Global Gynecological Drugs Market

Market Size in USD Billion

USD

67.51 Billion

USD

86.86 Billion

2024

2032

USD

67.51 Billion

USD

86.86 Billion

2024

2032

| 2025 - 2032 | |

| USD 67.51 Billion | |

| USD 86.86 Billion | |

| % | |

|

Gynecological Drugs Market Size

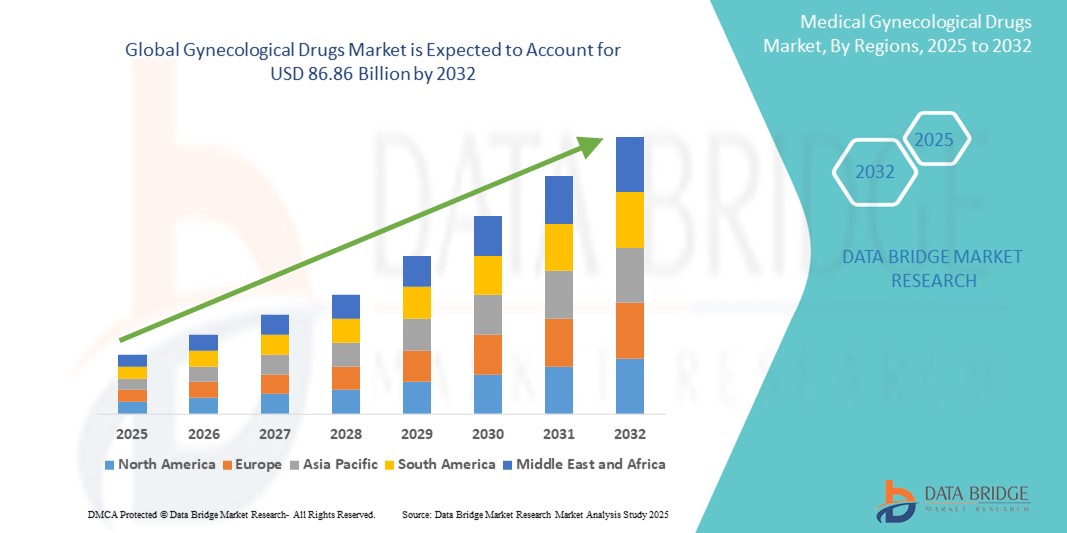

- The global gynecological drugs market size was valued at USD 67.51 billion in 2024 and is expected to reach USD 86.86 billion by 2032, at a CAGR of 3.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of gynecological disorders such as endometriosis, polycystic ovary syndrome (PCOS), and uterine fibroids, coupled with heightened awareness and improved healthcare infrastructure across developing nations

- Furthermore, rising demand for targeted and hormone-based therapies, along with advancements in drug delivery systems and increasing focus on women’s health by pharmaceutical companies, is establishing gynecological drugs as a key segment in the therapeutic space. These converging factors are accelerating the uptake of innovative treatment options, thereby significantly boosting the industry’s growth

Gynecological Drugs Market Analysis

- Gynecological drugs, encompassing a broad range of therapeutic solutions for conditions affecting the female reproductive system, are essential components of modern women's healthcare due to their role in managing disorders such as endometriosis, polycystic ovary syndrome (PCOS), menstrual disorders, and menopausal symptoms

- The escalating demand for gynecological drugs is primarily fueled by the increasing prevalence of gynecological conditions, rising awareness about women’s health, and growing access to healthcare services, particularly in emerging economies

- North America dominated the gynecological drugs market with the largest revenue share of 40.1% in 2024, characterized by a well-established healthcare infrastructure, high health expenditure, and strong presence of leading pharmaceutical companies, with the U.S. experiencing significant uptake of hormonal therapies and minimally invasive treatments driven by innovations in drug formulation and personalized medicine

- Asia-Pacific is expected to be the fastest growing region in the gynecological drugs market during the forecast period due to expanding healthcare access, improving diagnosis rates, and increasing investments in women’s health initiatives

- The hormonal therapy segment dominated the gynecological drugs market with a market share of 42.3% in 2024, driven by its effectiveness in managing menopause-related symptoms and menstrual disorders, as well as its growing adoption across both developed and developing markets

Report Scope and Gynecological Drugs Market Segmentation

|

Attributes |

Gynecological Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Gynecological Drugs Market Trends

“Advancement in Hormonal Therapies and Personalized Medicine”

- A significant and accelerating trend in the global gynecological drugs market is the growing emphasis on personalized medicine and advancements in hormonal therapies tailored to individual hormonal profiles and genetic markers. This evolution in treatment protocols is enhancing patient outcomes and minimizing side effects

