Global Dry Eye Syndrome Treatment Market

Market Size in USD Billion

USD

6.13 Billion

USD

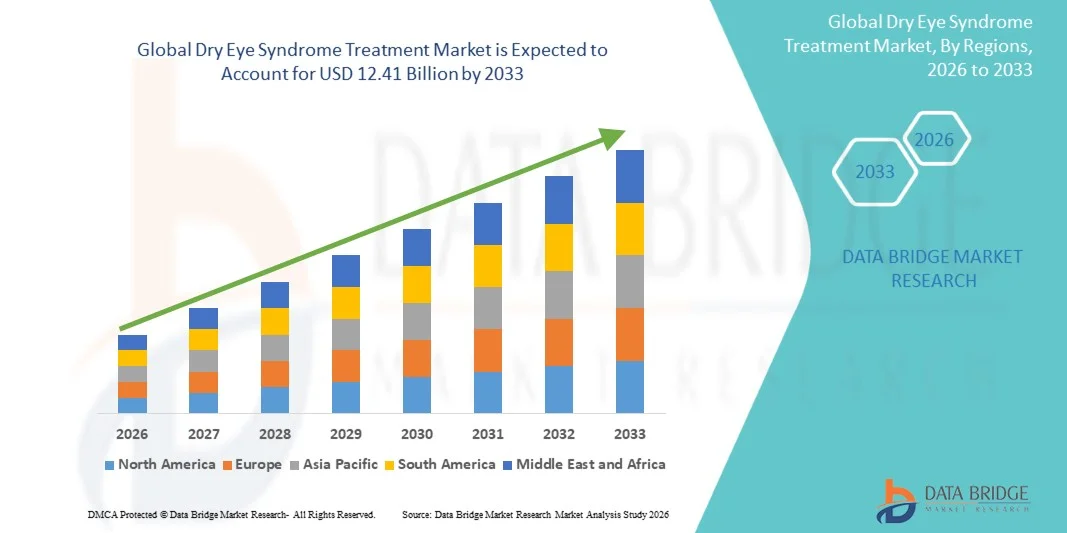

12.41 Billion

2025

2033

USD

6.13 Billion

USD

12.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.13 Billion | |

| USD 12.41 Billion | |

| % | |

|

What is the global Dry Eye Syndrome Treatment Market Size?

- As per Data Bridge Market Research analyses that the global dry eye syndrome treatment market size was valued at USD 6.13 billion in 2025 and is expected to reach USD 12.41 billion by 2033, at a CAGR of 9.22% during the forecast period

- The market growth is largely fueled by the increasing prevalence of dry eye syndrome, coupled with advancements in ophthalmic therapies and drug formulations, driving the adoption of effective treatment solutions across age groups

- Furthermore, rising awareness about eye health, growing access to healthcare, and demand for personalized, non-invasive, and long-lasting treatments are establishing modern dry eye therapies as the preferred choice for patients and clinicians. These converging factors are accelerating the uptake of innovative treatments, thereby significantly boosting the industry's growth

Market Size & Forecast

Global Market Value (2025): USD 6.13 Billion

Expected Market Value (2033): USD 12.41 Billion

Forecast CAGR (2026–2033): 9.22%

Dry Eye Syndrome Treatment Market Analysis

- Dry eye syndrome treatments, including prescription medications, over-the-counter eye drops, and advanced therapeutic devices, are increasingly vital components of ophthalmic care due to their ability to relieve discomfort, improve ocular surface health, and prevent long-term vision complications

- The escalating demand for dry eye treatments is primarily fueled by the growing prevalence of dry eye syndrome, increasing screen time and digital device usage, and rising awareness among patients and healthcare providers about early diagnosis and effective management

- North America dominated the dry eye syndrome treatment market with the largest revenue share of 40.9% in 2025, characterized by high healthcare expenditure, advanced ophthalmic infrastructure, and a strong presence of key pharmaceutical and medical device players, with the U.S. experiencing substantial growth in prescription therapies and innovative drug delivery systems

