Global Hemolytic Anemia Market

Market Size in USD Million

USD

362.01 Million

USD

551.38 Million

2024

2032

USD

362.01 Million

USD

551.38 Million

2024

2032

| 2025 - 2032 | |

| USD 362.01 Million | |

| USD 551.38 Million | |

| % | |

|

Hemolytic Anemia Market Size

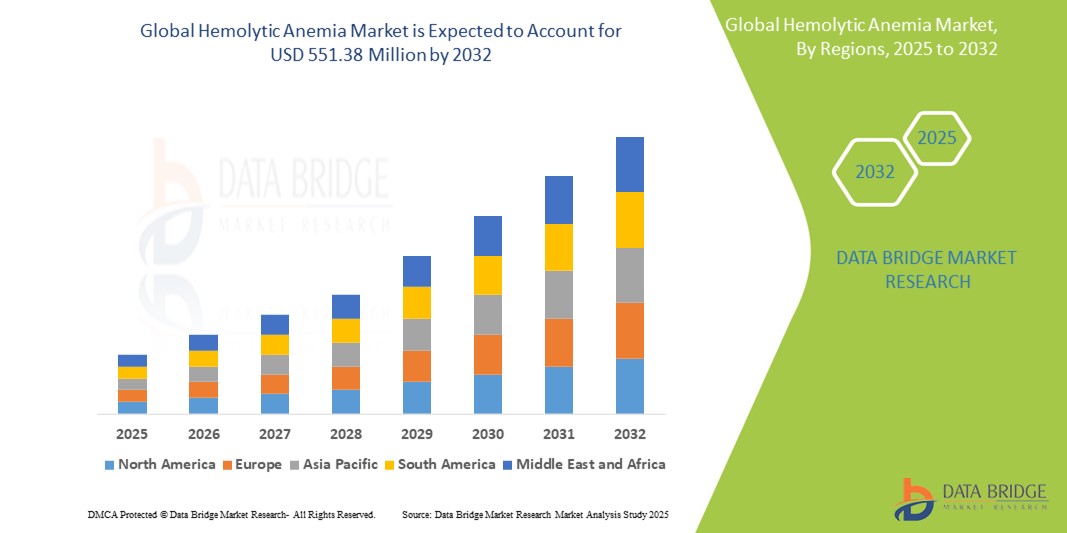

- The global hemolytic anemia market size was valued at USD 362.01 million in 2024 and is expected to reach USD 551.38 million by 2032, at a CAGR of 5.40% during the forecast period

- The market growth is primarily driven by the increasing prevalence of hemolytic anemia, particularly autoimmune and hereditary forms, coupled with advancements in diagnostic technologies and treatment options including gene therapy and targeted biologics

- Moreover, rising awareness, early diagnosis initiatives, and the introduction of novel therapeutics by key pharmaceutical players are transforming the disease management landscape. These factors are collectively contributing to a robust market trajectory, positioning hemolytic anemia as a critical focus within the broader rare disease therapeutics sector

Hemolytic Anemia Market Analysis

- Hemolytic anemia, characterized by the premature destruction of red blood cells, is gaining increasing clinical attention due to its complex etiology encompassing autoimmune, hereditary, and drug-induced causes, necessitating tailored diagnostics and therapeutic strategies across hospital and specialty care settings

- The rising demand for effective treatment options is fueled by increased awareness, advancements in molecular diagnostics, and improved understanding of genetic mutations, along with a growing patient population requiring long-term disease management

- North America dominated the hemolytic anemia market with the largest revenue share of 40.1% in 2024, driven by early adoption of advanced biologics, favorable reimbursement structures, and robust research investments, particularly in the U.S., where clinical trials and orphan drug approvals are accelerating treatment innovations

- Asia-Pacific is expected to be the fastest growing region in the hemolytic anemia market during the forecast period, attributed to improving healthcare infrastructure, rising diagnosis rates, and growing focus on rare disease management in countries such as China and India

- Blood transfusions segment dominated the hemolytic anemia market with a market share of 35.2% in 2024, driven by its established reputation for security and ease of retrofit into existing door setups

Report Scope and Hemolytic Anemia Market Segmentation

|

Attributes |

Hemolytic Anemia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hemolytic Anemia Market Trends

“Advancements in Targeted and Gene-Based Therapies”

- A key and accelerating trend in the global hemolytic anemia market is the advancement of targeted therapies and gene-based treatment approaches, particularly for inherited forms such as sickle cell disease and thalassemia. These innovations are reshaping the treatment landscape, offering potentially curative and less toxic alternatives to traditional interventions

