Global Hereditary Angioedema Therapeutic Market

Market Size in USD Billion

USD

4.25 Billion

USD

8.29 Billion

2024

2032

USD

4.25 Billion

USD

8.29 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.25 Billion | |

| USD 8.29 Billion | |

| % | |

|

Hereditary Angioedema Therapeutic Market Size

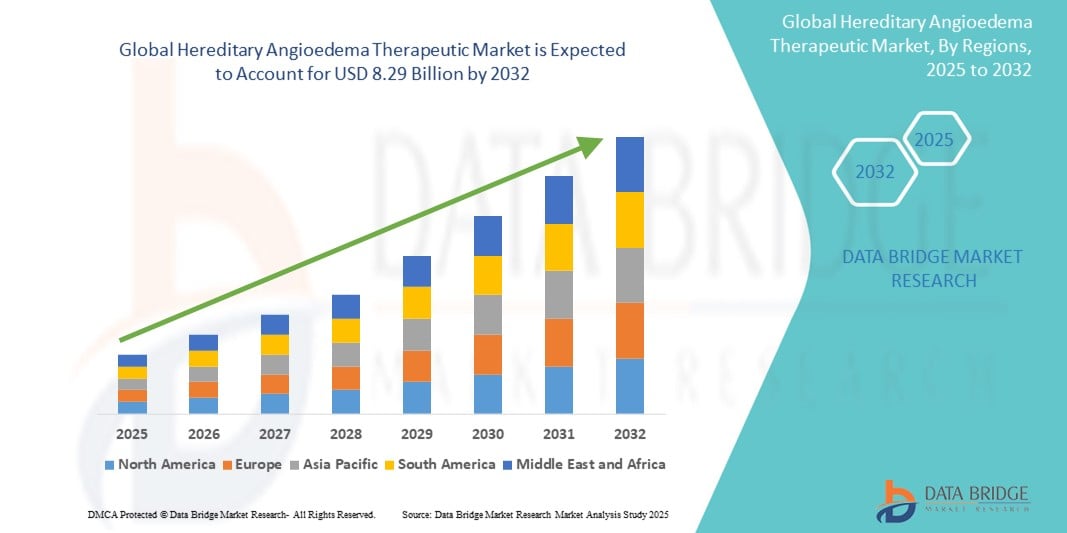

- The global hereditary angioedema therapeutic market size was valued at USD 4.25 billion in 2024 and is expected to reach USD 8.29 billion by 2032, at a CAGR of 8.72% during the forecast period

- The market growth is primarily driven by increasing awareness and diagnosis rates of HAE, along with the rising availability of targeted therapies and prophylactic treatment options

- Furthermore, the emergence of novel biologics and next-generation treatment modalities aimed at reducing attack frequency and severity is significantly improving patient outcomes and driving higher demand. These combined advancements are rapidly shaping a robust therapeutic landscape, thereby propelling the market's expansion

Hereditary Angioedema Therapeutic Market Analysis

- Hereditary angioedema (HAE) therapies, addressing unpredictable and potentially severe swelling episodes, are increasingly vital components of rare disease treatment protocols due to their targeted action, improved efficacy, and role in enhancing patient quality of life across both acute and preventive care settings

- The escalating demand for HAE therapeutics is primarily fueled by rising awareness among healthcare professionals and patients, increasing diagnosis rates, and expanding availability of advanced biologics and small-molecule therapies tailored to individual patient needs

- North America dominates the hereditary angioedema therapeutic market with the largest revenue share of 74% in 2024, characterized by strong diagnostic capabilities, high healthcare expenditure, and a concentrated presence of leading biopharmaceutical companies

- Asia-Pacific is expected to be the fastest growing region in the hereditary angioedema therapeutic market during the forecast period due to growing awareness of rare diseases, increasing healthcare access, and favorable regulatory developments supporting the introduction of novel treatments

- C1-esterase inhibitor segment dominates the hereditary angioedema therapeutic market with a market share of 52.7% in 2024, driven by its proven efficacy in both acute and prophylactic treatment, along with its well-established safety profile and widespread clinical adoption

Report Scope and Hereditary Angioedema Therapeutic Market Segmentation

|

Attributes |

Hereditary Angioedema Therapeutic Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hereditary Angioedema Therapeutic Market Trends

“Advancements in Targeted and Prophylactic Therapies”

- A significant and accelerating trend in the global hereditary angioedema (HAE) therapeutic market is the shift toward targeted and long-term prophylactic treatments that significantly reduce the frequency and severity of HAE attacks, improving patient outcomes and quality of life