- For instance, newer formulations of hormonal contraceptives and menopause management drugs are being developed with improved safety profiles, such as bioidentical hormone therapies that more closely mimic the body’s natural hormones. Companies such as Pfizer and Bayer are at the forefront of developing such advanced hormonal solutions for long-term use with better tolerance

- Personalized gynecological treatments increasingly leverage diagnostics and genomic data to customize therapies for conditions such as PCOS, endometriosis, and infertility. Companion diagnostics and hormone level profiling are being used to identify optimal drug regimens, reducing the trial-and-error approach traditionally associated with treatment

- The integration of digital health tools, such as mobile health apps and wearable hormone monitoring devices, is further enhancing treatment personalization. These technologies allow for real-time tracking of symptoms and hormone levels, facilitating timely drug adjustments and increasing patient engagement

- This trend towards precision healthcare is reshaping expectations for gynecological drug efficacy and safety. Consequently, pharmaceutical companies are investing in R&D pipelines that include targeted therapies and delivery systems tailored to individual patient needs

- The demand for gynecological drugs offering better tolerability, long-term effectiveness, and customized treatment plans is rapidly increasing across both developed and emerging markets, as awareness of reproductive and hormonal health continues to rise

Gynecological Drugs Market Dynamics

Driver

“Rising Prevalence of Gynecological Disorders and Increasing Awareness”

- The growing global burden of gynecological conditions such as uterine fibroids, endometriosis, PCOS, and menopause-related complications is a major driver of the gynecological drugs market. Increasing health awareness and the expansion of women-centric healthcare initiatives are further fueling demand

- For instance, in 2024, Organon & Co. launched a new awareness campaign focused on endometriosis, aimed at improving early diagnosis and treatment adoption. Such initiatives by key players are expected to accelerate the uptake of therapeutic solutions in this field

- As more women seek medical attention for previously underdiagnosed or stigmatized conditions, the demand for effective, accessible, and convenient pharmaceutical solutions continues to grow

- Furthermore, the growing global emphasis on women's reproductive health and the inclusion of gynecological care in public health agendas are increasing drug accessibility in emerging markets

- Advances in oral, injectable, and transdermal drug delivery systems are also enhancing patient adherence, convenience, and outcomes, supporting the rising adoption of these therapies across diverse demographics

Restraint/Challenge

“Side Effects, Social Stigma, and Regulatory Complexities”

- Despite the growing demand, side effects associated with hormonal treatments—such as weight gain, mood changes, and cardiovascular risks—remain a significant barrier to widespread adoption of certain gynecological drugs. These concerns can lead to patient reluctance or discontinuation of therapy

- For instance, concerns regarding long-term use of hormone replacement therapy (HRT) and its potential link to breast cancer or thrombosis have led to cautious prescribing, especially in older populations

- In addition, social stigma surrounding reproductive and menstrual health continues to deter open discussion and timely treatment in many cultures, particularly in developing countries. This limits diagnosis rates and access to appropriate therapy

- Regulatory hurdles for drug approval, particularly for hormone-based therapies and novel treatment modalities, further delay market entry. Pharmaceutical companies face lengthy clinical trial processes and stringent safety validation requirements

- Overcoming these challenges through the development of safer drug formulations, expanded awareness programs, cultural sensitivity in outreach, and accelerated regulatory pathways will be critical for unlocking the full potential of the gynecological drugs market

Gynecological Drugs Market Scope

The market is segmented on the basis of disease type, therapy type, population type, drug type, route of administration, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the gynecological drugs market is segmented into gynecological cancer, polycystic ovarian syndrome (PCOS), genital tract infection, endometriosis, ovarian cyst, contraception, and others. The contraception segment dominated the market with the largest market revenue share in 2024, driven by increasing awareness and use of birth control measures globally. The demand for hormonal contraceptives, including oral pills, injectables, and intrauterine devices, remains strong due to their effectiveness and ease of use. The market also sees strong growth in this segment due to supportive government policies and education initiatives focused on reproductive health.

The endometriosis segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising diagnosis rates, increased awareness among women, and the development of targeted therapies that offer symptom relief without invasive surgical interventions. The growing number of research studies and clinical trials dedicated to non-opioid and hormone-sparing treatments is also contributing to this segment’s acceleration.

- By Therapy Type

On the basis of therapy type, the gynecological drugs market is segmented into hormonal, non-hormonal, and others. The hormonal segment held the largest market revenue share of 42.3% in 2024 due to its widespread application in treating conditions such as PCOS, menopause-related disorders, and contraception. Hormonal drugs are often considered first-line therapies due to their proven efficacy, fast symptom relief, and clinical familiarity among healthcare providers. The segment continues to grow with the introduction of bioidentical hormones and combination therapies.