- For instance, the development of gene-editing therapies such as CRISPR-based treatments for sickle cell anemia is gaining momentum, with promising trial outcomes and increasing regulatory support. Vertex Pharmaceuticals and CRISPR Therapeutics have collaborated on a novel gene therapy, exagamglogene autotemcel (exa-cel), which has shown durable efficacy in early studies

- Targeted biologics such as rituximab for autoimmune hemolytic anemia (AIHA) are also witnessing expanded use due to their ability to precisely modulate the immune response while minimizing systemic side effects. These treatments are especially effective in patients unresponsive to corticosteroids or conventional immunosuppressants

- Furthermore, the emergence of oral agents such as voxelotor and luspatercept for sickle cell disease and beta-thalassemia, respectively, is transforming disease management by reducing the need for frequent transfusions and hospital visits. These oral therapies are improving patient compliance and quality of life

- The integration of precision diagnostics, such as next-generation sequencing (NGS) and high-resolution genotyping, allows for early detection, disease subtyping, and individualized therapy plans, contributing to improved clinical outcomes and reduced healthcare burdens

- This shift toward more precise, disease-modifying treatments is redefining therapeutic goals in hemolytic anemia, with leading pharmaceutical companies and biotech firms investing heavily in research and pipeline expansion to meet growing patient needs globally

Hemolytic Anemia Market Dynamics

Driver

“Rising Prevalence and Improved Diagnostic Awareness”

- The growing global prevalence of hemolytic anemia—both inherited and acquired forms—coupled with greater awareness and access to diagnostic services is a major driver fueling market growth. The rise in chronic conditions, autoimmune diseases, and genetic disorders has led to a steady increase in anemia diagnoses globally

- For instance, data from global health organizations indicate a rising burden of sickle cell disease and thalassemia in Africa, India, and parts of Southeast Asia, where newborn screening programs and public health initiatives are increasingly identifying affected individuals at an early age

- Hospitals and specialty clinics are expanding diagnostic capabilities with advanced hematological tests such as Coombs test, hemoglobin electrophoresis, and molecular genotyping. As early and accurate diagnosis becomes more widespread, more patients are receiving timely, effective treatment

- Biopharmaceutical companies are actively investing in clinical trials and orphan drug development, bolstered by regulatory incentives and government support in both developed and emerging markets. These efforts are expanding treatment access and driving the introduction of novel therapies

- Increased patient education campaigns, combined with global efforts to enhance rare disease registries and real-world evidence collection, are further contributing to the visibility and prioritization of hemolytic anemia in national healthcare agendas

Restraint/Challenge

“High Cost of Advanced Therapies and Limited Access in Developing Regions”

- Despite ongoing medical advances, the high cost of novel therapies such as gene editing, monoclonal antibodies, and biologics poses a significant challenge to widespread adoption, especially in low- and middle-income countries

- Treatments such as gene therapy and long-term use of targeted biologics often come with substantial price tags, placing them out of reach for many patients and national health systems without insurance or subsidy support. For instance, gene therapies such as exa-cel or LentiGlobin are projected to cost hundreds of thousands of dollars per treatment cycle

- Moreover, limited access to advanced diagnostics and specialty care in rural or underserved areas restricts early detection and intervention, leading to underdiagnosis and delayed treatment in regions where the disease burden is high

- Infrastructure gaps, shortages of trained hematologists, and fragmented supply chains further hinder the availability and consistency of care, particularly in parts of Africa, South Asia, and Latin America

- Addressing these challenges will require coordinated global efforts, including pricing reforms, the introduction of biosimilars, government-backed subsidy programs, and the development of cost-effective alternatives tailored to resource-limited settings. These measures are critical to ensuring equitable access and sustainable market expansion

Hemolytic Anemia Market Scope

The market is segmented on the basis of treatment type, route of administration, diagnosis, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the hemolytic anemia market is segmented into blood transfusions, medicines, plasmapheresis, surgery, blood and marrow stem cell transplants, and others. The blood transfusions segment dominated the market with the largest market revenue share of 35.2% in 2024, primarily due to its critical role in the rapid management of severe hemolytic episodes, particularly in emergency and hospital settings. This treatment remains a frontline approach for both acute and chronic cases across various anemia types, offering immediate restoration of red blood cell counts.

The medicines segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by the increasing availability of targeted drug therapies such as corticosteroids, immunosuppressants, biologics such as rituximab, and disease-modifying agents for conditions such as autoimmune hemolytic anemia and sickle cell disease.

- By Route Of Administration

On the basis of route of administration, the hemolytic anemia market is segmented into oral, parenteral, and others. The parenteral segment held the largest market share of 41.2% in 2024, driven by the widespread use of intravenous medications, blood transfusions, and biologics, which require direct administration into the bloodstream for faster therapeutic action. Hospitals and infusion centers remain the primary sites for this treatment modality due to the need for professional administration and monitoring.

