Global Down Syndrome Market

Market Size in USD Billion

USD

2.05 Billion

USD

5.93 Billion

2024

2032

USD

2.05 Billion

USD

5.93 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.05 Billion | |

| USD 5.93 Billion | |

| % | |

|

Down Syndrome Market Size

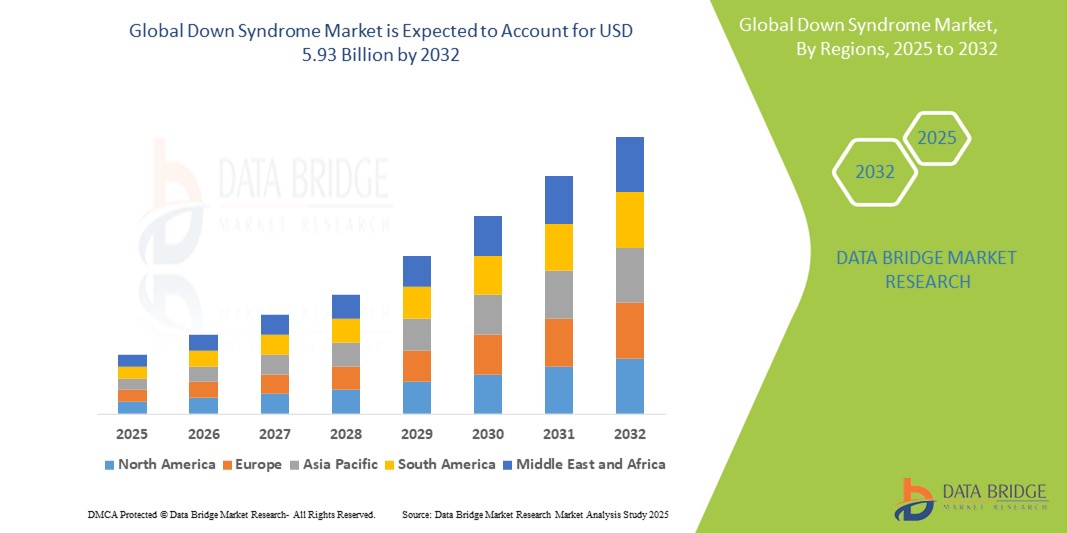

- The global Down syndrome market size was valued at USD 2.05 billion in 2024 and is expected to reach USD 5.93 billion by 2032, at a CAGR of 14.2% during the forecast period

- The market growth is primarily driven by increasing research and development efforts aimed at improving diagnosis, early intervention, and targeted therapies for Down syndrome across various age groups

- Furthermore, rising awareness about genetic disorders, expanding government initiatives, and enhanced healthcare access in both developed and developing regions are fueling market expansion. These converging factors are contributing to significant advancements in supportive care and treatment innovation, thereby accelerating the growth of the Down syndrome market globally

Down Syndrome Market Analysis

- The Down syndrome market, encompassing diagnostics, therapeutics, and supportive care solutions, is gaining prominence in the global healthcare landscape due to the growing emphasis on early detection, medical management, and long-term developmental support for individuals with trisomy 21

- The rising incidence of chromosomal disorders, increased public and professional awareness, and expanding access to prenatal screening technologies are key factors propelling demand within this market

- North America dominates the Down syndrome market with the largest revenue share of 39.4% in 2024, characterized by well-established healthcare infrastructure, strong research and development investments, and widespread availability of genetic testing service

- Asia-Pacific is expected to be the fastest growing region in the Down syndrome market during the forecast period due to improving healthcare access, growing awareness about genetic disorders, and a surge in government-led screening and rehabilitation programs, especially in countries such as China and India

- Trisomy 21 segment dominates the Down syndrome market with a market share of 94.5% in 2024, driven by its high genetic prevalence and widespread clinical recognition as the most common form of Down syndrome

Report Scope and Down Syndrome Market Segmentation

|

Attributes |

Down Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Down Syndrome Market Trends

“Enhanced Accuracy and Accessibility Through Non-Invasive Prenatal Testing (NIPT)”

- A significant and accelerating trend in the global Down syndrome market is the rapid advancement and adoption of non-invasive prenatal testing (NIPT), which analyzes fetal DNA through maternal blood samples. This evolution in diagnostic technology is significantly enhancing the accuracy, safety, and accessibility of early detection for chromosomal abnormalities such as trisomy 21