- For instance, therapies such as Takeda’s Takhzyro (lanadelumab), a subcutaneous monoclonal antibody, offer sustained prevention of HAE attacks with biweekly or monthly dosing, while BioCryst’s Orladeyo (berotralstat) provides the convenience of once-daily oral prophylaxis, appealing to patients seeking needle-free alternatives

- These advanced treatments target specific pathways such as plasma kallikrein inhibition or C1-esterase deficiency, offering a precision medicine approach that enhances treatment efficacy and minimizes side effects. The development of gene therapies is also gaining traction, with ongoing clinical trials exploring potential long-term or curative options for HAE patients

- Moreover, biopharmaceutical companies are actively investing in pipeline expansion and innovative delivery mechanisms such as subcutaneous self-administration and oral formulations to further simplify disease management

- This trend is fundamentally reshaping expectations for HAE care, with patients and providers increasingly prioritizing therapies that offer convenience, long-term protection, and improved safety. As a result, companies such as CSL Behring and Pharvaris are advancing next-generation HAE treatments that align with these evolving demands

- The growing preference for targeted, low-burden prophylactic therapies is rapidly transforming the therapeutic landscape, driving higher adoption rates and shaping the future direction of the hereditary angioedema market globally

Hereditary Angioedema Therapeutic Market Dynamics

Driver

“Rising Diagnosis Rates and Demand for Long-Term Preventive Therapies”

- The increasing rate of diagnosis of hereditary angioedema (HAE) due to growing awareness among healthcare providers and patients, combined with the escalating demand for long-term prophylactic treatment, is a significant driver for the expanding HAE therapeutic market

- For instance, in March 2024, BioCryst Pharmaceuticals expanded global access to its oral prophylactic therapy Orladeyo, aiming to improve availability in key emerging markets. Such initiatives by major companies are expected to drive the market growth during the forecast period

- As more patients are accurately diagnosed earlier, the need for therapies that prevent debilitating HAE attacks is growing, encouraging the adoption of novel biologics and oral treatments that offer improved convenience and sustained protection

- Furthermore, the availability of user-friendly and less invasive delivery methods, such as subcutaneous injections and once-daily oral pills, is contributing to improved adherence and quality of life for patients

- The growing emphasis on proactive disease management, supported by robust patient advocacy, education programs, and healthcare infrastructure improvements, is significantly boosting demand for advanced and accessible HAE therapies across both developed and emerging markets

Restraint/Challenge

“High Treatment Costs and Limited Awareness in Emerging Markets”

- The high cost of hereditary angioedema (HAE) therapies, especially biologics and novel prophylactic treatments, remains a significant challenge limiting broader market access, particularly in developing regions where healthcare budgets and insurance coverage are constrained

- For instance, the expensive nature of treatments such as C1-esterase inhibitors and monoclonal antibodies can restrict patient access and delay therapy initiation, contributing to under-treatment or reliance on less effective options

- Addressing affordability through patient assistance programs, expanded insurance reimbursement, and the development of cost-effective therapies is crucial for improving market penetration. Companies such as CSL Behring and Takeda are increasingly focusing on such initiatives to enhance accessibility

- Furthermore, limited disease awareness and diagnostic capabilities in emerging markets pose additional hurdles, resulting in delayed diagnosis and treatment, which negatively impact patient outcomes and market growth

- While advancements in treatment options continue, overcoming cost barriers and increasing education among healthcare providers and patients will be vital to driving sustained adoption and expanding the global hereditary angioedema therapeutic market

- Overcoming these challenges through improved affordability initiatives, expanded disease awareness programs, and enhanced healthcare infrastructure in emerging markets will be vital for sustained growth in the hereditary angioedema therapeutic market

Hereditary Angioedema Therapeutic Market Scope

The market is segmented on the basis of type, drug class, application, route of administration, end user, and distribution channel.

- By Type

On the basis of type, the hereditary angioedema therapeutic market is segmented into Type I HAE, Type II HAE, and Type III HAE. The Type I HAE segment dominates the largest market revenue share in 2024, driven by its higher global prevalence and early clinical recognition, which leads to a greater number of diagnosed and treated patients. Type I accounts for approximately 85% of all HAE cases, and the availability of established treatment protocols and awareness among healthcare professionals supports its dominance.

The Type III HAE segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising awareness, advances in genetic testing, and increased diagnosis rates. Research developments and emerging targeted therapies are expanding treatment opportunities for this less common subtype, which was historically underdiagnosed.

