Global Fixed Operator Telecom Service Assurance Market

Market Size in USD Million

USD

986.40 Million

USD

2,053.70 Million

2025

2033

USD

986.40 Million

USD

2,053.70 Million

2025

2033

| 2026 - 2033 | |

| USD 986.40 Million | |

| USD 2,053.70 Million | |

| % | |

|

Fixed Operator Telecom Service Assurance Market Size

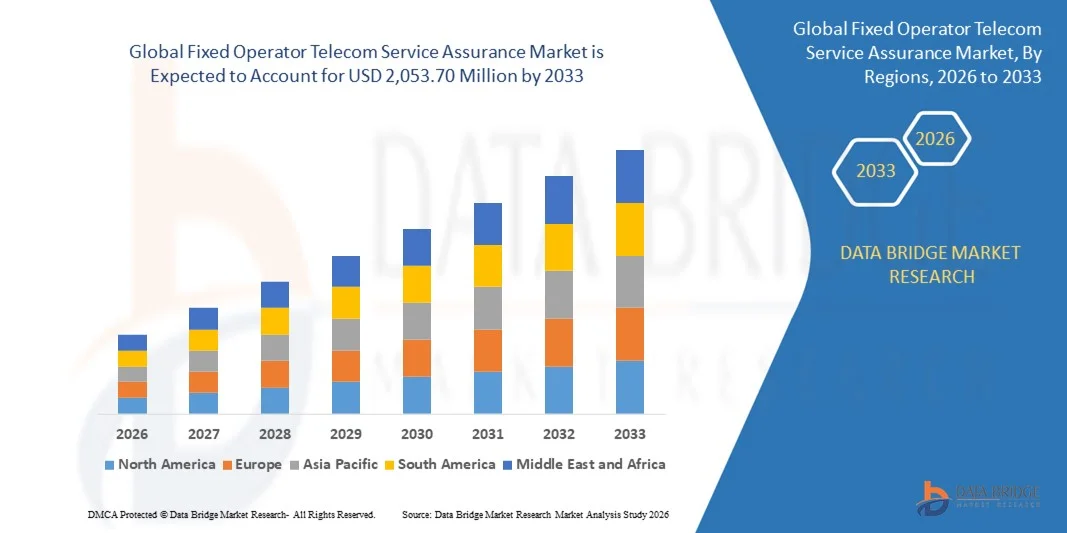

- The global fixed operator telecom service assurance market size was valued at USD 986.40 million in 2025 and is expected to reach USD 2,053.70 million by 2033, at a CAGR of 9.60% during the forecast period

- The market growth is largely fuelled by increasing demand for high-quality network performance monitoring, proactive fault detection, and enhanced customer experience management

- Rising adoption of advanced analytics, AI, and automation in telecom networks is driving operators to implement service assurance solutions for improved operational efficiency

Fixed Operator Telecom Service Assurance Market Analysis

- The market is witnessing significant growth due to operators focusing on reducing service downtime, optimizing network performance, and ensuring compliance with stringent quality standards

- Increasing investment in digital transformation initiatives, cloud-based network management, and end-to-end service visibility is boosting the adoption of telecom service assurance solutions

- North America dominated the global fixed operator telecom service assurance market with the largest revenue share of 38.7% in 2025, driven by increasing investments in advanced network monitoring, fault management, and predictive analytics solutions

- Asia-Pacific region is expected to witness the highest growth rate in the global fixed operator telecom service assurance market, driven by rapid digitalization, government initiatives supporting smart city and network infrastructure development, increasing telecom subscribers, and rising adoption of cloud and AI-powered service assurance solutions

- The Software segment held the largest market revenue share in 2025, driven by the increasing need for real-time monitoring, fault detection, and predictive analytics to ensure uninterrupted network performance. Software solutions enable operators to proactively detect network anomalies, optimize bandwidth allocation, and reduce service disruptions. Advanced analytics and AI integration in software platforms are enhancing operational efficiency and customer experience. These solutions are widely adopted by telecom providers to meet stringent SLA requirements and maintain high-quality service delivery

Report Scope and Fixed Operator Telecom Service Assurance Market Segmentation

|

Attributes |

Fixed Operator Telecom Service Assurance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Fixed Operator Telecom Service Assurance Market Trends

