Global Electric Orthopedic Screwdriver Market

Market Size in USD Million

USD

230.05 Million

USD

366.66 Million

2025

2033

USD

230.05 Million

USD

366.66 Million

2025

2033

| 2026 - 2033 | |

| USD 230.05 Million | |

| USD 366.66 Million | |

| % | |

|

Electric Orthopedic Screwdriver Market Size

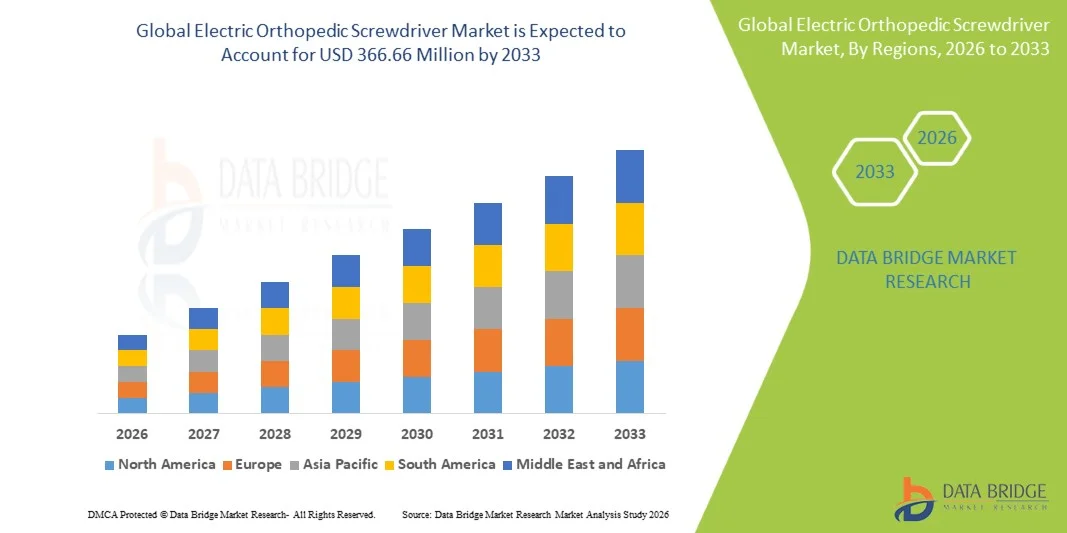

- The global electric orthopedic screwdriver market size was valued at USD 230.05 million in 2025 and is expected to reach USD 366.66 million by 2033, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive surgical procedures and advancements in orthopedic surgical tools, leading to improved precision, efficiency, and surgical outcomes in hospitals and ambulatory surgical centers

- Furthermore, rising demand for technologically advanced, ergonomically designed, and battery-operated surgical devices that enhance workflow efficiency and reduce operative time is driving the preference for electric orthopedic screwdrivers. These converging factors are accelerating the adoption of advanced orthopedic instruments, thereby significantly supporting the industry's growth

Electric Orthopedic Screwdriver Market Analysis

- Electric orthopedic screwdrivers, offering powered torque and precision for fastening and removing screws during orthopedic procedures, are increasingly vital components of modern surgical systems in both hospital and clinical settings due to their enhanced accuracy, reduced surgeon fatigue, and ability to improve efficiency in complex orthopedic interventions

- The escalating demand for electric orthopedic screwdrivers is primarily fueled by the rising prevalence of musculoskeletal disorders, increasing number of orthopedic surgeries, and growing preference for minimally invasive and precision-driven surgical procedures, along with advancements in battery-powered and ergonomically designed surgical instruments

- North America dominated the electric orthopedic screwdriver market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of innovative surgical technologies, and a strong presence of key medical device manufacturers, with the U.S. witnessing significant utilization in hospitals and ambulatory surgical centers driven by continuous technological advancements and procedural efficiency improvements

- Asia-Pacific is expected to be the fastest growing region in the electric orthopedic screwdriver market during the forecast period due to expanding healthcare infrastructure, rising surgical volumes, increasing healthcare expenditure, and growing adoption of advanced orthopedic surgical equipment in emerging economies

- Extremities and Trauma (SET) orthopedic devices segment dominated the electric orthopedic screwdriver market with a significant share of 41.7% in 2025, driven by the high incidence of trauma cases and fractures requiring surgical fixation, along with the frequent use of powered screwdrivers in emergency and reconstructive orthopedic procedures

Report Scope and Electric Orthopedic Screwdriver Market Segmentation

|

Attributes |

Electric Orthopedic Screwdriver Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Electric Orthopedic Screwdriver Market Trends

“Integration of Advanced Power Systems and Ergonomic Design”

- A significant and accelerating trend in the global electric orthopedic screwdriver market is the increasing integration of advanced battery technologies and ergonomic designs, enhancing surgical precision and efficiency in orthopedic procedures across diverse healthcare settings

