Global Hearing Screening Diagnostic Devices Market

Market Size in USD Billion

USD

2.45 Billion

USD

3.96 Billion

2025

2033

USD

2.45 Billion

USD

3.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.45 Billion | |

| USD 3.96 Billion | |

| % | |

|

Hearing Screening Diagnostic Devices Market Size

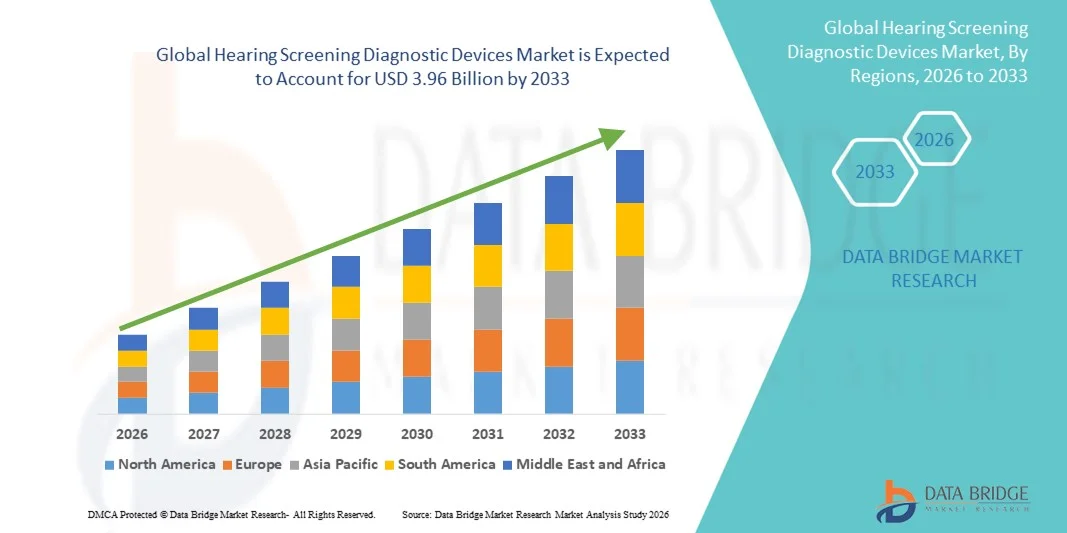

- The global hearing screening diagnostic devices market size was valued at USD 2.45 billion in 2025 and is expected to reach USD 3.96 billion by 2033, at a CAGR of 6.20% during the forecast period

- The market growth is largely driven by the rising prevalence of hearing loss across all age groups, along with increasing awareness regarding early diagnosis and preventive hearing healthcare, supported by advancements in audiometric and screening technologies

- Furthermore, growing adoption of hearing screening programs in hospitals, clinics, schools, and community healthcare settings, combined with demand for accurate, portable, and easy-to-use diagnostic solutions, is positioning hearing screening devices as essential tools in modern auditory healthcare, thereby significantly boosting overall market growth

Hearing Screening Diagnostic Devices Market Analysis

- Hearing screening diagnostic devices, which enable early detection and assessment of hearing impairments through audiometric and objective testing methods, are increasingly critical components of modern preventive healthcare across hospitals, clinics, neonatal care units, and community screening programs due to their accuracy, portability, and ease of use

- The growing demand for hearing screening diagnostic devices is primarily driven by the rising prevalence of hearing loss across all age groups, increasing awareness of early diagnosis benefits, and government-supported hearing screening initiatives, particularly for newborns, children, and the elderly population

- North America dominated the hearing screening diagnostic devices market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, high adoption of neonatal and adult hearing screening programs, and a strong presence of leading diagnostic device manufacturers, with the U.S. witnessing robust demand from hospitals, audiology clinics, and preventive health programs

- Asia-Pacific is expected to be the fastest growing region in the hearing screening diagnostic devices market during the forecast period due to expanding healthcare access, growing birth rates in emerging economies, increasing awareness of hearing health, and rising investments in public health screening initiatives

