Global Ganglion Cysts Treatment Market

Market Size in USD Billion

USD

1.70 Billion

USD

2.92 Billion

2024

2032

USD

1.70 Billion

USD

2.92 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.70 Billion | |

| USD 2.92 Billion | |

| % | |

|

Ganglion Cysts Treatment Market Size

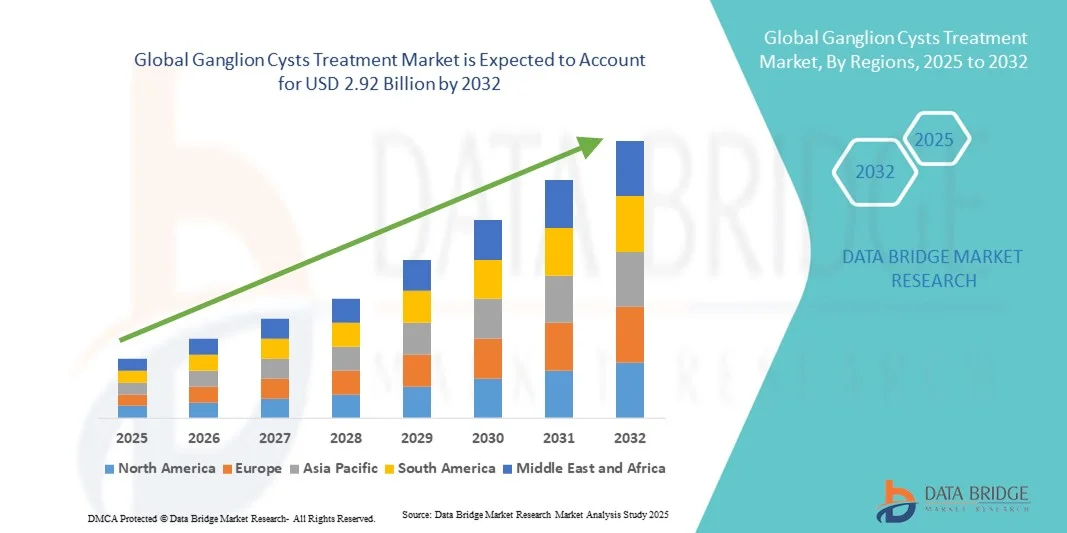

- The global ganglion cysts treatment market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 2.92 billion by 2032, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of musculoskeletal disorders and rising awareness regarding early diagnosis and management of ganglion cysts. Advancements in minimally invasive surgical procedures, imaging technologies, and pharmacological interventions are further supporting the expansion of the ganglion cysts treatment market globally

- Furthermore, the growing geriatric population, coupled with the rising number of sports-related injuries and enhanced access to orthopedic and specialized healthcare centers, is driving the adoption of effective ganglion cysts treatment solutions. These converging factors are accelerating the uptake of surgical and non-surgical treatment options, thereby significantly boosting the industry’s growth

Ganglion Cysts Treatment Market Analysis

- Ganglion Cysts Treatment, including surgical excision, aspiration, and conservative management, is increasingly recognized as a critical solution for managing benign soft tissue cysts and improving patient quality of life. The rising prevalence of ganglion cysts and advancements in minimally invasive treatment approaches are driving market expansion globally

- The market growth is primarily fueled by increasing awareness among healthcare providers and patients regarding early diagnosis and effective management of ganglion cysts. In addition, improved accessibility to orthopedic clinics and specialized surgical centers is accelerating the adoption of treatment solutions

- North America dominated the ganglion cysts treatment market with the largest revenue share of 41.3% in 2024, supported by advanced healthcare infrastructure, high incidence of musculoskeletal disorders, and strong adoption of minimally invasive surgical procedures in the U.S.

