Global Infrastructure As A Service Iaas Health Cloud Market

Market Size in USD Billion

USD

65.01 Billion

USD

229.84 Billion

2025

2033

USD

65.01 Billion

USD

229.84 Billion

2025

2033

| 2026 - 2033 | |

| USD 65.01 Billion | |

| USD 229.84 Billion | |

| % | |

|

What is the Global Infrastructure as a Service (IaaS) Health Cloud Market Size and Growth Rate?

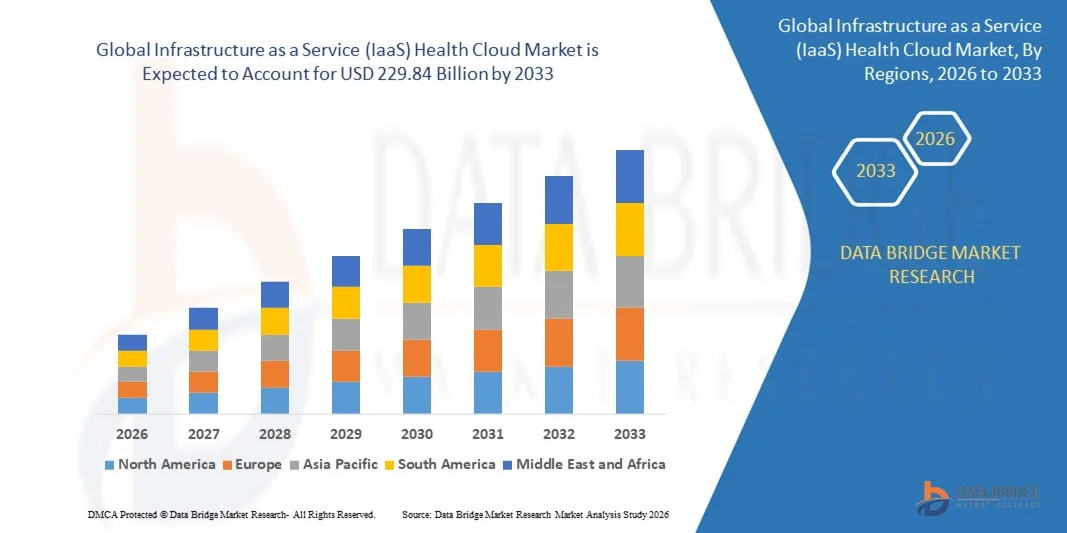

- The global infrastructure as a service (IaaS) health cloud market size was valued at USD 65.01 billion in 2025 and is expected to reach USD 229.84 billion by 2033, at a CAGR of17.10% during the forecast period

- Increasing proliferation of data centre colocation facilities across the globe, availability of low-cost rack solutions, increasing adoption of data centre solutions that enables easy and efficient management of data centre networks, rising usages of the solutions to support various servers in a secure environment along with increasing server density are some of the major as well as vital factors which will likely to augment the growth of the infrastructure as a service (IaaS) health cloud market

What are the Major Takeaways of Infrastructure as a Service (IaaS) Health Cloud Market?

- Increasing usages of blockchain in the health cloud, emergence of the telecloud, formation of accountable care organizations along with bridging the connectivity and accessibility gap which will further contribute by generating massive opportunities that will lead to the growth of the infrastructure as a service (IaaS) health cloud market in the above mentioned projected timeframe

- Increasing concern of data security and privacy along with complex regulations governing cloud data centers which will likely to act as market restraints factor for the growth of the infrastructure as a service (IaaS) health cloud in the above mentioned projected timeframe. Lack of technical expertise along with interoperability and portability issues which will become the biggest and foremost challenge for the growth of the market

- North America dominated the Infrastructure as a Service (IaaS) Health Cloud market with a 39.59% revenue share in 2025, driven by rapid adoption of cloud-based healthcare platforms, hyperscale data centres, edge computing deployment, and rising investment in high-density IT infrastructure across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 7.69% from 2026 to 2033, driven by rapid digitalization of hospitals and payer services, expansion of cloud-based health solutions, 5G network rollouts, and large-scale investments in healthcare data centers across China, Japan, India, Singapore, and South Korea

- The Healthcare Provider Solutions segment dominated the market with a 61.5% revenue share in 2025, driven by rising demand for electronic health records (EHRs), telemedicine platforms, patient management systems, and AI-powered diagnostic tools

Report Scope and Infrastructure as a Service (IaaS) Health Cloud Market Segmentation

|

Attributes |

Infrastructure as a Service (IaaS) Health Cloud Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Infrastructure as a Service (IaaS) Health Cloud Market?

