Global Infantile Systemic Hyalinosis Market

Market Size in USD Million

USD

340.42 Million

USD

448.26 Million

2024

2032

USD

340.42 Million

USD

448.26 Million

2024

2032

| 2025 - 2032 | |

| USD 340.42 Million | |

| USD 448.26 Million | |

| % | |

|

Infantile Systemic Hyalinosis Market Size

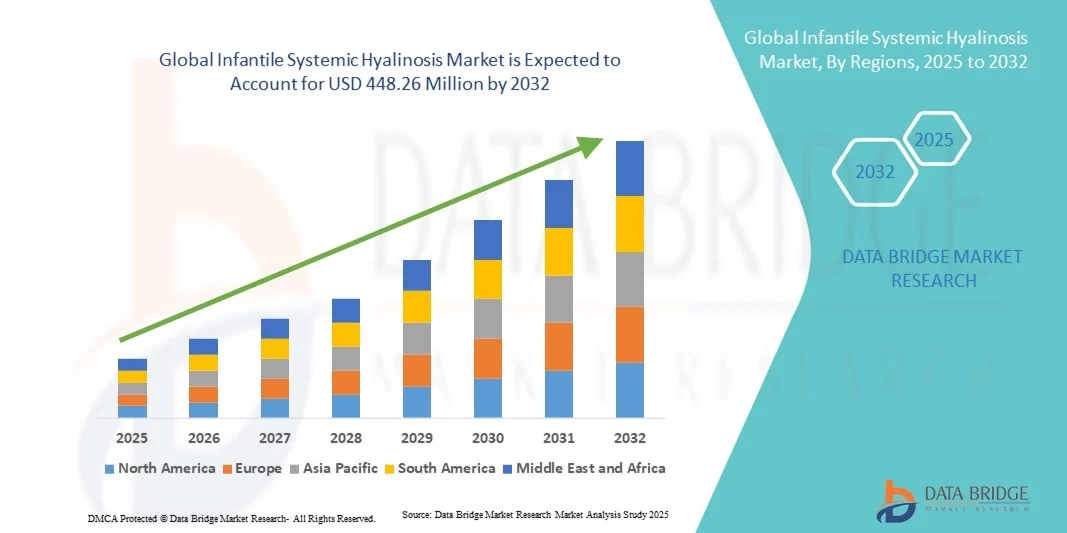

- The global infantile systemic hyalinosis market size was valued at USD 340.42 million in 2024 and is expected to reach USD 448.26 million by 2032, at a CAGR of 3.50% during the forecast period

- The market growth is largely driven by increasing research efforts focused on understanding rare genetic disorders and developing targeted therapies for early diagnosis and management of infantile systemic hyalinosis

- Furthermore, rising awareness among healthcare professionals, improved genetic testing capabilities, and growing government support for orphan disease research are fostering advancements in treatment options. These combined factors are accelerating clinical progress and market expansion, thereby significantly enhancing the industry’s growth trajectory

Infantile Systemic Hyalinosis Market Analysis

- Infantile systemic hyalinosis, a rare and severe genetic disorder marked by widespread deposition of hyaline material in connective tissues, is receiving growing clinical focus due to its complex pathology and significant unmet medical needs in pediatric care

- The rising demand for effective treatment options is primarily driven by advancements in genetic research, improved diagnostic accuracy, and increasing awareness among healthcare professionals and families regarding early detection and supportive management of rare disorders

- North America dominated the infantile systemic hyalinosis market with the largest revenue share of 41.5% in 2024, owing to the presence of advanced diagnostic facilities, well-established healthcare infrastructure, and strong initiatives for rare disease research, with the U.S. leading in clinical studies and patient registries

- Asia-Pacific is expected to be the fastest-growing region in the infantile systemic hyalinosis market during the forecast period due to improving healthcare accessibility, rising government funding for rare disease programs, and growing collaborations between regional hospitals and international research organizations

- The drugs segment dominated the market with a share of 45.9% in 2024, driven by the increasing focus on developing symptomatic and supportive pharmacological treatments aimed at pain management, inflammation control, and improving the quality of life in affected infants

Report Scope and Infantile Systemic Hyalinosis Market Segmentation

|

Attributes |

Infantile Systemic Hyalinosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Infantile Systemic Hyalinosis Market Trends