The non-hormonal segment is expected to witness the fastest CAGR from 2025 to 2032, driven by a rising preference for alternatives with fewer systemic side effects. These therapies are gaining traction particularly in the management of menopausal symptoms and mild gynecological infections among women who cannot or choose not to take hormone-based treatments.

- By Population Type

On the basis of population type, the gynecological drugs market is segmented into adolescents and adults. The adult segment dominated the market with the largest market revenue share in 2024, attributed to the high prevalence of gynecological disorders among women of reproductive and post-reproductive age. Adults represent the primary consumers of contraceptives, fertility treatments, and menopause management drugs, with strong growth supported by improved health awareness and increased gynecological consultations.

The adolescent segment is expected to witness the fastest CAGR from 2025 to 2032, due to growing menstrual health education and early diagnosis of hormonal imbalances and reproductive system disorders. Campaigns promoting adolescent health and better access to specialized care are further driving this segment.

- By Drug Type

On the basis of drug type, the gynecological drugs market is segmented into branded and generics. The branded segment held the largest market revenue share in 2024, driven by innovation, patent-protected therapies, and higher physician and consumer trust. Pharmaceutical companies continue to invest heavily in branded formulations that offer enhanced safety, efficacy, or novel delivery mechanisms.

The generics segment is anticipated to grow at the fastest rate from 2025 to 2032, supported by increasing demand for affordable healthcare solutions, especially in emerging markets. Patent expirations and healthcare cost-containment efforts are contributing significantly to the expanding footprint of generic gynecological drugs.

- By Route Of Administration

On the basis of route of administration, the gynecological drugs market is segmented into oral, parenteral, intravaginal, and others. The oral segment dominated the market with the largest market revenue share in 2024, supported by convenience, patient compliance, and the widespread use of oral hormonal contraceptives and hormone replacement therapies. The ease of administration and cost-effectiveness make this route the most preferred globally.

The intravaginal segment is expected to witness the fastest CAGR from 2025 to 2032, due to rising acceptance of local hormone therapies that minimize systemic exposure. Innovations in vaginal rings, creams, and pessaries tailored for prolonged and targeted delivery are fueling this segment’s

- By End User

On the basis of end user, the gynecological drugs market is segmented into hospitals, specialty clinics, diagnostic centers, research institutes, and others. The hospital segment held the largest market revenue share in 2024, driven by the availability of comprehensive diagnostic and therapeutic services under one roof. Hospitals serve as primary access points for women seeking specialized care for complex gynecological conditions, surgeries, and cancer treatments.

The specialty clinics segment is anticipated to witness the fastest growth rate from 2025 to 2032, supported by the growing number of women’s health centers and fertility clinics offering advanced treatment modalities. Increased focus on outpatient care and patient-centered approaches further drives this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The retail pharmacy segment dominated the market with the largest market revenue share in 2024, due to the easy availability of OTC products and prescription gynecological drugs. Widespread presence, affordability, and pharmacist guidance continue to favor this channel.

The online pharmacy segment is expected to witness the fastest growth from 2025 to 2032, driven by digital transformation in healthcare, increasing smartphone penetration, and rising consumer preference for doorstep delivery of prescription medications. Subscription-based platforms offering contraception and hormone therapy delivery services are also propelling growth in this segment

Gynecological Drugs Market Regional Analysis

- North America dominated the gynecological drugs market with the largest revenue share of 40.1% in 2024, characterized by a well-established healthcare infrastructure, high health expenditure, and strong presence of leading pharmaceutical companies, with the U.S. experiencing significant uptake of hormonal therapies and minimally invasive treatments driven by innovations in drug formulation and personalized medicine

- Consumers in the region place high value on early diagnosis, personalized treatment plans, and access to a wide range of hormonal and non-hormonal therapies offered through both public and private healthcare systems

- This widespread adoption is further supported by high healthcare spending, favorable reimbursement policies, and the presence of major pharmaceutical companies actively investing in R&D, establishing North America as a key market for advanced gynecological therapeutics and ongoing innovation

U.S. Gynecological Drugs Market Insight

The U.S. gynecological drugs market captured the largest revenue share of 78.5% in 2024 within North America, fueled by the rising prevalence of gynecological disorders and the country’s advanced healthcare infrastructure. Increasing awareness of women's reproductive health, along with access to a wide range of branded and generic drugs, supports robust market growth. The demand for hormonal therapies and personalized treatments is growing, supported by a strong pharmaceutical pipeline, widespread insurance coverage, and ongoing public health campaigns focused on early detection and treatment.

Europe Gynecological Drugs Market Insight

The Europe gynecological drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increased focus on women's health, favorable reimbursement policies, and rising diagnosis rates of conditions such as PCOS and endometriosis. The region’s aging female population and high demand for menopause-related treatments are key growth drivers. With strong regulatory oversight and proactive health initiatives, European countries are increasingly adopting innovative hormonal and non-hormonal therapies across both public and private healthcare settings.