- Asia-Pacific is expected to be the fastest growing region in the dry eye syndrome treatment market during the forecast period due to increasing geriatric population, rising prevalence of digital eye strain, and improving access to eye care services

- Prescription (Rx) Drugs segment dominated the dry eye syndrome treatment market with a market share of 46.5% in 2025, driven by their clinical efficacy, availability of novel formulations, and growing adoption among ophthalmologists for moderate-to-severe cases

Report Scope and Dry Eye Syndrome Treatment Market Segmentation

|

Attributes |

Dry Eye Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Dry Eye Syndrome Treatment Market Trends

“Rising Adoption of Advanced Therapeutics and Digital Health Solutions”

- A significant and accelerating trend in the global dry eye syndrome treatment market is the increasing adoption of advanced therapeutics, including prescription drugs, in-office procedures, and device-based therapies, alongside digital health solutions for remote monitoring and management

- For instance, devices such as LipiFlow enable automated thermal pulsation therapy for meibomian gland dysfunction, providing clinicians with a precise, patient-friendly treatment option. Similarly, prescription drops such as cyclosporine and lifitegrast are being increasingly integrated into personalized treatment regimens

- Integration with digital health platforms allows patients to track symptoms, adherence, and treatment efficacy via mobile apps, enhancing personalized care and facilitating tele-ophthalmology consultations. For instance, some AI-enabled apps can recommend follow-up interventions based on patient-reported outcomes

- The convergence of advanced therapeutics and digital tools is enabling more precise, convenient, and effective dry eye management, improving patient compliance and satisfaction

- This trend towards innovative, patient-centric, and technology-driven therapies is reshaping treatment standards and expectations in ophthalmology. Consequently, companies such as Allergan and Johnson & Johnson Vision are investing in next-generation therapeutics and connected health solutions to enhance treatment outcomes

- The demand for treatments that combine clinical efficacy with ease of use and remote monitoring capabilities is growing rapidly across both clinical and home-based care settings, as patients increasingly prioritize comfort and sustained symptom relief

- Emerging biotechnological innovations, including regenerative therapies and novel formulations such as nanomicellar eye drops, are gaining attention as potential game-changers for long-term dry eye relief, attracting investment from both pharmaceutical and medical device companies

Dry Eye Syndrome Treatment Market Dynamics

Driver

“Increasing Prevalence and Awareness of Dry Eye Syndrome”

- The rising prevalence of dry eye syndrome due to aging populations, extended screen time, and environmental factors, coupled with growing awareness of the condition, is a significant driver of the heightened demand for effective treatments

- For instance, a survey conducted in 2025 indicated that over 30% of adults in North America reported experiencing chronic dry eye symptoms, driving clinicians to adopt advanced therapeutic options

- As patients become more aware of the impact of untreated dry eye on vision and quality of life, demand for prescription medications, in-office procedures, and innovative devices has surged, offering a compelling rationale for treatment

- Furthermore, increasing routine eye examinations and proactive ophthalmic care programs are prompting earlier diagnosis and intervention, creating steady demand for both established and novel therapies

- The combination of patient education, rising digital device usage, and growing adoption of preventative ophthalmic care is propelling the market across both developed and emerging regions

- Expansion of corporate wellness programs and occupational eye health initiatives is driving awareness in workplaces, encouraging early screening and treatment of dry eye symptoms among working adults

- Rising collaborations between pharmaceutical companies and eye care providers for patient education campaigns are fostering greater adoption of advanced therapies, supporting overall market growth

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Markets”

- Concerns surrounding the high cost of advanced prescription medications and device-based therapies pose a significant challenge to broader market penetration, particularly in developing regions

- For instance, premium therapies such as intense pulsed light (IPL) treatment and LipiFlow can cost several hundred dollars per session, limiting access for price-sensitive patients