- Asia-Pacific is expected to be the fastest-growing region in the ganglion cysts treatment market during the forecast period, driven by increasing healthcare awareness, rising disposable incomes, and expanding access to orthopedic and specialized treatment centers in countries such as China and India

- The painful segment dominated the largest market revenue share of 55.3% in 2024, driven by the discomfort, restricted mobility, and urgency of seeking treatment associated with pain

Report Scope and Ganglion Cysts Treatment Market Segmentation

|

Attributes |

Ganglion Cysts Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ganglion Cysts Treatment Market Trends

Increasing Adoption of Minimally Invasive and Outpatient Procedures

- A notable trend in the global ganglion cysts treatment market is the increasing adoption of minimally invasive procedures, such as arthroscopic excision and aspiration techniques, which offer quicker recovery and reduced complications compared to traditional open surgery

- For instance, in March 2023, a leading hospital in Germany introduced an outpatient arthroscopic excision program for wrist ganglion cysts, enabling patients to return home the same day and resume normal activities within a week. This approach is gaining popularity in both urban and semi-urban healthcare settings

- Another trend is the rising integration of imaging guidance, such as ultrasound, during aspiration or surgical procedures, which improves precision, reduces recurrence, and enhances patient outcomes

- Clinicians are also increasingly combining conservative management with post-procedure physiotherapy to improve joint mobility and reduce the risk of recurrence

- The trend towards outpatient and minimally invasive treatments is driven by patient preference for less invasive options, shorter hospital stays, and reduced overall treatment costs

- Healthcare providers are investing in training and advanced equipment to meet this demand, resulting in broader adoption of these innovative procedures across hospitals and specialized clinics globally

Ganglion Cysts Treatment Market Dynamics

Driver

Growing Need Due to Rising Prevalence and Awareness of Ganglion Cysts

- The increasing prevalence of ganglion cysts among adults and the growing awareness regarding early diagnosis and treatment options is a significant driver for the heightened demand in the market

- For instance, in April 2024, leading healthcare providers launched awareness campaigns and advanced diagnostic initiatives to improve early detection and management of ganglion cysts. Such strategies by key companies are expected to drive the Ganglion Cysts Treatment industry growth in the forecast period

- As patients and clinicians become more aware of the complications associated with untreated cysts, including discomfort, reduced mobility, and potential nerve compression, demand for effective treatments such as aspiration, corticosteroid injections, and surgical interventions is increasing

- Furthermore, the growing availability of minimally invasive and outpatient procedures is making treatment more accessible and convenient for patients, improving adoption across both urban and semi-urban regions

- The convenience of non-surgical options, rapid recovery, and improved outcomes through advanced surgical techniques are key factors propelling the adoption of ganglion cyst treatments in both hospitals and specialized clinics. The trend towards early intervention and increasing patient awareness of treatment options further contribute to market growth

Restraint/Challenge

Concerns Regarding Treatment Costs and Recurrence Rates

- Concerns surrounding the high cost of certain ganglion cyst treatments, particularly surgical interventions, pose a significant challenge to broader market adoption. Patients in developing regions or those with budget constraints may opt for conservative management rather than advanced procedures

- For instance, recurring cases of ganglion cysts after initial treatment have made some patients hesitant to undergo surgical intervention, affecting overall treatment uptake

- Addressing these challenges through cost-effective treatment solutions, insurance coverage, and patient education about the benefits and risks of various interventions is crucial for building consumer trust. Hospitals and clinics emphasize their experienced medical teams and successful treatment outcomes to reassure patients. In addition, the relatively high cost of advanced surgical treatments compared to conservative management can be a barrier to adoption, particularly in regions with limited healthcare infrastructure. While basic aspiration techniques have become more widely available and affordable, premium interventions such as arthroscopic excision or specialized post-operative therapy often come with higher costs

- While treatment accessibility is gradually improving, patient concerns about recurrence and long-term outcomes can still hinder adoption, especially for those who do not perceive immediate symptoms or functional limitations

- Overcoming these challenges through improved clinical training, development of affordable treatment options, and enhanced patient education on post-treatment care and recurrence prevention will be vital for sustained market growth

Ganglion Cysts Treatment Market Scope

The market is segmented on the basis of type, diagnosis, treatment, body area, severity, gender, end-users, and distribution channel.

