Global Hypertrophic And Keloid Scar Treatment Market

Market Size in USD Billion

USD

2.19 Billion

USD

4.66 Billion

2025

2033

USD

2.19 Billion

USD

4.66 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.19 Billion | |

| USD 4.66 Billion | |

| % | |

|

Hypertrophic and Keloid Scar Treatment Market Size

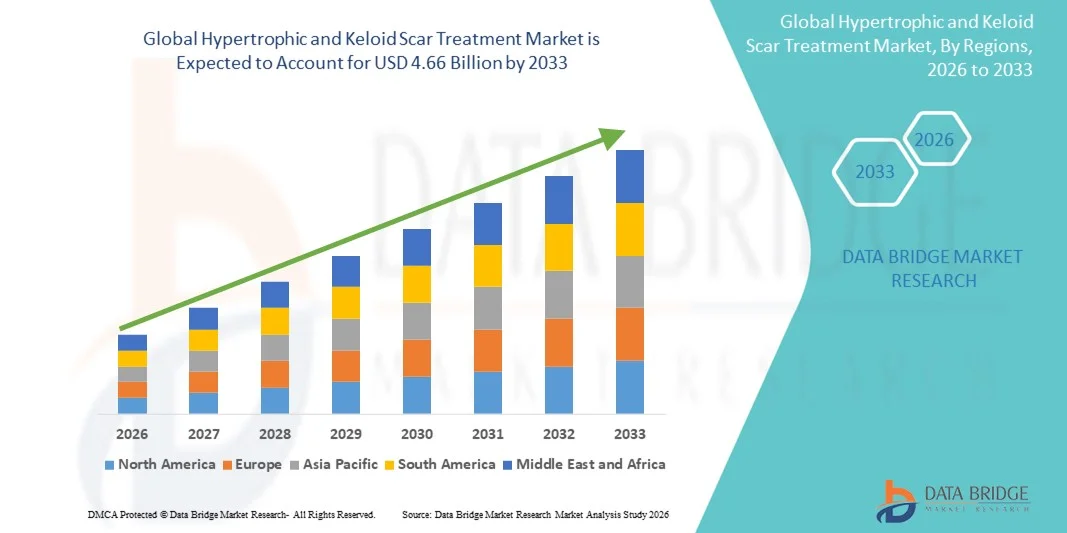

- The global hypertrophic and keloid scar treatment market size was valued at USD 2.19 billion in 2025 and is expected to reach USD 4.66 billion by 2033, at a CAGR of 9.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of skin injuries, surgical procedures, burns, and acne, which contribute to the formation of hypertrophic and keloid scars, driving demand for effective treatment solutions

- Furthermore, rising awareness about advanced dermatological therapies, growing adoption of minimally invasive procedures, and the development of innovative treatments such as laser therapy, corticosteroid injections, silicone gels, and pressure therapy are accelerating the uptake of Hypertrophic and Keloid Scar Treatment solutions, thereby significantly boosting the industry's growth

Hypertrophic and Keloid Scar Treatment Market Analysis

- Hypertrophic and keloid scar treatment solutions, including topical gels, corticosteroid injections, laser therapy, and pressure therapy, are increasingly vital components of modern dermatological and cosmetic care due to their effectiveness in minimizing scar formation, improving appearance, and enhancing patient quality of life

- The escalating demand for hypertrophic and keloid scar treatments is primarily fueled by the growing prevalence of skin injuries, burns, surgical procedures, and acne, coupled with rising awareness of advanced dermatological therapies and minimally invasive procedures

- North America dominated the hypertrophic and keloid scar treatment market with the largest revenue share of 38% in 2025, supported by advanced healthcare infrastructure, high adoption of dermatological treatments, strong awareness of scar management therapies, and the presence of leading skincare and pharmaceutical companies in the region

- Asia-Pacific is expected to be the fastest growing region in the hypertrophic and keloid scar treatment market during the forecast period due to increasing healthcare expenditure, rising prevalence of skin injuries, growing urbanization, and expanding access to advanced dermatological treatment facilities in countries such as China, India, and Japan