- For instance, leading manufacturers are introducing battery-powered orthopedic screwdrivers with longer operational life and lightweight designs, enabling surgeons to perform procedures with greater ease and reduced fatigue during prolonged surgeries

- Technological advancements in electric orthopedic screwdrivers enable features such as adjustable torque control, improved speed modulation, and enhanced sterilization compatibility, ensuring optimal performance and safety during surgical interventions

- The incorporation of user-friendly interfaces and cordless functionality allows surgeons to operate with improved mobility and control, facilitating smoother workflows and reducing dependency on external power sources in operating rooms

- This trend towards more efficient, portable, and precision-driven surgical instruments is fundamentally reshaping surgical practices in orthopedics. Consequently, companies such as Stryker and DePuy Synthes are developing advanced electric orthopedic screwdrivers with enhanced performance capabilities and ergonomic benefits

- The demand for electric orthopedic screwdrivers offering superior precision, portability, and ease of use is growing rapidly across hospitals and surgical centers, as healthcare providers increasingly prioritize improved patient outcomes and operational efficiency

- Growing integration of electric orthopedic screwdrivers with digital surgical ecosystems and navigation systems is further enhancing procedural accuracy and supporting data-driven surgical practices

Electric Orthopedic Screwdriver Market Dynamics

Driver

“Growing Need Due to Rising Orthopedic Surgeries and Technological Advancements”

- The increasing prevalence of orthopedic disorders and trauma cases, coupled with the rising number of surgical interventions, is a significant driver for the heightened demand for electric orthopedic screwdrivers

- For instance, in March 2025, Stryker Corporation introduced advanced battery-powered surgical tools aimed at improving efficiency and precision in orthopedic procedures, reflecting ongoing innovation in the market

- As healthcare providers focus on improving surgical outcomes and reducing operation time, electric orthopedic screwdrivers offer advantages such as consistent torque delivery, reduced manual effort, and enhanced procedural accuracy

- Furthermore, the growing adoption of minimally invasive surgical techniques and advanced orthopedic equipment is driving the demand for high-performance powered surgical instruments in hospitals and clinics

- The increasing investments in healthcare infrastructure and the expansion of ambulatory surgical centers are further contributing to the adoption of electric orthopedic screwdrivers across both developed and emerging markets

- The trend towards technologically advanced surgical solutions and the need for improved efficiency in operating rooms are key factors propelling the growth of the electric orthopedic screwdriver market

- Rising geriatric population globally, which is more prone to fractures and joint-related conditions, is further increasing the demand for orthopedic surgical procedures and associated powered instruments

- Growing preference among surgeons for precision-driven and time-efficient tools is accelerating the shift from manual to electric orthopedic screwdrivers in clinical practice

Restraint/Challenge

“High Equipment Costs and Maintenance Requirements”

- The high cost associated with advanced electric orthopedic screwdrivers and related surgical systems poses a significant challenge to widespread adoption, particularly in cost-sensitive healthcare settings and developing regions

- For instance, premium battery-operated surgical tools with advanced features often require substantial initial investment, limiting their accessibility for smaller hospitals and clinics with constrained budgets

- In addition, the need for regular maintenance, sterilization, and battery management adds to the overall operational costs, creating financial and logistical challenges for healthcare providers

- Concerns related to device reliability, potential technical failures, and the requirement for trained personnel to operate advanced equipment may also hinder adoption in certain healthcare facilities

- While technological advancements continue to improve device performance, the cost-benefit considerations remain a key factor influencing purchasing decisions among end users

- Overcoming these challenges through cost optimization, technological standardization, and increased accessibility of advanced surgical tools will be essential for sustained market growth

- Limited reimbursement policies for advanced surgical instruments in certain regions may restrict procurement decisions by healthcare providers

- Supply chain disruptions and dependency on specialized components for battery-powered systems can impact product availability and increase overall costs

Electric Orthopedic Screwdriver Market Scope

The market is segmented on the basis of application and end user.

- By Application

On the basis of application, the global electric orthopedic screwdriver market is segmented into hip orthopedic devices, knee orthopedic devices, spine orthopedic devices, craniomaxillofacial orthopedic devices, dental orthopedic devices, sports injuries, and extremities and trauma (SET) orthopedic devices. The extremities and trauma (SET) orthopedic devices segment dominated the market with the largest market revenue share of 41.7% in 2025, driven by the high incidence of fractures, road accidents, and trauma-related injuries requiring immediate surgical fixation. These procedures frequently require precise screw placement, making electric orthopedic screwdrivers essential tools in emergency and reconstructive surgeries. The increasing number of trauma cases globally and the need for efficient surgical outcomes further support the dominance of this segment. In addition, advancements in trauma fixation systems and the growing adoption of powered surgical tools in emergency care settings contribute significantly to segment growth. Hospitals prioritize SET procedures due to their urgency and frequency, thereby boosting the demand for these devices. The consistent rise in orthopedic trauma cases ensures sustained demand for electric orthopedic screwdrivers in this segment.