Advancements in Genetic Research and Early Diagnostic Technologies

- A significant and accelerating trend in the global infantile systemic hyalinosis market is the growing integration of advanced genetic research and next-generation sequencing (NGS) technologies for earlier and more accurate diagnosis of the disease. This evolution is enhancing the ability of clinicians to identify and manage cases at a much earlier stage

- For instance, recent adoption of whole-exome sequencing in pediatric genetic screening has enabled the identification of ANTXR2 gene mutations responsible for infantile systemic hyalinosis, allowing for earlier clinical intervention and counseling. Similarly, hospitals in the U.S. and Europe are increasingly offering targeted rare disease panels as part of neonatal screening programs

- The integration of molecular diagnostics with digital pathology and bioinformatics platforms allows for improved data interpretation, personalized care, and long-term disease monitoring. For instance, research collaborations between genetic laboratories and rare disease centers are advancing precision medicine approaches aimed at understanding disease mechanisms and identifying potential therapeutic targets

- Furthermore, partnerships between biotechnology firms and academic institutions are promoting data-sharing frameworks and rare disease registries that enhance global disease tracking and research efficiency. These developments are contributing to a more data-driven and coordinated approach to managing rare pediatric genetic disorders

- This trend toward advanced molecular diagnostics and global collaboration is reshaping the landscape of rare disease research. Consequently, several biotech startups are focusing on developing gene-based and RNA-targeted therapies aimed at addressing the underlying pathology of infantile systemic hyalinosis

- The demand for early genetic testing, personalized care, and advanced molecular diagnostics is rapidly growing across pediatric hospitals and genetic research centers, as healthcare systems increasingly prioritize early intervention and targeted therapy for rare disorders

Infantile Systemic Hyalinosis Market Dynamics

Driver

Rising Research Initiatives and Growing Awareness of Rare Genetic Disorders

- The increasing number of research programs focused on understanding rare pediatric disorders, coupled with enhanced awareness and advocacy for genetic disease management, is a major driver for the infantile systemic hyalinosis market

- For instance, in February 2024, several rare disease foundations launched global research collaborations to advance genetic testing and establish patient registries for disorders such as infantile systemic hyalinosis. Such coordinated efforts are expected to accelerate diagnosis and therapy development

- As awareness campaigns expand and families seek earlier diagnosis through advanced genetic screening, the demand for specialized care and supportive treatments continues to grow. This heightened focus on early intervention and personalized medicine is driving sustained market interest

- Furthermore, the expansion of healthcare infrastructure and increased availability of rare disease testing in hospitals and specialty clinics are enhancing diagnostic reach across both developed and emerging economies

- The growing number of clinical trials, orphan drug designations, and partnerships between pharmaceutical companies and research organizations are creating new opportunities for therapeutic innovation in this rare disorder space

- The ongoing collaboration between government agencies, non-profits, and research networks is further supporting early-stage discovery, funding, and awareness initiatives that fuel overall market growth

Restraint/Challenge

Limited Therapeutic Options and High Diagnostic Complexity

- The lack of approved, disease-specific therapies and the clinical complexity of diagnosing infantile systemic hyalinosis pose significant challenges to effective management and broader treatment access

- For instance, many cases remain undiagnosed or misdiagnosed due to overlapping symptoms with other connective tissue disorders, delaying appropriate clinical intervention and care strategies

- Addressing these diagnostic challenges through widespread availability of genetic testing, standardization of clinical guidelines, and improved clinician education is essential for better patient outcomes

- In addition, the extremely small patient population and high costs associated with drug development for rare diseases limit commercial incentives for pharmaceutical companies to invest in targeted therapies

- The absence of curative treatments and the reliance on symptomatic management further restrict long-term improvements in patient quality of life, underscoring the need for gene-based or molecularly targeted interventions

- Overcoming these challenges through global data sharing, rare disease funding initiatives, and broader clinical research participation will be vital for accelerating progress in this market

Infantile Systemic Hyalinosis Market Scope

The market is segmented on the basis of symptoms, treatment, mode of administration, distribution channel, and end user.