- Addressing affordability through generic formulations, insurance coverage, and patient assistance programs is crucial for expanding adoption. Companies such as Novartis and Bausch + Lomb emphasize patient support initiatives to mitigate cost barriers

- In addition, limited access to specialized ophthalmic care and diagnostic tools in rural or underdeveloped regions restricts the availability of advanced dry eye treatments, creating unequal treatment distribution

- Overcoming these challenges through cost-effective solutions, telemedicine platforms, and broader healthcare access will be vital for sustained growth in the global dry eye syndrome treatment market

- Regulatory hurdles, including stringent approval processes for new drugs and devices, can delay market entry and limit the availability of innovative therapies, impacting overall market expansion

- Patient non-compliance due to complex treatment regimens or discomfort associated with certain therapies can hinder treatment efficacy, emphasizing the need for user-friendly and tolerable treatment solutions

Dry Eye Syndrome Treatment Market Scope

The market is segmented on the basis of product type, dosage type, treatment, diagnosis, dose, medication type, container type, packaging type, type, distribution channel, and end-users.

- By Product Type

On the basis of product type, the market is segmented into tear stimulators, artificial tears, secretagogues, and others. The artificial tears segment dominated the market with the largest revenue share in 2025, driven by their widespread availability, affordability, and immediate relief from dry eye symptoms. Artificial tears are the first-line treatment for mild-to-moderate cases and are preferred by patients for ease of use and frequent administration. High adoption is also fueled by rising screen time, environmental factors, and general awareness about eye health. Physicians often recommend artificial tears in combination with other therapies for enhanced patient outcomes. Furthermore, artificial tears are compatible with long-term use and can be used alongside prescription medications without major side effects.

The tear stimulators segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing innovation in prescription therapies that stimulate tear production at the glandular level. These therapies provide longer-lasting relief, making them attractive for chronic and severe dry eye cases. Rising adoption is supported by clinical endorsements, improved formulation technologies, and growing awareness of advanced treatment options. Patients with moderate-to-severe symptoms increasingly prefer tear stimulators over frequent artificial tear use. The segment also benefits from digital marketing and patient education campaigns highlighting their efficacy.

- By Dosage Type

On the basis of dosage type, the market is segmented into liquid, semi-solid, and others. The liquid segment dominated in 2025 due to convenience, ease of administration, and patient familiarity with eye drops. Liquid formulations, including both artificial tears and prescription medications, provide rapid symptom relief and can be used multiple times a day. They are cost-effective and widely distributed across pharmacies and hospitals, supporting high adoption. Physicians often recommend liquid formulations for both acute and chronic dry eye management. The flexibility of liquid formulations allows combination therapy with other treatments for enhanced effectiveness. Their compatibility with multi-dose packaging further supports market dominance.

The semi-solid segment is expected to witness the fastest growth from 2026 to 2033, driven by innovative gel and ointment formulations that offer longer ocular surface retention. Semi-solid therapies reduce dosing frequency and improve patient adherence, particularly in severe cases. Growing acceptance of gel-based therapies among clinicians and patients supports this growth. These formulations also minimize discomfort and provide a sustained protective effect. Increasing technological advancements in formulation consistency and bioavailability further accelerate adoption.

- By Treatment

On the basis of treatment, the market is segmented into lubricating agents, cholinergics, anti-inflammatory, anti-infectives, anti-allergics, and others. The lubricating agents segment dominated in 2025, driven by broad applicability across mild, moderate, and severe cases. Lubricating agents provide instant relief, are easy to use, and are widely available both OTC and via prescription. Their affordability and compatibility with other therapies make them a preferred first-line treatment. Physicians frequently recommend lubricating agents to maintain ocular surface moisture and prevent further damage. Consumer familiarity and comfort with these agents ensure sustained high adoption. They also offer versatility in packaging, dosing, and combination with other treatments.