- By Type

On the basis of type, the Ganglion Cysts Treatment market is segmented into painful and non-painful cysts. The painful segment dominated the largest market revenue share of 55.3% in 2024, driven by the discomfort, restricted mobility, and urgency of seeking treatment associated with pain. Patients with painful cysts are more likely to consult physicians, undergo imaging, and choose active treatments, including surgical and non-surgical interventions. Hospitals and specialty clinics focus on these cases for better outcomes. Increasing awareness campaigns and targeted therapies contribute to higher adoption. Rising geriatric and working-age populations experiencing wrist and hand discomfort also drive demand. Painful cysts often affect daily activities, encouraging faster treatment. The segment benefits from insurance coverage and reimbursement policies in developed regions. In addition, urban hospitals report higher consultation rates for symptomatic patients, reinforcing revenue growth. The demand is supported by clinical preference for early intervention and patient desire for functional improvement.

The non-painful segment is expected to witness the fastest CAGR of 12.8% from 2025 to 2032, fueled by increasing awareness and routine screening programs. Patients with asymptomatic cysts now undergo diagnosis for preventive care and cosmetic concerns. Adoption is rising in outpatient centers and specialty clinics. Early intervention reduces the risk of progression to painful conditions, encouraging elective treatment. Non-painful cases are often discovered during imaging for unrelated issues, supporting growth. Patient education and teleconsultations are expanding awareness. The availability of minimally invasive procedures attracts cautious patients. Rising disposable incomes in emerging economies facilitate elective treatments. Healthcare providers are emphasizing non-surgical management where feasible. Growth is also driven by advancements in conservative therapies and physiotherapy. Insurance coverage for elective care is gradually increasing, supporting uptake.

- By Diagnosis

On the basis of diagnosis, the market is segmented into MRI, X-Rays, Ultrasound, and others. The ultrasound segment dominated the largest market revenue share of 46.7% in 2024, owing to cost-effectiveness, real-time imaging, and non-invasiveness. It is widely used for initial assessment and post-treatment monitoring. Outpatient centers and hospitals prefer ultrasound due to portability and speed. It provides accurate cyst size, location, and fluid content analysis. Ultrasound supports guided aspiration and follow-up care. The technique reduces unnecessary surgical interventions. Healthcare professionals recommend ultrasound as a first-line diagnostic tool. Availability in urban and semi-urban clinics reinforces adoption. Ultrasound reduces patient discomfort during repeated checks. It also supports monitoring of recurrent cysts effectively. Training programs for sonographers increase diagnostic reliability. Clinical guidelines highlight ultrasound as the preferred method, maintaining market dominance.

The MRI segment is expected to witness the fastest CAGR of 13.2% from 2025 to 2032, driven by detailed soft tissue visualization. MRI is preferred for complex or deep cysts, recurrent cases, and preoperative planning. High accuracy ensures minimal complications during surgery. Advanced imaging centers and hospitals are expanding MRI availability. Rising clinician awareness of MRI advantages supports adoption. MRI is critical for differential diagnosis when symptoms mimic other conditions. Integration with 3D planning improves surgical precision. Growth is supported by increasing hospital investments in advanced imaging. Patient preference for non-invasive, accurate diagnostics fuels the segment. Insurance coverage for MRI in complex cases is increasing. MRI adoption is higher in developed countries with advanced healthcare infrastructure. Technological innovations, such as faster MRI sequences, enhance patient throughput, driving growth.

- By Treatment

On the basis of treatment, the market is segmented into surgical, non-surgical, and others. The surgical segment dominated the largest market revenue share of 51.5% in 2024, owing to high success rates and permanent cyst removal. Hospitals and specialized clinics provide arthroscopic and open excision options. Surgical treatments ensure functional restoration and lower recurrence rates. Urban and tertiary hospitals drive revenue due to availability of skilled surgeons. Patient preference for long-term outcomes supports surgical adoption. Minimally invasive surgery reduces hospital stay and recovery time. Post-operative physiotherapy improves functional outcomes. Insurance reimbursement for surgery in developed countries facilitates uptake. Increasing prevalence of recurrent cysts maintains demand. Surgeons prefer standardized protocols, ensuring consistent results. Clinical awareness campaigns encourage timely surgical intervention. Population aging and increased wrist/hand usage in daily life further drive adoption.