- By Symptoms

On the basis of symptoms, the infantile systemic hyalinosis market is segmented into purplish patches develop over the medial and lateral malleoli of the ankles, the metacarpophalangeal joints, progressive joint contractures, osteopenia, skin abnormalities, chronic severe pain, and widespread deposition of hyaline material in tissues. The widespread deposition of hyaline material in tissues segment dominated the market in 2024, owing to its defining role in the pathogenesis of infantile systemic hyalinosis and its critical impact on diagnosis and treatment planning. This systemic symptom is often the first clinical indication leading to genetic testing for ANTXR2 mutations, making it central to disease identification. The widespread involvement of connective tissues affects multiple organs and skeletal systems, necessitating comprehensive and multidisciplinary care approaches. Its prevalence across nearly all diagnosed cases highlights its importance as a primary diagnostic and therapeutic focus. Continuous research efforts into the molecular mechanisms driving hyaline deposition are also fueling demand for targeted therapies.

The progressive joint contractures segment is anticipated to witness the fastest growth rate from 2025 to 2032 due to the increasing focus on early orthopedic and physical therapy interventions. These contractures severely limit mobility and quality of life, prompting higher demand for multidisciplinary treatment plans. Advances in rehabilitative techniques, surgical interventions, and supportive therapies for managing joint deformities are contributing to the segment’s expansion. In addition, growing clinical awareness and documentation of contracture progression in rare disease registries are supporting earlier detection and management, driving the segment’s growth potential.

- By Treatment

On the basis of treatment, the market is segmented into surgery and drugs. The drugs segment dominated the market in 2024 with the largest revenue share of 45.9%, primarily due to the reliance on pharmacological interventions for pain management, inflammation reduction, and supportive symptom control. As there is currently no curative therapy, drug-based management remains the mainstay of treatment. Increased adoption of anti-inflammatory and analgesic medications, along with advancements in drug formulations for pediatric care, are driving market growth. Pharmaceutical companies are also exploring potential orphan drug candidates and repurposed molecules for this condition, further supporting segment dominance.

The surgery segment is expected to register the fastest growth from 2025 to 2032 due to the increasing number of corrective and supportive surgical interventions aimed at alleviating complications such as contractures and gastrointestinal involvement. Surgical treatments, though palliative, are becoming more refined with improved post-operative outcomes. The rise in specialized pediatric surgical centers and the adoption of minimally invasive techniques are also contributing to this segment’s rapid growth. Moreover, growing awareness among caregivers and clinicians about the role of surgery in improving functional mobility is supporting this trend.

- By Mode of Administration

On the basis of mode of administration, the market is segmented into injectables, oral, and others. The injectables segment dominated the market in 2024, supported by the high efficacy and rapid onset of action associated with injectable therapies used for pain and inflammation management. Hospital-based treatments for severe cases often rely on injectables for symptom stabilization, especially in acute disease manifestations. Injectable biologics and corticosteroids are frequently used to control inflammation and tissue degeneration. The strong presence of this route in hospital and clinical settings ensures reliable dosing and monitoring, contributing to its leading position.

The oral segment is projected to be the fastest growing from 2025 to 2032, driven by increasing research into oral formulations that enhance patient compliance, especially in home-based management settings. As families seek easier administration routes for chronic symptom relief, demand for pediatric-appropriate oral drugs is rising. Pharmaceutical innovation in liquid suspensions and orally disintegrating tablets for rare pediatric disorders is further propelling growth. The segment also benefits from ongoing R&D aimed at developing safe, effective long-term oral therapeutics for symptom modulation.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment dominated the market in 2024, driven by the concentration of infantile systemic hyalinosis treatment within specialized hospital settings. Since most patients require close clinical supervision and regular treatment adjustments, hospital pharmacies play a key role in supplying and managing prescribed medications. The increasing establishment of rare disease units and partnerships between hospitals and pharmaceutical manufacturers ensure consistent drug availability. Moreover, the use of injectables and other hospital-administered treatments reinforces hospital pharmacies’ leading market share.

The online pharmacies segment is expected to grow at the fastest rate during 2025–2032, owing to the expanding digitalization of healthcare and growing accessibility of rare disease drugs via regulated e-pharmacy platforms. Online channels offer convenience, privacy, and accessibility, particularly for families managing chronic care from remote areas. Increasing government approval for e-pharmacy models, coupled with partnerships between specialty distributors and digital health platforms, is supporting this growth. Moreover, the adoption of subscription-based delivery for maintenance medications is enhancing patient adherence and fueling market expansion.