- By Drug Class

On the basis of drug class, the market is segmented into C1-esterase inhibitors, bradykinin B2 receptor antagonists, kallikrein inhibitors, and others. The C1-esterase inhibitors segment dominates the largest market share of 52.7% in 2024, driven by their established efficacy, broad clinical usage for both acute and prophylactic management, and long-standing approval in major healthcare markets. These therapies remain the cornerstone of HAE treatment, widely recommended in clinical guidelines.

The kallikrein inhibitors segment is projected to experience the fastest growth during the forecast period, propelled by innovative therapies offering oral or subcutaneous routes, improved patient adherence, and targeted inhibition mechanisms. These advantages position kallikrein inhibitors as a preferred alternative for patients seeking convenient and effective management options.

- By Application

On the basis of application, the market is segmented into treatment and prophylaxis. The treatment segment holds the largest share in 2024, attributed to the immediate need for rapid intervention during HAE attacks and the widespread use of on-demand therapies. Acute treatment is essential in preventing complications, thus maintaining consistent demand.

The prophylaxis segment is expected to witness the fastest growth over the forecast period, driven by increased preference for long-term control, growing availability of preventive drugs, and patient demand for therapies that reduce the frequency and severity of attacks. Advances in prophylactic options also reduce healthcare burden and improve quality of life

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and injectable. The injectable segment dominates the market in 2024 due to the historical use of intravenous and subcutaneous delivery in HAE therapies. Injectable products, especially biologics, have demonstrated high efficacy and are widely available in hospital and home care settings.

The oral segment is projected to grow at the fastest rate from 2025 to 2032, supported by the introduction of novel oral prophylactic agents. These offer convenience, eliminate the need for needles, and promote patient compliance, particularly among pediatric and elderly populations

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, home healthcare, and others. The hospitals segment currently dominates the market, primarily due to their central role in diagnosis, acute intervention, and specialized treatment administration. Hospital-based therapies remain critical during severe attacks and initial treatment phases.

The home healthcare segment is anticipated to grow at the fastest rate, driven by increasing adoption of self-administered therapies, greater availability of home-use drug delivery systems, and the shift toward personalized, home-based care models that enhance patient comfort and adherence.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment holds the largest market share in 2024, supported by the centralized distribution of specialty therapies, especially injectables, through healthcare institutions and in-patient settings.

The online pharmacy segment is expected to exhibit the fastest growth rate over the forecast period due to the rise in digital health platforms, teleconsultations, and e-prescriptions. The convenience of home delivery and increasing access in remote areas are also fueling this growth, particularly among younger and tech-savvy patients.

Hereditary Angioedema Therapeutic Market Regional Analysis

- North America dominates the hereditary angioedema therapeutic market with the largest revenue share of 74% in 2024, driven by strong diagnostic capabilities, high healthcare expenditure, and a concentrated presence of leading biopharmaceutical companies

- Patients in the region highly value the availability of advanced therapies, rapid access to healthcare services, and the strong support infrastructure for managing chronic and rare conditions

- This widespread adoption is further supported by high healthcare expenditure, a well-established regulatory framework for orphan drugs, and the growing preference for both acute and prophylactic treatment options, establishing HAE therapies as a critical solution across hospitals and homecare settings

U.S. Hereditary Angioedema Therapeutic Market Insight

The U.S. hereditary angioedema (HAE) therapeutic market captured the largest revenue share in North America in 2024, driven by strong clinical awareness, well-established healthcare infrastructure, and the early availability of FDA-approved treatments. Patients benefit from timely diagnosis and access to both prophylactic and on-demand therapies. The market is further fueled by increasing patient education, the presence of patient support groups, and growing participation in clinical trials. Robust insurance coverage and orphan drug policies are also instrumental in ensuring treatment accessibility.

Europe Hereditary Angioedema Therapeutic Market Insight

The Europe hereditary angioedema therapeutic market is projected to grow at a substantial CAGR throughout the forecast period, driven by rising awareness of rare genetic conditions and improved access to innovative therapies across major EU countries. Countries are increasingly integrating HAE treatment into national rare disease frameworks, supported by healthcare providers advocating early genetic screening. Expanded regulatory support for orphan drugs and increased availability of C1-inhibitors and kallikrein inhibitors are contributing to widespread therapeutic adoption across both public and private healthcare settings.

U.K. Hereditary Angioedema Therapeutic Market Insight

The U.K. hereditary angioedema therapeutic market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by national healthcare policies that encourage access to orphan therapies. Growing diagnosis rates, combined with the NHS's structured rare disease plans, are fostering better treatment coverage. Public awareness campaigns and specialized treatment centers are playing a pivotal role in improving patient outcomes. The UK’s commitment to research and cross-border collaborations is also expected to accelerate therapy uptake.