Rising Demand for Advanced Network Monitoring and Automation

- The growing focus on reliable, high-performance networks is significantly shaping the fixed operator telecom service assurance market, as operators increasingly require solutions that ensure service quality, minimize downtime, and proactively detect network faults. Service assurance solutions are gaining traction due to their ability to enhance operational efficiency, customer experience, and compliance, driving adoption across telecom operators and managed service providers

- Increasing awareness around the benefits of predictive maintenance, network optimization, and automated fault detection has accelerated the demand for fixed operator telecom service assurance solutions in broadband, 5G, and enterprise networks. Telecom operators and service providers are actively seeking platforms that provide real-time insights, analytics, and intelligent alerts, prompting vendors to enhance product capabilities and integration options

- Digital transformation and the growing adoption of AI, machine learning, and cloud-native platforms are influencing purchasing decisions, with telecom operators emphasizing seamless integration, scalability, and advanced analytics. These factors help operators differentiate their offerings, improve SLA adherence, and reduce operational costs, while also driving the adoption of next-generation network management tools

- For instance, in 2024, AT&T in the U.S. and BT Group in the U.K. expanded their service assurance portfolios by incorporating AI-driven monitoring and predictive analytics across fixed-line and broadband networks. These implementations were introduced in response to rising demand for improved network performance and customer experience, with deployment across enterprise and residential segments

- While demand for fixed operator telecom service assurance is growing, sustained market expansion depends on continuous R&D, cost-effective deployment, and integration with legacy systems. Vendors are also focusing on improving interoperability, cloud readiness, and developing innovative solutions that balance cost, performance, and scalability for broader adoption

Fixed Operator Telecom Service Assurance Market Dynamics

Driver

Growing Preference for AI-Enabled and Cloud-Based Network Monitoring

- Rising demand for intelligent, cloud-enabled service assurance solutions is a major driver for the market. Operators are increasingly replacing legacy monitoring tools with AI-powered platforms to enhance fault detection, predictive maintenance, and customer experience. This trend is also pushing research into advanced analytics and machine learning algorithms for network optimization

- Expanding applications in broadband, 5G, and enterprise networks are influencing market growth. Fixed operator service assurance solutions help enhance service quality, reduce downtime, and improve operational efficiency while maintaining compliance with regulatory standards. The increasing need for SLA adherence and improved QoE (Quality of Experience) further reinforces this trend

- Telecom operators are actively promoting AI-driven and cloud-based service assurance platforms through network upgrades, digital transformation initiatives, and vendor partnerships. These efforts are supported by the growing demand for automated fault management, predictive analytics, and real-time monitoring, encouraging collaboration between solution providers and operators to improve network performance

- For instance, in 2023, Verizon in the U.S. and Vodafone in Germany reported increased adoption of AI-enabled network monitoring and predictive analytics solutions in enterprise and residential segments. This expansion followed higher demand for proactive service management, operational efficiency, and SLA compliance, driving network reliability and customer satisfaction

- Although rising digitalization and cloud adoption support growth, wider market penetration depends on cost optimization, seamless integration, and scalable deployment models. Investment in cloud infrastructure, advanced analytics, and AI capabilities will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Implementation Costs And Integration Complexities

- The relatively high cost of deploying AI-enabled and cloud-based service assurance solutions compared to traditional monitoring tools remains a key challenge, limiting adoption among price-sensitive operators. Expenses related to software licensing, hardware upgrades, and workforce training contribute to elevated implementation costs

- Awareness and technical expertise remain uneven, particularly in emerging markets where advanced service assurance demand is still developing. Limited understanding of functional benefits restricts adoption across certain operator segments, slowing innovation uptake in less mature regions

- Integration with legacy networks and complex IT infrastructures also impacts market growth, as service assurance solutions require compatibility with diverse hardware, software, and protocol standards. Operational challenges, data privacy requirements, and multi-vendor environments further increase deployment complexity

- For instance, in 2024, mid-sized operators in Southeast Asia and Latin America reported slower adoption of AI-based network monitoring due to high implementation costs, integration challenges, and limited in-house expertise. These factors also prompted delays in network optimization projects, affecting service quality and operational efficiency

- Overcoming these challenges will require cost-efficient deployment, standardized integration frameworks, and focused training initiatives for operators. Collaboration with system integrators, managed service providers, and technology vendors can help unlock the long-term growth potential of the global fixed operator telecom service assurance market. Furthermore, developing scalable, interoperable, and cost-competitive solutions will be essential for widespread adoption

Fixed Operator Telecom Service Assurance Market Scope

The market is segmented on the basis of solution, organization size, and deployment type.

