Global Esophageal Cancer Market

Market Size in USD Billion

USD

1.45 Billion

USD

2.79 Billion

2024

2032

USD

1.45 Billion

USD

2.79 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.45 Billion | |

| USD 2.79 Billion | |

| % | |

|

Esophageal Cancer Market Size

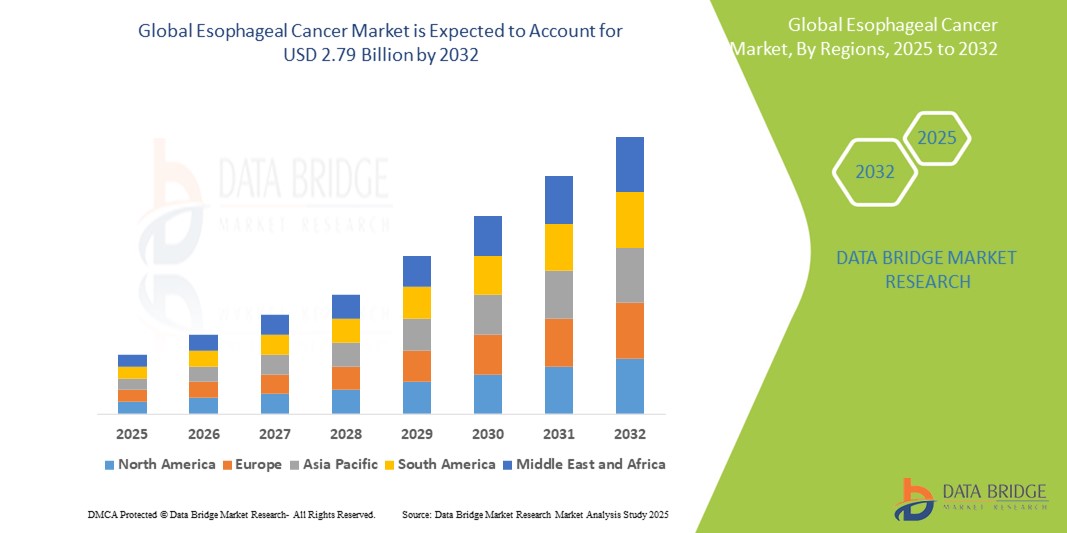

- The global esophageal cancer market size was valued at USD 1.45 billion in 2024 and is expected to reach USD 2.79 billion by 2032, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by the increasing global incidence and prevalence of esophageal cancer, coupled with significant technological progress in diagnostic tools, surgical techniques, and advanced therapeutic options. This is leading to improved patient outcomes and more comprehensive disease management

- Furthermore, rising healthcare demand for effective, personalized, and integrated solutions for early detection and treatment of esophageal cancer is establishing novel therapies and diagnostic modalities as the modern standard of care. These converging factors are accelerating the uptake of esophageal cancer solutions, thereby significantly boosting the industry's growth

Esophageal Cancer Market Analysis

- Esophageal cancer, encompassing both squamous-cell carcinoma and adenocarcinoma, is increasingly recognized as a critical global health concern due to its rising incidence, poor prognosis, and the urgent need for earlier diagnosis and effective treatment modalities

- The accelerating demand for advanced esophageal cancer therapies is primarily fueled by increasing awareness, the introduction of immunotherapies and targeted therapies, and rising healthcare expenditure globally

- North America dominated the esophageal cancer market with the largest revenue share of 41.16% in 2024, characterized by early adoption of innovative oncology treatments, high healthcare spending, and a strong presence of pharmaceutical giants

- Asia-Pacific is expected to be the fastest growing region with a CAGR of 8.7% in the esophageal Cancer market during the forecast period due to increasing urbanization, rising disposable incomes, expanding cancer registries, and growing access to healthcare infrastructure

- Chemotherapy segment dominated the esophageal cancer market with a market share of 38.5% in 2024, driven by its continued role in first-line treatment protocols and its widespread availability across both developed and developing regions

Report Scope and Esophageal Cancer Market Segmentation

|

Attributes |

Esophageal Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Esophageal Cancer Market Trends

“Enhanced Convenience Through Advanced Diagnostic and Treatment Technologies”