- For instance, tests such as Panorama by Natera and Harmony by Roche are being widely adopted for their ability to detect Down syndrome with over 99% accuracy, without the risks associated with invasive procedures such as amniocentesis. Similarly, Illumina’s Verifi test has become a preferred option across various prenatal care settings

- NIPT enables healthcare providers to identify high-risk pregnancies earlier in the gestation period, allowing for better-informed clinical decisions, more timely counseling, and proactive management of the pregnancy. For instance, leading laboratories now offer AI-assisted platforms that interpret results faster and deliver personalized risk profiles based on maternal and fetal genetic data. Furthermore, the minimally invasive nature of these tests provides expectant parents with peace of mind and a safer path to early diagnosis

- The seamless integration of NIPT into standard prenatal care protocols across hospitals and clinics facilitates centralized genetic screening alongside other routine obstetric assessments. Through a single testing pathway, physicians can detect Down syndrome along with other chromosomal conditions such as Edwards and Patau syndromes, improving overall pregnancy monitoring and care outcomes

- This trend toward more intelligent, precise, and non-invasive testing is fundamentally reshaping clinical expectations and patient experiences in prenatal diagnostics. Consequently, companies such as Illumina, Roche, and Myriad Genetics are investing in next-generation sequencing and AI-enabled analytics to improve test performance, affordability, and global reach

- The demand for NIPT that offers high sensitivity, low risk, and early detection is growing rapidly across both developed and developing regions, as healthcare systems increasingly prioritize preventive care, genetic counseling, and maternal-fetal health optimization

Down Syndrome Market Dynamics

Driver

“Increasing Demand Driven by Advancements in Early Diagnosis and Prenatal Screening”

- The growing demand for early and accurate detection of genetic disorders during pregnancy, combined with advancements in prenatal screening technologies, is a significant driver for the increasing growth of the Down syndrome market

- For instance, in February 2024, Illumina Inc. partnered with Myriad Genetics to expand access to next-generation non-invasive prenatal testing (NIPT) across North America and parts of Europe, enhancing early detection capabilities for trisomy 21 and related chromosomal abnormalities. Such strategic initiatives are expected to accelerate the market's growth over the forecast period

- As expectant parents become more proactive in seeking genetic information early in pregnancy, NIPT offers a non-invasive, accurate, and safe alternative to traditional invasive procedures such as amniocentesis, thereby boosting its adoption globally

- Furthermore, the rising awareness of prenatal care, growing maternal age in several regions, and the inclusion of NIPT in public health guidelines are making these tests an integral component of routine obstetric practice, especially in developed countries

- The availability of comprehensive screening through maternal blood samples, combined with rapid turnaround times and AI-assisted risk assessment, is enabling healthcare providers to deliver personalized and timely care. This not only reduces uncertainty for parents but also supports better clinical planning and counseling

- The increasing inclination towards early, risk-free, and precise prenatal diagnostics, along with ongoing research and technological innovation, continues to propel the growth of the Down syndrome market in both clinical and home-based testing environments

Restraint/Challenge

“Limited Access and High Costs of Advanced Screening Technologies”

- Limited access to advanced genetic screening tools such as non-invasive prenatal testing (NIPT), along with the high costs associated with these technologies, remains a significant challenge for the growth of the Down syndrome market. Despite their clinical accuracy and non-invasiveness, many expectant parents in low- and middle-income regions face financial and infrastructural barriers to utilizing such advanced diagnostics

- For instance, while NIPT is widely available in high-income countries and is increasingly being covered by insurance providers, its limited availability in public healthcare systems across developing regions restricts widespread adoption and early intervention

- To build broader market acceptance, stakeholders must address these challenges through cost optimization, increased reimbursement coverage, and strategic public-private collaborations aimed at improving accessibility. Companies such as Illumina and BGI Genomics are working to expand their presence in emerging markets by offering tiered pricing models and establishing local partnerships, but affordability and access disparities persist

- Furthermore, a lack of awareness about the availability and benefits of early screening, along with societal stigma and ethical considerations surrounding genetic testing, can reduce uptake, particularly in regions with lower levels of genetic literacy or where such conditions are culturally sensitive