Germany Hereditary Angioedema Therapeutic Market Insight

The Germany hereditary angioedema therapeutic market is expected to expand at a considerable CAGR, driven by robust healthcare funding, widespread access to specialized care, and the country's emphasis on precision medicine. Germany’s advanced genetic screening protocols and early diagnosis initiatives are supporting timely therapeutic interventions. The presence of global pharmaceutical companies and continuous R&D investment into rare disease drugs position Germany as a key growth market within the region.

Asia-Pacific Hereditary Angioedema Therapeutic Market Insight

The Asia-Pacific hereditary angioedema therapeutic market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare access, rising diagnosis rates, and improving affordability of targeted therapies. Governments in countries such as China, Japan, and South Korea are investing in rare disease treatment infrastructure and promoting early genetic screening programs. Increased collaborations between local healthcare systems and global pharmaceutical companies are also boosting the regional market's development.

Japan Hereditary Angioedema Therapeutic Market Insight

The Japan hereditary angioedema therapeutic market is gaining momentum due to the country’s strong pharmaceutical innovation base and well-organized healthcare system. With an emphasis on managing rare genetic disorders, Japan is accelerating HAE therapy approvals and broadening access to treatment. The presence of advanced hospitals and increasing awareness among physicians are driving patient adherence. Japan’s aging population also supports the demand for specialized, chronic condition management, contributing to consistent market growth.

India Hereditary Angioedema Therapeutic Market Insight

The India hereditary angioedema therapeutic market is expected to emerge as a high-potential segment in Asia Pacific, attributed to the country’s improving rare disease awareness, growing middle-class population, and expanding healthcare infrastructure. As India ramps up its efforts towards national rare disease policy implementation, access to HAE diagnosis and treatment is expected to improve significantly. Collaboration with international pharmaceutical companies and local production of cost-effective therapies are key factors driving market expansion.

Hereditary Angioedema Therapeutic Market Share

The hereditary angioedema therapeutic industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company Limited (Japan)

- CSL (Australia)

- BioCryst Pharmaceuticals, Inc. (U.S.)

- Pharming (Netherlands)

- Ionis Pharmaceuticals (U.S.)

- Novartis AG (Switzerland)

- CENTOGENE N.V. (Germany)

- Sanofi (France)

- KalVista Pharmaceuticals (U.S.)

- Pfizer Inc. (U.S.)

- GSK plc. (U.K.)

- AstraZeneca (U.K.)

- Medtronic. (U.S.)

- Lilly (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Amgen Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Incyte (U.S.)

- Bayer AG (Germany)

Latest Developments in Global Hereditary Angioedema Therapeutic Market

- In January 2024, a groundbreaking gene therapy trial demonstrated remarkable success in treating hereditary angioedema (HAE), offering hope for a potential cure. Utilizing CRISPR technology, the therapy targets the kallikrein gene responsible for HAE attacks. Participants in the phase-one trial experienced significant symptom relief, with many remaining attack-free for 18 months post-treatment. This advancement underscores the transformative potential of gene editing in managing rare genetic disorders

- In August 2023, Takeda Pharmaceutical Company announced that the U.S. FDA approved an expanded indication for TAKHZYRO (lanadelumab-flyo), allowing its use in children aged 2 years and older for the prevention of HAE attacks. This approval marks a significant step in pediatric HAE management, providing younger patients with access to a proven prophylactic treatment

- In November 2023, BioCryst Pharmaceuticals presented new real-world data highlighting the efficacy of ORLADEYO (berotralstat) in reducing HAE attack rates among patients with normal C1-inhibitor levels. The findings revealed a median attack rate of zero over a 12-month period, emphasizing ORLADEYO's potential as a reliable prophylactic option for this patient subgroup

- In April 2023, BioCryst Pharmaceuticals shared long-term data from the APeX-S clinical trial, demonstrating that patients treated with ORLADEYO maintained consistently high attack-free status over 96 weeks. The study encompassed diverse patient demographics, reinforcing the drug's broad applicability and sustained effectiveness in HAE prophylaxis.

- In February 2025, BioCryst Pharmaceuticals announced positive interim results from the APeX-P trial, evaluating ORLADEYO in pediatric patients aged 2 to <12 years. The oral granule formulation was well-tolerated and led to early and sustained reductions in monthly HAE attack rates, highlighting its promise as a pediatric-friendly prophylactic treatment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.