- The intralesional corticosteroid injection segment dominated the largest market revenue share of 46.3% in 2025, as it remains the first-line treatment for both hypertrophic and keloid scars due to high efficacy, ease of use, and minimal downtime

Report Scope and Hypertrophic and Keloid Scar Treatment Market Segmentation

|

Attributes |

Hypertrophic and Keloid Scar Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Smith & Nephew plc (U.K.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hypertrophic and Keloid Scar Treatment Market Trends

Rising Adoption of Advanced Minimally Invasive Therapies

- A key trend in the global hypertrophic and keloid scar treatment market is the increasing preference for minimally invasive and combination therapies, including intralesional corticosteroids, laser therapy, silicone gels, and cryotherapy. These therapies provide enhanced efficacy with reduced downtime and scarring, making them highly attractive to patients seeking cosmetic and functional improvement

- For instance, in June 2023, a multicenter study in the U.S. demonstrated that combining intralesional corticosteroid injections with fractional CO₂ laser therapy significantly reduced scar thickness and redness compared to monotherapy. This study highlighted the clinical effectiveness of combination treatment strategies in challenging cases

- Clinicians are increasingly adopting evidence-based protocols to personalize treatment based on scar type, location, and patient skin type, thereby improving outcomes and patient satisfaction

- There is also growing integration of adjunct therapies such as pressure therapy, silicone sheeting, and topical anti-fibrotic agents to enhance efficacy

- The increasing focus on post-surgical scar management in hospitals and dermatology clinics is further driving adoption

- Technological advances in laser devices and topical formulations are supporting better clinical outcomes, encouraging wider use

- Patients are increasingly aware of the cosmetic and functional implications of hypertrophic and keloid scars, driving demand for effective therapies

- The trend toward outpatient, clinic-based scar management is making treatments more accessible, reducing hospital stays and improving patient convenience

- Regional adoption is increasing in Asia-Pacific due to higher prevalence rates of keloid formation in darker skin populations

- Growing collaborations between dermatology clinics and plastic surgery centers are improving patient access to multimodal treatment

- Research into genetic and molecular mechanisms of abnormal scarring is influencing development of targeted therapeutics

- The market is also benefiting from rising insurance coverage for post-surgical scar management in certain countries, boosting accessibility

- Overall, the shift toward effective, minimally invasive, and patient-centric treatment protocols is reshaping the scar treatment landscape globally

Hypertrophic and Keloid Scar Treatment Market Dynamics

Driver

Rising Incidence of Hypertrophic and Keloid Scars

- The increasing prevalence of hypertrophic and keloid scars due to surgical procedures, trauma, burns, and acne is a major driver of market growth

- For instance, in March 2024, a study published in Dermatologic Surgery reported that nearly 40% of patients undergoing orthopedic and cosmetic surgeries in North America developed hypertrophic or keloid scars, emphasizing the need for effective management options

- Rising awareness among patients and healthcare providers about early intervention to prevent scar progression is driving demand for timely treatment

- Expansion of dermatology clinics, plastic surgery centers, and outpatient care facilities contributes to higher accessibility and adoption

- Insurance reimbursement policies in certain regions for post-surgical scar care encourage patients to seek professional treatment rather than home remedies. The increasing use of combination therapies and new treatment modalities, such as laser-assisted drug delivery and biologics, further stimulates demand

- Patient preference for non-invasive or minimally invasive procedures, due to shorter recovery and fewer complications, is also driving growth. High cosmetic consciousness and the psychological impact of visible scars are motivating patients to seek treatment

- Growth in medical tourism in regions like Asia-Pacific and the Middle East is supporting adoption of advanced therapies. Education campaigns by dermatology associations highlighting the long-term benefits of scar management encourage early and proactive treatment

- Research investments in scar biology and novel therapeutic agents are attracting attention from clinicians and patients alike. Overall, the increasing patient population, awareness, and clinical focus on effective scar management act as significant market growth drivers