- A significant and accelerating trend in the global Esophageal Cancer market is the advancement and integration of novel diagnostic and treatment technologies, including minimally invasive procedures and biomarker-based detection. This technological evolution is significantly improving early diagnosis, patient outcomes, and access to personalized therapies

- For instance, liquid biopsy is emerging as a non-invasive technique for detecting esophageal cancer biomarkers, enabling earlier intervention and monitoring of treatment response. Similarly, endoscopic submucosal dissection (ESD) is gaining traction for early-stage cancer removal with minimal complications

- The application of precision oncology is enabling clinicians to match patients with therapies based on genetic profiling. Targeted therapies such as trastuzumab for HER2-positive cases and checkpoint inhibitors such as nivolumab for advanced disease are transforming treatment protocols.

- Integrated diagnostic platforms are allowing clinicians to simultaneously assess tumor location, stage, and molecular characteristics, streamlining the treatment planning process. This convergence is improving workflow efficiency and enhancing individualized care strategies

- This trend towards more accurate, less invasive, and highly personalized diagnosis and treatment options is fundamentally reshaping clinical expectations in oncology. Consequently, companies such as Roche and Merck are investing in companion diagnostics and expanding their oncology portfolios to cater to evolving therapeutic needs

- The demand for esophageal cancer solutions that combine precision, minimal invasiveness, and real-time decision support is growing rapidly across healthcare systems worldwide, as patients and providers increasingly prioritize early detection, treatment efficacy, and improved survival rates

Esophageal Cancer Market Dynamics

Driver

“Growing Need Due to Rising Disease Incidence and Improved Treatment Accessibility”

- The increasing global incidence of esophageal cancer, driven by risk factors such as tobacco and alcohol consumption, poor dietary habits, and rising cases of gastroesophageal reflux disease (GERD), is a significant driver for the growing demand for early detection and effective treatment solutions

- For instance, in February 2024, the World Health Organization emphasized the rising burden of gastrointestinal cancers, including esophageal cancer, across Asia and Africa, urging health systems to enhance cancer screening and treatment infrastructure. Such international focus is expected to boost the Esophageal Cancer industry growth during the forecast period

- As awareness about the importance of early detection grows, healthcare systems are increasingly investing in endoscopic screening programs and advanced diagnostic modalities, allowing for timely and more effective intervention

- Furthermore, the expanding reach of healthcare services, especially in developing countries, and increasing access to advanced treatments such as immunotherapy and targeted therapy are reshaping the treatment landscape for esophageal cancer

- The demand for less invasive procedures, improved patient outcomes, and government-led cancer awareness campaigns are propelling the development and adoption of innovative therapeutic solutions. The trend toward personalized medicine and genomic profiling is further contributing to the rise in precision-based esophageal cancer treatments

Restraint/Challenge

“High Treatment Costs and Limited Access to Early Diagnosis”

- High treatment costs, particularly for advanced therapies such as immunotherapy and biologics, continue to pose a significant barrier to the widespread adoption of modern esophageal cancer treatments. This is especially challenging in low-income regions where healthcare reimbursement is limited

- For instance, despite clinical success, drugs such as nivolumab and pembrolizumab come with substantial price tags, making them inaccessible to a large segment of the patient population in underfunded healthcare systems

- Limited availability of early screening programs in rural and underserved areas often leads to late-stage diagnoses, reducing the effectiveness of treatment and negatively impacting survival rates. Delays in seeking medical care, coupled with insufficient diagnostic infrastructure, further exacerbate this issue Tackling these challenges requires broader healthcare policy support, including subsidized treatment programs, public-private partnerships, and investments in affordable screening technologies. Moreover, global health organizations and local governments need to work together to increase public awareness and expand diagnostic accessibility

Esophageal Cancer Market Scope

The market is segmented on the basis of type, treatment type, route of administration, end-users, and distribution channel.

• By Type

On the basis of type, the esophageal cancer market is segmented into esophageal squamous-cell carcinoma, esophageal adenocarcinoma, and others. The esophageal squamous-cell carcinoma segment held the largest market revenue share of 58.3% in 2024, attributed to its higher global prevalence, especially in regions such as Asia and parts of Africa. This form of cancer is strongly associated with risk factors such as tobacco use, alcohol consumption, and nutritional deficiencies, contributing to its high incidence.