The oral segment is expected to witness the highest CAGR during the forecast period, supported by increased availability of user-friendly oral agents for long-term management, including iron supplements, hydroxyurea, and newly approved oral drugs for sickle cell disease and thalassemia, improving patient adherence and convenience.

- By Diagnosis

On the basis of diagnosis, the hemolytic anemia market is segmented into blood tests, biopsy, urine tests, and others. The blood tests segment dominated with the highest revenue share of 47.8% in 2024, as these non-invasive diagnostic tools—such as the Coombs test, complete blood count (CBC), reticulocyte count, and hemoglobin electrophoresis—are essential for detecting and subtyping hemolytic anemia efficiently and cost-effectively.

The biopsy segment is projected to grow steadily during forecast period due to its critical role in complex and unexplained anemia cases, particularly bone marrow biopsy in evaluating marrow function or ruling out malignancies. However, its growth is moderated by the invasive nature and higher cost compared to blood testing.

- By End User

On the basis of end-users, the hemolytic anemia market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the market with the largest market share of 52.3% in 2024, owing to the comprehensive services offered, including diagnostics, transfusions, parenteral therapy, and acute care, which are central to hemolytic anemia management.

The homecare segment is expected to grow rapidly during the forecast period, driven by increasing availability of at-home treatment options such as oral medications and remote monitoring tools, especially for patients with chronic or stable forms of anemia requiring long-term management outside of clinical settings.

- By Distribution Channel

On the basis of distribution channel, the hemolytic anemia market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment led the market with a revenue share of 38.9% in 2024, given its role in dispensing critical medications, transfusion-related products, and biologics in hospital settings, which are essential for managing moderate to severe anemia cases.

The online pharmacy segment is expected to grow at the fastest during forecast period due to increasing digitalization in healthcare, ease of medication access, rising use of telemedicine, and the growing preference for home delivery of chronic disease medications, especially in urban and tech-savvy populations.

Hemolytic Anemia Market Regional Analysis

- North America dominated the hemolytic anemia market with the largest revenue share of 40.1% in 2024, driven by early adoption of advanced biologics, favorable reimbursement structures, and robust research investments, particularly in the U.S., where clinical trials and orphan drug approvals are accelerating treatment innovations

- Patients in the region benefit from widespread access to advanced treatments such as biologics, stem cell transplants, and specialty care, supported by robust reimbursement frameworks and awareness campaigns

- This dominance is further supported by high healthcare spending, active clinical trials, and strong presence of leading pharmaceutical companies, establishing North America as a key hub for both treatment and research in hemolytic anemia

U.S. Hemolytic Anemia Market Insight

The U.S. hemolytic anemia market captured the largest revenue share of 78.3% in 2024 within North America, driven by the high prevalence of autoimmune diseases, advanced diagnostic capabilities, and access to innovative therapies. The nation benefits from extensive clinical research, a strong pharmaceutical pipeline, and supportive reimbursement policies. The increasing adoption of biologics and precision medicine, combined with the presence of specialized hematology centers, continues to strengthen the market. Public and private investments in rare disease research are also accelerating treatment accessibility and market expansion.

Europe Hemolytic Anemia Market Insight

The Europe hemolytic anemia market is projected to expand at a substantial CAGR throughout the forecast period, fueled by a growing burden of inherited blood disorders and the adoption of personalized medicine. Rising awareness, improved diagnostic pathways, and the availability of novel therapeutics are fostering market growth across the region. Countries such as Germany, France, and Italy are witnessing increased government support and clinical trials, particularly for rare and chronic anemia subtypes. Expansion of specialist care networks and collaborations with biotechnology firms further support the European market’s progression.

U.K. Hemolytic Anemia Market Insight

The U.K. hemolytic anemia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by an increase in national screening programs, awareness campaigns, and healthcare reforms targeting rare diseases. The NHS’s focus on early diagnosis and integration of innovative biologics has enhanced patient access to treatment. Moreover, rising incidence of immune hemolytic anemias and advancements in blood transfusion safety standards contribute significantly to the market’s expansion within the country.

Germany Hemolytic Anemia Market Insight

The Germany hemolytic anemia market is expected to expand at a considerable CAGR during the forecast period, propelled by technological innovation in diagnostics and increased investment in orphan drug development. A strong pharmaceutical landscape, coupled with a focus on early intervention and individualized care, supports the adoption of advanced therapeutics. The country’s comprehensive health insurance system and emphasis on research and development enhance treatment access for both hereditary and acquired forms of hemolytic anemia.