- By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market in 2024, attributed to the critical need for multidisciplinary treatment involving geneticists, pediatricians, surgeons, and pain specialists. Hospitals remain the primary point of diagnosis and comprehensive management for this complex condition. The availability of advanced diagnostic tools, specialized laboratories, and integrated care units supports the segment’s leadership. Furthermore, clinical research conducted within hospital settings contributes significantly to understanding disease progression and therapeutic outcomes.

The homecare segment is projected to witness the fastest growth from 2025 to 2032, fueled by the rising emphasis on long-term symptom management and patient comfort outside clinical environments. Home-based care offers continuous pain management, physiotherapy, and nutritional support, reducing hospital dependency. Increasing caregiver training programs and the availability of telehealth consultations for rare disease patients are further driving this segment’s expansion. In addition, advancements in portable monitoring devices and at-home drug delivery solutions enhance the feasibility of effective homecare management for affected infants.

Infantile Systemic Hyalinosis Market Regional Analysis

- North America dominated the infantile systemic hyalinosis market with the largest revenue share of 41.5% in 2024, owing to the presence of advanced diagnostic facilities, well-established healthcare infrastructure, and strong initiatives for rare disease research, with the U.S. leading in clinical studies and patient registries

- Healthcare providers and families in the region increasingly rely on early genetic screening, precision medicine, and multidisciplinary treatment programs for improved management of this rare pediatric disorder

- This regional dominance is further supported by active participation of research institutions, patient advocacy groups, and biotech firms engaged in orphan drug development, establishing North America as the leading hub for diagnosis, clinical trials, and therapeutic innovation in infantile systemic hyalinosis

U.S. Infantile Systemic Hyalinosis Market Insight

The U.S. infantile systemic hyalinosis market captured the largest revenue share of 82% in 2024 within North America, driven by the presence of advanced genetic testing infrastructure and high investment in rare disease research. The country’s strong network of specialized pediatric hospitals and genomic laboratories supports early diagnosis and clinical management of this rare condition. The growing emphasis on precision medicine, supported by government programs and orphan drug incentives, is further fueling research and therapeutic development. Moreover, increasing awareness among clinicians and families about early intervention and genetic counseling is contributing significantly to market growth.

Europe Infantile Systemic Hyalinosis Market Insight

The Europe infantile systemic hyalinosis market is projected to expand at a substantial CAGR throughout the forecast period, fueled by robust healthcare policies supporting rare disease diagnosis and treatment. Rising adoption of next-generation sequencing (NGS) technologies and growing collaboration between academic institutions and biotechnology firms are advancing early detection and research initiatives. The increasing number of clinical trials and government-backed orphan disease frameworks, such as those under the European Medicines Agency (EMA), are also driving market expansion. The market is witnessing strong demand for genetic counseling services and specialized care facilities across leading European countries.

U.K. Infantile Systemic Hyalinosis Market Insight

The U.K. infantile systemic hyalinosis market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by expanding government initiatives for rare disease awareness and research funding. The presence of leading genetic research centers, such as Genomics England, facilitates advanced diagnostic studies and patient registries. Increasing public awareness and access to specialized pediatric genetics services are driving earlier identification and management of the condition. Furthermore, collaborations between the National Health Service (NHS) and rare disease foundations are enhancing patient support programs, thereby accelerating market growth across the country.

Germany Infantile Systemic Hyalinosis Market Insight

The Germany infantile systemic hyalinosis market is expected to expand at a considerable CAGR during the forecast period, attributed to the country’s strong biomedical research infrastructure and early adoption of advanced diagnostic tools. Germany’s focus on precision medicine and genetic testing integration within public healthcare systems has enhanced detection rates for rare disorders. The country’s commitment to rare disease policy frameworks and ongoing participation in EU-funded research consortia further drive clinical progress. In addition, increasing collaboration between hospitals, universities, and pharmaceutical firms supports innovation in gene-based and symptomatic therapies.

Asia-Pacific Infantile Systemic Hyalinosis Market Insight

The Asia-Pacific infantile systemic hyalinosis market is poised to grow at the fastest CAGR of 23.5% during the forecast period of 2025 to 2032, driven by growing healthcare investment, expanding awareness of rare genetic disorders, and improved diagnostic capabilities in countries such as China, Japan, and India. The region’s adoption of molecular testing and government-led healthcare digitalization programs is enhancing early detection. Moreover, the emergence of regional research collaborations and affordable testing kits is expanding accessibility to rare disease diagnosis and care. Increasing pediatric healthcare spending and integration of genetic counseling services are further propelling market growth.

