Global Fluidized Catalytic Cracking Fcc Catalyst Market

Market Size in USD Billion

USD

3.00 Billion

USD

4.17 Billion

2024

2032

USD

3.00 Billion

USD

4.17 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.00 Billion | |

| USD 4.17 Billion | |

| % | |

|

What is the Global Fluidized Catalytic Cracking (FCC) Catalyst Market Size and Growth Rate?

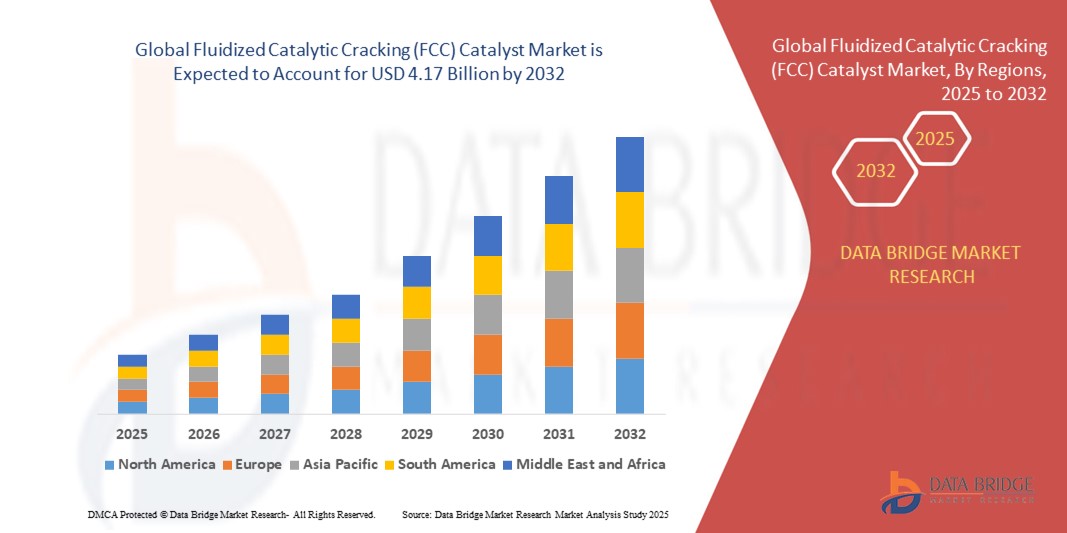

- The global fluidized catalytic cracking (FCC) catalyst market size was valued at USD 3.00 billion in 2024 and is expected to reach USD 4.17 billion by 2032, at a CAGR of 4.20% during the forecast period

- The fluidized catalytic cracking (FCC) catalyst market is a vital segment within the petroleum refining industry, driven by the increasing demand for cleaner-burning fuels and petrochemical feedstocks. Key factors such as rising energy consumption, stringent environmental regulations, and advancements in catalyst technology shape the dynamics of this market, with leading manufacturers continually innovating to improve catalyst performance and meet evolving industry needs

- The fluidized catalytic cracking catalyst market is characterized by intense competition, strategic collaborations, and investments in research and development to enhance process efficiency and product quality

What are the Major Takeaways of Fluidized Catalytic Cracking (FCC) Catalyst Market?

- This increasing demand for refined petroleum products is fuelled by rapid urbanization, industrialization, and transportation needs across the globe, particularly in emerging economies experiencing robust economic growth. As populations grow and living standards improve, there is a rising reliance on automobiles, aviation, and other forms of transportation, leading to heightened consumption of gasoline, diesel, jet fuel, and other refined petroleum products

- The developing petrochemical sector contributes to the increasing need for refined petroleum products, which are used to make plastics, chemicals, and other vital materials. This trend is further amplified by increasing disposable incomes and changing consumer preferences, driving demand for a wide range of petrochemical-derived products used in everyday life. As a result, refineries worldwide are under pressure to increase production capacities and optimize processes, creating a sustained demand for fluidized catalytic cracking catalysts to facilitate the efficient conversion of heavy hydrocarbons into valuable refined products

- Asia-Pacific dominated the fluidized catalytic cracking (FCC) catalyst market with the largest revenue share of 33.47% in 2024, driven by increasing industrialization, expanding petrochemical production, and high demand for light olefins

- North America fluidized catalytic cracking catalyst market is projected to grow at the fastest CAGR of 5.9% during 2025–2032, fueled by refinery modernization efforts and rising demand for cleaner transportation fuels

- The Zeolite-based Catalyst segment dominated the market with the largest revenue share of 45.6% in 2024, driven by its high activity, selectivity, and durability in refining operations

Report Scope and Fluidized Catalytic Cracking (FCC) Catalyst Market Segmentation

|

Attributes |

Fluidized Catalytic Cracking (FCC) Catalyst Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Fluidized Catalytic Cracking (FCC) Catalyst Market?