Growing Adoption of AI-Optimized, Scalable, and Automation-Driven Health Cloud Infrastructure

- The Infrastructure as a Service (IaaS) Health Cloud market is witnessing increasing adoption of AI-optimized, scalable, and automation-ready cloud architectures designed to support clinical workloads, electronic health records (EHRs), medical imaging, and high-performance analytics

- Cloud providers are introducing self-healing, auto-scaling, and high-availability frameworks that improve data handling, enhance interoperability, and streamline deployment of healthcare applications across hybrid and multi-cloud environments

- Rising demand for cost-efficient, compliant, and secure health cloud systems is driving adoption across hospitals, diagnostic centers, telehealth platforms, and insurance networks

- For instance, Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM Cloud, and Oracle expanded healthcare-focused cloud portfolios with improved compliance tools, AI-driven analytics, and advanced automation capabilities

- Growing need for real-time data processing, improved clinical workflow automation, and integrated patient data management is accelerating adoption of advanced IaaS health cloud solutions

- As healthcare systems transition toward digitized, AI-enabled, and interoperable infrastructures, IaaS Health Cloud platforms are expected to remain central to modernization, scalability, and secure data exchange

What are the Key Drivers of Infrastructure as a Service (IaaS) Health Cloud Market?

- Rising demand for cost-effective, secure, and scalable cloud resources to support healthcare analytics, EHR storage, imaging workflows, telemedicine, and patient management systems

- For instance, in 2025, Microsoft, Google, and IBM enhanced their health cloud offerings to support AI-driven diagnostics, virtual care applications, and compliant data environments

- Rapid global expansion of digital health ecosystems, telehealth services, e-prescription platforms, and remote monitoring systems is boosting adoption across the U.S., Europe, and Asia-Pacific

- Advancements in data encryption, zero-trust security, container orchestration, and cloud-native technologies have improved reliability, interoperability, and performance of IaaS solutions

- Rising adoption of AI, IoT medical devices, 5G-enabled healthcare, and advanced analytics is driving demand for resilient cloud infrastructure with high compute capacity

- With strong investments in health IT modernization, cybersecurity, cloud-native applications, and global partnerships, the IaaS Health Cloud market is expected to maintain robust long-term growth

Which Factor is Challenging the Growth of the Infrastructure as a Service (IaaS) Health Cloud Market?

- High implementation costs associated with premium cloud infrastructure, compliant data storage systems, and advanced cybersecurity frameworks limit adoption among small and mid-sized healthcare facilities

- For instance, during 2024–2025, rising cloud security expenses, data migration complexities, and compliance-related requirements increased operational costs for healthcare providers

- Stringent health data protection regulations, including HIPAA, GDPR, and regional compliance mandates, add complexity to cloud deployment and maintenance

- Limited awareness and technical expertise in emerging markets regarding cloud governance, data integration, and multi-cloud orchestration restrict optimal implementation

- Strong competition from on-premises health IT systems, hybrid infrastructures, and vendor-specific managed services creates pressure on pricing, differentiation, and customization

- To overcome these challenges, companies are focusing on cost-optimized cloud models, enhanced security frameworks, regulatory compliance, and training programs to support widespread adoption of IaaS Health Cloud platforms

How is the Infrastructure as a Service (IaaS) Health Cloud Market Segmented?

The market is segmented on the basis of product, component, deployment model, pricing model, and end user.

- By Product Type

On the basis of product type, the Infrastructure as a Service (IaaS) Health Cloud market is segmented into Healthcare Provider Solutions and Healthcare Payer Solutions. The Healthcare Provider Solutions segment dominated the market with a 61.5% revenue share in 2025, driven by rising demand for electronic health records (EHRs), telemedicine platforms, patient management systems, and AI-powered diagnostic tools. Hospitals, diagnostic centers, and ambulatory care facilities increasingly deploy provider-focused cloud solutions to streamline operations, improve patient outcomes, and ensure regulatory compliance. The Healthcare Payer Solutions segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing adoption of cloud-based insurance claims processing, fraud detection systems, premium management, and analytics platforms. Payers are leveraging secure cloud infrastructure to improve efficiency, reduce operational costs, and enable predictive modeling for patient care and reimbursement strategies. Rising emphasis on interoperability, compliance, and data-driven healthcare continues to drive growth.