- Pure-tone Test segment dominated the hearing screening diagnostic devices market with a market share of 41.5% in 2025, driven by its widespread clinical acceptance, cost-effectiveness, and extensive use across routine hearing assessments in both pediatric and adult populations

Report Scope and Hearing Screening Diagnostic Devices Market Segmentation

|

Attributes |

Hearing Screening Diagnostic Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Hearing Screening Diagnostic Devices Market Trends

Integration of AI and Digital Health Technologies for Early Detection

- A significant and accelerating trend in the global hearing screening diagnostic devices market is the increasing integration of artificial intelligence (AI), digital signal processing, and cloud-based platforms to enhance screening accuracy, efficiency, and early diagnosis across diverse healthcare settings

- For instance, several modern otoacoustic emission (OAE) and automated auditory brainstem response (AABR) devices now incorporate AI-driven algorithms to reduce false positives and enable faster screening in newborn and pediatric populations, improving workflow efficiency in hospitals

- AI integration in hearing screening devices enables features such as automated result interpretation, adaptive testing based on patient responses, and intelligent flagging of abnormal patterns, thereby reducing reliance on highly specialized audiologists and minimizing human error

- The growing compatibility of hearing screening devices with electronic health records (EHRs), telehealth platforms, and mobile applications facilitates seamless data sharing, remote monitoring, and centralized management of screening outcomes across healthcare networks

- This trend toward more intelligent, connected, and user-friendly diagnostic solutions is reshaping expectations for preventive hearing care, particularly in large-scale public health screening programs and resource-limited environments

- The adoption of portable and handheld hearing screening devices is increasing significantly, enabling rapid testing in remote, rural, and point-of-care settings without the need for specialized infrastructure

- Consequently, companies such as Natus Medical and Interacoustics are developing advanced hearing screening systems with AI-supported analytics, cloud connectivity, and portable designs to address the evolving needs of modern healthcare providers

Hearing Screening Diagnostic Devices Market Dynamics

Driver

Rising Prevalence of Hearing Loss and Expansion of Screening Programs

- The increasing prevalence of hearing impairment across newborns, adults, and the aging population, combined with growing awareness of early diagnosis benefits, is a major driver fueling demand for hearing screening diagnostic devices

- For instance, in March 2025, several public health authorities expanded mandatory newborn hearing screening initiatives, driving increased procurement of AABR and OAE devices by hospitals and maternity centers

- As untreated hearing loss is increasingly linked to delayed speech development, cognitive decline, and reduced quality of life, healthcare providers are prioritizing routine hearing assessments, thereby accelerating device adoption

- Furthermore, government-backed screening programs and recommendations from organizations such as pediatric and geriatric healthcare associations are making hearing screening a standard component of preventive care pathways

- Increasing focus on early childhood development and speech-language outcomes is driving hospitals and pediatric clinics to invest in routine hearing screening equipment

- Moreover, growing life expectancy and the expanding geriatric population are accelerating demand for regular hearing assessments, particularly in age-related hearing loss management programs

- The growing availability of portable, automated, and easy-to-use screening devices is supporting wider adoption across primary care clinics, schools, and community healthcare settings, contributing significantly to market growth

Restraint/Challenge

High Equipment Costs and Limited Skilled Workforce

- The relatively high cost of advanced hearing screening diagnostic devices, particularly those incorporating AI, automation, and connectivity features, poses a challenge to widespread adoption, especially in low- and middle-income regions

- For instance, budget constraints in public healthcare systems can delay large-scale procurement of modern screening equipment, limiting access to early hearing detection in underserved populations

- In addition, the need for trained personnel to operate devices, interpret results, and manage follow-up referrals remains a barrier in regions facing shortages of audiologists and skilled healthcare professionals

- While automated systems reduce complexity, concerns related to calibration, maintenance, and compliance with clinical standards can hinder adoption among smaller clinics and rural healthcare facilities

- Limited awareness regarding hearing screening importance in certain regions continues to restrict testing rates, particularly outside neonatal and hospital-based environments

- Furthermore, inconsistent reimbursement policies and lack of standardized screening guidelines across countries can discourage healthcare providers from adopting advanced diagnostic devices

- Overcoming these challenges through cost-effective device development, workforce training initiatives, and increased government funding for hearing health programs will be critical for sustaining long-term market growth

Hearing Screening Diagnostic Devices Market Scope

The market is segmented on the basis of product, age group, indication, test type, and end user.