Advanced Process Efficiency and Environmental Optimization

- A significant trend in the global fluidized catalytic cracking (FCC) catalyst market is the shift toward catalysts engineered for enhanced process efficiency and lower environmental impact. Manufacturers are focusing on developing FCC catalysts that improve yield, reduce coke formation, and optimize sulfur removal, enabling refineries to meet stricter environmental regulations while maintaining high productivity

- For instance, Zeolyst International recently introduced a next-generation FCC catalyst designed to maximize middle distillates and minimize coke formation, supporting cleaner operations and higher throughput. Similarly, Topsoe A/S has developed catalysts targeting ultra-low sulfur gasoline production, aligning with global emissions standards

- FCC catalysts are increasingly optimized to handle diverse feedstocks, including heavy residues and high-sulfur crude oils, offering flexibility and operational efficiency. Advanced formulations improve selectivity toward desired products, reducing waste and enhancing refinery margins

- Integration of digital process monitoring and predictive analytics with FCC catalyst operations enables refiners to adjust reaction conditions in real-time, maximizing performance while minimizing energy consumption

- Companies such as BASF SE and Honeywell UOP are focusing on environmentally friendly FCC catalysts that combine high activity, selectivity, and durability, supporting compliance with evolving global regulations

- The growing emphasis on sustainability and process optimization is driving demand for FCC catalysts that balance operational efficiency with environmental performance across global refining operations

What are the Key Drivers of Fluidized Catalytic Cracking (FCC) Catalyst Market?

- The rising global demand for cleaner fuels, combined with stricter environmental regulations, is a major driver of FCC catalyst adoption. Refineries are actively seeking catalysts that enhance conversion efficiency while reducing sulfur and nitrogen emissions

- For example, in March 2024, Shell reported upgrading its FCC units with high-performance catalysts to comply with ultra-low sulfur fuel standards, illustrating how regulatory pressures stimulate market growth

- Increasing complexity in crude oil slates and the need for refining heavier, high-sulfur feedstocks also fuel the adoption of advanced FCC catalysts, as they offer higher selectivity, reduced coke formation, and improved product yield

- The growing demand for transportation fuels, petrochemicals, and specialty products such as propylene and diesel encourages refiners to deploy FCC catalysts optimized for maximum light olefins or middle distillates production

- Operational cost savings, process flexibility, and the ability to retrofit existing FCC units with modern catalysts provide additional incentives for refiners, particularly in regions experiencing rapid industrial and infrastructure growth

Which Factor is Challenging the Growth of the Fluidized Catalytic Cracking (FCC) Catalyst Market?

- High operational and replacement costs of advanced FCC catalysts can limit adoption, particularly in price-sensitive regions or for smaller refineries. Premium catalysts with specialized formulations often require higher capital investment and periodic replacement, impacting operational budgets

- Variability in feedstock quality and the need for continuous monitoring to prevent catalyst deactivation pose technical challenges, requiring skilled personnel and precise process management

- Environmental compliance requirements demand that catalysts deliver high efficiency but also maintain low emissions, creating pressure on manufacturers to innovate continuously

- In addition, geopolitical factors, such as fluctuating crude oil prices and supply chain disruptions, can affect catalyst availability and cost, potentially delaying installations or upgrades

- Addressing these challenges requires developing more cost-effective, durable, and feedstock-flexible FCC catalysts, alongside advanced monitoring systems to optimize performance and ensure compliance with environmental standards

How is the Fluidized Catalytic Cracking (FCC) Catalyst Market Segmented?

The market is segmented on the basis of catalyst type, process, application, and end-users.

- By Catalyst Type

On the basis of catalyst type, the Fluidized Catalytic Cracking (FCC) Catalyst market is segmented into Zeolite-based Catalyst, Metal-based Catalyst, and Additive-based Catalyst. The Zeolite-based Catalyst segment dominated the market with the largest revenue share of 45.6% in 2024, driven by its high activity, selectivity, and durability in refining operations. Zeolite-based catalysts are highly effective in maximizing the yield of light olefins and middle distillates while minimizing coke formation, making them ideal for processing complex feedstocks.