The spine orthopedic devices segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing prevalence of spinal disorders and the rising number of spinal fusion and corrective surgeries. The growing aging population and sedentary lifestyles have significantly contributed to spinal conditions such as degenerative disc disease and spinal deformities. Electric orthopedic screwdrivers are widely used in spine surgeries for accurate screw placement and improved surgical precision. Technological advancements in spinal implants and navigation-assisted surgeries further enhance the adoption of powered surgical tools in this segment. In addition, the shift toward minimally invasive spine procedures is driving demand for compact and high-performance electric screwdrivers. Increasing healthcare investments and awareness regarding spinal health are also contributing to the rapid growth of this segment.

- By End User

On the basis of end user, the global electric orthopedic screwdriver market is segmented into hospital, clinic, and others. The hospital segment dominated the market with the largest market revenue share in 2025, attributed to the high volume of orthopedic surgeries performed in hospital settings and the availability of advanced surgical infrastructure. Hospitals are equipped with specialized operating rooms and skilled professionals, enabling the adoption of technologically advanced surgical tools such as electric orthopedic screwdrivers. The presence of emergency care facilities and trauma centers further drives the demand for powered surgical instruments in hospitals. In addition, higher patient inflow and increased surgical procedures contribute to the dominance of this segment. Government and private investments in hospital infrastructure also support the widespread adoption of advanced orthopedic devices. The preference for hospitals for complex and high-risk procedures further strengthens this segment’s leading position.

The clinic segment is expected to witness the fastest growth rate during the forecast period, driven by the increasing shift toward outpatient surgical procedures and minimally invasive treatments. Clinics and ambulatory surgical centers are gaining popularity due to cost-effectiveness, reduced hospital stays, and faster patient recovery times. The growing availability of compact and portable electric orthopedic screwdrivers makes them suitable for use in smaller healthcare settings. In addition, advancements in surgical techniques are enabling clinics to perform a wider range of orthopedic procedures. Increasing patient preference for convenient and accessible healthcare services further supports the growth of this segment. The expansion of outpatient care facilities, particularly in emerging economies, is also contributing to the rising adoption of electric orthopedic screwdrivers in clinics.

Electric Orthopedic Screwdriver Market Regional Analysis

- North America dominated the electric orthopedic screwdriver market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of innovative surgical technologies, and a strong presence of key medical device manufacturers

- Healthcare providers in the region highly value the precision, efficiency, and ergonomic benefits offered by electric orthopedic screwdrivers, along with their ability to improve surgical outcomes and reduce procedure time in complex orthopedic interventions

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, and the presence of leading medical device manufacturers, along with the growing preference for minimally invasive procedures, establishing electric orthopedic screwdrivers as essential tools in modern surgical practices

U.S. Electric Orthopedic Screwdriver Market Insight

The U.S. electric orthopedic screwdriver market captured the largest revenue share in 2025 within North America, fueled by the high volume of orthopedic surgeries and the rapid adoption of advanced surgical technologies. Healthcare providers are increasingly prioritizing precision-driven and efficient surgical tools to enhance patient outcomes and reduce operation time. The growing presence of leading medical device manufacturers, combined with continuous innovation in battery-powered surgical systems, further propels the market. Moreover, the increasing adoption of minimally invasive procedures and advanced orthopedic techniques is significantly contributing to the market's expansion.

Europe Electric Orthopedic Screwdriver Market Insight

The Europe electric orthopedic screwdriver market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare expenditure and the rising demand for advanced surgical solutions. The growth in aging population, coupled with the prevalence of orthopedic disorders, is fostering the adoption of electric surgical instruments. European healthcare systems are also focusing on improving surgical efficiency and patient safety, encouraging the use of precision-based tools. The region is experiencing steady growth across hospitals and specialty clinics, with electric orthopedic screwdrivers being widely utilized in both routine and complex procedures.

U.K. Electric Orthopedic Screwdriver Market Insight

The U.K. electric orthopedic screwdriver market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing number of orthopedic procedures and a strong focus on improving surgical outcomes. In addition, the demand for technologically advanced and ergonomically designed surgical instruments is encouraging healthcare providers to adopt electric screwdrivers. The UK’s well-established healthcare infrastructure, along with ongoing investments in medical technologies, is expected to continue to stimulate market growth.

Germany Electric Orthopedic Screwdriver Market Insight

The Germany electric orthopedic screwdriver market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of advanced surgical technologies and the demand for high-quality medical devices. Germany’s strong healthcare infrastructure, combined with its emphasis on innovation and precision engineering, promotes the adoption of electric orthopedic screwdrivers, particularly in hospitals and specialized surgical centers. The integration of advanced surgical tools with modern healthcare systems is also becoming increasingly prevalent, aligning with the country’s focus on efficiency and patient safety.