The anti-inflammatory segment is expected to witness the fastest growth from 2026 to 2033, fueled by the growing understanding of inflammation as a key driver of chronic dry eye. Prescription anti-inflammatory drugs such as cyclosporine and lifitegrast target underlying causes and are preferred for moderate-to-severe cases. Increasing clinician awareness, new formulations, and improved drug delivery methods are driving growth. Patient education campaigns on managing inflammation-related dry eye support adoption. Regulatory approvals for new anti-inflammatory therapies further contribute to market expansion.

- By Diagnosis

On the basis of diagnosis, the market is segmented into comprehensive eye exam, Schirmer test, tear osmolarity test, and others. The comprehensive eye exam segment dominated in 2025 due to its ability to provide a holistic assessment of ocular health. Eye exams allow early detection of underlying conditions and guide effective treatment selection. They remain the standard diagnostic procedure recommended by ophthalmologists and optometrists worldwide. Comprehensive exams can be combined with other tests to tailor treatment plans. High adoption is supported by insurance coverage and routine preventive care programs. Increasing awareness of eye health among patients further drives utilization.

The tear osmolarity test segment is anticipated to witness the fastest growth from 2026 to 2033, driven by demand for objective, quantitative diagnostic tools. Tear osmolarity allows early detection of dry eye severity and helps customize therapy. Rising adoption of precision ophthalmology and integration with digital health monitoring platforms is fueling growth. These tests are increasingly being used in specialty clinics and hospital settings. Clinicians value tear osmolarity tests for monitoring treatment efficacy over time. Technological advancements are making these tests faster, more accurate, and patient-friendly.

- By Dose

On the basis of dose, the market is segmented into unit dose and multi-dose. The multi-dose segment dominated in 2025 due to cost-effectiveness, convenience, and compatibility with frequent use. Multi-dose formulations allow long-term management and are preferred for both OTC and prescription medications. Hospitals and retail pharmacies favor multi-dose packaging for ease of stocking. Frequent users and chronic patients benefit from lower per-use costs. Multi-dose formats also reduce environmental waste compared to multiple unit-dose packs. Patient familiarity with multi-dose bottles supports continued dominance.

The unit-dose segment is expected to witness the fastest growth from 2026 to 2033, driven by the need for preservative-free, sterile formulations. Unit-dose packaging reduces contamination risk and supports patient safety, especially for chronic dry eye cases. Travel-friendly and portable designs enhance convenience. Increasing adoption of prescription eye drops in unit-dose formats is supporting growth. Patient adherence improves with easier-to-use single-use vials. Clinical guidelines increasingly recommend unit-dose formats for sensitive eyes.

- By Medication Type

On the basis of medication type, the market is segmented into prescription (Rx) drugs and over-the-counter (OTC) drugs. The Prescription (Rx) Drugs segment dominated the dry eye syndrome treatment market with a market share of 46.5% in 2025, driven by its clinical efficacy in treating moderate-to-severe cases, growing adoption by ophthalmologists, and the ability to target underlying causes such as inflammation or meibomian gland dysfunction. Prescription drugs, including cyclosporine, lifitegrast, and newer biologics, offer longer-lasting relief compared to OTC therapies and are supported by strong clinical evidence. High adoption is also fueled by increasing awareness among patients about advanced treatment options and the rising prevalence of chronic dry eye globally. These therapies are often used in combination with other treatment modalities, enhancing overall patient outcomes.

The Over-The-Counter (OTC) Drugs segment is expected to witness the fastest growth in the dry eye syndrome treatment market from 2026 to 2033, driven by rising consumer preference for easily accessible, self-administered therapies for mild-to-moderate dry eye symptoms. OTC products, such as artificial tears and lubricating drops, provide immediate relief and are available without a prescription, making them highly convenient for frequent use. Increasing awareness about eye health, prolonged screen time, and environmental factors are further fueling demand. Growth is supported by expanding retail and online pharmacy channels, which enhance accessibility and convenience for patients.