The Additive-based Catalyst segment is expected to witness the fastest growth from 2025 to 2032, fueled by refiners’ need for customized solutions to optimize specific product yields, improve sulfur handling, and extend catalyst life. The ability of additive-based catalysts to target specific operational challenges ensures their growing adoption across refineries globally.

- By Process

On the basis of process, the market is segmented into Gasoline Sulfur Reduction, Maximum Light Olefins, Maximum Middle Distillates, Maximum Bottoms Conversion, Low Coke Production, and Others. The Maximum Middle Distillates segment accounted for the largest revenue share of 42.3% in 2024, driven by the global demand for diesel, jet fuel, and kerosene.

The Maximum Light Olefins segment is expected to witness the fastest CAGR from 2025 to 2032, supported by the rising demand for petrochemical feedstocks such as ethylene and propylene. FCC catalysts optimized for light olefins enable refiners to enhance yield while maintaining operational efficiency, making them increasingly important for regions emphasizing petrochemical production.

- By Application

On the basis of application, the fluidized catalytic cracking (FCC) catalyst market is segmented into Vacuum Gas Oil (VGO), Residue, and Others. The Vacuum Gas Oil (VGO) segment accounted for the largest market revenue share of 47.1% in 2024, driven by its widespread use as FCC feedstock for producing diesel, gasoline, and LPG. Increasing refinery modernization and the need for efficient conversion of heavy fractions into high-value products are also encouraging adoption.

The Residue segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the growing processing of heavy and ultra-heavy crude oils. Residue-oriented FCC catalysts are engineered to handle high sulfur and metal content, supporting efficient refining operations and meeting the rising demand for heavy crude conversion in emerging markets.

- By End-Users

On the basis of end-users, the fluidized catalytic cracking (FCC) catalyst market is segmented into Refineries, Petrochemicals, and Others. The Refineries segment accounted for the largest market revenue share of 54.2% in 2024, as FCC catalysts are essential for converting heavy fractions into lighter, high-value products efficiently. The Petrochemicals segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing demand for light olefins as feedstock for polymers, plastics, and other chemical products. Expanding petrochemical production capacities and integration of FCC catalysts into chemical operations are supporting faster adoption in this segment globally.

Which Region Holds the Largest Share of the Fluidized Catalytic Cracking (FCC) Catalyst Maret?

- Asia-Pacific dominated the fluidized catalytic cracking (FCC) catalyst market with the largest revenue share of 33.47% in 2024, driven by increasing industrialization, expanding petrochemical production, and high demand for light olefins

- Major economies such as China, Japan, and India are leading the adoption of FCC catalysts due to growing refinery capacities, modernization of processing units, and rising consumption of petroleum products

- The widespread adoption is further supported by government initiatives promoting industrial growth, technological advancements in refining processes, and the emergence of APAC as a manufacturing hub for catalyst systems, establishing FCC catalysts as a critical component in both refinery and petrochemical operations

China Fluidized Catalytic Cracking (FCC) Catalyst Market Insight

China fluidized catalytic cracking catalyst market captured the largest revenue share in Asia-Pacific in 2024, owing to its vast refining industry, continuous capacity expansions, and emphasis on maximizing gasoline yields. The presence of domestic catalyst producers, coupled with government initiatives to enhance energy self-sufficiency, further fuels adoption. China’s role as both a key consumer and manufacturer strengthens its leadership position in the regional FCC catalyst landscape.

India Fluidized Catalytic Cracking (FCC) Catalyst Market Insight

India fluidized catalytic cracking catalyst market is expected to grow at a substantial CAGR during the forecast period, supported by surging fuel demand and capacity expansions in state-owned refineries such as IOC, BPCL, and HPCL. India’s economic growth, coupled with urbanization and rising vehicle ownership, is driving fluidized catalytic cracking unit utilization. Ongoing investments in upgrading refinery processes to produce cleaner fuels also stimulate catalyst demand.

Japan Fluidized Catalytic Cracking (FCC) Catalyst Market Insight

Japan fluidized catalytic cracking catalyst market is gaining traction as the country focuses on improving refining efficiency and meeting strict fuel quality standards. While overall refining capacity is stable, refiners are adopting advanced fluidized catalytic cracking catalysts to maximize value from existing assets. Japan’s commitment to sustainability and energy efficiency is also encouraging the shift toward eco-friendly and high-performance catalyst solutions.