The non-surgical segment is expected to witness the fastest CAGR of 12.5% from 2025 to 2032, driven by patient preference for conservative management. Techniques include aspiration, corticosteroid injection, and physiotherapy. Outpatient and clinic-based treatment supports rapid adoption. Reduced recovery time and minimal invasiveness attract patients. Awareness campaigns promote non-surgical alternatives. Teleconsultations facilitate early intervention and follow-up care. Rising adoption in emerging regions supports growth. Non-surgical procedures are cost-effective compared to surgery. Patient compliance improves with home-based physiotherapy. Insurance coverage for non-surgical options is expanding. Cosmetic concerns drive uptake among younger patients. Increasing availability of trained clinicians enhances treatment accessibility. Non-surgical interventions are preferred in mild to moderate cases, sustaining growth.

- By Body Area

On the basis of body area, the market is segmented into hands, wrist, foot, knee, and others. The wrist segment dominated the largest market revenue share of 47.8% in 2024, due to high incidence of ganglion cysts in the wrist and its functional importance. Wrist cysts affect daily tasks and occupational activities, encouraging treatment. Clinics and hospitals prioritize wrist cases for both surgical and non-surgical management. Imaging diagnostics are widely used for wrist cysts. Recurrent wrist cysts are common, sustaining repeat treatment demand. Patient education emphasizes early treatment for wrist functionality. Urban populations report higher incidence due to desk jobs. Clinical research supports wrist-focused protocols. Wrist cyst management ensures functional restoration and low recurrence. Skilled surgeons and physiotherapists enhance outcomes. Insurance coverage facilitates access. Awareness campaigns promote early detection, maintaining dominance.

The hand segment is expected to witness the fastest CAGR of 13.0% from 2025 to 2032, driven by cosmetic concerns and functional importance. Early detection in hand cysts is rising due to routine check-ups. Outpatient interventions support convenience and rapid recovery. Non-invasive and minimally invasive treatments encourage adoption. Patient education on hand mobility and dexterity promotes early treatment. Clinics are expanding hand-specific treatment offerings. Telemedicine consultations improve follow-up compliance. Growth is supported by increasing awareness campaigns. Insurance coverage for hand treatment procedures is rising. Cosmetic outcomes attract younger patient groups. Workplace ergonomics awareness promotes treatment. Recurrent cysts in hand regions sustain demand. Minimally invasive procedures reduce downtime, driving adoption.

- By Severity

On the basis of severity, the market is segmented into mild, moderate, and severe. The moderate segment dominated the largest market revenue share of 49.2% in 2024, as moderate cysts often impair function and necessitate medical attention. Treatment typically involves a combination of imaging, non-surgical management, and selective surgery. Clinics and hospitals prioritize moderate cases for functional restoration. Moderate severity ensures higher patient engagement and follow-up. Recurrent cysts contribute to repeated treatment demand. Awareness campaigns encourage intervention before progression to severe conditions. Insurance coverage for moderate treatment is widely available. Outpatient procedures are preferred for moderate cases. Physiotherapy complements treatment to enhance mobility. Moderate cysts are commonly observed in the wrist and hand. Urban and semi-urban clinics report high case numbers, supporting revenue growth. Population aging maintains moderate severity prevalence.

The severe segment is expected to witness the fastest CAGR of 12.7% from 2025 to 2032, fueled by increasing awareness and need for surgical intervention. Severe cysts are associated with pain, functional limitation, or recurrence. Surgical treatment is preferred for permanent resolution. Outpatient monitoring ensures proper post-procedure care. Specialized clinics are expanding severe cyst management programs. Insurance reimbursement supports adoption in developed countries. Patient education highlights urgency of treatment. Minimally invasive surgery reduces hospital stay. Rehabilitation protocols improve recovery. Growth is supported by urban healthcare infrastructure expansion. Advanced diagnostics improve detection of severe cases. Awareness campaigns emphasize timely treatment, sustaining demand. Clinical research reinforces best practices for severe cyst management.

- By Gender

On the basis of gender, the market is segmented into male and female. The female segment dominated the largest market revenue share of 54.1% in 2024, reflecting a higher incidence of ganglion cysts among women, especially in the wrist and hand. Female patients are more likely to seek medical attention for both functional and cosmetic reasons. Clinics report higher consultation rates among women. Imaging and treatment adoption is higher in females. Urban population trends support female dominance in revenue. Cosmetic outcomes drive elective treatment in women. Awareness programs emphasize early detection. Insurance coverage encourages intervention. Female-centric outpatient programs enhance access. Telemedicine facilitates follow-ups for working women. Recurrent cysts in females maintain treatment demand. Hospital and specialty clinics prioritize female patients. Functional restoration and low recurrence rates sustain market growth.