- By Container Type

On the basis of container type, the market is segmented into unit-dose vials, bottles, and tubes. Bottles dominated in 2025 due to affordability, convenience, and suitability for frequent use. They are compatible with multi-dose therapies and widely distributed across pharmacies. Patients prefer bottles for ease of administration and storage. Hospitals and clinics often stock bottled formulations in bulk. Bottles provide flexibility for both OTC and prescription drugs. Consumer familiarity with bottles ensures sustained demand.

The unit-dose vials segment is expected to witness the fastest growth from 2026 to 2033, driven by rising demand for preservative-free, sterile packaging that minimizes contamination risk and supports patient safety, especially for frequent dosing in chronic cases. Unit-dose vials reduce contamination risk and improve patient safety. They are ideal for sensitive eyes and chronic therapy management. Clinicians favor unit-dose vials for in-office administration. Portability and ease of use enhance adoption among patients. Regulatory support for preservative-free formulations accelerates market penetration.

- By Packaging Type

On the basis of packaging type, the market is segmented into plastic, aluminium, and glass. Plastic packaging dominated in 2025 due to lightweight design, cost-effectiveness, and wide adoption for both OTC and prescription therapies. Plastic containers are convenient for transport, storage, and disposal. Retail and hospital pharmacies favor plastic packaging for logistics efficiency. Patients prefer lightweight plastic for ease of daily use. Plastic allows flexibility for multiple formulations. Environmental and recycling programs also support continued use.

Aluminium packaging is expected to witness the fastest growth from 2026 to 2033, driven by superior barrier properties, longer shelf-life, and growing environmental sustainability concerns. Aluminium tubes are increasingly preferred for gel and ointment formulations. Aluminium tubes are preferred for gels and ointments. They protect formulations from light and air, enhancing efficacy. Manufacturers are increasingly adopting aluminium for premium products. Growth is also fueled by rising consumer preference for eco-friendly packaging

- By Type

On the basis of type, the market is segmented into brands and generics. Branded formulations dominated in 2025 due to strong physician trust, proven clinical efficacy, and marketing reach. Brand loyalty and physician endorsements support consistent adoption. Branded drugs are widely stocked across hospitals and retail pharmacies. Awareness campaigns by major companies reinforce market dominance. Patients perceive branded drugs as higher quality. Clinical data supporting branded efficacy further solidifies market preference.

Generics are expected to witness the fastest growth from 2026 to 2033, driven by cost-effectiveness, increasing availability, and healthcare policies promoting affordable access. Generic adoption is higher in emerging markets. Rising awareness and bioequivalence studies enhance clinician confidence. Insurance coverage also supports generic growth. Patients seeking long-term therapy often prefer generics for affordability. Generic adoption is also supported by healthcare policies promoting affordable access to essential medications.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. Retail pharmacies dominated in 2025 due to accessibility, high footfall, and convenience for OTC purchases. Hospitals and clinics also distribute OTC drugs via retail setups. Patients prefer retail pharmacies for immediate availability. Distribution networks are well-established, ensuring consistent supply. Marketing campaigns target retail channels to maximize reach.

The online pharmacy segment is projected to witness the fastest growth from 2026 to 2033, fueled by digital adoption, home delivery convenience, and access to prescription medications. Online platforms enhance reach to rural and urban patients. Growth is supported by telemedicine and e-prescription trends. Patients prefer online ordering for privacy and convenience. E-pharmacies also facilitate subscription-based supply for chronic patients. Regulatory approvals for online dispensing support adoption.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. Hospitals dominated in 2025 due to high patient volumes, specialist ophthalmologists, and integrated care infrastructure. Hospitals provide both prescription therapies and advanced procedural interventions. Adoption is driven by clinician recommendations. Hospitals also serve as distribution hubs for multi-dose and branded drugs. Patient trust in hospital-administered therapies sustains dominance.