Restraint/Challenge

High Treatment Costs and Variable Efficacy

- The high cost of advanced scar therapies, including laser treatment, biologics, and combination therapy regimens, can restrict adoption, especially in price-sensitive regions

- For instance, in July 2023, a survey of dermatology clinics in Europe highlighted that patient out-of-pocket expenses for multi-session combination therapies exceeded USD 2,000 on average, limiting accessibility for some populations

- Efficacy of treatments varies depending on scar type, size, and patient genetics, creating uncertainty among patients regarding outcomes. Some patients experience recurrence even after multiple treatment sessions, impacting perceived value

- Limited availability of specialized dermatologists and plastic surgeons in rural areas constrains access to advanced therapies. Awareness gaps regarding appropriate treatment protocols among general practitioners may delay referrals to specialists

- Side effects such as skin atrophy, pigmentation changes, or pain during procedures can discourage patients. Insurance coverage for certain scar therapies remains inconsistent across regions, further challenging affordability

- Standardization of treatment protocols is still evolving, leading to variability in clinical outcomes. Patient adherence to multi-session treatment regimens can be low due to time, cost, or discomfort

- Addressing these challenges through patient education, development of more cost-effective therapies, and improved clinical guidance is critical

- Despite high costs and variable efficacy, ongoing clinical research and innovations in treatment modalities are expected to gradually reduce these barriers, ensuring long-term market growth

Hypertrophic and Keloid Scar Treatment Market Scope

The market is segmented on the basis of type, product type, treatment, end-users, and distribution channel.

- By Type

On the basis of type, the Hypertrophic and Keloid Scar Treatment market is segmented into hypertrophic and keloid scars. The keloid scar segment dominated the largest market revenue share of 57.4% in 2025, driven by the higher prevalence of keloid formation in darker skin populations, genetic susceptibility, and the greater cosmetic and functional concern associated with these scars. Keloid scars often require complex treatment protocols, including combination therapies, which increase market consumption. Clinics and hospitals are increasingly focusing on personalized treatment plans for keloid management, incorporating laser therapy, corticosteroid injections, and surgical options to improve patient outcomes. Awareness campaigns highlighting early intervention and long-term efficacy further drive demand. Rising incidences due to post-surgical complications and trauma support segment growth. Patient preference for clinically proven therapies over home remedies strengthens this trend. Expansion of dermatology and plastic surgery centers globally ensures better accessibility for keloid treatments. Increasing adoption in Asia-Pacific and African regions due to higher prevalence of keloid scars also contributes to revenue growth. Research into innovative therapies such as biologics and novel drug delivery systems is further expanding keloid treatment options. Overall, the segment remains the market leader due to a combination of higher prevalence, complexity of care, and strong clinical adoption.

The hypertrophic scar segment is anticipated to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by rising post-surgical procedures, trauma cases, and burn injuries. Hypertrophic scars often require early intervention to prevent progression, encouraging use of corticosteroids, silicone dressings, and laser therapy. Increased awareness among patients and clinicians regarding aesthetic and functional outcomes fuels growth. Technological advances in non-invasive treatment options make management more accessible. The rise in cosmetic and orthopedic surgeries contributes to the segment’s rapid adoption. Regional expansion in emerging economies with growing healthcare infrastructure supports market penetration. Enhanced patient education on post-surgical scar prevention also boosts segment uptake. Combination therapy adoption in hypertrophic scars is rising due to improved efficacy. The integration of outpatient care and specialized dermatology services enhances accessibility and treatment compliance. Improved insurance coverage for post-surgical scar management in certain regions promotes affordability. Growth in the use of minimally invasive techniques supports sustained market expansion. The segment benefits from ongoing clinical research and development of innovative topical and injectable formulations.