The male segment is expected to witness the fastest CAGR of 11.9% from 2025 to 2032, fueled by rising awareness and adoption of both surgical and non-surgical treatments. Men are increasingly seeking treatment due to functional impairment and occupational needs. Early intervention programs attract male patients. Clinics are offering tailored male-focused care. Outpatient and minimally invasive procedures support rapid recovery. Insurance coverage in male patient populations is increasing. Growth is supported by rising geriatric male populations. Awareness campaigns target male-specific risks. Teleconsultations facilitate compliance. Cosmetic concerns are becoming relevant among men. Advanced diagnostics improve detection in male patients. Urban and semi-urban adoption supports rapid expansion. Male segment growth is expected to continue robustly.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, home healthcare, and others. The hospitals segment dominated the largest market revenue share of 58.5% in 2024, owing to availability of surgical infrastructure, specialized staff, and advanced diagnostic facilities. Hospitals cater to both mild and severe cases and provide integrated post-operative care. Urban hospitals report higher patient inflow. Insurance reimbursement and government support enhance hospital adoption. Hospitals lead in minimally invasive and advanced surgical procedures. Outpatient and follow-up care is streamlined. Clinical protocols support consistent treatment outcomes. Awareness campaigns encourage hospital consultations. Recurrent cysts are managed efficiently. Hospitals ensure functional restoration and low recurrence rates. Patient preference for trusted institutions supports dominance. Advanced infrastructure maintains revenue share.

The specialty clinics segment is expected to witness the fastest CAGR of 13.5% from 2025 to 2032, driven by rising outpatient care, minimally invasive procedures, and patient preference for convenient services. Clinics offer focused treatment for wrist and hand cysts. Non-surgical options, physiotherapy, and cosmetic interventions support growth. Urban and semi-urban adoption is rising. Awareness campaigns increase clinic visits. Telemedicine integration enhances follow-up. Outpatient care reduces hospital burden. Early detection and elective procedures drive growth. Insurance coverage for clinic-based treatment is improving. Functional and cosmetic outcomes attract younger patients. Specialized staff and modern equipment enhance service quality. Clinic expansion in emerging regions contributes to rapid adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the largest market revenue share of 52.4% in 2024, due to direct availability of treatment post-consultation and reliable supply chains. Hospital pharmacies ensure immediate access to medications and support inpatient care. Urban hospitals contribute to high revenue share. Insurance coverage supports hospital pharmacy adoption. Availability of combination therapies enhances market capture. Hospitals manage severe and recurrent cases efficiently. Clinical monitoring ensures proper drug use. Training and awareness improve patient adherence. Integrated care models support revenue. Hospital pharmacy distribution maintains high trust and credibility. Post-surgical care and prescription fulfillment reinforce dominance. Hospital infrastructure expansion sustains revenue

The online pharmacy segment is expected to witness the fastest CAGR of 14.1% from 2025 to 2032, driven by convenience, telemedicine adoption, and increasing e-commerce penetration. Patients prefer home delivery for non-urgent medications. Urban and semi-urban internet penetration supports growth. Rising awareness and digital literacy encourage adoption. Online pharmacies provide access to rare or specialty drugs. Subscription and delivery models improve adherence. Teleconsultation integration enhances user experience. Cost-effectiveness attracts price-sensitive patients. Pandemic-driven adoption supports continued growth. Insurance partnerships facilitate reimbursements. Emerging regions are increasingly relying on online access. Rapid logistics and tracking improve service reliability. Expansion of online pharmacy platforms sustains market momentum

Ganglion Cysts Treatment Market Regional Analysis

- North America dominated the ganglion cysts treatment market with the largest revenue share of 41.3% in 2024, supported by advanced healthcare infrastructure, high incidence of musculoskeletal disorders, and strong adoption of minimally invasive surgical procedures in the U.S. The region benefits from well-established hospitals and specialty clinics offering advanced diagnostic and treatment options

- Increasing patient awareness regarding functional and cosmetic outcomes drives adoption. High healthcare spending and insurance coverage enhance accessibility of treatments. Urban populations with sedentary lifestyles contribute to higher prevalence, encouraging early intervention. Growing preference for outpatient and ambulatory care centers supports market expansion