The homecare segment is expected to witness the fastest growth from 2026 to 2033, driven by self-administered therapies, OTC medications, and tele-ophthalmology support. Patients increasingly prefer managing mild-to-moderate dry eye at home. Homecare adoption is supported by convenience, cost-effectiveness, and digital monitoring. Growing awareness of chronic disease management fuels uptake. Availability of portable formulations such as unit-dose vials supports home use.

Dry Eye Syndrome Treatment Market Regional Analysis

- North America dominated the dry eye syndrome treatment market with the largest revenue share of 40.9% in 2025, characterized by high healthcare expenditure, advanced ophthalmic infrastructure, and a strong presence of key pharmaceutical and medical device players

- Patients and clinicians in the region highly value clinically proven prescription therapies, advanced in-office procedures, and diagnostic tools that enable early detection and effective management of dry eye symptoms

- This widespread adoption is further supported by high healthcare expenditure, presence of leading pharmaceutical and medical device companies, and growing access to both OTC and prescription treatments, establishing North America as a key market for both acute and chronic dry eye management

U.S. Dry Eye Syndrome Treatment Market Insight

The U.S. dry eye syndrome treatment market captured the largest revenue share of 79% in 2025 within North America, driven by the increasing prevalence of dry eye, rising screen time, and a strong healthcare infrastructure. Patients and clinicians are prioritizing advanced prescription therapies, in-office procedures, and innovative diagnostic tools for effective disease management. Growing awareness of eye health, combined with high healthcare spending and insurance coverage, further propels market growth. The demand for OTC lubricating drops and preservative-free formulations is also rising among mild-to-moderate cases. Furthermore, the integration of tele-ophthalmology platforms and digital health monitoring enhances treatment accessibility and patient adherence.

Europe Dry Eye Syndrome Treatment Market Insight

The Europe dry eye syndrome treatment market is projected to expand at a substantial CAGR during the forecast period, driven by rising aging populations, high prevalence of digital eye strain, and stringent healthcare standards. Growing urbanization and increased access to ophthalmic care are fostering the adoption of both prescription and OTC therapies. Patients are increasingly seeking effective, convenient, and minimally invasive treatments, boosting demand for advanced therapeutics and device-based interventions. The market is also seeing strong growth in specialty clinics and hospital settings, with dry eye management being integrated into routine eye care services. In addition, government initiatives and awareness campaigns promoting eye health are supporting market expansion across the region.

U.K. Dry Eye Syndrome Treatment Market Insight

The U.K. dry eye syndrome treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising awareness of eye health, increasing prevalence of dry eye, and growing adoption of home-based therapies. Concerns about vision deterioration and lifestyle-related eye strain are encouraging both patients and clinicians to prioritize effective management options. The availability of prescription drugs, OTC lubricants, and procedural therapies enhances treatment accessibility. The U.K.’s well-established healthcare infrastructure, robust retail pharmacy network, and telemedicine platforms are also driving market growth. Consumer preference for advanced, convenient, and patient-friendly therapies continues to stimulate adoption.

Germany Dry Eye Syndrome Treatment Market Insight

The Germany dry eye syndrome treatment market is expected to expand at a considerable CAGR during the forecast period, driven by rising awareness of ocular health, growing geriatric populations, and increasing digital device usage. Germany’s strong healthcare system, high healthcare spending, and emphasis on innovative, clinically proven treatments support the adoption of prescription drugs and device-based therapies. Patients increasingly prefer personalized treatment plans and minimally invasive procedures. Integration of advanced diagnostic tests, such as tear osmolarity and comprehensive eye exams, is facilitating early diagnosis and improved treatment outcomes. In addition, the focus on preventive care and patient education is boosting market penetration in both urban and semi-urban areas.