- By Product

On the basis of product, the global hearing screening diagnostic devices market is segmented into OAE/ABR testing devices, audiometers, and immittance screeners. The OAE/ABR testing devices segment dominated the market in 2025, driven by their widespread use in universal newborn hearing screening programs and their ability to provide objective, fast, and reliable results without active patient participation. These devices are particularly critical in neonatal and pediatric settings, where early detection of hearing impairment is essential for timely intervention and speech development. Strong government mandates, hospital adoption, and technological advancements such as automated interpretation further support the dominance of this segment. In addition, OAE/ABR devices are increasingly preferred due to their portability and suitability for large-scale screening initiatives.

The audiometers segment is expected to be the fastest growing during the forecast period, supported by rising demand for comprehensive hearing assessments across adult and geriatric populations. Audiometers are widely used in diagnostic clinics, occupational health screenings, and audiology centers to evaluate hearing thresholds and monitor progressive hearing loss. Growing awareness of age-related and noise-induced hearing loss, coupled with increasing workplace hearing conservation programs, is accelerating adoption. Technological improvements such as digital, PC-based, and portable audiometers are further expanding their application scope and market growth potential.

- By Age

On the basis of age, the market is segmented into newborn hearing screening and others. The newborn hearing screening segment held the largest revenue share in 2025, driven by mandatory screening policies in many developed and developing countries aimed at early identification of congenital hearing loss. Hospitals and maternity centers routinely deploy OAE and AABR devices to screen newborns within the first days of life, ensuring early intervention and improved developmental outcomes. Strong support from pediatric healthcare organizations and public health authorities further reinforces the dominance of this segment. The proven long-term benefits of early diagnosis in reducing speech and learning delays continue to sustain high adoption rates.

The others segment is projected to witness the fastest growth over the forecast period, fueled by increasing screening initiatives among children, adults, and the elderly population. Rising prevalence of age-related hearing loss, occupational noise exposure, and lifestyle-related auditory issues is driving demand for routine hearing assessments beyond neonatal care. Schools, workplaces, and community healthcare programs are increasingly incorporating hearing screening to detect impairments at earlier stages. This expanding focus on lifelong hearing health is supporting rapid growth of this segment.

- By Indication

On the basis of indication, the market is segmented into conductive hearing loss, sensorineural hearing loss, combination hearing loss, and others. The sensorineural hearing loss segment dominated the market in 2025, primarily due to its high prevalence across all age groups and its association with aging, noise exposure, genetic factors, and chronic diseases. Hearing screening devices play a crucial role in early identification and monitoring of sensorineural impairments, particularly in newborns and older adults. The increasing global burden of irreversible hearing loss is driving sustained demand for diagnostic screening solutions. This segment also benefits from extensive clinical focus and research attention.

The combination hearing loss segment is expected to grow at the fastest rate during the forecast period, supported by increasing recognition of mixed auditory conditions requiring comprehensive diagnostic evaluation. Advances in screening technologies now allow more accurate differentiation between conductive and sensorineural components, improving diagnosis and treatment planning. Growing access to diagnostic services and specialist care is enabling better detection of complex hearing loss cases. As awareness improves, demand for advanced screening devices capable of multi-parameter assessment is rising.

- By Test

On the basis of test type, the market is segmented into pure-tone test, bone conduction test, tests of the middle ear, speech discrimination test, speech recognition threshold test, most comfortable listening test, and uncomfortable loudness level test. The pure-tone test segment dominated the market in 2025 with a market share of 41.5%, owing to its widespread use as a standard and cost-effective method for initial hearing assessment. Pure-tone audiometry is routinely performed across hospitals, clinics, and diagnostic centers for both pediatric and adult populations. Its simplicity, reliability, and compatibility with a wide range of audiometers contribute to its dominant position. The test remains a foundational component of hearing evaluation protocols worldwide.