Asia-Pacific Hemolytic Anemia Market Insight

The Asia-Pacific hemolytic anemia market is poised to grow at the fastest CAGR of 25.6% during the forecast period of 2025 to 2032, due to a rising incidence of genetic disorders such as thalassemia and sickle cell anemia. Growth is particularly strong in India, China, and Southeast Asia, where public health initiatives and newborn screening programs are expanding. Increasing healthcare investments, growing awareness, and the presence of low-cost treatment alternatives are improving access to care. Regional biopharma innovation and expanding diagnostic infrastructure also drive market growth

Japan Hemolytic Anemia Market Insight

The Japan hemolytic anemia market is gaining momentum due to an aging population, increased disease surveillance, and strong public health infrastructure. The country's adoption of advanced therapeutics, including monoclonal antibodies and gene therapy trials, is bolstering treatment outcomes. Integration of hemolytic anemia care into national health insurance coverage, along with robust regulatory support for orphan drugs, contributes to consistent market expansion. Research into autoimmune hemolytic conditions is also on the rise.

India Hemolytic Anemia Market Insight

The India hemolytic anemia market accounted for the largest market revenue share in Asia Pacific in 2024, driven by the country’s large population base, genetic predisposition to blood disorders, and expansion of government-led healthcare schemes. With rising awareness and the availability of cost-effective treatment options, including generics and biosimilars, the market is rapidly evolving. India’s growing biopharmaceutical sector, coupled with public-private partnerships and the push for affordable diagnostics, continues to strengthen market access and coverage.

Hemolytic Anemia Market Share

The hemolytic anemia industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Teva Pharmaceutical Industries Ltd.(Ireland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Fresenius SE & Co. KGaA (Germany)

- Lupin (India)

- ViforPharma Ltd. (Switzerland)

- AMAG Pharmaceuticals (U.S.)

- Akebia Therapeutics, INC. (U.S.)

- CHO-A Pharmaceutical CO., LTD. (South Korea)

- Orion Corporation (Finland)

- Pharmacosmos A/S (Denmark)

- Shield Therapeutics (U.K.)

- Advanz Pharmaceutical (U.K.)

- Alkem Labs (India)

- Zydus Cadila (India)

- Hikma Pharmaceuticals PLC (U.K.)

What are the Recent Developments in Global Hemolytic Anemia Market?

- In April 2023, Sanofi announced promising results from its Phase 3 clinical trial evaluating sutimlimab-jome in patients with cold agglutinin disease (CAD), a rare autoimmune hemolytic anemia. The trial demonstrated significant reductions in hemolysis and transfusion needs, underscoring the potential of complement inhibition in addressing CAD symptoms. These findings reinforce Sanofi’s leadership in rare hematologic disorders and its ongoing investment in immunohematology innovations

- In March 2023, Apellis Pharmaceuticals received expanded regulatory approval in the European Union for Empaveli (pegcetacoplan) for the treatment of paroxysmal nocturnal hemoglobinuria (PNH), a rare form of hemolytic anemia. The label extension follows strong clinical efficacy data showing durable hemoglobin stabilization and transfusion avoidance. This move strengthens Apellis’ global presence and highlights the increasing acceptance of complement-targeting therapies in rare anemia treatment

- In March 2023, Grifols S.A. introduced a new plasma-derived therapy under investigation for autoimmune hemolytic anemia, leveraging its expertise in immunoglobulin and plasma protein therapeutics. The company announced a new clinical trial site expansion across North America and Europe, aimed at accelerating development timelines. Grifols’ innovation in plasma therapies reflects the growing demand for targeted, well-tolerated treatment options for chronic hemolytic conditions

- In February 2023, Agios Pharmaceuticals, Inc. reported positive long-term data from its pivotal Phase 2 study of mitapivat in adults with pyruvate kinase deficiency (PKD), a hereditary hemolytic anemia. The data demonstrated sustained hemoglobin improvements and a favorable safety profile. Agios also revealed plans to explore mitapivat’s potential in thalassemia and sickle cell disease, marking a strategic expansion into broader hemolytic anemia indications and reinforcing its commitment to genetically driven hematologic disorders

- In January 2023, Regeneron Pharmaceuticals and Alnylam Pharmaceuticals expanded their RNA interference (RNAi) collaboration to include investigational programs targeting rare blood disorders, including autoimmune hemolytic anemia. The collaboration aims to harness Alnylam’s RNAi platform to silence disease-driving genes, while leveraging Regeneron’s expertise in antibody therapies. This joint initiative highlights a trend toward precision medicine approaches in treating rare hemolytic anemias, focusing on sustainable, long-term disease control

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.