Asia-Pacific Dry Eye Syndrome Treatment Market Insight

The Asia-Pacific dry eye syndrome treatment market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing digital device usage, rising urbanization, and growing disposable incomes in countries such as China, Japan, and India. The region’s growing awareness of eye health and expanding healthcare infrastructure are driving adoption of both OTC and prescription therapies. In addition, the rise in chronic conditions and environmental factors such as pollution are increasing dry eye prevalence. Government programs promoting preventive eye care and the expansion of specialty clinics are supporting market growth. Affordability of locally manufactured medications and availability of tele-ophthalmology platforms further enhance accessibility.

Japan Dry Eye Syndrome Treatment Market Insight

The Japan dry eye syndrome treatment market is gaining momentum due to high digital device usage, an aging population, and increased focus on preventive healthcare. Patients are seeking convenient, effective, and safe therapies for managing chronic dry eye symptoms. Integration of diagnostic technologies and personalized treatment plans is driving adoption in both clinical and homecare settings. Japan’s strong healthcare system and high awareness about eye health contribute to widespread utilization of prescription medications and advanced therapeutic devices. The demand for patient-friendly and minimally invasive therapies is increasing, particularly among the elderly population. Furthermore, telemedicine and digital health solutions are facilitating early diagnosis and consistent treatment adherence.

India Dry Eye Syndrome Treatment Market Insight

The India dry eye syndrome treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid urbanization, rising digital device usage, and increasing prevalence of dry eye syndrome among the working-age population. India has a growing middle class with higher disposable incomes, boosting demand for OTC and prescription therapies. The government’s focus on eye health awareness campaigns and initiatives for digital eye care services is supporting market growth. Affordable locally manufactured treatments and expansion of retail and online pharmacy channels further increase accessibility. Rising adoption of self-administered therapies and tele-ophthalmology services in both urban and semi-urban areas is propelling the market forward.

Dry Eye Syndrome Treatment Market Share

The Dry Eye Syndrome Treatment industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Alcon Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson and Services, Inc. (U.S.)

- Bausch + Lomb (U.S.)

- URSAPHARM Arzneimittel GmbH (Germany)

- NicOx S.A. (France)

- Novaliq GmbH (Germany)

- OASIS Medical (U.S.)

- AFT Pharmaceuticals (New Zealand)

- Kenvue Brands LLC (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Senju Pharmaceutical Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Scope Ophthalmics Ltd. (U.K.)

- Similasan Corporation (Switzerland)

- Aerie Pharmaceuticals Inc. (U.S.)

What are the Recent Developments in Global Dry Eye Syndrome Treatment Market?

- In May 2025, Grifols received FDA clearance to initiate a Phase II clinical trial for GRF312, an immunoglobulin‑based eye drop designed to address inflammation and immune dysregulation in dry eye disease, marking one of the first efforts to explore immunoglobulin therapy for ocular surface disorders

- In May 2025, the U.S. Food and Drug Administration approved Tryptyr (acoltremon ophthalmic solution) as a new prescription treatment for dry eye disease that stimulates natural tear production by activating corneal sensory nerves, paving the way for introduction in the U.S. market

- In February 2025, DiagnosTear Technologies announced that the pivotal results of the largest clinical dry eye syndrome diagnostic study using TeaRx™ were accepted for presentation at the ARVO 2025 Annual Meeting, highlighting advances in multi‑parameter point‑of‑care diagnostics that improve severity assessment and treatment responsiveness

- In September 2024, perfluorohexyloctane ophthalmic solution (MIEBO™), co‑developed by Bausch + Lomb and Novaliq, had already been FDA‑approved in 2023 and continued wider regulatory availability across markets, as the first prescription eye drop targeting tear evaporation in dry eye disease

- In April 2023, Sun Pharmaceutical launched CEQUA® in India, the country’s first dry eye disease treatment utilizing nanomicellar technology for improved delivery of cyclosporine, expanding access to advanced DED therapy in a major emerging market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.