- By Solution

On the basis of solution, the global fixed operator telecom service assurance market is segmented into Software and Services. The Software segment held the largest market revenue share in 2025, driven by the increasing need for real-time monitoring, fault detection, and predictive analytics to ensure uninterrupted network performance. Software solutions enable operators to proactively detect network anomalies, optimize bandwidth allocation, and reduce service disruptions. Advanced analytics and AI integration in software platforms are enhancing operational efficiency and customer experience. These solutions are widely adopted by telecom providers to meet stringent SLA requirements and maintain high-quality service delivery.

The Services segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising demand for managed service offerings, consulting, and support services. Services help operators implement and maintain service assurance frameworks without heavy in-house investments. Managed services provide continuous monitoring, troubleshooting, and optimization, allowing operators to focus on core business activities. The increasing complexity of telecom networks and the growing need for professional expertise are further fueling the adoption of service-based solutions. In addition, service contracts often offer flexible and scalable options tailored to operator requirements.

- By Organization Size

On the basis of organization size, the market is segmented into Large Enterprises and Small and Medium Enterprise (SMEs). Large Enterprises held the largest revenue share in 2025, owing to their extensive network infrastructure and higher investments in advanced service assurance solutions. These organizations typically operate complex, multi-layered networks requiring comprehensive monitoring, predictive maintenance, and automated fault management. Large operators prioritize investment in robust solutions to ensure minimal downtime and high customer satisfaction. They also benefit from economies of scale in deploying integrated software and services for network performance optimization.

The SME segment is projected to witness the fastest growth from 2026 to 2033, supported by the increasing adoption of scalable and cost-effective service assurance solutions. SMEs are leveraging cloud-based and managed services to monitor network performance efficiently without heavy capital expenditure. Smaller operators are increasingly adopting software-as-a-service (SaaS) models to quickly implement service assurance without extensive infrastructure. The flexibility and affordability of these solutions make them ideal for SMEs aiming to maintain service quality while optimizing operational costs. Growing awareness of SLA compliance and customer experience is further accelerating adoption in this segment.

- By Deployment Type

On the basis of deployment type, the market is segmented into On-Premises, Hosted, and Cloud. The On-Premises segment dominated the market in 2025, driven by the preference for in-house control, data security, and customization of service assurance operations. On-premises deployments allow operators to fully manage network data, integrate with existing IT systems, and maintain compliance with regulatory requirements. Organizations with sensitive data and legacy network systems often prefer this deployment type for greater reliability and security. In addition, on-premises solutions offer complete customization for operators to tailor service assurance processes to their specific network architecture.

The Cloud segment is projected to witness the fastest growth from 2026 to 2033, due to the flexibility, scalability, and reduced upfront costs offered by cloud-based deployments. Cloud service assurance allows operators to access advanced analytics, AI-driven insights, and remote monitoring capabilities from anywhere. It supports rapid deployment, easy integration with multiple network elements, and seamless updates without significant infrastructure investment. Cloud-based solutions are particularly attractive for operators expanding into new regions or managing distributed networks. The growing adoption of digital transformation initiatives and IoT integration in telecom networks is further accelerating the shift toward cloud deployments.

Fixed Operator Telecom Service Assurance Market Regional Analysis

- North America dominated the global fixed operator telecom service assurance market with the largest revenue share of 38.7% in 2025, driven by increasing investments in advanced network monitoring, fault management, and predictive analytics solutions

- Telecom operators in the region are focused on ensuring uninterrupted service delivery, optimizing network performance, and meeting stringent SLA requirements, which is driving the adoption of service assurance solutions

- The widespread adoption is further supported by high network penetration, the presence of major telecom operators, and growing demand for managed and cloud-based services, establishing service assurance as a critical component of telecom operations

U.S. Telecom Service Assurance Market Insight

The U.S. market captured the largest revenue share in 2025 within North America, fueled by the rapid deployment of 5G networks and the expansion of broadband infrastructure. Operators are increasingly prioritizing the adoption of AI-driven analytics, real-time monitoring, and automated fault detection to enhance service quality. The growing focus on customer experience, combined with the integration of cloud-based and software solutions, is further propelling the market. In addition, regulatory compliance and competitive pressures are accelerating investments in service assurance technologies.