The speech recognition threshold test segment is anticipated to be the fastest growing during forecast period, driven by increasing emphasis on functional hearing assessment and real-world communication abilities. This test provides valuable insights into a patient’s ability to recognize and understand speech, which is critical for treatment planning and hearing aid fitting. Rising demand for patient-centric diagnostic approaches is supporting adoption of speech-based tests. Technological integration with digital audiology systems is further enhancing their clinical relevance.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic centers, and others. The hospitals and clinics segment dominated the market in 2025, driven by high patient inflow, availability of skilled professionals, and routine implementation of hearing screening programs. Hospitals serve as primary centers for newborn screening, pediatric assessments, and adult diagnostic evaluations, ensuring consistent demand for screening devices. Integration of hearing screening into preventive healthcare pathways further strengthens this segment’s dominance. Access to advanced diagnostic infrastructure also supports broader device utilization.

The diagnostic centers segment is expected to register the fastest growth during the forecast period, supported by the rising number of specialized audiology and diagnostic facilities. These centers offer dedicated hearing assessment services with shorter wait times and advanced testing capabilities, attracting both referred and self-paying patients. Increasing privatization of healthcare and demand for specialized diagnostics are accelerating growth in this segment. Expansion of standalone screening centers in urban and semi-urban areas further contributes to rapid market expansion.

Hearing Screening Diagnostic Devices Market Regional Analysis

- North America dominated the hearing screening diagnostic devices market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, high adoption of neonatal and adult hearing screening programs, and a strong presence of leading diagnostic device manufacturers

- Healthcare providers in the region place significant importance on accurate, efficient, and automated hearing screening solutions that integrate seamlessly with hospital information systems and electronic health records

- This widespread adoption is further supported by advanced healthcare infrastructure, favorable reimbursement policies, high healthcare expenditure, and strong awareness of preventive hearing care, establishing hearing screening devices as essential tools across hospitals, clinics, and diagnostic centers

U.S. Hearing Screening Diagnostic Devices Market Insight

The U.S. hearing screening diagnostic devices market captured the largest revenue share within North America in 2025, driven by the strong emphasis on early diagnosis, widespread implementation of universal newborn hearing screening programs, and high healthcare expenditure. Healthcare providers increasingly prioritize advanced, automated hearing screening solutions to improve detection accuracy and clinical efficiency. The growing prevalence of age-related and noise-induced hearing loss further supports market growth. In addition, the integration of hearing screening devices with electronic health records and tele-audiology platforms is significantly contributing to market expansion.

Europe Hearing Screening Diagnostic Devices Market Insight

The Europe hearing screening diagnostic devices market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by well-established public healthcare systems and strong regulatory support for preventive screening. Increasing awareness of early hearing loss detection and rising adoption of routine screening across hospitals and diagnostic centers are fostering market growth. European healthcare providers also value standardized diagnostic protocols and high-quality medical devices. The region is witnessing consistent demand across neonatal, pediatric, adult, and geriatric screening applications, supported by both public and private healthcare investments.

U.K. Hearing Screening Diagnostic Devices Market Insight

The U.K. hearing screening diagnostic devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong government-backed newborn hearing screening initiatives and increasing focus on preventive healthcare. Rising awareness of hearing health among the aging population is encouraging routine screening in hospitals and community settings. The U.K.’s well-integrated healthcare infrastructure supports the adoption of advanced diagnostic technologies. In addition, growing use of portable and automated screening devices is enhancing accessibility across primary care and diagnostic facilities.

Germany Hearing Screening Diagnostic Devices Market Insight

The Germany hearing screening diagnostic devices market is expected to expand at a considerable CAGR during the forecast period, supported by advanced healthcare infrastructure and high adoption of technologically sophisticated medical devices. Germany’s emphasis on early diagnosis, precision diagnostics, and quality healthcare is driving demand for reliable hearing screening solutions. Increasing screening among the elderly population further contributes to market growth. The integration of digital diagnostic systems and strict adherence to clinical standards align well with local healthcare practices, reinforcing adoption across hospitals and specialized clinics.