- By Product Type

On the basis of product type, the market is segmented into topical products, laser products, injectable products, and others. The injectable products segment dominated the largest market revenue share of 42.6% in 2025, primarily driven by widespread use of intralesional corticosteroid injections for both hypertrophic and keloid scars. Injectable therapies offer targeted treatment, high efficacy, and ease of administration in clinic settings. Clinicians prefer injectable formulations for severe or refractory scars due to their proven effectiveness. Adoption of combination therapy protocols including injections plus laser or cryotherapy further strengthens demand. Awareness among dermatologists and plastic surgeons about optimized dosing schedules improves patient outcomes. Clinics and hospitals increasingly stock injectable solutions for timely intervention. Research supporting long-term scar reduction via injections enhances clinician confidence. Patient preference for minimally invasive, outpatient-administered injections encourages adoption. Cost-effectiveness relative to surgical excision supports higher usage. Training programs for healthcare professionals on injectable therapies expand accessibility. Rising global prevalence of scars requiring medical intervention contributes to market dominance. High patient satisfaction and repeat treatment cycles also sustain revenue growth.

The laser products segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, owing to technological advancements in fractional CO₂, pulsed dye, and Nd:YAG laser systems. Laser therapy is increasingly preferred due to its non-invasive nature and ability to reduce scar redness, thickness, and pigmentation. Rising demand for combination therapy including lasers plus topical agents accelerates adoption. Availability of outpatient laser centers and portable devices supports accessibility. Patients are motivated by shorter recovery times and aesthetic improvements. Insurance reimbursement for certain laser procedures encourages uptake in developed markets. Expanding cosmetic dermatology clinics in Asia-Pacific and Middle East regions drive segment growth. Growing awareness campaigns about post-surgical scar management promote laser use. Clinical evidence supporting long-term efficacy boosts clinician confidence. Increasing investments in R&D for more precise and effective laser systems fuel adoption. Rising demand for skin rejuvenation and aesthetic improvement in post-trauma scars complements segment growth. Adoption in both adult and pediatric populations enhances market potential.

- By Treatment

On the basis of treatment, the market is segmented into cryotherapy, surgical excision, pressure dressings, intralesional 5-fluorouracil, superficial X-ray, intralesional corticosteroid injection, and others. The intralesional corticosteroid injection segment dominated the largest market revenue share of 46.3% in 2025, as it remains the first-line treatment for both hypertrophic and keloid scars due to high efficacy, ease of use, and minimal downtime. Clinicians widely recommend corticosteroid injections for moderate-to-severe scars, particularly in outpatient and clinic settings. Combination therapy involving corticosteroids plus laser or silicone sheeting further increases adoption. Patient preference for minimally invasive procedures with proven results drives segment leadership. Availability in hospitals, clinics, and dermatology centers globally ensures accessibility. Clinical guidelines support early intervention with corticosteroids, improving outcomes. Expansion of dermatology and plastic surgery facilities strengthens market penetration. Technological improvements in injection devices allow precise dosage and reduced discomfort. Research demonstrating reduced recurrence rates further enhances clinician confidence. Growing patient awareness about cosmetic appearance motivates treatment uptake. Pharmaceutical innovations in corticosteroid formulations support better compliance and efficacy. The segment remains dominant due to its proven clinical efficacy, convenience, and broad acceptance.

The cryotherapy segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by adoption in outpatient settings for small, localized scars and as an adjunct therapy in combination treatments. Cryotherapy offers a non-invasive, cost-effective option for scar reduction. Patient acceptance is high due to minimal discomfort and rapid recovery. Rising awareness about post-trauma scar management and preventive care encourages use. Availability of portable cryotherapy devices supports adoption in clinics. Integration with other treatments, including corticosteroids and laser therapy, enhances efficacy. Growth in dermatology and plastic surgery centers in emerging economies expands market penetration. Clinical evidence highlighting reduced recurrence and improved scar aesthetics boosts confidence. Use in pediatric and adult populations increases applicability. Training programs for clinicians enhance technique adoption. Awareness campaigns emphasizing early intervention further stimulate growth. Overall, cryotherapy adoption is accelerating due to affordability, efficacy, and minimal downtime.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The hospital segment dominated the largest market revenue share of 55.8% in 2025, driven by complex scar cases, availability of trained specialists, and access to advanced treatment modalities. Hospitals provide comprehensive care including combination therapies, laser treatment, and injectable administration. Rising post-surgical scar cases and trauma patients support hospital adoption. Insurance coverage for hospital-based treatments encourages patients to seek care. Hospitals are investing in specialized dermatology and plastic surgery units to meet growing demand. Research and clinical trials conducted in hospitals enhance treatment credibility. Hospital pharmacies ensure timely availability of corticosteroids, biologics, and laser consumables. Hospitals serve as referral centers for severe scar management, increasing patient inflow. Expansion of healthcare infrastructure globally further supports hospital segment dominance. Collaboration with cosmetic and reconstructive specialists enhances treatment outcomes. Patient confidence in hospital-administered treatments reinforces market leadership. Overall, hospitals remain the key treatment hub due to accessibility, expertise, and advanced care offerings.