Europe Telecom Service Assurance Market Insight

The Europe market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent regulatory standards, the increasing complexity of telecom networks, and rising demand for network reliability. Telecom operators are adopting advanced monitoring solutions to proactively detect and resolve faults. The region is witnessing rapid adoption of cloud and hosted solutions to reduce operational costs and improve service quality. Growing investments in smart city initiatives and next-generation network deployments are also fostering the uptake of service assurance solutions.

U.K. Telecom Service Assurance Market Insight

The U.K. market is expected to witness significant growth from 2026 to 2033, driven by the rollout of 5G networks and the increasing emphasis on customer experience. Telecom operators are deploying service assurance solutions to minimize downtime, improve fault resolution times, and optimize network performance. In addition, the U.K.’s strong IT infrastructure, digital adoption, and focus on managed and cloud services are boosting market expansion. The demand for scalable, flexible, and automated service assurance solutions is expected to remain high across both large enterprises and SMEs.

Germany Telecom Service Assurance Market Insight

The Germany market is projected to witness strong growth from 2026 to 2033, fueled by increasing investments in network modernization, digital transformation initiatives, and AI-driven analytics. Operators are focusing on predictive maintenance, fault detection, and automated monitoring to ensure high-quality service delivery. Germany’s advanced infrastructure, coupled with a technology-focused regulatory environment, supports the adoption of both software and managed service solutions. In addition, operators are integrating service assurance platforms with network management systems to achieve end-to-end operational efficiency.

Asia-Pacific Telecom Service Assurance Market Insight

The Asia-Pacific market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid telecom network expansion, increasing broadband penetration, and the adoption of next-generation technologies in countries such as China, India, and Japan. Operators are increasingly leveraging cloud-based, hosted, and managed service solutions to enhance network reliability and operational efficiency. Government initiatives promoting digital connectivity and smart city deployments are further boosting market adoption. The presence of both global and regional service assurance vendors is helping to improve solution availability and reduce deployment costs.

Japan Telecom Service Assurance Market Insight

The Japan market is expected to witness significant growth from 2026 to 2033, supported by the country’s advanced telecom infrastructure, high digital adoption, and demand for efficient network management. Operators are increasingly implementing cloud-based and AI-powered service assurance platforms to improve fault detection and network performance. The integration of service assurance solutions with existing network management systems is enhancing operational efficiency. Moreover, Japan’s focus on smart city development and high expectations for uninterrupted service quality are further driving market expansion.

China Telecom Service Assurance Market Insight

The China market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid telecom network expansion, high adoption of 5G technology, and government initiatives supporting digital infrastructure development. Telecom operators are investing in service assurance software and managed services to ensure service reliability and optimize network performance. The availability of cost-effective solutions, coupled with strong domestic vendors, is accelerating market growth. In addition, the country’s growing demand for enhanced customer experience and SLA compliance is propelling the adoption of advanced service assurance solutions.

Fixed Operator Telecom Service Assurance Market Share

The Fixed Operator Telecom Service Assurance industry is primarily led by well-established companies, including:

- Broadcom (U.S.)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Hewlett Packard Enterprise Development LP (U.S.)

- NEC Technologies India Private Limited (India)

- Nokia (Finland)

- Accenture (Ireland)

- Amdocs (U.S.)

- Comarch SA (Poland)

- Huawei Technologies Co., Ltd (China)

- IBM (U.S.)

- MYCOM OSI (U.K.)

- NETSCOUT (U.S.)

- Oracle (U.S.)

- Spirent Communications (U.K.)

- Tata Consultancy Services Limited (India)

- TEOCO Corporation (U.S.)

- VIAVI Solutions Inc. (U.S.)

- ZTE Corporation (China)

- Cisco Systems Inc. (U.S.)

- JDS Worldwide Corp (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.