- By Component

On the basis of component, the market is segmented into Services and Software. The Software segment dominated the market with a 64.2% revenue share in 2025, owing to widespread adoption of cloud-native applications for EHR management, AI analytics, clinical workflow automation, and healthcare interoperability. Healthcare providers and payers are leveraging advanced software tools for secure data storage, compliance with HIPAA and GDPR, and integration with IoT medical devices. The Services segment is projected to register the fastest CAGR from 2026 to 2033, supported by growing demand for implementation, integration, migration, cloud maintenance, and lifecycle management services. Increasing complexity in hybrid cloud deployments, multi-cloud environments, and AI-driven healthcare workloads is driving demand for consulting, managed services, and professional support globally.

- By Deployment Model

On the basis of deployment model, the market is segmented into Private Cloud, Hybrid Cloud, and Public Cloud. The Hybrid Cloud segment dominated the market with a 52.8% share in 2025, as it offers healthcare organizations flexibility to combine secure on-premises infrastructure with scalable public cloud resources. Hybrid models support sensitive patient data storage, high-performance computing for AI diagnostics, and compliance with data privacy regulations. The Public Cloud segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rapid adoption among small to mid-sized hospitals, telehealth providers, and payer organizations seeking cost-efficient, scalable, and globally accessible infrastructure. Cloud providers are expanding region-specific offerings and compliance-enabled solutions, accelerating adoption across healthcare systems.

- By Pricing Model

On the basis of pricing model, the market is segmented into Pay-As-You-Go and Spot Pricing. The Pay-As-You-Go pricing model dominated the market with a 59.4% revenue share in 2025, driven by healthcare providers’ preference for flexible, operational expenditure-based billing that scales with patient volume, compute needs, and cloud usage. The Spot Pricing model is projected to grow at the fastest CAGR from 2026 to 2033, supported by increasing demand from data-intensive healthcare workloads, AI training, and analytics applications that require temporary burst capacity at optimized costs. Rising emphasis on cost efficiency, resource optimization, and scalable healthcare IT infrastructure is fueling adoption of dynamic cloud pricing models.

- By End User

On the basis of end user, the market is segmented into Hospitals, Pharmacies, Diagnostic and Imaging Centers, Ambulatory Centers, Private Payers, and Public Payers. The Hospitals segment dominated the market with a 48.7% revenue share in 2025, driven by large-scale adoption of cloud infrastructure for EHRs, telemedicine, AI diagnostics, and patient management. The Private Payers segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by increasing adoption of cloud platforms for claims processing, predictive analytics, fraud detection, and population health management. Rising investments in cloud-enabled digital transformation initiatives, secure patient data exchange, and AI-powered healthcare solutions continue to accelerate adoption across all end-user categories.

Which Region Holds the Largest Share of the Infrastructure as a Service (IaaS) Health Cloud Market?

- North America dominated the Infrastructure as a Service (IaaS) Health Cloud market with a 39.59% revenue share in 2025, driven by rapid adoption of cloud-based healthcare platforms, hyperscale data centres, edge computing deployment, and rising investment in high-density IT infrastructure across the U.S. and Canada. Strong adoption of AI-powered healthcare workloads, multi-cloud architectures, and digital transformation programs continues to boost cloud service consumption across hospitals, payer organizations, and diagnostic centers

- Leading cloud providers and rack solution vendors are expanding portfolios with innovations in energy-efficient architecture, modular assembly, airflow optimization, and compatibility with AI/GPU workloads. Regulatory emphasis on healthcare data security, HIPAA compliance, and green IT infrastructure further strengthens regional leadership

- High IT spending, large-scale hospital digitalization, and ongoing modernization of healthcare networks continue to fuel long-term growth

U.S. Infrastructure as a Service (IaaS) Health Cloud Market Insight

The U.S. is the largest contributor in North America, supported by extensive cloud adoption across hospitals, diagnostic centers, and payer organizations. Investments in AI-enabled health analytics, telemedicine, and edge data centers are driving adoption of high-density, modular cloud infrastructure due to superior scalability, security, and operational efficiency. Advanced healthcare IT standards, regulatory frameworks, and digital service expansion further strengthen market growth.

Canada Infrastructure as a Service (IaaS) Health Cloud Market Insight

Canada contributes significantly to regional growth, led by government-backed digital health programs, expansion of colocation and cloud facilities, and rising adoption of secure, cloud-based healthcare solutions. Healthcare providers are increasingly deploying modular, energy-efficient IT infrastructure to improve patient care, optimize operational costs, and support AI-driven analytics.