The clinic segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2033, due to growing outpatient visits and early intervention trends. Clinics provide easy access, shorter waiting times, and focused scar management services. Rising awareness encourages people to seek early consultation. Expansion of specialized dermatology and cosmetic clinics supports this growth. Adoption of portable diagnostic and treatment devices in clinics increases demand. Clinics are convenient for follow-up visits and multiple treatment sessions. Increased patient preference for outpatient minimally invasive procedures fuels adoption. Regional penetration in urban and suburban areas enhances accessibility. Growing demand for aesthetic care drives clinic-based treatment. Availability of combination therapies in clinics supports comprehensive care. Clinics offer competitive pricing relative to hospitals, boosting affordability. Increased use of telemedicine and virtual consultations promotes patient engagement. Overall, clinics are emerging as a fast-growing end-user channel due to accessibility, affordability, and patient-centric care.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 59.1% in 2025, driven by centralized procurement for inpatient and outpatient scar management. Hospitals and specialized clinics rely on hospital pharmacies for timely access to injectable corticosteroids, biologics, and laser consumables. Bulk purchasing ensures cost efficiency. Regulatory compliance and quality assurance further support hospital pharmacy dominance. Hospital pharmacies are preferred for complex and combination therapies. Availability of trained pharmacists to guide proper dosing enhances reliability. Expansion of hospital networks globally strengthens market penetration. High patient volume in hospitals ensures consistent demand. Hospitals can stock a range of products for different scar types. Clinical trials and research partnerships reinforce hospital pharmacy usage. Patients trust hospital pharmacies for authentic medications and consumables. Overall, hospital pharmacies remain the dominant channel due to accessibility, trust, and comprehensive supply.

The online pharmacy segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, driven by digital healthcare growth and patient preference for home delivery. Online platforms offer convenience, quick access, and doorstep delivery, particularly for topical products. Rising smartphone usage and internet penetration support this trend. Increased preference for remote purchasing boosts demand. Subscription and refill programs encourage regular use. Competitive pricing and promotional offers accelerate adoption. Online access improves availability for patients in remote or underserved areas. Digital marketing campaigns by pharmaceutical brands raise awareness. Patients increasingly trust verified online pharmacies for quality products. Ease of comparison across brands and products drives selection. Teleconsultations integrated with online ordering enhance patient convenience. Overall, online pharmacies are growing rapidly due to accessibility, affordability, and convenience.

Hypertrophic and Keloid Scar Treatment Market Regional Analysis

- North America dominated the hypertrophic and keloid scar treatment market with the largest revenue share of 38% in 2025

- Supported by advanced healthcare infrastructure, high adoption of dermatological treatments, strong awareness of scar management therapies

- The presence of leading skincare and pharmaceutical companies in the region

U.S. Hypertrophic and Keloid Scar Treatment Market Insight

The U.S. hypertrophic and keloid scar treatment market captured the largest revenue share in 2025 within North America, fueled by the high adoption of innovative scar treatment therapies, proactive dermatological care programs, and growing awareness among patients and healthcare providers regarding effective scar management solutions.