Asia-Pacific Electric Orthopedic Screwdriver Market Insight

The Asia-Pacific electric orthopedic screwdriver market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing healthcare investments, rising surgical volumes, and expanding healthcare infrastructure in countries such as China, Japan, and India. The region's growing burden of orthopedic disorders and trauma cases, supported by improving access to healthcare services, is driving the adoption of advanced surgical instruments. Furthermore, as APAC emerges as a key manufacturing hub for medical devices, the affordability and accessibility of electric orthopedic screwdrivers are expanding across a wider range of healthcare facilities.

Japan Electric Orthopedic Screwdriver Market Insight

The Japan electric orthopedic screwdriver market is gaining momentum due to the country’s advanced healthcare system, aging population, and increasing demand for precision surgical tools. The Japanese market places significant emphasis on efficiency and patient safety, and the adoption of electric orthopedic screwdrivers is driven by the growing number of orthopedic and spinal procedures. The integration of advanced surgical instruments with modern healthcare technologies is fueling growth. Moreover, Japan's aging population is likely to spur demand for reliable and easy-to-use surgical tools in both hospitals and specialty clinics.

India Electric Orthopedic Screwdriver Market Insight

The India electric orthopedic screwdriver market accounted for a significant market share in Asia Pacific in 2025, attributed to the country's expanding healthcare infrastructure, rising incidence of trauma and orthopedic conditions, and increasing adoption of advanced surgical technologies. India is emerging as a key market for medical devices, and electric orthopedic screwdrivers are becoming increasingly utilized in hospitals and surgical centers. The push towards improving healthcare accessibility, along with government initiatives and the presence of domestic and international manufacturers, are key factors propelling the market in India.

Electric Orthopedic Screwdriver Market Share

The Electric Orthopedic Screwdriver industry is primarily led by well-established companies, including:

- Zimmer Biomet (U.S.)

- Smith & Nephew (U.K.)

- Medtronic (Ireland)

- Stryker (U.S.)

- B. Braun SE (Germany)

- NuVasive, Inc. (U.S.)

- DJO, LLC (U.S.)

- Institut Straumann AG (Switzerland)

- OSSTEM IMPLANT CO., LTD. (South Korea)

- Narang Medical Limited (U.S.)

- Globus Medical, Inc. (U.S.)

- Arthrex, Inc. (U.S.)

- CONMED Corporation (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- RTI Surgical, Inc. (U.S.)

- W. L. Gore & Associates, Inc. (U.S.)

- Corin Group (U.K.)

- Medacta International SA (Switzerland)

- Orthofix Medical Inc. (U.S.)

What are the Recent Developments in Global Electric Orthopedic Screwdriver Market?

- In October 2025, Johnson & Johnson announced plans to separate its orthopedics business (DePuy Synthes) into a standalone entity to strengthen focus on specialized orthopedic innovations and technologies. This strategic move aims to enhance operational efficiency and accelerate innovation in orthopedic devices, including powered surgical instruments such as electric screwdrivers. The separation is expected to allow more targeted investments in research and development within the orthopedic segment

- In March 2025, Johnson & Johnson MedTech showcased a new portfolio of digital orthopedic solutions at the AAOS 2025 conference, including advanced powered surgical tools and data-driven technologies. These innovations are designed to enhance surgical precision, streamline workflows, and improve patient outcomes across orthopedic procedures. The company emphasized integration of powered instruments with digital platforms and analytics for better intraoperative decision-making

- In August 2024, Stryker Corporation announced the launch of its CD NXT System, an advanced addition to its surgical power tools portfolio, designed to provide real-time depth measurement and enhanced precision during orthopedic procedures. This innovation improves screw placement accuracy and reduces the risk of over-penetration in bone fixation surgeries. The system reflects growing demand for intelligent and precision-driven powered surgical instruments

- In April 2023, Johnson & Johnson (through DePuy Synthes) advanced its VIPER PRIME™ system, featuring an integrated screwdriver-controlled mechanism for streamlined pedicle screw placement. This system allows surgeons to insert screws in a single pass without the need for multiple instruments, improving efficiency and reducing procedural complexity. The innovation demonstrates the evolution of electric screwdriver-integrated systems in spine surgeries

- In September 2022, Johnson & Johnson’s DePuy Synthes announced the launch of its UNIUM™ orthopedic power tool system, designed to improve surgical efficiency and ergonomics across trauma, spine, and sports medicine procedures. The system focuses on lightweight design, reliability, and ease of use, enabling surgeons to perform procedures with greater precision and reduced fatigue. It also supports a wide range of attachments, making it adaptable for multiple orthopedic applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.