNA markers are widely used across clinical research, agricultural genomics, and forensic science in the country. The U.K.’s advanced healthcare infrastructure and emphasis on precision medicine continue to drive adoption.

Germany DNA Markers Market Insight

The Germany DNA Markers market is expected to expand at a considerable CAGR, fueled by the country’s strong biotechnology sector, advanced laboratory infrastructure, and focus on research and innovation. DNA markers are extensively utilized in pharmaceutical R&D, molecular diagnostics, and academic research. Germany’s emphasis on quality standards and technologically advanced analytical tools supports sustained market growth.

Asia-Pacific DNA Markers Market Insight

The Asia-Pacific DNA Markers market is expected to be the fastest-growing region over the forecast period, driven by increasing government support for genomics initiatives, expanding biotechnology research capabilities, and rising adoption of molecular diagnostics. Countries such as China, India, and Japan are investing heavily in genomic research, precision medicine, and agricultural biotechnology, where DNA markers are fundamental tools. Improving laboratory infrastructure and growing awareness of genetic testing further accelerate regional growth.

Japan DNA Markers Market Insight

The Japan DNA Markers market is gaining momentum due to strong technological expertise, increasing use of molecular diagnostics, and growing focus on personalized healthcare. DNA markers are widely applied in clinical research, cancer diagnostics, and pharmacogenomics. Japan’s aging population and emphasis on early disease detection continue to support demand for advanced genomic tools.

China DNA Markers Market Insight

The China DNA Markers market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid expansion of genomics research, rising government funding, and a growing biotechnology industry. DNA markers are increasingly adopted in clinical diagnostics, agricultural genomics, forensic science, and large-scale population studies. The country’s push toward precision medicine and domestic development of sequencing technologies further fuels market growth.

DNA Markers Market Share

The DNA Markers industry is primarily led by well-established companies, including:

• Thermo Fisher Scientific (U.S.)

• Agilent Technologies (U.S.)

• Bio-Rad Laboratories (U.S.)

• Takara Bio Inc. (Japan)

• Promega Corporation (U.S.)

• New England Biolabs (U.S.)

• Qiagen N.V. (Germany)

• GenScript Biotech Corporation (U.S.)

• Lonza Group (Switzerland)

• HiMedia Laboratories (India)

• Cleaver Scientific (U.K.)

• GeneDireX (Taiwan)

• Norgen Biotek (Canada)

• Vivantis Technologies (Malaysia)

Latest Developments in Global DNA Markers Market

- In March 2023, multiple companies in the DNA test and genotyping space released over 67 new genetic marker-based DNA kit products covering more than 7,000 markers — expanding the scope of marker detection for ancestry, health, and research applications, and accelerating adoption of high-resolution DNA marker panels

- In September 2023, Thermo Fisher Scientific launched a new DNA sequencing platform designed to deliver improved accuracy and faster processing times, enabling more scalable genomic analysis and supporting broader use of DNA markers in forensic and clinical workflows

- In June 2024, Illumina, Inc. launched the MiSeq™ i100 Series sequencing systems, enhancing next-generation sequencing (NGS) capabilities and marker detection throughput in laboratories — a significant boost for studies relying on comprehensive SNP and genomic marker profiling

- In October 2024, EpiMedTech Global introduced epiGeneComplete, a clinical-grade NGS test combining DNA methylation and SNP marker analysis to provide highly detailed insights into aging, stress, metabolism, inflammation, and addiction risk — illustrating expanded marker panel use in clinical diagnostics

- In March 2025, Takara Bio launched a high-precision DNA ladder kit (100 bp–50 kb) with improved readability on standard gel electrophoresis systems — supporting more accurate DNA fragment sizing and marker confirmation in genotyping and sequencing workflows

- In February 2025, Bio-Rad Laboratories and Thermo Fisher Scientific announced a strategic partnership to co-develop and supply standardized DNA ladder kits for quality control in molecular diagnostics, facilitating consistent marker usage across research and clinical labs

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.