Europe Hypertrophic and Keloid Scar Treatment Market Insight

The Europe hypertrophic and keloid scar treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing prevalence of skin injuries, well-established healthcare infrastructure, and the adoption of advanced dermatological therapies in countries such as Germany, France, and the U.K.

U.K. Hypertrophic and Keloid Scar Treatment Market Insight

The U.K. hypertrophic and keloid scar treatment market is expected to grow at a noteworthy CAGR during the forecast period, supported by rising awareness of scar management treatments, government healthcare initiatives, and increasing demand for patient-centric dermatological solutions.

Germany Hypertrophic and Keloid Scar Treatment Market Insight

The German hypertrophic and keloid scar treatment market is expected to witness significant growth over the forecast period, driven by the country’s high healthcare expenditure and a strong focus on innovation in dermatology treatments. The increasing adoption of advanced scar management therapies across both hospital and outpatient care settings is further fueling market expansion. Germany’s well-established healthcare infrastructure and growing patient awareness regarding effective scar care are also contributing to the market’s positive trajectory.

Asia-Pacific Hypertrophic and Keloid Scar Treatment Market Insight

The Asia-Pacific hypertrophic and keloid scar treatment market is projected to experience the fastest growth between 2026 and 2033. This growth is primarily supported by the rising prevalence of skin injuries, expanding healthcare infrastructure, and improved access to advanced dermatological treatment facilities. Countries such as China, India, and Japan are witnessing a surge in demand for innovative scar treatment solutions, driven by increasing healthcare awareness, growing urban populations, and investments in modern healthcare technologies.

Japan Hypertrophic and Keloid Scar Treatment Market Insight

Japan’s hypertrophic and keloid scar treatment market is showing notable momentum due to the country’s aging population and the rising incidence of skin injuries. The increasing adoption of innovative scar management therapies in both hospital and home care settings is a key driver of market growth. In addition, the focus on patient-centric dermatological solutions and the integration of advanced treatment methods are contributing to the steady expansion of the market.

China Hypertrophic and Keloid Scar Treatment Market Insight

China hypertrophic and keloid scar treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, increasing prevalence of skin injuries, rising healthcare awareness, and the availability of advanced and affordable scar treatment therapies, supported by strong domestic pharmaceutical and skincare manufacturers.

Hypertrophic and Keloid Scar Treatment Market Share

The Hypertrophic and Keloid Scar Treatment industry is primarily led by well-established companies, including:

• Smith & Nephew plc (U.K.)

• MediTox Inc. (South Korea)

• Beiersdorf AG (Germany)

• Hugel, Inc. (South Korea)

• Sanofi S.A. (France)

• Pfizer Inc. (U.S.)

• Lumenis Ltd. (Israel)

• Cynosure, Inc. (U.S.)

• L’Oreal S.A. (France)

• Medtronic plc (Ireland)

• Novartis AG (Switzerland)

• Johnson & Johnson (U.S.)

• GlaxoSmithKline plc (U.K.)

• BioScience GmbH (Germany)

• Asclepius Pharmaceuticals (U.S.)

• Derma Sciences Inc. (U.S.)

• Collagenex Pharmaceuticals (U.S.)

Latest Developments in Global Hypertrophic and Keloid Scar Treatment Market

- In September 2024, the KECORT study (an international e‑Delphi survey of dermatologists and plastic surgeons) reached expert consensus on how to use intralesional corticosteroids for keloids. Physicians agreed on using triamcinolone acetonide 40 mg/mL, with injections spaced every 4 weeks, and on specific needle sizes and injection techniques — helping standardize a first‑line treatment

- In March 2025, a clinical trial published in Lasers in Medical Science demonstrated that fractional CO₂ laser therapy, given in 5 monthly sessions, led to significant clinical and histological improvements in hypertrophic scars, with minimal side effects

- In May 2025, a randomized, double-blind study showed that combining ablative fractional CO₂ laser with topical triamcinolone acetonide cream produced a much greater reduction in scar volume (45.2%) compared to laser + placebo (28.7%) at 6 months, along with better patient-reported outcomes for pain and itching

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.