- Bridging these gaps through improved education, healthcare training, and policy support will be essential to ensure that high-quality Down syndrome diagnostics become universally accessible and effectively integrated into routine prenatal care across all regions

Down Syndrome Market Scope

The market is segmented on the basis of disease type, treatment, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Down syndrome market is segmented into Trisomy 21, Translocation Down Syndrome, and Mosaic Down Syndrome. The Trisomy 21 segment dominates the largest market revenue share of 94.5% in 2024, driven by its overwhelming prevalence among all Down syndrome cases. This chromosomal condition accounts for the majority of diagnoses worldwide due to non-disjunction of chromosome 21, making it the primary focus of screening programs and genetic counseling services.

The Mosaic Down Syndrome segment is anticipated to witness the fastest growth rate from 2025 to 2032, attributed to increasing awareness, better diagnostic differentiation through advanced genetic testing techniques, and a growing number of late or misdiagnosed cases now being identified with higher accuracy

- By Treatment

On the basis of treatment, the market is segmented into diagnosis and therapy. The diagnosis segment dominated the market with the largest revenue share in 2024, propelled by the rising adoption of early prenatal screening techniques such as NIPT, ultrasonography, and chromosomal microarray analysis. Diagnostic advancements enable earlier intervention and comprehensive care planning, reinforcing the segment’s strong market position.

The therapy segment is projected to be the fastest growing during the forecast period, fueled by increased recognition of the importance of postnatal developmental support, including physiotherapy, speech-language pathology, behavioral therapy, and educational intervention programs that aim to improve long-term outcomes for individuals with Down syndrome.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, homecare settings, therapy centers, and others. Hospitals dominate the down syndrome market in 2024, owing to their access to advanced diagnostic infrastructure, genetic consultation, multidisciplinary care, and integration of prenatal and postnatal services under one roof.

Therapy centers are expected to register the fastest growth rate from 2025 to 2032, driven by the rising demand for specialized early intervention services, which play a crucial role in addressing developmental challenges and enhancing quality of life through targeted therapeutic programs.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct tender, retail sales, and others. The direct tender segment dominated the market with the largest revenue share in 2024, supported by institutional purchases made by hospitals and government health departments for prenatal screening programs and centralized therapeutic services.

The Retail Sales segment is projected to grow at the fastest pace during the forecast period, driven by increasing availability of home-based care products, assistive devices, and access to direct-to-consumer genetic testing services through e-commerce and online diagnostic platforms.

Down Syndrome Market Regional Analysis

- North America dominates the Down syndrome market with the largest revenue share of 39.4% in 2024, driven by well-established healthcare infrastructure, strong research and development investments, and widespread availability of genetic testing services

- The region benefits from early and widespread adoption of advanced diagnostic tools such as non-invasive prenatal testing (NIPT), coupled with high availability of genetic counseling services and supportive government initiatives aimed at developmental care

- Furthermore, the growing focus on individualized therapeutic approaches, high healthcare expenditure, and the active involvement of non-profit organizations advocating for Down syndrome support services have significantly contributed to the market's expansion across both the U.S. and Canada

U.S. Down Syndrome Market Insight

The U.S. Down syndrome market holds the largest revenue share of 78% in North America in 2024, driven by advanced prenatal screening programs and widespread access to diagnostic technologies such as non-invasive prenatal testing (NIPT). Growing awareness and early diagnosis contribute to timely intervention and therapeutic management, fueling market growth. In addition, well-established healthcare infrastructure and extensive research funding are supporting the development of innovative therapies and supportive care programs. The increasing number of support organizations and government initiatives focused on improving the quality of life for individuals with Down syndrome further propel the market expansion.

Europe Down Syndrome Market Insight

The Europe Down syndrome market is projected to grow at a steady CAGR over the forecast period, driven by increased awareness, widespread availability of diagnostic and therapeutic services, and government-supported health policies. Rising healthcare expenditures and enhanced genetic counseling programs across countries such as Germany, France, and the U.K. encourage early diagnosis and better management of Down syndrome. Furthermore, increased focus on inclusive education and supportive therapies is fostering demand for comprehensive treatment options. The region’s emphasis on patient advocacy and social support systems also positively impacts the market.