The esophageal adenocarcinoma segment is anticipated to witness the fastest CAGR of 7.4% from 2025 to 2032, driven by the increasing prevalence of obesity and gastroesophageal reflux disease (GERD), particularly in Western countries. The rising diagnosis of Barrett’s esophagus as a precursor condition is also boosting the demand for targeted therapies in this subtype.

• By Treatment Type

On the basis of treatment type, the market is segmented into chemotherapy, targeted therapy, radiation therapy, immunotherapy, and others. The chemotherapy segment held the largest market revenue share of 38.5% in 2024, as it remains the standard treatment approach in both localized and advanced stages of esophageal cancer. Its use in combination with radiation and surgery enhances treatment outcomes in many patients.

The immunotherapy segment is expected to witness the fastest CAGR of 9.1% from 2025 to 2032, owing to growing clinical adoption of immune checkpoint inhibitors such as PD-1/PD-L1 inhibitors, particularly in recurrent or metastatic esophageal cancer cases. Increasing regulatory approvals and positive trial results continue to fuel momentum in this segment.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The parenteral segment held the largest market revenue share of 66.7% in 2024, driven by the fact that most chemotherapy and targeted therapies are administered intravenously. Hospitals and oncology centers continue to prefer parenteral routes due to their controlled dosage delivery.

The oral segment is projected to witness the fastest CAGR of 6.3% from 2025 to 2032, with a rising number of oral formulations entering the market, improving patient compliance and enabling outpatient treatment regimens.

• By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty centres, and others. The hospitals segment captured the largest market revenue share of 61.5% in 2024, as these settings offer the most comprehensive diagnostic, surgical, and therapeutic care for esophageal cancer patients.

The homecare segment is projected to record the fastest CAGR of 6.9% from 2025 to 2032, due to an increasing shift towards oral therapies and remote monitoring technologies, enabling care delivery outside traditional healthcare facilities.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment held the dominant market share of 53.4% in 2024, supported by the centralized procurement and dispensation of high-cost oncology medications within institutional settings.

The online pharmacy segment is expected to grow at the fastest CAGR of 8.2% from 2025 to 2032, driven by growing digital health adoption, ease of medication refills for chronic patients, and expanded access to specialty drugs through e-commerce platforms.

Esophageal Cancer Market Regional Analysis

- North America dominated the esophageal cancer market with the largest revenue share of 41.16% in 2024, primarily driven by the high prevalence of esophageal adenocarcinoma, widespread adoption of advanced treatment technologies, and robust healthcare infrastructure

- The region benefits from early diagnosis due to enhanced screening programs, strong reimbursement frameworks, and the presence of major pharmaceutical companies actively involved in clinical trials and new drug approvals

- In addition, increasing lifestyle-related risk factors such as obesity, GERD, and smoking contribute significantly to the region’s high disease burden, reinforcing the demand for innovative treatment modalities and expanding the therapeutic landscape

U.S. Esophageal Cancer Market Insight

The U.S. esophageal cancer market captured the largest revenue share of 73.8% in 2024 within North America, driven by rapid advancements in diagnostic technologies and increased adoption of personalized treatment approaches. The rising incidence of esophageal adenocarcinoma and government initiatives promoting early screening are key growth factors. Furthermore, strong investments in clinical research and availability of advanced therapeutics contribute to robust market expansion.

Europe Esophageal Cancer Market Insight

The Europe esophageal cancer market held a revenue share of 28.3% in 2024 and is expected to grow at a CAGR of around 11% during the forecast period. Growth is supported by increasing awareness programs and improvements in healthcare infrastructure. Stringent regulatory frameworks and growing adoption of targeted therapies are fueling market expansion.

U.K. Esophageal Cancer Market Insight

The U.K. esophageal cancer market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by widespread screening programs and increasing healthcare expenditure. The government’s focus on cancer research and availability of innovative treatment modalities such as immunotherapy are key drivers.

Germany Esophageal Cancer Market Insight

Germany’s esophageal cancer market is expected to expand at a considerable CAGR during the forecast period. The country’s robust healthcare system and growing patient awareness, combined with accessibility to advanced therapies, contribute significantly to this growth.