- Technologically advanced imaging modalities, such as MRI and ultrasound, further strengthen diagnosis and treatment rates. Clinical awareness campaigns and professional training programs boost patient inflow. Rising geriatric populations and working-age adults with repetitive strain injuries reinforce demand. Strong government support and favorable reimbursement policies also contribute to market growth

U.S. Ganglion Cysts Treatment Market Insight

The U.S. ganglion cysts treatment market captured the largest revenue share of 82% in 2024 within North America, fueled by the rising prevalence of wrist and hand cysts, growing geriatric population, and increasing demand for minimally invasive surgical procedures. Patients increasingly seek treatment for functional restoration and cosmetic reasons. The availability of advanced imaging and treatment technologies, along with experienced orthopedic surgeons, enhances treatment outcomes. Outpatient and day-care procedures are expanding adoption. Telemedicine and follow-up care improve patient compliance. Urban and suburban regions report higher case numbers due to lifestyle and occupational factors. Insurance coverage and supportive reimbursement policies further facilitate market growth. Awareness campaigns and patient education initiatives are driving early intervention. Government initiatives promoting musculoskeletal health contribute to expansion. Rising incidence of recurrent cysts increases repeat procedures. Elective treatment for cosmetic and functional concerns is on the rise. Hospital infrastructure and advanced orthopedic centers continue to support market dominance.

Europe Ganglion Cysts Treatment Market Insight

The Europe ganglion cysts treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing awareness of musculoskeletal health, technological advancements in minimally invasive procedures, and well-developed healthcare systems. Stringent regulations and professional guidelines encourage early diagnosis and treatment. Urbanization and rising disposable incomes support treatment affordability. Hospitals and specialty clinics are expanding services, providing comprehensive care for both surgical and non-surgical interventions. Patient preference for outpatient and day-care procedures is growing. Clinical awareness campaigns emphasize functional recovery and cosmetic outcomes. Government reimbursement policies facilitate access to advanced treatments. Emerging minimally invasive techniques reduce recovery time and improve patient satisfaction. The demand spans both primary and recurrent cases. The growing focus on preventive care encourages early intervention. Healthcare infrastructure improvements support consistent treatment delivery. Increasing prevalence of musculoskeletal disorders contributes to steady market expansion.

U.K. Ganglion Cysts Treatment Market Insight

The U.K. ganglion cysts treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising awareness of wrist and hand disorders, adoption of minimally invasive surgeries, and patient preference for outpatient care. High-quality healthcare infrastructure supports advanced imaging and treatment options. Evolving lifestyle patterns, including desk-based work and repetitive strain injuries, contribute to prevalence. Patients increasingly seek early intervention for functional and cosmetic benefits. Government initiatives and insurance coverage promote affordability. Specialty clinics and hospitals are expanding service offerings. Telemedicine and home-based rehabilitation enhance patient compliance. Urban centers report higher procedure volumes due to lifestyle-related disorders. Public health campaigns increase awareness of musculoskeletal conditions. Adoption of arthroscopic and minimally invasive procedures reduces recovery time. Growing interest in non-invasive and conservative management complements surgical approaches. The trend toward integrated treatment pathways drives overall market growth.

Germany Ganglion Cysts Treatment Market Insight

The Germany ganglion cysts treatment market is expected to expand at a considerable CAGR during the forecast period, driven by high prevalence of musculoskeletal disorders, advanced healthcare infrastructure, and focus on minimally invasive orthopedic procedures. Hospitals and specialty clinics are equipped with state-of-the-art imaging and surgical technologies. Patient awareness regarding functional and cosmetic outcomes is increasing. Outpatient and day-care treatments are preferred for efficiency and comfort. Insurance coverage and reimbursement policies enhance accessibility. Urbanization and sedentary lifestyles contribute to rising case numbers. National guidelines support early diagnosis and standardized treatment protocols. Specialty orthopedic centers manage both primary and recurrent cases effectively. Rehabilitation programs post-surgery improve patient outcomes. Research and clinical studies support adoption of minimally invasive techniques. Technological advancements in surgical procedures reduce complications. Awareness campaigns promote early intervention. The growing aging population ensures sustained demand for treatments.