Japan Infantile Systemic Hyalinosis Market Insight

The Japan infantile systemic hyalinosis market is gaining momentum due to the country’s advanced genomics research infrastructure and focus on early genetic screening. Japan’s highly developed healthcare system emphasizes innovation in rare disease diagnostics and therapeutic development. The growing application of next-generation sequencing and the presence of specialized pediatric care institutions are accelerating the identification of cases. Furthermore, collaborations between academic research institutes and biotech firms are fostering innovation in gene-based therapies. Rising government initiatives aimed at strengthening rare disease registries are also supporting sustained market growth.

India Infantile Systemic Hyalinosis Market Insight

The India infantile systemic hyalinosis market accounted for the largest market revenue share in Asia Pacific in 2024, driven by expanding healthcare accessibility, rising awareness of rare disorders, and an increasing focus on pediatric genetic testing. India’s rapid advancement in genomic research and the availability of cost-effective diagnostic services are strengthening early detection capabilities. Growing partnerships between government health agencies, hospitals, and private research organizations are promoting the establishment of national rare disease programs. In addition, increasing investment in child healthcare and a growing number of clinical collaborations are expected to further boost market development in the country.

Infantile Systemic Hyalinosis Market Share

The Infantile Systemic Hyalinosis industry is primarily led by well-established companies, including:

- BioMarin (U.S.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Amicus Therapeutics, Inc. (U.S.)

- Sarepta Therapeutics, Inc. (U.S.)

- Krystal Biotech, Inc. (U.S.)

- AVITA Medical, Inc. (U.S.)

- Castle Creek Biosciences, Inc. (U.S.)

- Bio-Techne (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GeneDx, LLC (U.S.)

- Blueprint Genetics Oy (Finland)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Vertex, Inc. (U.S.)

- Moderna, Inc. (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Fulgent Genetics (U.S.)

What are the Recent Developments in Global Infantile Systemic Hyalinosis Market?

- In September 2025, an Oxford Medical Case Reports paper described a 6-month-old infant with ISH whose diagnosis was confirmed by a homozygous ANTXR2 (CMG2) mutation, highlighting ongoing use of trio/exome sequencing to secure early, definitive diagnoses and reinforce the link between clinical presentation and ANTXR2 pathogenic variants. The report emphasizes multidisciplinary management and genetic counselling as central to care

- In March 2024, researchers published a computational genetics study analyzing ANTXR2 (CMG2) single-nucleotide variants and identified deleterious and tolerated nsSNPs that alter receptor function work that expands molecular understanding of ANTXR2, suggests candidate variants for further functional testing, and may inform future biomarker or therapeutic-strategy research

- In August 2022, a Molecular Genetics & Genomic Medicine article reported a novel 4.41-kb gross deletion in ANTXR2 (compound heterozygosity) in a patient with the severe ISH phenotype, and reviewed >100 cases to strengthen genotype–phenotype correlations. This paper enlarged the mutation spectrum and noted instances where IVIG or supportive interventions correlated with clinical improvement

- In November 2021, a Journal of Pediatric Genetics (Thieme) study of six infants with ISH presenting as “pseudo-paralysis” reported clinical series data, confirmed pathogenic ANTXR2 variants in cases, and emphasized how genetic diagnosis enabled prenatal counselling and avoided unnecessary investigations calling attention to diagnostic patterns in consanguineous populations

- In July 2021, a short case note in Congenital Anomalies described a novel ANTXR2 variant from India, adding to the geographic and mutational diversity of reported ANTXR2 lesions and reinforcing the importance of reporting new variants to build global mutation databases that support diagnosis, counselling, and research

- https://pubmed.ncbi.nlm.nih.gov/40979812/

- https://www.mdpi.com/2073-4425/15/4/426

- https://pubmed.ncbi.nlm.nih.gov/35726349/

- https://www.thieme-connect.com/products/ejournals/abstract/10.1055/s-0041-1736558

- https://pubmed.ncbi.nlm.nih.gov/33724566/?

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.