U.K. Down Syndrome Market Insight

The U.K. Down syndrome market is expected to grow significantly due to heightened awareness programs, advancements in diagnostic techniques, and increasing government support for inclusive care. The prevalence of genetic testing and early intervention therapies is rising, supported by the NHS and various charitable organizations. Growing demand for personalized treatment plans and community-based therapy centers further propels market growth. The U.K.’s strong research ecosystem is also contributing to the development of innovative treatment methodologies and supportive care.

Germany Down Syndrome Market Insight

The Germany’s Down syndrome market is anticipated to expand at a robust CAGR, driven by advanced healthcare infrastructure and strong governmental policies promoting early diagnosis and intervention. The growing adoption of cutting-edge genetic screening technologies and increasing investment in therapeutic research fuel the market. Germany’s focus on rehabilitation programs, educational inclusion, and social welfare initiatives contributes to increasing demand for treatment and support services. Consumer preference for specialized clinics and therapy centers further supports market growth.

Asia-Pacific Down Syndrome Market Insight

The Asia-Pacific Down syndrome market is poised for the fastest CAGR during the forecast period due to rising healthcare awareness, increasing availability of diagnostic and therapeutic services, and government initiatives focused on maternal and child health. Countries such as China, India, and Japan are witnessing growing prenatal screening adoption and expanding healthcare infrastructure. The region’s large population base and improving socioeconomic conditions are driving demand for early diagnosis and supportive care services. In addition, growing advocacy for special needs education and therapy centers enhances the market’s potential.

Japan Down Syndrome Market Insight

The Japan’s Down syndrome market is gaining traction owing to the country’s advanced healthcare system, aging population, and increasing focus on early diagnosis and personalized therapies. Integration of comprehensive care programs, including physical, speech, and occupational therapies, is fueling demand. Moreover, government policies promoting inclusive education and social support for individuals with Down syndrome are encouraging market growth. Technological advancements in prenatal screening and therapeutic research further contribute to the expanding market.

India Down Syndrome Market Insight

The India accounts for the largest market revenue share in Asia-Pacific in 2024, supported by rising healthcare awareness, increasing prenatal diagnostic adoption, and expanding therapeutic facilities. The growing middle-class population and urbanization have led to better access to healthcare services, including genetic testing and intervention therapies. Government efforts toward maternal and child health, along with NGOs promoting special needs education and therapy, are key market drivers. The affordability of treatment options and increasing number of therapy centers also support the market growth in India.

Down Syndrome Market Share

The Down Syndrome industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Lilly (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Biogen Inc. (U.S.)

- Novartis AG (Switzerland)

- AstraZeneca U.K.)

- Sanofi (France)

- Amgen Inc. (U.S.)

- GSK plc. (U.K.)

- Bristol-Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Vertex Pharmaceuticals Incorporated (U.S.)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Ipsen S.A. (France)

Latest Developments in Global Down Syndrome Market

- In December 2024, a clinical trial led by the Hospital del Mar Medical Research Institute demonstrated that the molecule AEF0217, developed by Aelis Farma, significantly improves cognitive function in individuals with Down syndrome. The study's success paves the way for an international Phase II trial to determine optimal dosing and further assess functional benefits

- In February 2024, Invitae Corporation announced the completion of its sale of non-invasive prenatal screening (NIPT) and carrier screening assets to Natera. This strategic move allows Invitae to focus on its core strengths in clinical germline genetic information, while Natera expands its capabilities in reproductive health diagnostics

- In March 2024, Sanofi launched an awareness campaign for World Down Syndrome Day, encouraging employees to wear mismatched socks to symbolize the extra chromosome in individuals with Down syndrome. This initiative aimed to promote inclusion and raise awareness about the condition

- In April 2024, Roche Diagnostics introduced advancements in prenatal screening technologies, including the Harmony Prenatal Test, which assesses the risk of Down syndrome and other chromosomal disorders. These innovations aim to provide expectant parents with more accurate and accessible testing options

- In May 2024, Plex Pharmaceuticals initiated a research program focusing on therapies to address developmental delays associated with Down syndrome. The program aims to explore new treatment avenues to enhance the quality of life for individuals with the condition

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.