Asia-Pacific Ganglion Cysts Treatment Market Insight

The Asia-Pacific ganglion cysts treatment market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare awareness, rising disposable incomes, and expanding access to orthopedic and specialized treatment centers in countries such as China and India. Government initiatives promoting musculoskeletal health are boosting early diagnosis and treatment. Urbanization and industrialization increase the prevalence of repetitive strain injuries. Private and public healthcare facilities are expanding service offerings for minimally invasive procedures. Rising patient awareness about functional and cosmetic outcomes encourages treatment. Outpatient care and day-care procedures are increasingly preferred. Investments in healthcare infrastructure improve treatment availability. Training of orthopedic surgeons enhances quality of care. Telemedicine and digital platforms facilitate follow-up and rehabilitation. Emerging economies are witnessing growing affordability and accessibility. Adoption of advanced imaging modalities supports precise diagnosis. Cosmetic concerns and occupational requirements drive elective procedures. The overall healthcare expansion in APAC supports robust market growth.

Japan Ganglion Cysts Treatment Market Insight

The Japan ganglion cysts treatment market is gaining momentum due to increasing geriatric population, high prevalence of musculoskeletal disorders, and strong healthcare infrastructure. Advanced imaging and minimally invasive treatment options are widely available. Patients seek treatment for functional restoration and cosmetic improvement. Outpatient care and day-care procedures are preferred. Government initiatives promote musculoskeletal health awareness. Insurance coverage supports affordability and access. Telemedicine enhances follow-up care and patient compliance. Urban populations show higher prevalence due to desk-based work. Hospitals and specialty clinics offer comprehensive management. Early intervention programs reduce risk of recurrence. Technological advancements in surgical procedures ensure efficient outcomes. Rehabilitation programs post-treatment improve recovery rates. Cosmetic and functional concerns drive patient preference.

China Ganglion Cysts Treatment Market Insight

The China ganglion cysts treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to increasing healthcare awareness, rising prevalence of musculoskeletal disorders, and expanding access to orthopedic and specialized treatment centers. Rapid urbanization and lifestyle changes contribute to higher incidence of wrist and hand cysts. Patients increasingly prefer minimally invasive surgical options and outpatient care. Hospitals and specialty clinics are expanding services to meet growing demand. Telemedicine and home-based rehabilitation improve treatment accessibility. Government initiatives and insurance policies enhance affordability. Growing disposable incomes support elective procedures for cosmetic and functional outcomes. Advanced imaging modalities facilitate early diagnosis. Recurrent cases drive repeat procedures. Awareness campaigns educate patients about treatment options. Urban centers report higher procedure volumes. Access to trained orthopedic surgeons ensures high-quality care. Rising patient demand for functional restoration sustains market growth.

Ganglion Cysts Treatment Market Share

The Ganglion Cysts Treatment industry is primarily led by well-established companies, including:

• Stryker (U.S.)

• Johnson & Johnson and its affiliates (U.S.)

• MicroPort Scientific Corporation (China)

• Arthrex, Inc. (U.S.)

• Smith & Nephew plc (U.K.)

• ConMed Corporation (U.S.)

• Mitek Sports Medicine (U.S.)

• Medtronic plc (Ireland/U.S.)

• NuVasive, Inc. (U.S.)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Orthofix Medical Inc. (U.S.)

• Globus Medical, Inc. (U.S.)

• B. Braun SE (Germany)

• Integra LifeSciences Holdings Corporation (U.S.)

• Henan Tianrui Medical Instrument Co., Ltd. (China)

Latest Developments in Global Ganglion Cysts Treatment Market

- In March 2023, a prospective interventional control trial was conducted at Saveetha Medical College Hospital in Chennai, India, comparing the efficacy of surgical excision versus steroid injection for treating ganglion cysts. The study involved 54 patients and aimed to provide insights into the most effective treatment options for this condition

- In August 2025, a retrospective analysis of 1,784 patients undergoing plastic surgery for ganglion cysts revealed that 83.4% had cysts in the upper extremity, with 58.9% localized in the dorsal wrist. The study aimed to evaluate treatment approaches and outcomes for ganglion cysts

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.