Asia-Pacific Infrastructure as a Service (IaaS) Health Cloud Market

Asia-Pacific is projected to register the fastest CAGR of 7.69% from 2026 to 2033, driven by rapid digitalization of hospitals and payer services, expansion of cloud-based health solutions, 5G network rollouts, and large-scale investments in healthcare data centers across China, Japan, India, Singapore, and South Korea. Rising demand for scalable, secure, and cost-efficient cloud infrastructure is accelerating adoption across hospitals, diagnostic centers, and payer networks. Growth in e-health, telemedicine, AI-assisted diagnostics, and digital payment integration further boosts regional adoption.

China Infrastructure as a Service (IaaS) Health Cloud Market Insight

China is the largest contributor in Asia-Pacific, supported by the fastest-growing cloud-based healthcare ecosystem, government-backed digital health initiatives, and large-scale investments in hyperscale cloud infrastructure. Rising adoption of AI-driven medical analytics, high-density server racks, and advanced cooling and network technologies fuels strong demand for scalable, secure cloud solutions.

Japan Infrastructure as a Service (IaaS) Health Cloud Market Insight

Japan shows steady growth due to rising demand for low-latency telemedicine, advanced hospital networks, and modernization of legacy healthcare IT systems. High focus on premium infrastructure, energy-efficient deployment, and compliance with healthcare regulations drives adoption of modular, scalable cloud solutions.

India Infrastructure as a Service (IaaS) Health Cloud Market Insight

India is emerging as a key growth hub, fueled by government cloud initiatives, expansion of hospitals and payer IT systems, and rising adoption of digital health solutions. Increasing deployment of telehealth, AI diagnostics, and edge facilities boosts demand for flexible, modular, and secure cloud infrastructure.

South Korea Infrastructure as a Service (IaaS) Health Cloud Market Insight

South Korea contributes significantly due to strong demand for AI-powered healthcare services, 5G-enabled telemedicine, and large-scale digital health platforms. Rising installation of high-performance computing systems and cloud-native healthcare applications drives adoption of scalable, energy-efficient, and secure cloud solutions.

Which are the Top Companies in Infrastructure as a Service (IaaS) Health Cloud Market?

The infrastructure as a service (IaaS) health cloud industry is primarily led by well-established companies, including:

- IBM Corporation (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- athenahealth, Inc. (U.S.)

- CareCloud Corporation (U.S.)

- Siemens Healthcare GmbH (Germany)

- eClinicalWorks (U.S.)

- Allscripts Healthcare, LLC (U.S.)

- NTT DATA, Inc. (Japan)

- Sectra AB (Sweden)

- GENERAL ELECTRIC COMPANY (U.S.)

- NXGN Management, LLC (U.S.)

- DXC Technology Company (U.S.)

- INFINITT North America Inc. (U.S.)

- Hyland Software, Inc. (U.S.)

- Orion Health group of companies (New Zealand)

- FUJIFILM Holdings America Corporation (U.S.)

- VEPRO AG (Switzerland)

- Dell Inc. (U.S.)

- ENSOFTEK INC (U.S.)

What are the Recent Developments in Global Infrastructure as a Service (IaaS) Health Cloud Market?

- In December 2023, ZKTeco announced a partnership with Amazon Web Services (AWS) to launch the innovative Minerva IoT platform and enhance its cloud capabilities, aiming to leverage AWS’s robust cloud infrastructure for developing a secure, scalable IoT platform with advanced functionalities, marking a significant step in strengthening IoT and cloud integration

- In November 2023, Leaseweb Global, a cloud services and Infrastructure as a Service (IaaS) provider, introduced a new channel partner program in the U.K., designed for managed service providers (MSPs) to build long-term sales partnerships and deliver strategic advice along with high-quality cloud services, further expanding its footprint in the European cloud market

- In December 2022, F5 launched Distributed Cloud App infrastructure protection, a solution enhancing application observability and security for cloud-native infrastructures, enabling enterprises to improve operational reliability and safeguard mission-critical workloads

- In October 2022, Lenovo announced upgrades to its Lenovo TruScale Infrastructure-as-a-Service technology solution deployed across enterprises, extending partnerships with Nutanix, Veeam, and Red Hat, providing enhanced on-premises safety, control, and hybrid cloud flexibility, and reinforcing customer adoption and trust

- In August 2022, 11:11 Systems, an infrastructure solution provider, acquired cloud management services from Sungard Availability Services to provide cross-platform cloud deployments with enhanced scalability, compliance, and availability, empowering clients to better manage, optimize, and secure mission-critical cloud environments, strengthening its enterprise cloud solutions portfolio

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.