Asia-Pacific Hearing Screening Diagnostic Devices Market Insight

The Asia-Pacific hearing screening diagnostic devices market is poised to grow at the fastest CAGR during the forecast period, driven by expanding healthcare access, rising birth rates, and increasing awareness of hearing health in countries such as China, Japan, and India. Government-led initiatives promoting early diagnosis and preventive care are accelerating adoption of screening devices. Rapid urbanization and improvements in healthcare infrastructure are further supporting market growth. In addition, the availability of cost-effective and portable screening solutions is expanding access to hearing diagnostics across a broader population base.

Japan Hearing Screening Diagnostic Devices Market Insight

The Japan hearing screening diagnostic devices market is gaining momentum due to the country’s aging population, strong healthcare system, and high awareness of hearing-related health issues. Demand for regular hearing assessments among elderly individuals is driving adoption across hospitals and clinics. Japan’s focus on technological innovation supports the use of advanced and automated screening devices. Furthermore, integration of hearing screening into routine health checkups is fueling steady market growth across both public and private healthcare sectors.

India Hearing Screening Diagnostic Devices Market Insight

The India hearing screening diagnostic devices market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to a large population base, high birth rates, and growing emphasis on early diagnosis of hearing impairment. Increasing government initiatives for newborn and school-based screening programs are supporting market expansion. Rapid improvements in healthcare infrastructure and rising awareness of hearing health are further driving adoption. The availability of affordable screening devices and expanding diagnostic centers are key factors propelling market growth across urban and semi-urban regions in India.

Hearing Screening Diagnostic Devices Market Share

The Hearing Screening Diagnostic Devices industry is primarily led by well-established companies, including:

- Interacoustics A/S (Denmark)

- Natus Medical Incorporated (U.S.)

- MedRx Inc. (U.S.)

- Amplivox (U.K.)

- Vivosonic Inc (Canada)

- Grason‑Stadler Inc. (U.S.)

- Path Medical GmbH (Germany)

- Sivantos Group (Singapore/Germany)

- Welch Allyn (Hillrom/Baxter) (U.S.)

- RION Co., Ltd. (Japan)

- Echodia (France)

- Auditdata A/S (Denmark)

- Benson Medical Instruments Co. (U.S.)

- Micro‑DSP Technology Co., Ltd. (Taiwan)

- Hearing Screening Associates (U.S.)

- Otometrics A/S (Denmark/U.S.)

- William Demant Holding A/S (Denmark)

- WS Audiology (Denmark)

- Cochlear Limited (Australia)

What are the Recent Developments in Global Hearing Screening Diagnostic Devices Market?

- In October 2025, Natus Sensory entered an agreement with Auditdata to distribute the Otometrics® Measure system, a portable all-in-one audiometer and fitting unit, broadening access to flexible hearing assessment and diagnostic solutions worldwide

- In January 2025, Apple released a software feature that effectively turns AirPods Pro 2 into hearing aid–capable devices and enables pure-tone audiometry testing via iPhone/iPad, increasing awareness of hearing screening and promoting early self-testing for mild to moderate hearing loss

- In October 2024, Neuranix’s med-wave® audiology device received regulatory approval in the UK and Ireland for use on babies from newborn to two years old, providing fast, non-invasive middle ear analysis and enhancing neonatal and pediatric hearing assessments

- In September 2024, Natus Medical Incorporated launched the MADSEN Zodiac+ audiometer with enhanced connectivity features and AI-powered test protocols, improving screening efficiency and data management capabilities for clinicians conducting hearing screening programs

- In May 2024, hearX Group officially launched hearOAE, a next-generation otoacoustic emissions (OAE) testing device capable of TEOAE and DPOAE screening and diagnostics, designed for smartphone and tablet use with Bluetooth connectivity, aiming to expand accessible hearing testing in newborn and elderly care settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.