Asia-Pacific Esophageal Cancer Market Insight

The Asia-Pacific esophageal cancer market is poised to grow at the fastest CAGR of 8.7% during the forecast period of 2025 to 2032. This rapid growth is driven by rising prevalence of risk factors, increasing healthcare spending, and government initiatives in countries such as China, Japan, and India.

China Esophageal Cancer Market Insight

The China esophageal cancer market commands the largest share within the Asia-Pacific region with 12.2% of the global market revenue in 2024, supported by urbanization, government cancer programs, and increasing accessibility to advanced treatments. Rising awareness campaigns and strong domestic pharmaceutical manufacturing capabilities are accelerating early diagnosis and treatment uptake. The presence of leading regional oncology centers also contributes to faster innovation and clinical trial activity.

India Esophageal Cancer Market Insight

The India esophageal cancer market esophageal cancer market currently holds an 5% share of the Asia-Pacific market. This growth is driven by increasing incidence rates, expanding healthcare infrastructure, government initiatives to improve cancer care, and rising adoption of advanced therapies. Increasing collaboration between public and private healthcare providers is helping bridge treatment gaps.In addition, a growing patient pool and focus on affordable drug development present vast opportunities for market expansion.

Esophageal Cancer Market Share

The esophageal cancer industry is primarily led by well-established companies, including:

- Johnson & Johnson Services, Inc. (U.S.)

- Cipla (U.S.)

- Abbott (U.S.)

- AbbVie Inc. (U.S.)

- Merck KGaA (Germany)

- LEO Pharma A/S (Denmark)

- Bausch Health Companies Inc. (Canada)

- Sun Pharmaceutical Industries Ltd. (India)

- Aurobindo Pharma (India)

- Lupin (India)

- Hikma Pharmaceuticals PLC (U.K.)

- Amneal Pharmaceuticals LLC (U.S.)

- Pfizer Inc. (U.S.)

- Viatris Inc. (U.S.)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Jiangsu Hengrui Pharmaceuticals Co., Ltd. (China)

Latest Developments in Global Esophageal Cancer Market

- In May 2024, Bristol-Myers Squibb Company announced promising Phase III clinical trial results for its immune checkpoint inhibitor nivolumab in combination with chemotherapy for treating advanced esophageal squamous cell carcinoma. The study demonstrated improved overall survival and progression-free survival, reinforcing the role of immunotherapy in first-line treatment settings and highlighting the company's focus on innovative oncology therapies

- In April 2024, Merck KGaA revealed the expansion of its oncology pipeline with the initiation of a global clinical trial evaluating its anti-PD-L1 antibody in combination with targeted therapies for esophageal adenocarcinoma. This move aims to enhance therapeutic efficacy and patient outcomes in hard-to-treat cases, positioning Merck as a key innovator in the immuno-oncology segment

- In February 2024, Pfizer Inc. entered into a collaborative agreement with a biotechnology firm to develop next-generation biomarkers for early diagnosis and treatment response in esophageal cancer. The initiative focuses on leveraging AI and genomics to improve diagnostic accuracy and personalize treatment protocols, reflecting a strategic shift toward precision oncology

- In January 2024, Novartis AG launched a real-world data registry program across multiple countries to monitor long-term outcomes in patients treated with combination therapy for esophageal cancer. This post-marketing initiative supports evidence-based treatment planning and helps refine clinical guidelines by generating valuable insights on safety and effectiveness

- In December 2023, Johnson & Johnson Services, Inc. received FDA fast-track designation for its investigational monoclonal antibody targeting HER2-expressing esophageal tumors. The therapy shows promise in early clinical trials and is part of the company’s broader effort to address unmet needs in upper gastrointestinal cancers

- In November 2023, Sun Pharmaceutical Industries Ltd. announced the launch of a generic version of paclitaxel used in the chemotherapeutic management of esophageal cancer across several emerging markets. The move aims to improve affordability and access to essential oncology treatments, particularly in Asia and Africa

- In October 2023, Aurobindo Pharma received regulatory approval in India for its novel fixed-dose combination therapy designed to treat late-stage esophageal carcinoma. The combination therapy has demonstrated improved patient adherence and reduced toxicity profiles in clinical evaluations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.