U.K. Gynecological Drugs Market Insight

The U.K. gynecological drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising public awareness, early intervention strategies, and strong access to healthcare services. Efforts to improve menstrual health education and increase diagnosis of reproductive disorders are encouraging market growth. In addition, the U.K.’s National Health Service (NHS) support for contraceptives and hormone therapies continues to facilitate broader access to gynecological treatments.

Germany Gynecological Drugs Market Insight

The Germany gynecological drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced research capabilities, growing patient awareness, and strong demand for both branded and biosimilar hormonal therapies. Germany's comprehensive health insurance coverage and well-structured healthcare delivery system support increased access to reproductive and hormonal health treatments. Innovations in drug delivery and a focus on patient-centric care further stimulate demand across various patient populations.

Asia-Pacific Gynecological Drugs Market Insight

The Asia-Pacific gynecological drugs market is poised to grow at the fastest CAGR of 23.2% during the forecast period of 2025 to 2032, driven by rising awareness of women’s health, increasing access to healthcare services, and rapid urbanization in countries such as China, India, and Japan. Government-led initiatives and partnerships with global health organizations are strengthening early diagnosis and access to essential gynecological medications. The growing middle class and expansion of digital health platforms further support market growth.

Japan Gynecological Drugs Market Insight

The Japan gynecological drugs market is gaining momentum due to an aging female population, growing demand for menopause and osteoporosis-related treatments, and strong adoption of advanced hormonal therapies. Japan’s focus on preventive care, coupled with high standards for pharmaceutical quality and efficacy, supports continued innovation and uptake of both traditional and novel gynecological drugs. Integration with digital health technologies is also enhancing treatment adherence and personalized care.

India Gynecological Drugs Market Insight

The India gynecological drugs market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to growing awareness of women’s health, expanding healthcare infrastructure, and rising incidence of conditions such as PCOS and fibroids. The increasing availability of cost-effective generic options, government-sponsored health programs, and a large target population are driving demand. India’s strong domestic pharmaceutical industry and focus on improving access to reproductive health services position it as a key growth market in the region.

Gynecological Drugs Market Share

The gynecological drugs industry is primarily led by well-established companies, including:

- Lilly (U.S.)

- Pfizer, Inc. (U.S.)

- Amgen Inc. (U.S.)

- AstraZeneca (U.K.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Bayer AG (Germany)

- Aldan Healthcare (India)

- Xeno Pharmaceuticals (U.S.)

- AbbVie Inc. (U.S.)

- Lupin (India)

- TherapeuticsMD Inc. (U.S.)

- Ferring (Switzerland)

- Teva Pharmaceutical Industries Limited (Israel)

- ADDEX THERAPEUTICS (Switzerland)

- BIOCAD (Russia)

What are the Recent Developments in Global Gynecological Drugs Market?

- In April 2023, Organon & Co., a global healthcare company focused on women’s health, announced the launch of a collaborative awareness initiative in partnership with local healthcare providers in Latin America to improve early diagnosis and treatment of endometriosis. The campaign includes educational programs, diagnostic support, and access to hormonal therapies, highlighting Organon’s commitment to addressing underserved gynecological conditions and expanding access to treatment across emerging markets

- In March 2023, Myovant Sciences and Pfizer Inc. received expanded regulatory approval for MYFEMBREE®, a once-daily treatment for moderate to severe endometriosis pain, in the European Union. This marks a significant advancement in non-surgical treatment options, offering improved quality of life for women living with chronic gynecological pain. The approval strengthens the companies’ joint portfolio and reflects growing investment in innovative hormonal therapies

- In March 2023, Bayer AG announced new clinical trial results for its investigational drug OCEANA—a non-hormonal therapy targeting uterine fibroids. The Phase II study demonstrated promising efficacy and safety outcomes, paving the way for further development. Bayer’s continued focus on fibroid and endometriosis research emphasizes its strategic priority to lead in women’s health through targeted drug innovation

- In February 2023, AbbVie, in collaboration with Neurocrine Biosciences, expanded the market reach of ORILISSA® and ORIAHNN® by introducing the therapies into select Asia-Pacific countries through strategic regional partnerships. These treatments offer oral, non-invasive options for managing endometriosis and uterine fibroid symptoms, aligning with the rising regional demand for advanced, accessible women’s healthcare solutions

- In January 2023, Teva Pharmaceuticals launched a generic version of a leading oral contraceptive in the U.S. market, increasing accessibility and affordability for a broad patient base. The introduction underscores the importance of generic competition in improving healthcare equity and Teva’s continued contribution to expanding treatment options within the gynecological drugs space

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.