Which Region is the Fastest Growing Region in the Fluidized Catalytic Cracking (FCC) Catalyst Market?

North America fluidized catalytic cracking catalyst market is projected to grow at the fastest CAGR of 5.9% during 2025–2032, fueled by refinery modernization efforts and rising demand for cleaner transportation fuels. U.S. refiners are increasingly investing in advanced fluidized catalytic cracking catalyst technologies to enhance operational efficiency, reduce emissions, and adapt to changing fuel specifications. Growth is also supported by technological innovation, strong R&D capabilities, and the presence of leading catalyst manufacturers in the region.

U.S. Fluidized Catalytic Cracking (FCC) Catalyst Market Insight

U.S. fluidized catalytic cracking catalyst market accounted for the largest share in North America in 2024, driven by one of the world’s most advanced refining infrastructures. Rising gasoline consumption, combined with refinery upgrades to process shale oil, is boosting FCC catalyst demand. Moreover, the emphasis on producing low-sulfur fuels and higher-value petrochemicals enhances adoption of next-generation catalyst solutions.

Canada Fluidized Catalytic Cracking (FCC) Catalyst Market Insight

Canada fluidized catalytic cracking catalyst market is expected to witness steady growth, supported by expanding refining operations and the country’s focus on energy security. Canadian refiners are increasingly adopting fluidized catalytic cracking catalysts to enhance processing flexibility and maximize product output, particularly in light of fluctuating crude quality and environmental compliance requirements.

Which are the Top Companies in Fluidized Catalytic Cracking (FCC) Catalyst Market?

The fluidized catalytic cracking (FCC) catalyst industry is primarily led by well-established companies, including:

- Albemarle Corporation (U.S.)

- BASF SE (Germany)

- CLARIANT (Switzerland)

- Chevron Corporation (U.S.)

- Exxon Mobil Corporation (U.S.)

- W. R. Grace & Co.-Conn (U.S.)

- Honeywell International Inc. (U.S.)

- Johnson Matthey (U.K.)

- KBR Inc. (U.S.)

- LyondellBasell Industries Holdings B.V. (U.S.)

- China Petroleum & Chemical Corporation (China)

- Axens (France)

- DORF KETAL CHEMICALS INDIA PRIVATE LIMITED (India)

- Topsoe A/S (Denmark)

- Shell (Netherlands)

- SABIC (Saudi Arabia)

- WISON (China)

- Zeolyst International (U.S.)

- JGC HOLDINGS CORPORATION (Japan)

- Rezel Catalysts Corporation (China)

- Antenchem (China)

- SINOCATA (China)

What are the Recent Developments in Global Fluidized Catalytic Cracking (FCC) Catalyst Market ?

- In October 2023, W. R. Grace & Co.-Conn introduced its latest breakthrough in catalyst technology with the launch of the PARAGON FCC catalyst, aimed at helping refiners produce transportation fuels while reducing their carbon footprint. The catalyst features a novel rare earth-based Vanadium (V) trap integrated into high matrix surface area solutions for FCC units, enabling refiners to expand operational flexibility and process a wider range of feedstocks for improved profitability. This innovation underscores the company’s commitment to enhancing refinery efficiency and sustainability

- In June 2022, BASF announced its plan to provide a range of chemical intermediates with a product carbon footprint significantly lower than the global market average. This initiative is designed to meet growing sustainability demands while offering environmentally responsible solutions across industries. The move highlights BASF’s focus on aligning product development with global decarbonization efforts

- In June 2022, Albemarle Corporation (NYSE, ALB) completed an investment exceeding US$ 500 million to establish the La Negra III/IV chemical conversion plant, now recognized as one of the most advanced facilities in Latin America. The plant incorporates the region’s first thermal evaporator, significantly reducing freshwater use per metric ton and reflecting Albemarle’s dedication to sustainable operations. This development strengthens the company’s position as a leader in sustainable chemical production

- In March 2022, BASF SE launched Fourtitude, a new FCC catalyst engineered to maximize butylenes from resid feedstocks. Built on the company’s award-winning multiple framework topology (MFT) technology, Fourtitude is optimized to deliver superior selectivity for butylenes while maintaining strong catalyst activity. The launch reinforces BASF’s leadership in delivering innovative FCC catalyst solutions for the refining industry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Fluidized Catalytic Cracking Fcc Catalyst Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Fluidized Catalytic Cracking Fcc Catalyst Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Fluidized Catalytic Cracking Fcc Catalyst Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.